Global Veterinary Artificial Insemination Market By Animal Type (Bovine, Porcine, Ovine, Caprine, Equine, Canine and Others), By Product Type (Semen, Equipment and Reagents and Kits), By End User (Veterinary Hospitals, Breeding Centers, Dairy Farms, Pig Farms, Poultry Farms and Others), Region and Companies – Industry Segment Outlook, Market Assessment, Competition Scenario, Trends and Forecast 2026-2035

- Published date: April 2026

- Report ID: 183674

- Number of Pages: 264

- Format:

-

keyboard_arrow_up

Quick Navigation

Report Overview

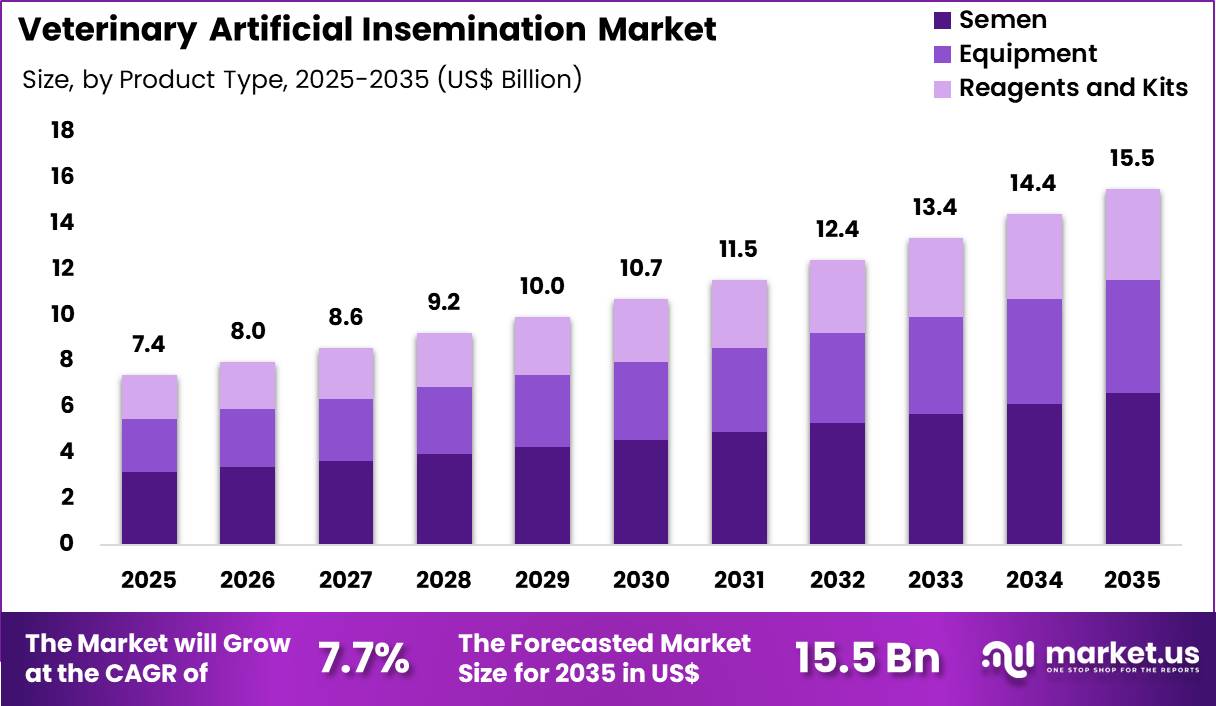

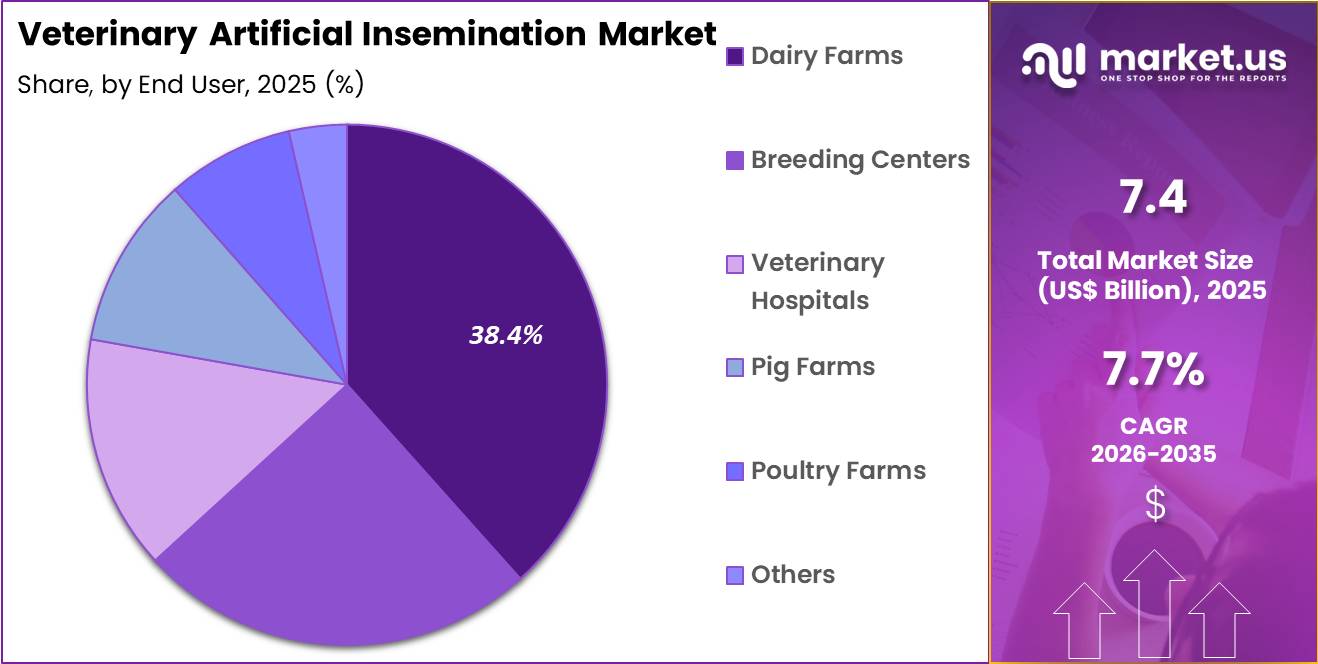

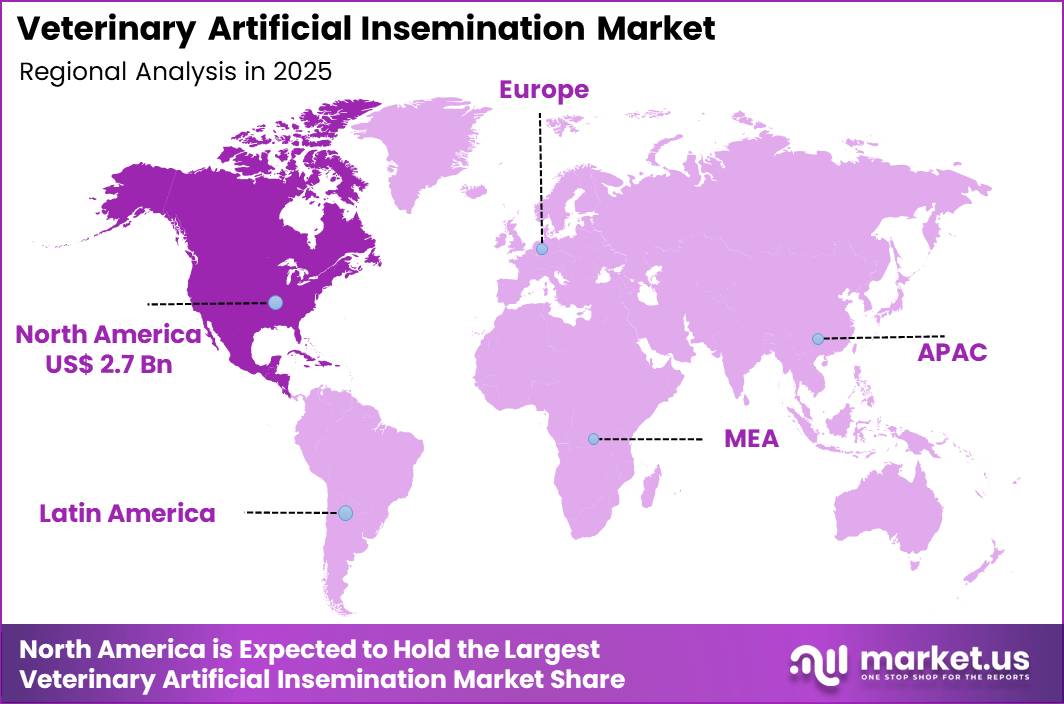

The Global Veterinary Artificial Insemination Market size is expected to be worth around US$ 15.5 Billion by 2035 from US$ 7.4 Billion in 2025, growing at a CAGR of 7.7% during the forecast period 2026-2035. In 2025, North America led the market, achieving over 35.8% share with a revenue of US$ 2.7 Billion.

Increasing focus on genetic improvement and reproductive efficiency in livestock production propels the Veterinary Artificial Insemination market as producers seek technologies that enhance conception rates, reduce disease transmission, and accelerate genetic progress across species.

Swine breeders increasingly implement artificial insemination programs using extended boar semen to introduce superior genetics into commercial herds, improving litter size, growth rate, and carcass quality while minimizing the biosecurity risks associated with live boar movement.

Dairy producers apply artificial insemination with sexed semen to generate replacement heifers, optimizing herd composition and milk production potential through precise genetic selection. Equine practitioners utilize fresh, chilled, or frozen semen for artificial insemination in performance horses, enabling access to elite stallions without physical transport and reducing injury risk during natural breeding.

In small ruminants, artificial insemination supports accelerated breeding programs in sheep and goats, allowing synchronization of estrus and out-of-season reproduction for improved lambing or kidding uniformity. Poultry and aquaculture operations also adopt artificial insemination techniques to maintain genetic lines and control reproduction in high-value breeding stock.

Manufacturers pursue opportunities to develop automated semen processing and insemination equipment that standardize dose preparation and delivery, expanding applications in medium- and large-scale operations where labor efficiency and consistency are critical. These advancements support integration with estrus detection technologies and ovulation synchronization protocols, improving timing accuracy and conception rates.

In February 2026, IMV Technologies launched the GTB 500, an automated system designed for filling and sealing porcine semen doses. The solution is specifically aimed at medium-scale breeding operations, helping standardize production processes and reduce reliance on manual labor. This innovation is expected to enhance dose consistency and overall quality, which are critical factors for achieving higher conception rates in commercial pig farming.

Recent trends emphasize precision breeding tools, sexed semen utilization, and data-driven reproductive management, positioning veterinary artificial insemination as a cornerstone of modern, efficient, and genetically progressive animal production systems.

Key Takeaways

- In 2025, the market generated a revenue of US$ 7.4 Billion, with a CAGR of 7.7%, and is expected to reach US$ 15.5 Billion by the year 2035.

- The animal type segment is divided into bovine, porcine, ovine, caprine, equine, canine and others, with bovine taking the lead with a market share of 58.4%.

- Considering product type, the market is divided into semen, equipment and reagents and kits. Among these, semen held a significant share of 42.7%.

- Furthermore, concerning the end user segment, the market is segregated into veterinary hospitals, breeding centers, dairy farms, pig farms, poultry farms and others. The dairy farms sector stands out as the dominant player, holding the largest revenue share of 38.4% in the market.

- North America led the market by securing a market share of 35.8%..

Animal Type Analysis

Bovine accounted for 58.4% of growth within animal type and dominate the veterinary artificial insemination market due to the strong demand for genetic improvement and productivity enhancement in cattle farming. Dairy and beef producers actively use artificial insemination to improve milk yield, fertility rates, and disease resistance in herds.

Global livestock data indicates that cattle farming remains one of the largest agricultural sectors, which supports consistent adoption of breeding technologies. Bovine artificial insemination is expected to expand as farmers focus on high-quality genetics and efficient herd management.

The segment benefits from established breeding programs and widespread availability of high-grade semen. Farmers are likely to adopt artificial insemination to reduce breeding risks and improve reproductive efficiency. Increasing demand for dairy products is projected to support further growth. As livestock productivity becomes a priority, bovine remains estimated to hold the dominant position in this market.

Product Type Analysis

Semen accounted for 42.7% of growth within product type and dominate the veterinary artificial insemination market due to its central role in the breeding process. High-quality semen determines genetic traits, reproductive success, and overall herd performance. Breeding programs rely heavily on selected semen from superior sires to enhance productivity and disease resistance.

The segment is expected to grow as demand for genetically superior livestock increases globally. Semen products are likely to see high repeat demand due to continuous breeding cycles. The segment benefits from advancements in cryopreservation and storage technologies that improve viability and transport efficiency.

Increasing adoption of selective breeding practices is projected to support market expansion. As genetic improvement remains a key focus in livestock farming, semen is anticipated to remain the leading product segment in this market.

End-User Analysis

Dairy farms accounted for 38.4% of growth within end user and dominate the veterinary artificial insemination market due to their reliance on efficient breeding practices to maximize milk production. Dairy farmers use artificial insemination to ensure consistent calving intervals and improve herd genetics.

Rising global demand for milk and dairy products drives the need for high-yield cattle, which supports adoption of advanced breeding techniques. Dairy farms are expected to expand their use of artificial insemination as they aim to improve productivity and profitability. The segment benefits from structured breeding programs and access to high-quality genetic material.

Farmers are likely to prefer artificial insemination over natural breeding due to better control and reduced disease transmission. As dairy production continues to grow worldwide, dairy farms are estimated to maintain their dominant position in the veterinary artificial insemination market.

Key Market Segments

By Animal Type

- Bovine

- Porcine

- Ovine

- Caprine

- Equine

- Canine

- Others

By Product Type

- Semen

- Equipment

- Reagents and Kits

By End User

- Veterinary Hospitals

- Breeding Centers

- Dairy Farms

- Pig Farms

- Poultry Farms

- Others

Drivers

Expansion of livestock production and genetic improvement programs is driving the Veterinary Artificial Insemination market.

The global emphasis on enhancing animal productivity has accelerated the utilization of artificial insemination techniques to propagate superior genetic traits in cattle, swine, and other species. Farmers and breeders increasingly employ this method to achieve higher milk yields, improved meat quality, and better disease resistance across herds.

In the United States, more than 60 percent of dairy cows are bred using artificial insemination, facilitating precise selection for traits such as milk production and overall herd health. Large-scale dairy and beef operations rely on this technology to optimize reproductive efficiency and reduce dependency on natural service bulls.

Rising global demand for animal protein further incentivizes investment in structured breeding initiatives that incorporate artificial insemination. Government-supported programs in various regions promote widespread adoption to elevate livestock standards and support sustainable agriculture.

The technique allows for controlled timing of insemination synchronized with estrus cycles, resulting in higher conception rates under managed conditions. Integration with sexed semen technologies enables producers to influence offspring gender ratios according to commercial needs.

These operational advantages contribute to consistent procedural volumes in both developed and emerging agricultural systems. Consequently, this focus on genetic advancement and productivity gains serves as a core driver sustaining market momentum during the 2022–2025 period.

Restraints

Shortage of skilled technicians and logistical challenges in remote areas are restraining the Veterinary Artificial Insemination market.

Adequate training and availability of qualified personnel remain critical bottlenecks that limit the effective delivery of artificial insemination services, particularly in dispersed farming communities. Conception failure rates continue to pose concerns, often linked to improper timing, semen handling, or technique execution, which discourages consistent adoption among producers.

In many regions, the unavailability of technicians during optimal heat detection windows leads to missed breeding opportunities and reduced overall success. Logistical difficulties associated with semen storage, transportation, and timely access in rural or underdeveloped zones exacerbate these issues.

Small and marginal farms face additional hurdles due to limited infrastructure and technical knowledge, resulting in lower utilization rates compared to larger commercial entities. These constraints contribute to variability in outcomes and erode confidence in the technology among certain user groups.

Administrative and scheduling interruptions further compound delays in service provision. Resource limitations in veterinary support networks slow the scaling of comprehensive programs. Persistent gaps in workforce capacity and support systems moderate the pace of broader implementation. As a result, such operational and human resource factors impose measurable restraint on accelerated market expansion throughout the 2022–2025 timeframe.

Opportunities

Advancements in sexed semen and cryopreservation technologies are creating growth opportunities in the Veterinary Artificial Insemination market.

Refinements in semen sorting and preservation methods have enhanced the precision and viability of insemination doses, enabling producers to achieve targeted breeding outcomes with greater reliability. Opportunities arise for expanded application in dairy herds where gender selection supports efficient replacement stock management and maximizes genetic progress.

nd shortens generation intervals. Commercial entities can develop customized solutions tailored to specific breeds or production systems, broadening accessibility across diverse livestock segments. Potential exists for combining artificial insemination with digital monitoring tools that improve heat detection accuracy and insemination timing.

These innovations reduce wastage and elevate conception rates, delivering clear economic returns to adopters. Collaboration between technology providers and agricultural organizations facilitates knowledge transfer and program scaling in emerging markets. Alignment with sustainability objectives encourages investment in efficient breeding practices that minimize resource use.

Overall, technological enhancements in semen processing unlock substantial prospects for diversified applications and sustained industry development.

Impact of Macroeconomic / Geopolitical Factors

Macroeconomic forces and geopolitical developments are playing a decisive role in shaping efficiency, cost dynamics, and global adoption patterns within the veterinary artificial insemination market. Rising demand for meat and dairy products is pushing farmers to adopt advanced breeding techniques that improve productivity and genetic quality, thereby strengthening market expansion.

At the same time, inflation is increasing the cost of semen processing, storage infrastructure, and veterinary services, which can strain margins for service providers and limit adoption among small-scale farmers. Currency fluctuations and trade uncertainties are also affecting the import of high-quality genetic material and specialized equipment used in insemination procedures.

Geopolitical tensions are disrupting cross-border semen distribution networks and delaying access to superior livestock genetics, particularly in developing regions that rely on imports. Current US tariffs on imported biological inputs, laboratory equipment, and cold-chain technologies are adding cost pressure across breeding programs and service providers.

These added costs may slow penetration in cost-sensitive agricultural markets and reduce short-term investment in advanced reproductive technologies. However, such trade measures are encouraging domestic semen production, localized breeding programs, and stronger regional supply chains, which improve long-term sustainability.

Overall, despite near-term cost and trade constraints, the need for higher livestock productivity and genetic advancement is expected to maintain a positive and resilient growth outlook.

Latest Trends

Incorporation of sexed semen technologies and IoT-enabled breeding solutions represents a recent trend in the Veterinary Artificial Insemination market.

During 2024 and 2025, the sector has observed heightened deployment of sexed semen products that achieve elevated female calf yields, particularly in dairy operations seeking optimized herd composition. This progression supports strategic breeding decisions aimed at balancing replacement needs with commercial objectives.

Concurrently, integration of Internet of Things devices for real-time estrus monitoring and automated data collection has gained traction, facilitating more accurate insemination scheduling. Industry participants have pursued acquisitions and partnerships to embed advanced sensor technologies and software platforms into existing reproductive services.

Implementations demonstrate improvements in conception efficiency through precise timing and reduced manual intervention. The trend aligns with broader digital transformation efforts in livestock management, where data-driven insights enhance overall reproductive performance. Continued refinement of these tools addresses previous limitations in remote or large-scale settings.

Prominent developments observed in 2024–2025 underscore a shift toward intelligent, technology-augmented breeding practices that prioritize accuracy and operational simplicity. This orientation continues to reshape delivery models within the veterinary artificial insemination domain.

Regional Analysis

North America is leading the Veterinary Artificial Insemination Market

North America accounted for 35.8% of the veterinary artificial insemination market in 2025, supported by the region’s highly organized livestock industry and strong adoption of genetic improvement practices in animal breeding. Producers across the United States and Canada are increasingly using controlled breeding techniques to enhance productivity, disease resistance, and overall herd quality, particularly in dairy and beef cattle segments.

Data from the U.S. Department of Agriculture shows that U.S. milk production exceeded 226 billion pounds in 2023, reflecting the scale of dairy operations that rely on advanced breeding technologies to maintain output efficiency. Breeding programs are prioritizing superior genetic traits, which has increased demand for high-quality semen, precision insemination tools, and reproductive management services.

Technological advancements such as estrus synchronization and genomic selection are improving conception rates and breeding outcomes. Veterinary professionals and breeding specialists are also offering tailored reproductive services to optimize herd performance. Large-scale farms are integrating data-driven herd management systems that support reproductive planning.

Industry players are investing in cryopreservation and semen processing innovations to enhance product quality. These factors have collectively reinforced steady growth of assisted reproductive technologies in North America.

The Asia Pacific region is expected to experience the highest CAGR during the forecast period

Asia Pacific is expected to expand at a notable pace over the forecast period as livestock modernization and food security initiatives drive adoption of advanced breeding practices. Countries such as India, China, and Australia are actively promoting genetic improvement programs to increase milk and meat production efficiency.

The Food and Agriculture Organization highlights that Asia accounts for a significant share of the global cattle and buffalo population, creating strong demand for reproductive technologies that improve herd productivity. Governments across the region are implementing artificial insemination programs at scale, particularly in rural farming communities, to enhance livestock genetics and farmer income.

Veterinary networks and extension services are expanding access to reproductive technologies and technical training. Private sector players are introducing cost-effective semen products and breeding equipment suited to local conditions.

Increasing awareness among farmers regarding the economic benefits of controlled breeding is accelerating adoption. Research institutions are also advancing reproductive biotechnology to improve success rates. These developments are expected to support sustained expansion of assisted breeding solutions across Asia Pacific.

Key Regions and Countries

North America

- The US

- Canada

Europe

- Germany

- France

- The U.K.

- Italy

- Spain

- Russia & CIS

- Rest of Europe

Asia Pacific

- China

- India

- Japan

- South Korea

- ASEAN

- Australia & New Zealand

- Rest of Asia Pacific

Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

Latin America

- Brazil

- Mexico

- Rest of Latin America

Key Players Analysis

Key participants in the Veterinary Artificial Insemination Market expand growth by advancing genetic selection technologies, improving semen preservation methods, and strengthening partnerships with livestock breeders and dairy farms to enhance reproductive efficiency. Companies invest in high-quality semen production, genomic testing, and breeding analytics that help optimize herd productivity and disease resistance.

They also expand distribution networks and training programs for veterinarians and technicians to increase adoption of assisted breeding techniques. Genus plc represents a prominent participant in the Veterinary Artificial Insemination Market and operates as a UK-based animal genetics company that develops breeding technologies, genetic improvement programs, and reproductive solutions for livestock industries worldwide.

The company focuses on genetic innovation and data-driven breeding strategies to improve animal performance and farm profitability. Industry competitors continue to introduce advanced reproductive technologies, expand global breeding programs, and strengthen farmer engagement initiatives to drive adoption and sustain long-term market growth.

Top Key Players

- Zoetis Inc.

- Merck & Co., Inc. (MSD Animal Health)

- Elanco Animal Health Incorporated

- Boehringer Ingelheim International GmbH

- Genus plc (ABS Global & PIC)

- IMV Technologies Group

- CRV Holding B.V.

- VikingGenetics

- SEMEX

- Select Sires Inc.

- Alta Genetics Inc.

- URUS Group (GENEX)

- KUBUS S.A.

- Minitube GmbH

- Taurus Service Inc.

Recent Developments

- In March 2026, Zoetis announced a definitive agreement to acquire the animal genomics business from Neogen. Expected to close by late 2026, this move strengthens Zoetis’ position in precision animal health by integrating advanced genomics capabilities into its portfolio. The acquisition is expected to support more data-driven breeding strategies, where genetic insights guide the selection of superior sires in artificial insemination programs, improving productivity and herd quality.

- In February 2026, Genus plc reported a 57% increase in adjusted pretax profit for the first half of fiscal year 2026. This strong performance was driven by its royalty-based business model and the expansion of its Chinese porcine joint venture, which received regulatory approval in December 2025. The joint venture is expected to provide a significant growth platform, enabling Genus to strengthen its leadership in genetic improvement and artificial insemination technologies within the global pork industry.

- In late 2025, IMV Technologies received the Sommets d’Or for its BovIntel software. When integrated with the Easi-Scan:Go ultrasound system, BovIntel leverages AI-assisted analysis to support real-time reproductive decision-making. This capability allows veterinarians to optimize insemination timing directly in field conditions, improving breeding efficiency and reproductive outcomes.

Report Scope

Report Features Description Market Value (2025) US$ 7.4 Billion Forecast Revenue (2035) US$ 15.5 Billion CAGR (2026-2035) 7.7% Base Year for Estimation 2025 Historic Period 2020-2024 Forecast Period 2026-2035 Report Coverage Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments Segments Covered By Animal Type (Bovine, Porcine, Ovine, Caprine, Equine, Canine and Others), By Product Type (Semen, Equipment and Reagents and Kits), By End User (Veterinary Hospitals, Breeding Centers, Dairy Farms, Pig Farms, Poultry Farms and Others) Regional Analysis North America – The US, Canada; Europe – Germany, France, The U.K., Italy, Spain, Russia & CIS, Rest of Europe; Asia Pacific – China, India, Japan, South Korea, ASEAN, Australia & New Zealand, Rest of Asia Pacific; Middle East & Africa – GCC, South Africa, Rest of Middle East & Africa; Latin America – Brazil, Mexico, Rest of Latin America Competitive Landscape Zoetis Inc., Merck & Co., Inc., Elanco Animal Health, Boehringer Ingelheim, Genus plc, IMV Technologies Group, CRV Holding B.V., VikingGenetics, SEMEX, Select Sires Inc., Alta Genetics Inc., URUS Group, KUBUS S.A., Minitube GmbH, Taurus Service Inc. Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF)  Veterinary Artificial Insemination MarketPublished date: April 2026add_shopping_cartBuy Now get_appDownload Sample

Veterinary Artificial Insemination MarketPublished date: April 2026add_shopping_cartBuy Now get_appDownload Sample -

-

- Zoetis Inc.

- Merck & Co., Inc. (MSD Animal Health)

- Elanco Animal Health Incorporated

- Boehringer Ingelheim International GmbH

- Genus plc (ABS Global & PIC)

- IMV Technologies Group

- CRV Holding B.V.

- VikingGenetics

- SEMEX

- Select Sires Inc.

- Alta Genetics Inc.

- URUS Group (GENEX)

- KUBUS S.A.

- Minitube GmbH

- Taurus Service Inc.

Our Clients

- 183674

- April 2026