Quick Navigation

Report Overview

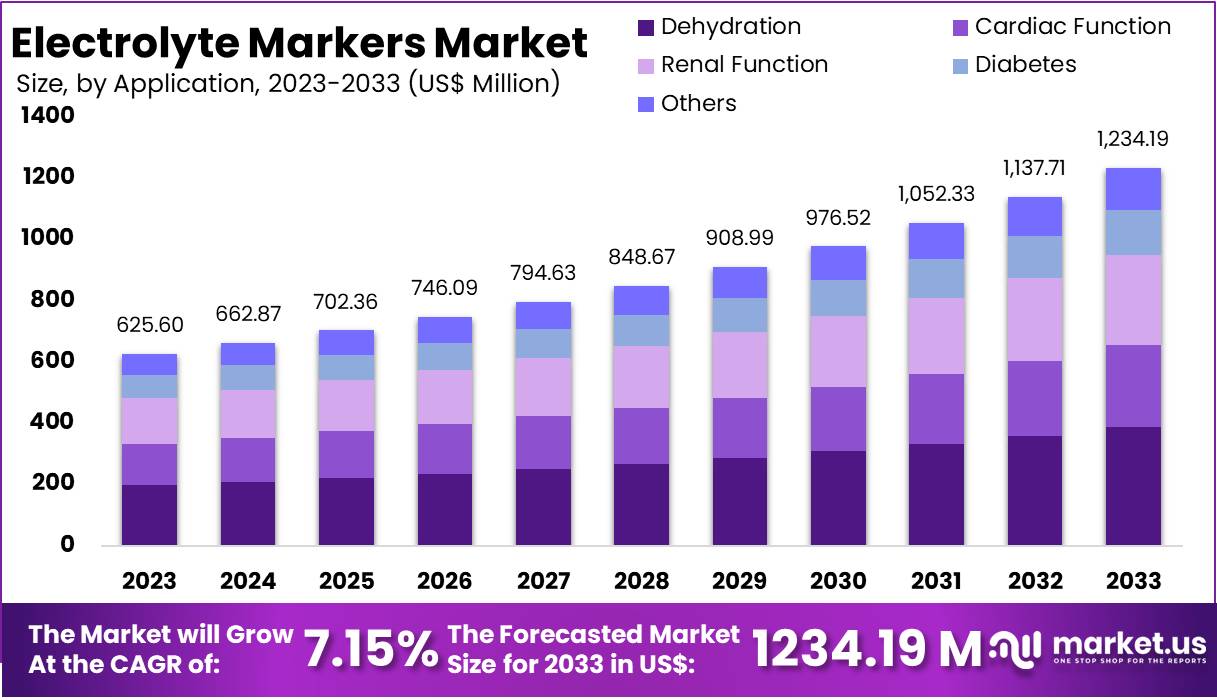

The Global Electrolyte Markers Market Size is expected to be worth around US$ 1234.19 Million by 2033, from US$ 625.6 Million in 2023, growing at a CAGR of 7.15% during the forecast period from 2024 to 2033.

Electrolyte markers are biochemical indicators used to measure the levels of electrolytes in the body, such as sodium, potassium, chloride, and bicarbonate. These markers are crucial for diagnosing and monitoring various medical conditions that affect fluid and electrolyte balance, including dehydration, kidney disease, heart disorders, and disturbances in acid-base balance. Electrolyte testing is commonly performed through blood tests or urinalysis and is a standard component of routine health screenings.

The global electrolyte markers market is experiencing significant growth, driven by factors such as the rising prevalence of chronic diseases, aging populations, and increasing demand for point-of-care diagnostic testing. Technological advancements in diagnostic tools, which provide quicker and more accurate results, are further fueling this expansion. Additionally, the global push to enhance healthcare infrastructure and the growing awareness of preventive healthcare contribute to the rising adoption of electrolyte testing solutions.

Healthcare facilities, including hospitals, clinics, and diagnostic centers, are the primary users of electrolyte testing devices. The shift towards personalized medicine has also boosted market growth. For example, electrolyte tests play a crucial role in tailoring treatment plans to individual patient needs. As healthcare systems embrace integrated diagnostic solutions, the market is well-positioned to address evolving health challenges and leverage technological developments.

According to import-export data from ZAUBA, China is a major exporter of electrolyte analyzers, accounting for 38.99% of India’s imports under Sub Chapter 9027. Switzerland follows closely, contributing 29.86% to these imports. In 2016, India imported electrolyte analyzers from multiple countries, including China, Germany, and Japan, with an average import price of approximately $64.58 per unit. These devices are essential in clinical settings for accurate measurement of electrolyte levels, ensuring precise patient assessments.

Electrolyte markers such as sodium and potassium are critical for maintaining bodily functions. Regulatory agencies like the U.S. Food and Drug Administration (FDA) oversee their inclusion in beverages. For instance, the FDA mandates sodium levels in non-juice beverages to range from 5-20 milliequivalents per liter and potassium levels from 3-7 milliequivalents per liter to ensure consumer safety. Similarly, the World Health Organization (WHO) sets guidelines for drinking-water quality, influencing national standards to maintain safe electrolyte concentrations in water supplies.

In the United States, the Environmental Protection Agency (EPA) regulates public drinking water systems through the National Primary Drinking Water Regulations. These standards limit over 90 contaminants, including certain electrolytes, to safeguard public health. Excessive sodium, for example, can lead to hypertension, while imbalances in other electrolytes may cause various health issues. Regular testing and adherence to these guidelines help maintain safe electrolyte levels in drinking water.

Monitoring water quality is essential to prevent health risks. A study by the Centers for Disease Control and Prevention (CDC) estimates that at least 1.1 million Americans fall ill annually due to germs in drinking water. While this primarily highlights microbial contamination, it underscores the importance of comprehensive monitoring, including electrolyte levels. Maintaining proper electrolyte concentrations in water and beverages is critical for preventing illness and supporting overall public health.

Key Takeaways

- The global Electrolyte Markers Market is projected to reach US$ 1234.19 million by 2033, growing from US$ 625.6 million in 2023, with a 7.15% CAGR.

- In 2023, the Electrolyte Panel Test led the product segment of the market, capturing over 35.20% of the total market share.

- Dehydration dominated the application segment in 2023, holding more than 31.50% of the market share for electrolyte markers.

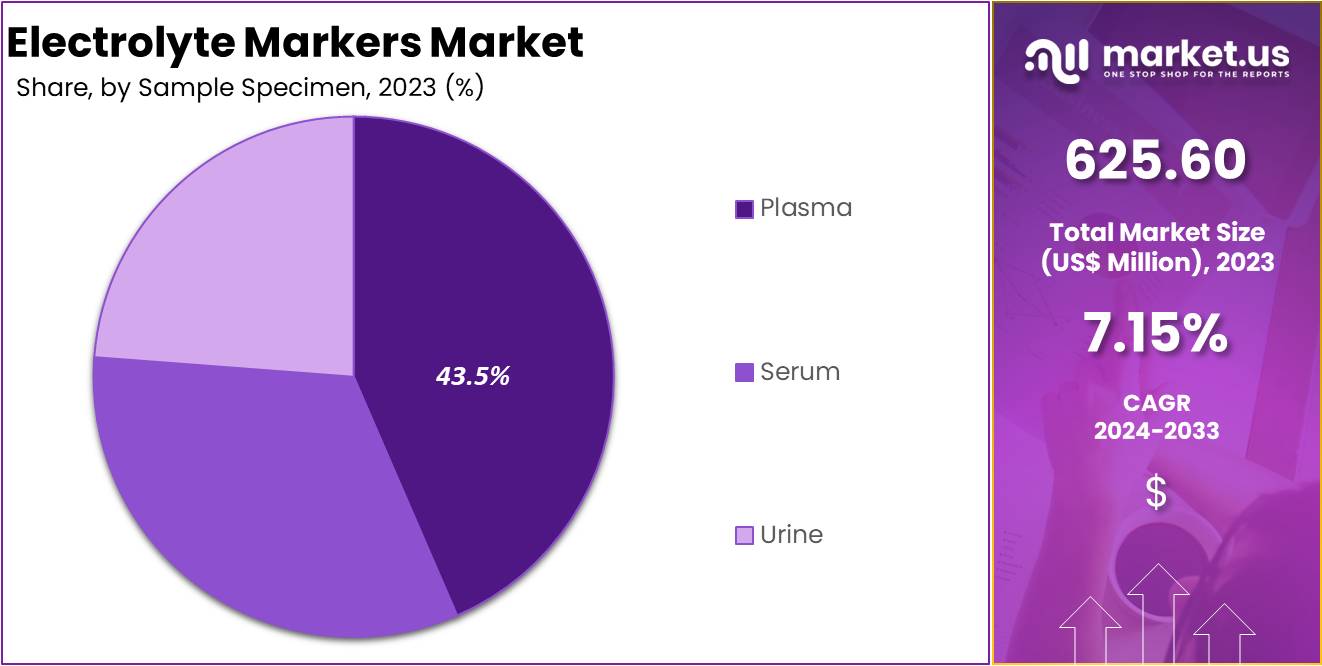

- Plasma was the leading specimen sample in 2023, accounting for over 43.50% of the market share in electrolyte marker testing.

- Clinical laboratories were the dominant end users in 2023, holding more than 49.60% of the market share for electrolyte markers.

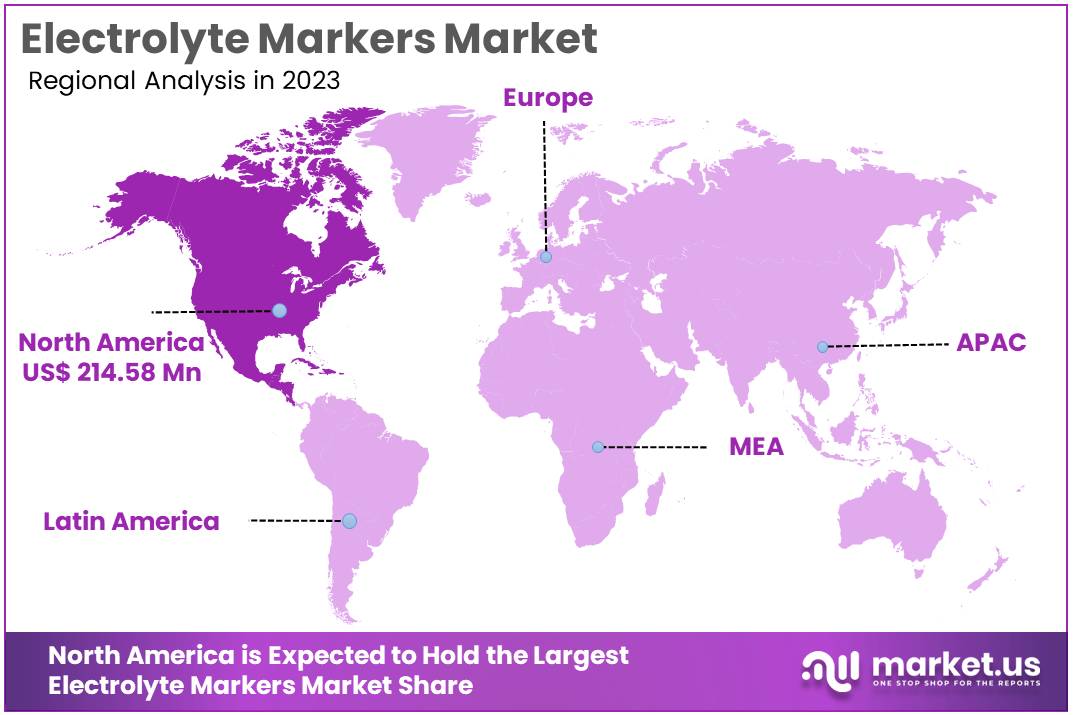

- North America was the dominant region in 2023, controlling over 34.30% of the electrolyte markers market, with a market value of US$ 214.58 million.

Product Analysis

In 2023, Electrolyte Panel Test held a dominant market position in the Product Segment of the Electrolyte Markers Market, capturing more than a 35.20% share. This test is essential for diagnosing and monitoring electrolyte imbalances in the body. It assesses key electrolytes such as sodium, potassium, chloride, and bicarbonate. The Electrolyte Panel Test is often the first choice for clinicians due to its comprehensive results and ability to provide valuable insights into a patient’s health.

Other tests, like the Carbon Dioxide (CO2) Assay, are also critical in monitoring electrolyte levels. CO2 assays help evaluate the body’s acid-base balance, which can indicate respiratory or metabolic issues. Sodium Assay is another key test, measuring sodium levels in the blood. It is crucial for monitoring fluid balance and nerve function. Additionally, Chloride Assay helps detect electrolyte imbalances, especially in conditions like dehydration and kidney disease.

Tests such as Calcium Assay, Potassium Assay, and Magnesium Assay are gaining prominence. Calcium Assay is important for assessing bone health and muscle function. Potassium Assay is vital for heart function and muscle contraction. Magnesium Assay, on the other hand, plays a role in enzyme function and nerve transmission. Lithium Assay is crucial for patients on lithium therapy, helping to avoid toxicity. These specialized tests meet specific clinical needs and contribute to the market’s growth.

Application Analysis

In 2023, Dehydration held a dominant market position in the Application Segment of the Electrolyte Markers Market, capturing more than a 31.50% share. Dehydration is a common condition that significantly impacts electrolyte balance. As the body loses water, critical electrolytes like sodium, potassium, and chloride are also lost. This creates an urgent need to monitor electrolyte levels. Electrolyte markers are key in detecting and managing dehydration.

Cardiac Function also plays a significant role in the market. Electrolyte imbalances can lead to arrhythmias and other heart issues. Monitoring these markers ensures better heart health management. Renal Function is another critical area. The kidneys regulate electrolyte levels, and any dysfunction can result in serious imbalances. Electrolyte markers help in assessing kidney function.

Diabetes is increasingly contributing to the market. Diabetic patients often experience electrolyte disturbances due to fluctuating blood sugar levels. Electrolyte markers are used to monitor these imbalances. Other applications, such as monitoring critical illnesses and treatment responses, are also growing. The demand for electrolyte testing tools is rising across various sectors, including healthcare and diagnostics.

Overall, the Electrolyte Markers Market is expanding, driven by the need for precise and reliable applications in healthcare. With advancements in diagnostic technology, the usage of electrolyte markers will continue to rise across diverse medical conditions.

Sample Specimen Analysis

In 2023, Plasma held a dominant market position in the Sample Specimen Segment of the Electrolyte Markers Market, capturing more than a 43.50% share. Plasma is the preferred choice for electrolyte analysis in medical diagnostics. It is widely used for its high stability and ease of collection. These factors make plasma a reliable specimen for accurate electrolyte testing. As a result, it remains the leader in the market and continues to drive demand for electrolyte marker testing.

Serum, another crucial specimen, follows closely behind plasma in terms of market share. It is commonly used in diagnostic procedures and offers reliable results for electrolyte concentration measurements. Serum’s versatility in various tests contributes to its strong market presence. It is frequently chosen for routine diagnostics and helps healthcare providers monitor electrolyte imbalances. As a result, serum plays an essential role in the global electrolyte markers market.

Urine specimens are also significant in the analysis of electrolyte markers. Though less commonly used than plasma or serum, urine testing provides valuable information about kidney function. It is particularly useful for detecting electrolyte imbalances related to renal health. With rising awareness of kidney diseases, urine-based tests are expected to grow in demand. This segment continues to show steady growth and complements the use of plasma and serum in electrolyte marker testing.

End User Analysis

In 2023, Clinical Laboratories held a dominant market position in the End User Segment of the Electrolyte Markers Market, capturing more than a 49.60% share. This strong position can be attributed to the increasing need for accurate diagnostics and patient monitoring. Clinical laboratories are equipped with advanced technology, allowing them to analyze electrolyte markers in plasma, serum, and urine samples. These laboratories play a critical role in diagnosing electrolyte imbalances and related health conditions.

The demand for electrolyte marker testing has been rising, especially as the prevalence of chronic diseases grows. Hospitals and diagnostic centers rely on clinical laboratories to provide timely and accurate results. As a result, the clinical laboratory segment is expected to continue its market dominance. Plasma testing is widely used due to its precision, while serum and urine testing also see significant demand, particularly for monitoring patient health.

In addition to accurate results, clinical laboratories offer a broad range of tests that help healthcare providers address electrolyte imbalances. This growing focus on diagnostics and improved patient outcomes is a key factor contributing to the expansion of the electrolyte markers market. As healthcare systems evolve, the need for reliable testing in clinical laboratories will continue to rise, ensuring sustained growth for this segment.

Key Market Segments

By Product

- Electrolyte Panel Test

- Carbon Dioxide (CO2) Assay

- Sodium Assay

- Chloride Assay

- Calcium Assay

- Potassium Assay

- Magnesium Assay

- Lithium Assay

- Others

By Application

- Dehydration

- Cardiac Function

- Renal Function

- Diabetes

- Others

By Sample Specimen

- Plasma

- Serum

- Urine

By End User

- Point of Care Diagnostic Centers

- Clinical Laboratory

- Home care Setting

Drivers

Increasing Prevalence of Chronic Diseases

The growing prevalence of chronic diseases, including kidney disease, diabetes, and cardiovascular disorders, is significantly driving the electrolyte markers market. These conditions often disrupt the balance of essential electrolytes in the body, such as sodium, potassium, and calcium. As a result, patients require frequent monitoring of their electrolyte levels to avoid severe complications. The need for accurate and real-time measurement of electrolyte imbalances is pushing the demand for advanced electrolyte markers in healthcare.

Furthermore, chronic diseases often lead to complications that affect multiple body systems. For instance, kidney disease can impair electrolyte regulation, while diabetes can cause fluctuations in blood glucose levels, indirectly affecting electrolytes. Cardiovascular conditions also exacerbate electrolyte imbalances due to medications and heart-related issues. These factors create a growing need for reliable monitoring solutions, increasing the adoption of electrolyte markers among healthcare providers.

In response to this rising demand, healthcare systems are investing in advanced diagnostic tools. Electrolyte monitoring devices enable early detection and management of imbalances, which is crucial for improving patient outcomes. As the number of chronic disease cases continues to rise globally, the electrolyte markers market is expected to expand significantly. This trend highlights the need for continuous innovation in electrolyte monitoring technologies to better address the challenges faced by patients with chronic health conditions.

Restraints

High Cost of Electrolyte Testing Equipment

The high initial cost of advanced electrolyte analyzers is a significant restraint in the electrolyte markers market. Many healthcare facilities, especially in emerging economies, face financial challenges in acquiring such expensive equipment. This makes it difficult for hospitals and clinics in lower-income regions to implement these technologies, limiting their access to advanced diagnostic tools. As a result, the adoption of electrolyte testing equipment is slower in these markets, hindering overall market growth.

The substantial investment required for electrolyte testing devices also poses a barrier to small and mid-sized healthcare providers. These institutions may prioritize other areas of medical infrastructure due to budget constraints. Consequently, they may delay or forgo upgrading to more advanced electrolyte testing equipment. This limits the market’s expansion potential, especially in regions where healthcare budgets are stretched thin and cost-effectiveness is a key consideration.

Additionally, the high cost of electrolyte testing equipment contributes to a disparity in healthcare quality between high-income and low-income regions. Even though advanced diagnostic tools are crucial for accurate patient care, the cost barrier prevents many underserved areas from benefiting from such innovations. Therefore, the high price of electrolyte analyzers remains a key restraint, slowing the overall adoption of these technologies in global healthcare systems.

Opportunities

Growth of Point-of-Care Diagnostics

The growing trend of point-of-care (POC) diagnostics presents a significant opportunity for the electrolyte markers market. As healthcare systems shift towards more decentralized care, there is an increasing demand for rapid, on-site testing. This demand drives the need for electrolyte monitoring solutions that are portable and easy to use. POC diagnostics offer the potential for faster results, improving patient outcomes by enabling timely interventions.

Electrolyte markers play a critical role in monitoring health conditions, especially for patients with chronic diseases or those undergoing critical treatments. The development of user-friendly, portable devices for electrolyte testing can cater to this rising demand. This convenience allows for continuous monitoring in various settings, including home care, clinics, and emergency rooms, which can significantly enhance patient care and satisfaction.

The growth of POC diagnostics opens doors for innovation within the electrolyte markers market. Manufacturers can focus on creating compact, cost-effective devices that offer high accuracy and ease of use. By meeting the increasing need for rapid electrolyte testing, companies can tap into an expanding market and position themselves as leaders in the healthcare technology space. This opportunity is poised to drive growth and improve overall health management.

Trends

Growing Adoption of Real-Time Monitoring Technologies in Electrolyte Markers Market

The electrolyte markers market is witnessing a significant boost due to advancements in real-time monitoring technologies. Wearable devices designed for continuous electrolyte measurement are becoming increasingly popular. These devices cater to the rising demand for instant health insights, particularly among athletes and individuals managing chronic conditions. The ability to monitor electrolyte levels seamlessly in real time offers a proactive approach to health management, driving adoption rates globally.

This trend aligns with the growing focus on personalized healthcare solutions. Wearable electrolyte monitoring systems provide users with tailored feedback, promoting better hydration and electrolyte balance. Their compact designs and user-friendly interfaces enhance usability, making them ideal for daily use. Such innovations are drawing attention from both healthcare providers and consumers, further fueling market growth.

Moreover, the integration of advanced sensors and data analytics in these devices is revolutionizing health tracking. These technologies ensure accurate, real-time data collection and interpretation. As awareness of preventive healthcare grows, the demand for such cutting-edge monitoring systems is expected to rise. This trend highlights a promising opportunity for stakeholders in the electrolyte markers market to innovate and expand their product portfolios.

Regional Analysis

In 2023, North America held a dominant market position in the Electrolyte Markers Market, capturing more than a 34.30% share and holding a market value of US$ 214.58 million for the year. This significant share is primarily due to the advanced healthcare infrastructure in the region. Facilities equipped with cutting-edge technologies enable precise and rapid testing of electrolytes, essential for diagnosing and managing various health conditions.

The prevalence of chronic diseases such as diabetes and kidney disorders also contributes to the demand for electrolyte markers. In North America, these health issues necessitate ongoing monitoring, thereby boosting the market. Additionally, substantial investments from both government and private sectors in healthcare research encourage continual innovation in diagnostic technologies.

The presence of leading healthcare companies further supports the market’s growth. These companies invest heavily in research and development, leading to the introduction of more accurate and efficient products. Collaborative efforts between research institutions and healthcare enterprises are aimed at enhancing electrolyte testing technologies. This collaboration helps maintain North America’s strong market presence by expanding the applications of electrolyte markers in medical diagnostics.

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia

- Netherland

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- New Zealand

- Singapore

- Thailand

- Vietnam

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Key Players Analysis

The electrolyte markers market is growing steadily, driven by advancements in diagnostic technologies and rising demand for rapid testing. Atlas Medical GmbH is a key player in this market, known for its high-quality diagnostic reagents. The company has a strong presence in global markets, backed by continuous investment in R&D to improve accuracy. However, it faces fierce competition from other established players. To maintain its position, Atlas Medical must keep innovating and expanding its product offerings.

Weldon Biotech India Pvt. Ltd. specializes in providing cost-effective diagnostic solutions. It is known for offering affordable electrolyte marker testing kits, particularly in emerging markets. The company has a strong local presence in India and has formed strategic partnerships to enhance its product offerings. While Weldon Biotech has a competitive edge in price-sensitive markets, its ability to expand into premium sectors with higher margins is limited. Expansion into international markets is also a challenge.

In the UK, Sussex Pathology Limited offers a wide range of diagnostic tests, including electrolyte markers. The company’s strong reputation for accuracy and comprehensive testing services has helped it gain trust within the healthcare sector. Sussex Pathology is well-integrated with hospitals and clinics, enhancing its market reach. However, its international presence remains limited. The company must focus on expanding outside the UK to compete with global players in the electrolyte marker market.

Mitsubishi Chemical is a prominent player, leveraging its large-scale production capabilities. The company supplies electrolyte marker reagents globally, backed by significant investments in R&D. Mitsubishi Chemical’s diversified product portfolio across multiple industries gives it a competitive advantage. However, its focus on various sectors may lead to less emphasis on the electrolyte marker segment. Randox Laboratories, another key player, has a broad product portfolio and a strong global presence, but faces competition from both large and emerging companies in the diagnostic market.

Market Key Players

- Atlas Medical GmbH

- Weldon Biotech India Pvt. Ltd.

- Sussex Pathology Limited

- Mitasabishi Chemical

- Randox Laboratories

- Merck Group (Sigma-Aldrich Corporation)

- Nova-Tech International, Inc.

- EKF Diagnostics USA (Stanbio Laboratory)

- Beckmann Coulter Inc. (Danaher Corporation)

- Abbott Laboratories

- F. Hoffmann-la Roche Ltd

- SMC Enterprice

Recent Developments

- In May 2023: Mitsubishi Chemical signed a memorandum of understanding with Koura, an Orbia business, to explore collaboration opportunities aimed at strengthening the supply chain for formulated electrolytes for lithium-ion batteries in North America. This collaboration is part of Mitsubishi Chemical’s strategic efforts to meet the growing demand for xEVs, bolstered by incentives like the U.S. Inflation Reduction Act of 2022. They plan to establish a production facility in Louisiana, which is expected to commence operations in late 2025.

- In January 2023: Atlas Medical GmbH secured a significant financial boost with a €2.4 million Series A funding round led by Ancora Finance Group. This funding aims to expand their operations within Europe, with the capital increase specifically allocated for enhancing their technological capabilities in interventional radiology and orthopedics. The centerpiece of this development is their 4D laser navigation robot, which is designed to improve the precision of microsurgeries and injections..

- In May 2022: Weldon Biotech sold its i-chroma brand business to CPC Diagnostics Pvt. Ltd., a subsidiary of the Singaporean group Everlife. This transaction involved the transfer of point-of-care testing (POCT) products manufactured by Boditech Med Inc., Korea. CPC Diagnostics took over the distribution rights of the i-chroma brand, enhancing its footprint in the growing POCT market in India.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2023) | US$ 625.60 Million |

| Forecast Revenue (2033) | US$ 1234.19 Million |

| CAGR (2024-2033) | 7.15% |

| Base Year for Estimation | 2023 |

| Historic Period | 2019-2022 |

| Forecast Period | 2024-2033 |

| Report Coverage | Revenue Forecast, Market Dynamics, COVID-19 Impact, Competitive Landscape, Recent Developments |

| Segments Covered | By Product (Electrolyte Panel Test, Carbon Dioxide (CO2) Assay, Sodium Assay, Chloride Assay, Calcium Assay, Potassium Assay, Magnesium Assay, Lithium Assay, Others), By Application (Dehydration, Cardiac Function, Renal Function, Diabetes, Others), By Sample Specimen (Plasma, Serum, Urine), By End User (Point of Care Diagnostic Centers, Clinical Laboratory, Home care Setting) |

| Regional Analysis | North America – The US, Canada, & Mexico; Western Europe – Germany, France, The UK, Spain, Italy, Portugal, Ireland, Austria, Switzerland, Benelux, Nordic, & Rest of Western Europe; Eastern Europe – Russia, Poland, The Czech Republic, Greece, & Rest of Eastern Europe; APAC – China, Japan, South Korea, India, Australia & New Zealand, Indonesia, Malaysia, Philippines, Singapore, Thailand, Vietnam, & Rest of APAC; Latin America – Brazil, Colombia, Chile, Argentina, Costa Rica, & Rest of Latin America; Middle East & Africa – Algeria, Egypt, Israel, Kuwait, Nigeria, Saudi Arabia, South Africa, Turkey, United Arab Emirates, & Rest of MEA |

| Competitive Landscape | Atlas Medical GmbH, Weldon Biotech India Pvt. Ltd., Sussex Pathology Limited, Mitasabishi Chemical, Randox Laboratories, Merck Group (Sigma-Aldrich Corporation), Nova-Tech International, Inc., EKF Diagnostics USA (Stanbio Laboratory), Beckmann Coulter Inc. (Danaher Corporation), Abbott Laboratories, F. Hoffmann-la Roche Ltd, SMC Enterprice |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |