Quick Navigation

Report Overview

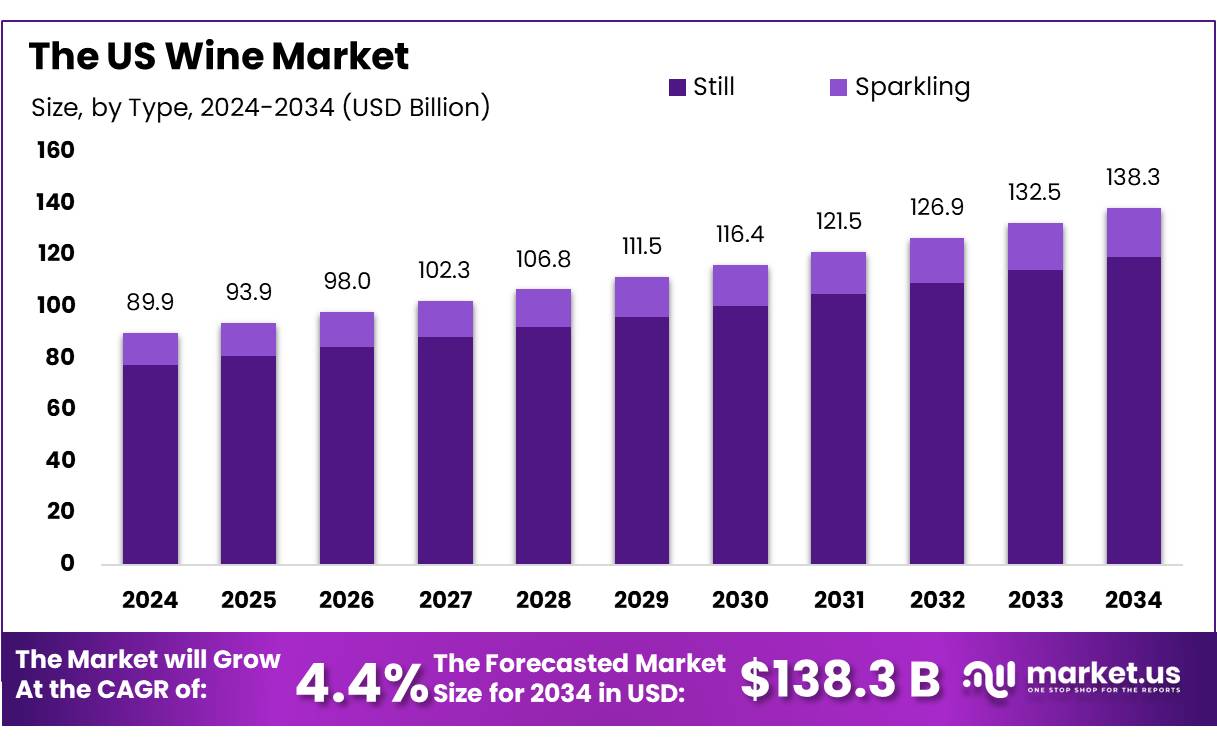

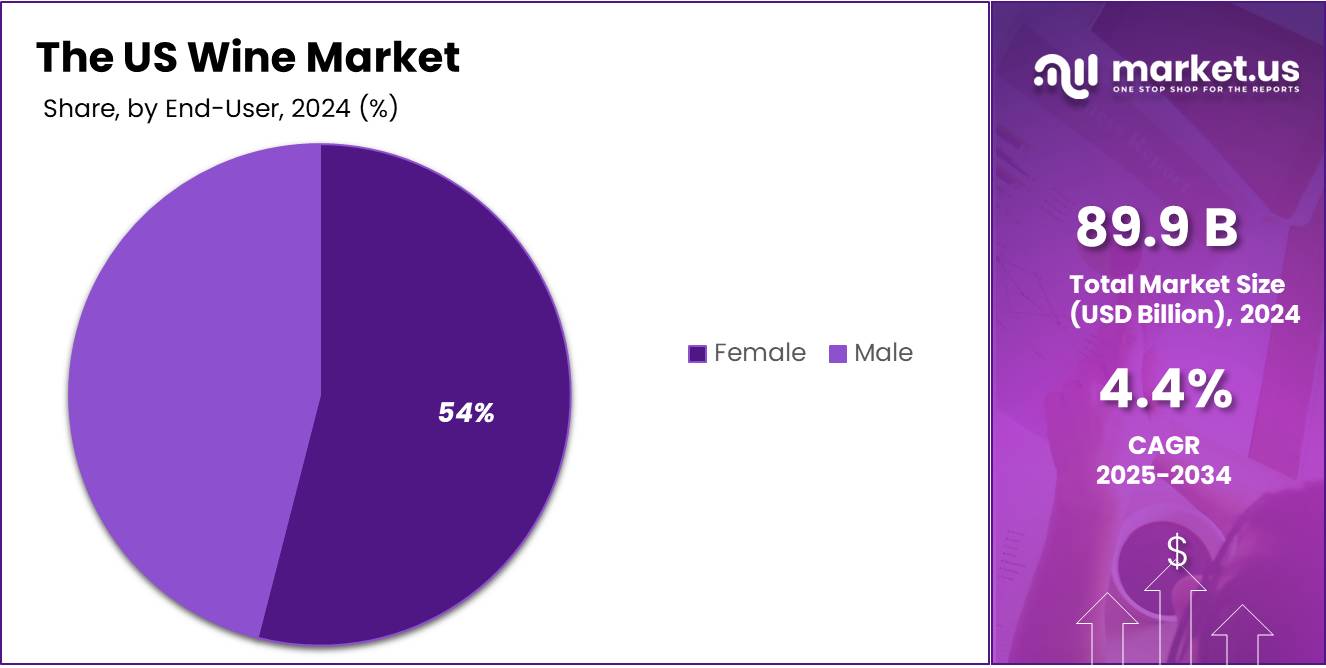

The US Wine Market size is expected to be worth around USD 138.3 Billion by 2034, from USD 89.9 Billion in 2024, growing at a CAGR of 4.4% during the forecast period from 2025 to 2034.

The US wine market, one of the largest in the world, is characterized by significant production and consumption levels. According to USAFacts, the United States produced just over 752 million gallons of wine in 2022, with a staggering 92% of this production coming from four major states: California, Washington, New York, and Oregon. This dominance is reflective of the concentrated nature of wine production in the country, with California leading the charge, contributing 80% of the total wine output.

As per Winefolly, the state is renowned for producing bodacious, fruit-forward wines, particularly from French varieties such as Cabernet Sauvignon, Merlot, Chardonnay, and Pinot Noir. Additionally, US wine consumption is projected to remain stable in 2024, with a per capita consumption of 4.5 liters and a total estimated consumption of 17,800 million liters, according to 8Wines.

The US wine market presents substantial growth opportunities, driven by both domestic and international consumption. With 92% of US wine production coming from a few states like California, Washington, New York, and Oregon, opportunities for expansion lie in diversifying production areas, developing new wine varieties, and tapping into emerging consumer trends such as organic and low-alcohol wines.

The government’s role in this sector is significant, with various regulations that ensure the safe and responsible production and sale of alcohol. Additionally, government investments aimed at research into sustainable farming practices and supporting vineyard development through grants or tax incentives could enhance the sector’s sustainability and long-term growth.

According to industry reports, the overall demand for US wines, particularly in export markets like China and the European Union, continues to expand, reinforcing the need for regulatory frameworks that balance consumer protection with market flexibility.

Key Takeaways

- U.S. Wine Market size is expected to be worth around USD 138.3 Billion by 2034, from USD 89.9 Billion in 2024, growing at a CAGR of 4.4%.

- Still wine held a dominant position in the US wine market, capturing more than an 86.30% share.

- White wine held a dominant position in the US wine market, capturing more than a 52.20% share.

- Cabernet Sauvignon held a dominant market position in the US wine market, capturing more than an 18.40% share.

- Off-trade channels held a dominant market position in the US wine market, capturing more than a 68.50% share.

- Bottles held a dominant position in the US wine market, capturing more than a 93.70% share.

- 36-45 held a dominant market position in the US wine market, capturing more than a 34.50% share.

- Females held a dominant market position in the US wine market, capturing more than a 54.30% share.

By Type

Still Wine Dominates US wine Market with 86.30% Share in 2024

In 2024, Still wine held a dominant position in the US wine market, capturing more than an 86.30% share. The segment has consistently led the market, driven by strong consumer demand for traditional and versatile wine options. The popularity of still wine is further reflected in its year-over-year growth, as consumers continue to favor it for both casual drinking and special occasions. Over the years, this segment has maintained its leading position, with steady demand from wine enthusiasts across various demographics.

Looking ahead to 2025, Still wine is expected to maintain its significant share, though the growth rate may stabilize as consumers start to explore other wine types. Still, the segment remains the go-to choice for a majority of the US wine market, with its wide-ranging appeal and established presence in retail and hospitality sectors.

By Color

White Wine Leads US wine Market with 52.20% Share in 2024

In 2024, White wine held a dominant position in the US wine market, capturing more than a 52.20% share. The segment’s success can be attributed to its broad consumer base, appealing to a wide range of tastes and preferences. White wine has continued to enjoy strong sales, especially during the warmer months, when its refreshing qualities make it a popular choice. The steady growth in consumer interest in lighter, more versatile wine options has helped White wine maintain its stronghold in the market.

Looking ahead to 2025, White wine is expected to remain a top performer in the US market, with its share continuing to be a significant portion of total wine sales. While other segments, such as red or rose, may see growth, White wine’s established appeal and versatility make it a reliable choice for consumers.

By Grape Variety

Cabernet Sauvignon Dominates US Wine Market with 18.40% Share in 2024

In 2024, Cabernet Sauvignon held a dominant market position in the US wine market, capturing more than an 18.40% share. This grape variety remains one of the most popular choices among consumers, thanks to its rich, full-bodied flavor and versatility. Known for its deep color and complex taste, Cabernet Sauvignon is favored in both red wine blends and single-varietal wines, making it a consistent performer in the market. The strong preference for this variety is reflected in its steady growth over the years, supported by its widespread presence in both retail and restaurant settings.

As we move into 2025, Cabernet Sauvignon is expected to continue its dominance in the US wine market. While other grape varieties may show growth, this classic variety’s established fan base and recognition will likely keep it at the forefront of wine sales. Its consistent quality and depth of flavor ensure its position as a staple choice for wine lovers across the country.

By Distribution Channel

Off-Trade Channels Lead US Wine Market with 68.50% Share in 2024

In 2024, Off-trade channels held a dominant market position in the US wine market, capturing more than a 68.50% share. This segment, which includes retail stores, supermarkets, and online platforms, continues to be the preferred method for purchasing wine. Off-trade sales benefit from consumers’ desire for convenience and the ability to purchase wine for home consumption. The rise of e-commerce and home delivery services has further fueled the growth of off-trade channels, providing customers with more options and access to a variety of wine selections.

Looking ahead to 2025, Off-trade channels are expected to maintain their dominant share of the market. With the ongoing trend of online shopping and home-based consumption, the off-trade segment is well-positioned to sustain its leadership, offering a diverse range of wine choices for consumers to enjoy at home or during social gatherings.

By Packaging Type

Bottles Dominates US Wine Market with 93.70% Share in 2024

In 2024, Bottles held a dominant position in the US wine market, capturing more than a 93.70% share. The packaging type has consistently been the preferred choice for consumers due to its convenience, preservation qualities, and widespread availability. Bottled wine remains the most recognizable form of wine, commonly seen in retail stores, restaurants, and at events. This packaging provides a reliable method for maintaining the wine’s quality and freshness, contributing to its continued market leadership.

Looking forward to 2025, Bottles are expected to maintain their dominant share, with little change in consumer preferences. While alternative packaging, such as cans and cartons, may experience some growth, Bottled wine’s traditional appeal and established infrastructure ensure its continued role as the primary packaging format in the US market.

By Age Group

Consumers Aged 36-45 Lead US Wine Market with 34.50% Share in 2024

In 2024, consumers aged 36-45 held a dominant market position in the US wine market, capturing more than a 34.50% share. This age group continues to be a key demographic, as they have a well-established preference for quality wine, balancing between traditional choices and more experimental varieties. Their strong purchasing power and interest in both premium and everyday wines contribute significantly to the overall market growth.

As we look towards 2025, this age group is expected to maintain its leadership in the wine market. With their increasing interest in diverse wine experiences, including wine pairings and emerging wine trends, the 36-45 age group will likely continue to be the primary drivers of demand in the US wine sector. Their influence remains strong, especially as they seek high-quality wines for social events, family gatherings, and personal enjoyment.

By End-User

Females Lead US Wine Market with 54.30% Share in 2024

In 2024, females held a dominant market position in the US wine market, capturing more than a 54.30% share. This demographic has consistently been the largest consumer group, with many women favoring wine for both casual and special occasions. The preference for wine among females is driven by factors such as social trends, lifestyle choices, and the increasing availability of wines tailored to various tastes and occasions. This group’s broad and diverse interest in wine contributes significantly to its market dominance.

Looking ahead to 2025, females are expected to continue holding the largest share in the US wine market. Their increasing involvement in wine culture, from wine tasting events to social media-driven wine communities, will likely sustain their leading position. With more women discovering new wine varieties and brands, this demographic will remain a central force driving growth in the US wine sector.

Key Market Segments

By Type

- Still

- Sparkling

By Color

- White

- Red

- Rose Wine

By Grape Variety

- Cabernet Sauvignon

- Merlot

- Airen

- Tempranillo

- Chardonnay

- Syrah

- Grenache

- Sauvignon Blanc

- Trebbiano Toscana

- Others

By Distribution Channel

- On-trade

- Pubs, Bars & Cafe’s

- Hotels & Restaurants

- Others

- Off -trade

- Supermarkets/Hypermarkets

- Specialty Stores

- Online Stores

By Packaging Type

- Bottles

- Cans

By Age Group

- 18-25 Years

- 26-35 Years

- 36-45 Years

- Above 46 Years

By End-User

- Male

- Female

Drivers

Growing Consumer Preference for Premium Wines Drives Market Expansion

In the United States, the wine market is experiencing significant growth driven primarily by increasing consumer demand for premium wines. This trend reflects a broader shift in consumer preferences towards high-quality and fine wines across various demographics.

The allure of premium wines is not only in their quality but also in the rich, diverse flavors and prestigious branding that come with them, making them highly sought after for both personal enjoyment and social gatherings. Additionally, the growing sophistication of consumers, coupled with a rising interest in gourmet food pairings, has further bolstered the demand for these upscale wines.

This preference for premium offerings is influencing winemakers to focus on crafting exceptional wines that meet the expectations of a discerning clientele, thereby fueling the expansion of the market. The emphasis on quality over quantity is reshaping purchasing patterns and setting new standards in the wine industry, promising sustained growth as consumers continue to pursue the finest wine experiences.

Restraints

High Production Costs Challenge Expansion in the US Wine Market

The US wine market faces significant challenges due to high production costs, which can impede the growth of smaller wineries, particularly in premium segments. The cultivation of wine grapes involves extensive labor and the use of expensive, specialized equipment, not to mention the costs associated with land in prime viticultural areas.

Additionally, the production process itself, from harvesting to bottling, demands substantial investment in technology and manpower. These high upfront costs can be prohibitive for new entrants and smaller producers, limiting their ability to scale operations and compete with larger, established companies. Moreover, the market is also contending with changing consumer preferences.

There is a noticeable shift among consumers, particularly younger demographics, who are increasingly gravitating towards alternative alcoholic beverages like craft beers and spirits. This diversification in consumer tastes can further strain the growth prospects of the wine industry, as producers must innovate and possibly restructure their offerings to capture and retain consumer interest in a highly competitive beverage market.

Growth Factors

Expanding Wine Production in Emerging U.S. Regions Fuels Market Growth

The U.S. wine market presents significant growth opportunities, particularly through the expansion of wine production into emerging regions such as Texas, Washington, and New York. These areas, traditionally less recognized than their Californian or Oregonian counterparts, are now gaining prominence due to their unique climates and terroirs, appealing to a diverse array of consumers and connoisseurs alike.

Additionally, the rising interest in non-alcoholic wines provides an avenue for industry players to cater to a broader demographic, including health-conscious individuals and those opting to decrease their alcohol intake. This trend towards non-alcoholic variants speaks to shifting consumer preferences and opens new segments within the market.

Moreover, the surge in popularity of private label wines offers lucrative prospects for wineries. By collaborating with retailers to produce these labels, wineries can access the expansive mass-market segment, providing affordable options for budget-conscious consumers.

Trends

Organic and Biodynamic Wines Gain Popularity in the US Market

The US wine market is witnessing a notable shift towards organic and biodynamic wines, reflecting a growing consumer demand for environmentally sustainable and ethically produced beverages. This trend is fueled by heightened awareness of environmental issues and health consciousness among consumers, who are increasingly seeking products that align with their values of sustainability and natural production methods.

The appeal of organic and biodynamic wines stems from their minimal use of synthetic chemicals and fertilizers in vineyards, promoting a healthier ecosystem and offering a purer expression of the vineyard’s terroir. Moreover, these wines often carry certifications that assure consumers of their organic and biodynamic status, enhancing their marketability and consumer trust.

This movement towards organic and biodynamic practices is not only shaping consumer preferences but also encouraging winemakers to adopt more sustainable viticulture practices, thereby influencing the broader landscape of the wine industry in the United States.

Key Players Analysis

Constellation Brands is a major player in the alcoholic beverage industry, with a robust portfolio that includes some of the most popular wine brands globally. Known for its focus on premiumization, the company invests heavily in brand development and marketing to cater to upscale consumers. Its strategic acquisitions have broadened its market reach, making it a key influencer in the wine sector’s dynamics.

The Wine Group LLC stands as one of the world’s largest wine producers by volume. The company is celebrated for its cost-effective production methods and wide range of products that appeal to various consumer segments. With a commitment to sustainability and innovation, The Wine Group continues to expand its market share through consumer-focused branding and widespread retail distribution.

Pernod Ricard is a global beacon in the wine and spirits industry, holding a prestigious portfolio of internationally recognized wine labels. The company’s strategy focuses on premiumization and sustainable growth, leveraging its global distribution channels to enhance accessibility and visibility. Pernod Ricard’s emphasis on craftsmanship and heritage in its wine production helps maintain a high level of consumer loyalty and brand strength.

Top Key Players in the Market

- The Wine Group

- Treasury Wine Estates

- Delicato Family Wines

- Bronco Wine Company

- Ste. Michelle Wine Estates

- Jackson Family Wines

- Deutsch Family Wine & Spirits

- Viña Concha Y Toro (Fetzer Vineyards)

- Precept Wine

- Bogle Vineyards

- Vintage Wine Estates

- WX Brands

- The Family Coppola

- C. Mondavi & Family

- Foley Family Wines

- J. Lohr Vineyards & Wines

- Korbel Champagne Cellars

- E & J Gallo Winery

- Constellation Brands

Recent Developments

- In April 2024, Full Glass Wine Co. successfully secured a significant investment of $14 million, enabling them to acquire Bright Cellars, a prominent direct-to-consumer wine subscription brand, enhancing their market presence and service offerings.

- In September 2024, Ferovinum announced a substantial series A funding round amounting to £17.5 million, aimed at investing in the development of their innovative platform, further strengthening their technological capabilities and market reach.

- In December 2024, Butterfly executed a major strategic move by completing the acquisition of The Duckhorn Portfolio for $1.95 billion, significantly expanding their portfolio and reinforcing their position in the premium wine market.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2024) | USD 89.9 Billion |

| Forecast Revenue (2034) | USD 138.3 Billion |

| CAGR (2025-2034) | 4.4% |

| Base Year for Estimation | 2024 |

| Historic Period | 2020-2023 |

| Forecast Period | 2025-2034 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Type (Still, Sparkling), By Color (White, Red, Rose Wine), By Grape Variety (Cabernet Sauvignon, Merlot, Airen, Tempranillo, Chardonnay, Syrah, Grenache, Sauvignon Blanc, Trebbiano Toscana, Others), By Distribution Channel (On-trade, Off -trade), By Packaging Type (Bottles, Cans), By Age Group (18-25 Years, 26-35 Years, 36-45 Years, Above 46 Years), By End-User (Male, Female) |

| Competitive Landscape | The Wine Group, Treasury Wine Estates, Delicato Family Wines, Bronco Wine Company, Ste. Michelle Wine Estates, Jackson Family Wines, Deutsch Family Wine & Spirits, Viña Concha Y Toro (Fetzer Vineyards), Precept Wine, Bogle Vineyards, Vintage Wine Estates, WX Brands, The Family Coppola, C. Mondavi & Family, Foley Family Wines, J. Lohr Vineyards & Wines, Korbel Champagne Cellars, E & J Gallo Winery, Constellation Brands |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |