Quick Navigation

Report Overview

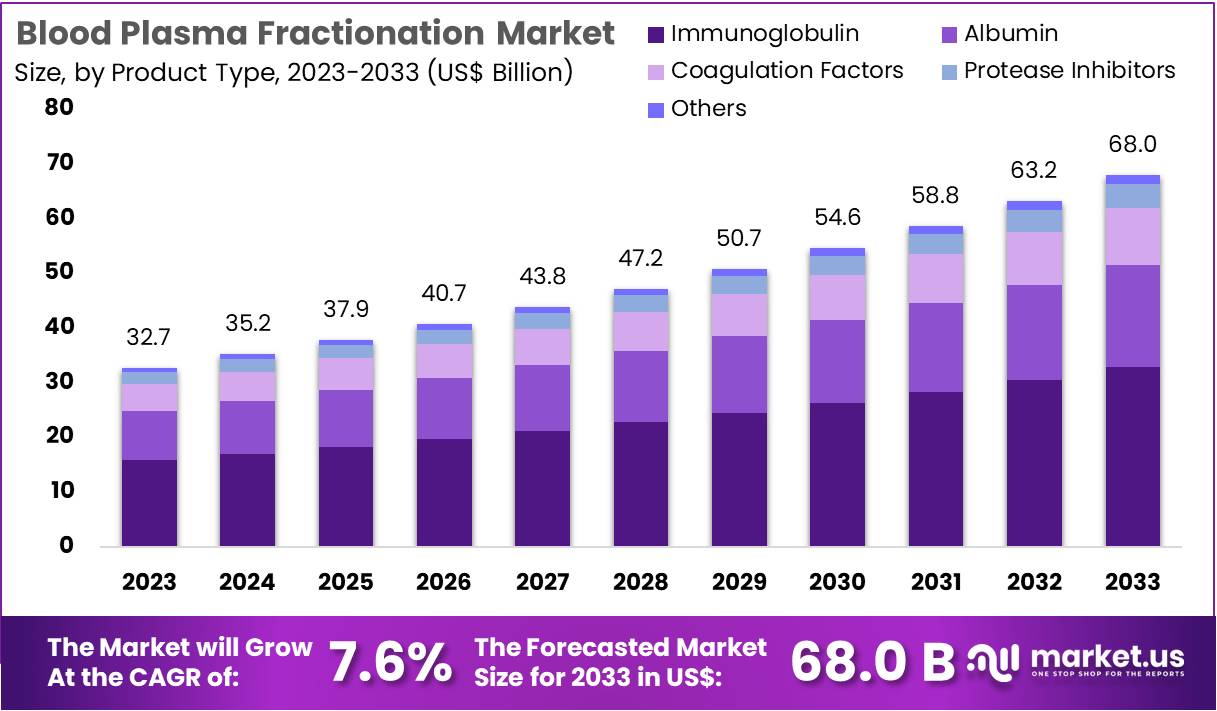

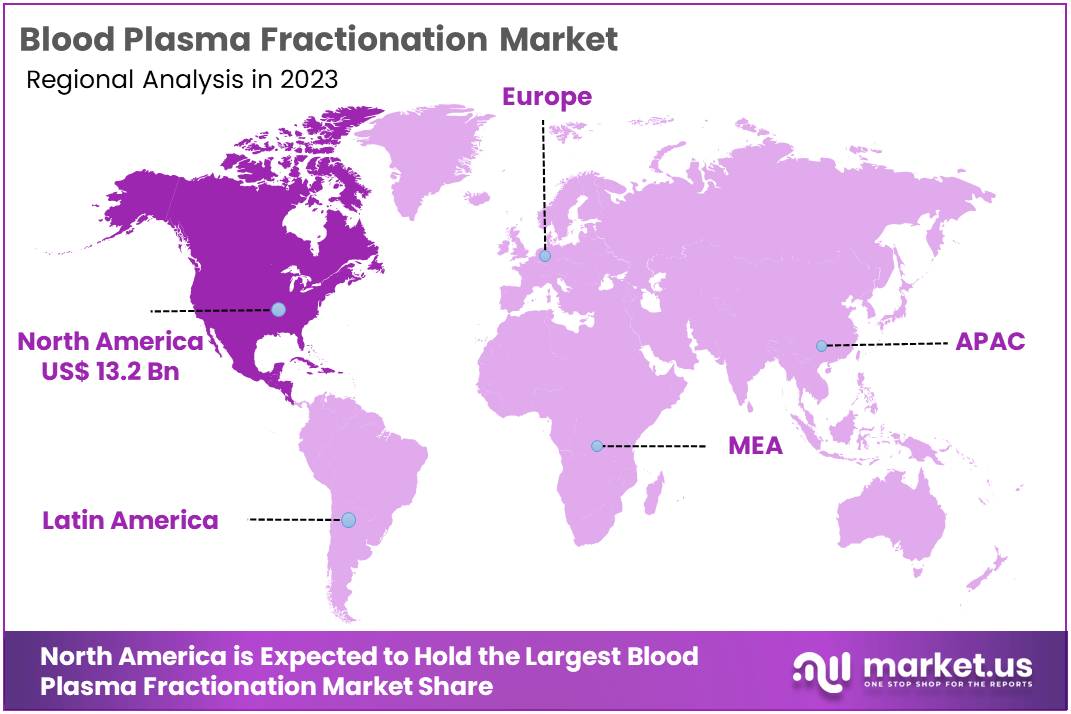

The Global Blood Plasma Fractionation Market size is expected to be worth around US$ 68 Billion by 2033, from US$ 32.7 Billion in 2023, growing at a CAGR of 7.6% during the forecast period from 2024 to 2033. North America held a dominant market position, capturing more than a 40.3% share and holds US$ 13.2 Billion market value for the year.

Increasing demand for plasma-derived therapies is driving the growth of the blood plasma fractionation market. Plasma fractionation involves the separation of blood plasma into its component parts, which can then be used in a variety of therapeutic applications, including treatments for immunodeficiencies, bleeding disorders, and neurological diseases.

The rising prevalence of chronic conditions such as Chronic Inflammatory Demyelinating Polyneuropathy (CIDP), with approximately 60,000 cases diagnosed annually in the US, is boosting the need for plasma-derived therapies. The GBS/CIDP Foundation International’s 2022 report highlights the growing patient population requiring these treatments.

In March 2021, the World Health Organization issued new guidelines to increase the availability of plasma-derived medicinal products, particularly focusing on plasma fractionation in low- and middle-income countries. This development reflects the increasing global efforts to expand access to life-saving therapies derived from blood plasma.

Additionally, advancements in fractionation technologies are improving the efficiency of plasma processing and enabling the production of higher-quality plasma derivatives. As healthcare systems strive to meet the growing demand for immunoglobulins, clotting factors, and albumin, the market is witnessing continued investment and innovation.

Opportunities also lie in expanding collection programs, improving plasma donation rates, and addressing the need for more localized plasma fractionation infrastructure. With a broader range of applications and a growing patient base, the blood plasma fractionation market is expected to continue its upward trajectory.

Key Takeaways

- In 2023, the market for blood plasma fractionation generated a revenue of US$ 32.7 billion, with a CAGR of 7.6%, and is expected to reach US$ 68.0 billion by the year 2033.

- The product type segment is divided into albumin, immunoglobulin, coagulation factors, protease inhibitors, and others, with immunoglobulin taking the lead in 2023 with a market share of 48.3%.

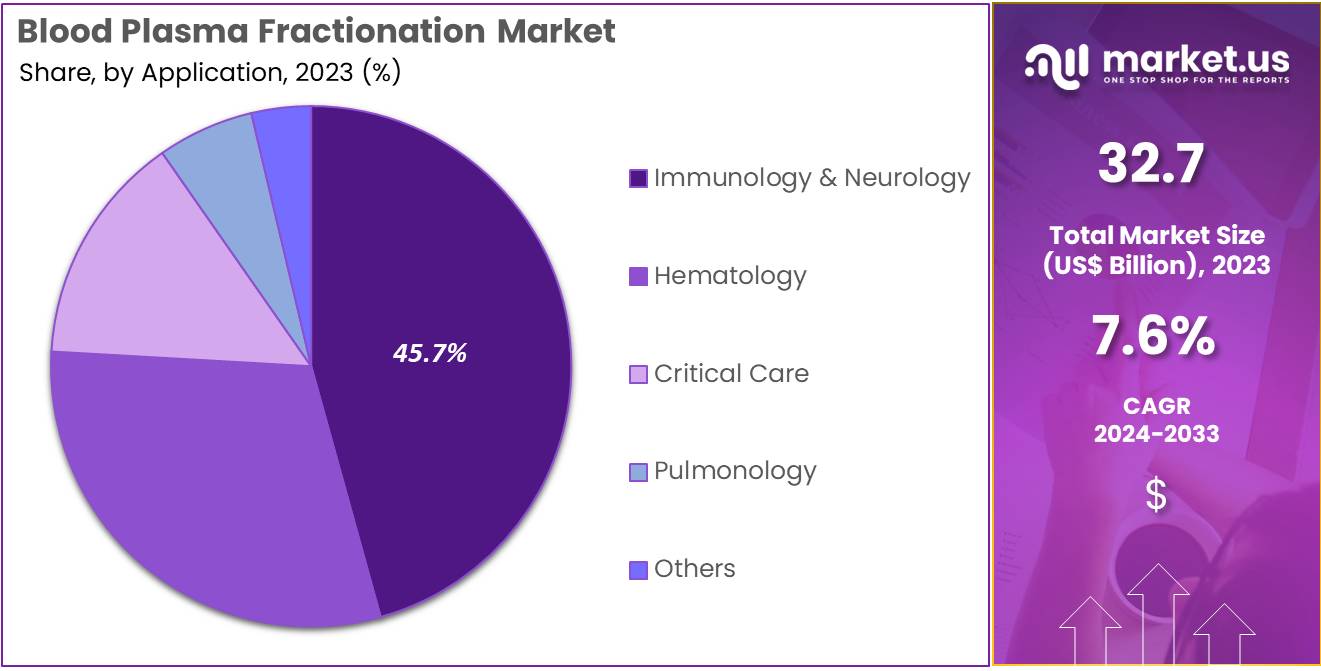

- Considering application, the market is divided into immunology & neurology, hematology, critical care, pulmonology, and others. Among these, immunology & neurology held a significant share of 45.7%.

- Furthermore, concerning the end-user segment, the market is segregated into hospitals & clinics, clinical research laboratories, and others. The hospitals & clinics sector stands out as the dominant player, holding the largest revenue share of 53.4% in the blood plasma fractionation market.

- North America led the market by securing a market share of 40.3% in 2023.

Industrial Advantages

Blood plasma fractionation offers substantial business benefits for market key players. This process leads to the production of high-value proteins used in various therapies, significantly enhancing revenue streams. It also allows companies to diversify their product offerings into different therapeutic areas such as immunology, oncology, and hematology, which broadens their market reach and potential.

The industrial advantages of blood plasma fractionation are notable. Technological advancements in the fractionation process improve the yield and purity of plasma products. This not only reduces costs but also elevates safety standards. Additionally, companies engaged in plasma fractionation can better comply with the stringent regulatory requirements, ensuring product quality and safety, which gives them a competitive edge.

There are several opportunities in the plasma fractionation industry. Innovations in this area can lead to the development of new therapeutic products and applications. This opens up possibilities for companies to pioneer novel treatments. Furthermore, strategic alliances and partnerships with biotech firms, academic institutions, and healthcare providers can significantly enhance product development capabilities and expand market reach.

Emerging markets offer lucrative growth prospects for players in the plasma fractionation field. As healthcare spending increases and the demand for plasma-derived therapeutics grows in these regions, companies can capitalize on these opportunities. This enables them to not only expand their geographical footprint but also to meet the growing global demand for plasma products, optimizing their overall market presence.

Product Type Analysis

The immunoglobulin segment led in 2023, claiming a market share of 48.3% owing to the increasing prevalence of immune-related disorders and infections. Immunoglobulin therapy plays a crucial role in treating autoimmune diseases, immunodeficiencies, and chronic inflammatory conditions, making it a vital component of plasma-derived therapies.

As the global incidence of these conditions rises, the demand for immunoglobulin-based treatments is projected to expand. Furthermore, advancements in the production and purification processes of immunoglobulin are likely to improve the efficiency and affordability of these therapies, contributing to market growth.

The growing emphasis on personalized medicine and targeted therapies for immune disorders is anticipated to further boost the immunoglobulin segment, as healthcare providers seek more effective and tailored treatment options.

Application Analysis

The immunology & neurology held a significant share of 45.7% due to the increasing demand for plasma-derived therapies in the treatment of neurological and immunological diseases. Plasma proteins, such as immunoglobulins, are used to manage a range of conditions including multiple sclerosis, Guillain-Barré syndrome, and other neurological disorders.

The growth of this segment is supported by rising awareness about the benefits of plasma-based treatments in managing immune and neurological diseases, coupled with the development of more advanced therapies. Additionally, ongoing research and clinical trials focusing on the use of immunoglobulins and other plasma proteins for neurological conditions are likely to further fuel the demand for these therapies, ensuring sustained growth in the segment.

End-user Analysis

The hospitals and clinics segment exhibited significant growth, achieving a revenue share of 53.4%. This growth is primarily driven by the increasing adoption of advanced plasma-derived therapies within these facilities. These therapies are utilized to treat a range of conditions, including autoimmune diseases, chronic infections, and hematologic disorders. The effectiveness of products such as immunoglobulins and albumin in managing life-threatening conditions has heightened their usage in medical settings.

The demand for plasma-derived products in healthcare settings is poised to escalate. This trend is bolstered by the rising prevalence of conditions that necessitate such treatments. Hospitals and clinics are progressively integrating blood plasma fractionation products into their treatment protocols, enhancing patient care quality and outcomes.

The expansion of healthcare facilities and the shift towards specialized care centers offering plasma therapy further contribute to this segment’s growth. As hospitals aim to improve patient outcomes and reduce the costs associated with long-term treatments, the continued rise in the adoption of blood plasma fractionation products is anticipated. This ongoing trend underscores the sector’s commitment to advancing therapeutic practices and enhancing patient care standards.

Key Market Segments

By Product Type

- Albumin

- Immunoglobulin

- IVIG

- SCIG

- Coagulation Factors

- Factor IX

- Factor VIII

- Fibrinogen Concentrates

- Prothrombin Complex Concentrates

- Others

- Protease Inhibitors

- Others

By Application

- Immunology & Neurology

- Hematology

- Critical Care

- Pulmonology

- Others

By End-user

- Hospitals & Clinics

- Clinical Research Laboratories

- Others

Drivers

Growing Prevalence of Bleeding Disorders Driving Market Growth

The growing prevalence of bleeding disorders significantly drives the blood plasma fractionation market. According to the 2022 global survey by the World Federation of Hemophilia, the number of individuals affected by bleeding disorders worldwide reached 454,690 in 2022, an increase from 393,658 in 2020. This rise in prevalence is expected to continue, with a notable impact on the demand for fractionated plasma products used in the treatment of conditions like hemophilia.

Plasma-derived therapies, such as clotting factor concentrates, are essential for managing bleeding episodes in individuals with hemophilia and other bleeding disorders. As the incidence of these conditions rises, the need for more efficient and widely available plasma fractionation processes to ensure a steady supply of these critical therapies will increase, further driving the market for plasma fractionation technologies.

Restraints

Supply Chain Constraints Restraining Market Growth

Rising supply chain constraints pose a significant challenge to the blood plasma fractionation market. These constraints, including limited availability of raw plasma, transportation bottlenecks, and production delays, have the potential to impede the market’s growth. The complex process of collecting and processing human plasma, combined with the increasing demand for plasma-derived therapies, is likely to create additional strain on existing supply chains.

Such disruptions are expected to result in delays in product availability, especially in regions with high healthcare needs. Furthermore, fluctuations in plasma supply and regulatory hurdles could hamper the ability of manufacturers to scale production quickly, ultimately slowing the market’s growth. Overcoming these supply chain issues is crucial for ensuring uninterrupted access to life-saving therapies.

Opportunities

High Occurrence of HIV Infection as an Opportunity

The high occurrence of HIV infection presents a significant opportunity for the blood plasma fractionation market. According to the World Health Organization (WHO), approximately 39.0 million people globally were living with HIV in 2022. This large patient population requires ongoing treatment, including plasma-derived therapies, for managing related complications such as hemophilia or immune deficiency.

The increasing demand for HIV treatments and related medical needs is expected to drive the demand for fractionated plasma products. Additionally, the ongoing need for high-quality, purified plasma-derived therapies for individuals with HIV-related conditions presents an expanding market opportunity. As the global prevalence of HIV remains high, the need for efficient blood plasma fractionation to meet the therapeutic needs of this patient group is projected to grow, benefiting manufacturers in the plasma fractionation sector.

Impact of Macroeconomic / Geopolitical Factors

Macroeconomic and geopolitical factors play a significant role in shaping the blood plasma fractionation market. Economic downturns and increased healthcare spending pressures can limit the ability of governments and institutions to invest in blood plasma fractionation facilities and research. On the other hand, geopolitical instability, such as trade disputes or conflicts in key regions, may disrupt the supply chains that provide essential raw materials like blood plasma.

Additionally, regulatory changes in major markets, such as tightening restrictions or approvals for plasma collection centers, could delay market expansion. Despite these challenges, the global demand for life-saving therapies derived from blood plasma, particularly for immunoglobulins and clotting factors, continues to rise. The focus on improving healthcare access in developing countries and the growing prevalence of conditions such as hemophilia and immunodeficiencies are expected to drive market growth, providing a positive outlook for the sector.

Trends

Rising Surge in Partnerships and Collaborations

Rising partnerships and collaborations are expected to significantly drive the blood plasma fractionation market. High industry consolidation, marked by strategic alliances between key players, has been pivotal in advancing the commercialization of plasma-derived products. In July 2024, Biotest AG announced a collaboration with Kedrion to commercialize and distribute its immunoglobulin product, Yimmugo, across the US, following the FDA’s approval of its Biologic License Application (BLA).

Such collaborations help companies leverage each other’s strengths in research, regulatory approvals, and distribution networks, thereby enhancing product availability and market reach. This surge in partnerships is anticipated to expedite the development of new therapies and improve plasma collection and fractionation processes, ultimately fostering continued market growth.

Regional Analysis

North America is leading the Blood Plasma Fractionation Market

North America dominated the market with the highest revenue share of 40.3% owing to advancements in healthcare and increasing demand for plasma-derived therapies. The approval of ALTUVIIIO Antihemophilic Factor (Recombinant) by the US FDA in February 2023 was a key milestone for the industry, as it offers a new treatment option for individuals living with hemophilia A. The rising prevalence of hemophilia and other blood disorders, coupled with an aging population, has resulted in greater demand for effective plasma-derived treatments.

Additionally, the increasing focus on improving patient outcomes and enhancing the efficiency of plasma fractionation processes has fueled market growth. The expansion of healthcare infrastructure, increasing investments in research and development, and supportive government policies aimed at improving access to treatments also contributed to the market’s expansion. As North America continues to be a hub for cutting-edge biomedical research and innovation, the blood plasma fractionation market is anticipated to maintain strong growth throughout the year.

The Asia Pacific region is expected to experience the highest CAGR during the forecast period

Asia Pacific is expected to grow with the fastest CAGR owing to the region’s increasing healthcare needs and rising adoption of advanced medical therapies. The demand for plasma-derived therapies is anticipated to rise due to the growing prevalence of chronic diseases, such as hemophilia, immunodeficiencies, and autoimmune disorders, which require specialized treatments.

As healthcare systems in countries like China, India, and Japan continue to improve, increased investments in healthcare infrastructure and biotechnology research are likely to support market growth. Additionally, governments in the region are expected to implement favorable policies to boost the availability and affordability of plasma-derived therapies. The increasing focus on enhancing healthcare access and improving the quality of life for patients is projected to drive the demand for blood plasma fractionation services across Asia Pacific in the coming years.

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia

- Netherland

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- New Zealand

- Singapore

- Thailand

- Vietnam

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Key Players Analysis

The major players in the blood plasma fractionation market are actively engaged in the development and introduction of innovative products, as well as implementing strategic initiatives aimed at enhancing their competitive positioning. Key players in the blood plasma fractionation market focus on expanding their product portfolios, enhancing operational efficiency, and improving patient outcomes to drive growth.

Companies prioritize technological advancements such as automated systems for fractionation, which improve yield and purity, while reducing processing time and costs. Strategic mergers, acquisitions, and collaborations with hospitals, blood banks, and pharmaceutical companies help strengthen their market presence and access new markets. Additionally, key players invest in expanding their global reach, particularly in emerging markets, to meet the increasing demand for plasma-derived therapies. They also emphasize compliance with regulatory standards and certifications to ensure product safety and effectiveness.

Grifols, a prominent player in the blood plasma fractionation market, employs a growth strategy centered on innovation, global expansion, and strategic acquisitions. The company focuses on expanding its network of collection centers, while also advancing its fractionation technologies to enhance production efficiency and product quality. Grifols’ portfolio includes a range of plasma-derived therapies for treating conditions like hemophilia and immunodeficiencies. With a strong global presence, Grifols continues to lead in the market through its commitment to research, customer partnerships, and sustainable growth initiatives.

Top Key Players in the Blood Plasma Fractionation Market

- Takeda Pharmaceutical Company Limited

- Shilpa Medicare Limited

- Sanquin

- Octapharma AG

- Grifols S.A.

- CSL Limited

- Biotest AG

Recent Developments

- In January 2024: Takeda shared that the FDA approved its Immune Globulin Infusion 10% solution as a treatment to address neuromuscular disability and impairment in adults suffering from chronic inflammatory demyelinating polyneuropathy.

- In August 2023: Shilpa Medicare Limited successfully completed Phase 1 trials for its recombinant human albumin 20% product.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2023) | US$ 32.7 billion |

| Forecast Revenue (2033) | US$ 68.0 billion |

| CAGR (2024-2033) | 7.6% |

| Base Year for Estimation | 2023 |

| Historic Period | 2019-2022 |

| Forecast Period | 2024-2033 |

| Report Coverage | Revenue Forecast, Market Dynamics, COVID-19 Impact, Competitive Landscape, Recent Developments |

| Segments Covered | By Product Type (Albumin, Immunoglobulin (IVIG and SCIG), Coagulation Factors (Factor IX, Factor VIII, Fibrinogen Concentrates, Prothrombin Complex Concentrates, and Others), Protease Inhibitors, and Others), By Application (Immunology & Neurology, Hematology, Critical Care, Pulmonology, and Others), By End-user (Hospitals & Clinics, Clinical Research Laboratories, and Others) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, New Zealand, Singapore, Thailand, Vietnam, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA |

| Competitive Landscape | Takeda Pharmaceutical Company Limited, Shilpa Medicare Limited, Sanquin, Octapharma AG, Grifols S.A., CSL Limited, and Biotest AG. |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |