Quick Navigation

Report Overview

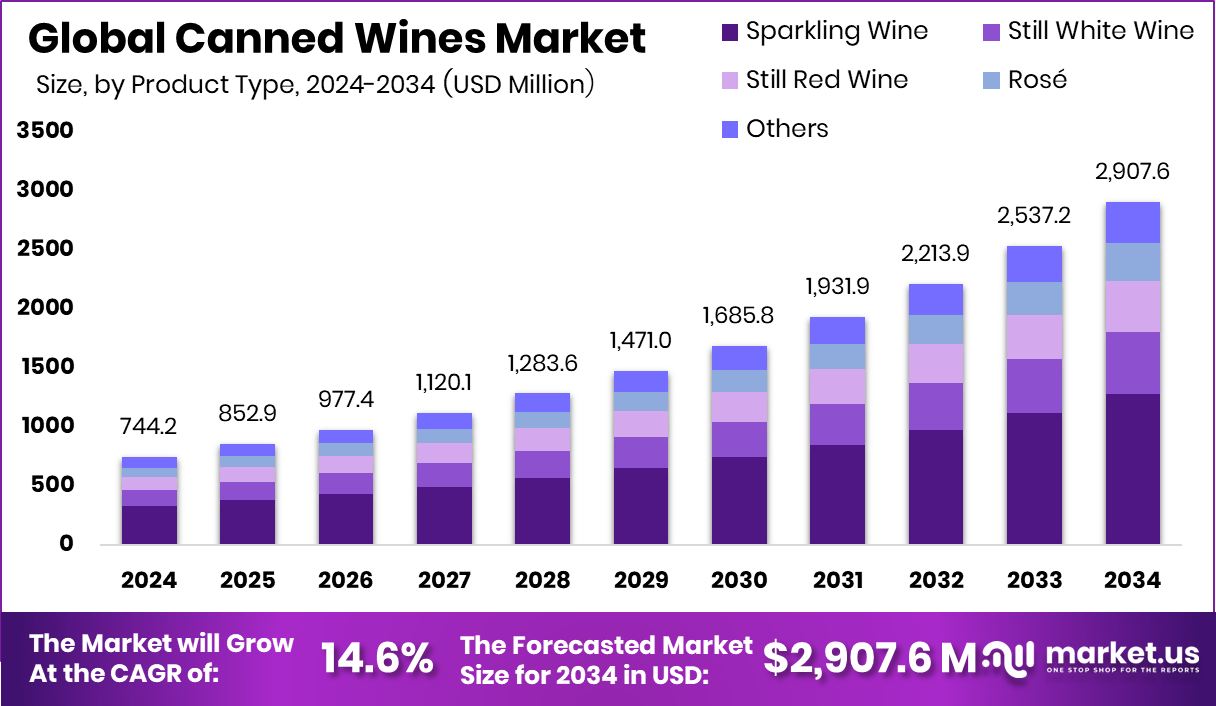

The Global Canned Wines Market is expected to be worth around USD 2,907.6 Million by 2034, up from USD 744.2 Million in 2024, and grow at a CAGR of 14.6% from 2025 to 2034. North America’s 45.20% dominance reflects a rising preference for convenient wine formats across all demographics.

Canned wines are exactly what they sound like: wine packaged in a can instead of the traditional glass bottle. This trend caters to a more casual, convenient, and portable way of enjoying wine. Typically, canned wines are available in smaller, single-serving sizes, making them a great choice for outdoor events, picnics, or when you just want a single glass without opening a whole bottle.

The canned wines market refers to the industry and sales surrounding wines packaged in cans. It encompasses various wine types, from sparkling to still and from red to white, provided in canned form. The market has gained significant traction due to shifting consumer preferences toward more convenient and sustainable packaging options.

In the canned wines market, total imports reached $7.5 billion in FY 2021, expected to increase to $7.7 billion by FY 2022, driven primarily by Italy and France, each supplying $2.5 billion worth of imports. Additionally, a dedicated investment of $250,000 under Colorado’s Senate Bill 21-248 aims to enhance the state’s processing capabilities, signaling robust growth opportunities for canned wine producers in the region.

One of the main growth factors for the canned wines market is the increasing consumer interest in convenient and eco-friendly packaging. Cans are lighter than bottles, reduce the risk of breakage, and are often made from recycled materials, appealing to environmentally conscious consumers. Additionally, the portable nature of cans makes them ideal for new consumption occasions, thus broadening the market.

Demand for canned wines is driven by the millennial and Gen Z demographics, who appreciate not only the convenience and portability but also the casual and approachable image that canned wines offer. This shift is supported by the growing trend of outdoor and informal gatherings where traditional glass bottles might be less practical.

Key Takeaways

- The Global Canned Wines Market is expected to be worth around USD 2,907.6 Million by 2034, up from USD 744.2 Million in 2024, and grow at a CAGR of 14.6% from 2025 to 2034.

- Sparkling wine holds a 44.20% share in the canned wines market, showing strong consumer preference globally.

- The 250 ml (8.4 oz) segment dominates with 56.30%, driven by convenience and single-serve trends.

- Hypermarkets and supermarkets lead sales channels at 38.40%, benefiting from high foot traffic and product visibility.

- North American region’s market value reached USD 336.3 million, showing strong consumer demand.

By Product Type Analysis

Sparkling canned wines dominate the market with 44.20% consumer preference globally.

In 2024, Sparkling Wine held a dominant market position in the By Product Type segment of the Canned Wines Market, with a 44.20% share. This leadership can be attributed to the rising consumer preference for light, refreshing alcoholic beverages, especially among millennials and Gen Z.

Sparkling wines, known for their effervescence and celebratory appeal, have seen growing traction in ready-to-drink formats, aligning well with the convenience trend. The canned format further amplifies this appeal by offering portability, portion control, and sustainability benefits. Consumers increasingly associate canned sparkling wine with casual, outdoor, and on-the-go drinking occasions, expanding its adoption beyond traditional settings.

Additionally, innovative flavor infusions and premium offerings in this segment are capturing attention at retail shelves, enhancing product visibility and consumer trial. The packaging also resonates with eco-conscious buyers due to aluminum cans’ high recyclability. While red and white canned wines continue to hold notable shares, sparkling variants outperform due to their festive image and social-media-friendly aesthetics.

This product type has become particularly popular in markets with evolving alcohol consumption habits and rising disposable incomes. The dominance of sparkling wine in the canned format signifies a strong shift in purchasing behavior, where experience, convenience, and occasion-based drinking are pivotal decision-making drivers.

By Package Size Analysis

The 250 ml size leads with 56.30%, ideal for single servings.

In 2024, 250 ml (8.4 oz) held a dominant market position in the By Package Size segment of the Canned Wines Market, with a 56.30% share. This format has emerged as the preferred choice among consumers due to its convenience, portability, and ideal single-serving portion.

The 250 ml size meets the growing demand for moderation in alcohol consumption, offering consumers a controlled quantity without compromising on experience. It also aligns with the shift toward individual servings, particularly suited for casual, on-the-go, and outdoor settings such as picnics, festivals, and sporting events.

This package size benefits from strong shelf appeal and is easy to chill and consume, which enhances its suitability for immediate consumption. Its dominance is also driven by rising adoption among younger consumers who favor practical, lifestyle-friendly packaging formats.

Retailers and brands increasingly prefer the 250 ml cans for their compatibility with standard display and storage requirements, enabling wider distribution. Moreover, the compact format supports eco-conscious choices, as aluminum cans are lightweight and widely recyclable.

By Sales Channel Analysis

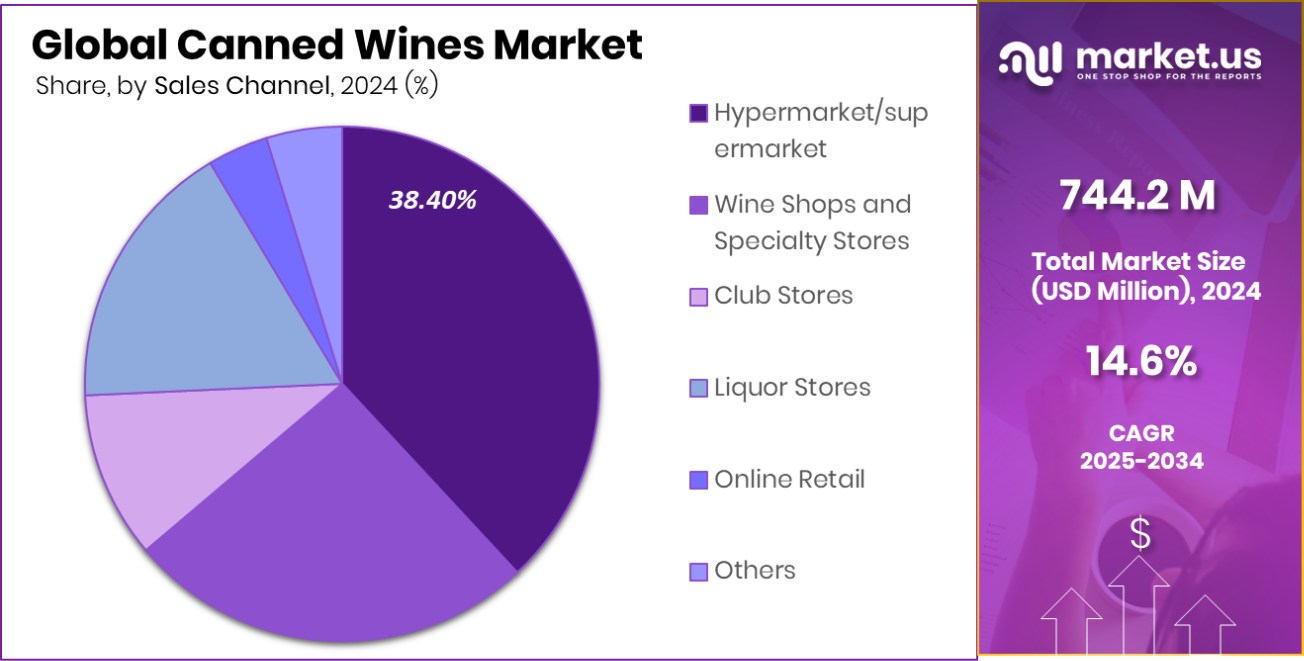

Hypermarkets and supermarkets account for 38.40% of canned wine retail sales.

In 2024, Hypermarket/Supermarket held a dominant market position in the By Sales Channel segment of the Canned Wines Market, with a 38.40% share. This dominance is primarily driven by the wide availability, product variety, and strong in-store promotions offered by these retail formats.

Consumers prefer hypermarkets and supermarkets for their one-stop shopping convenience, allowing them to explore multiple brands and flavors of canned wines in a single visit. These outlets also offer strategic shelf placements, eye-catching displays, and frequent discounts that attract both regular and impulse buyers.

The 38.40% market share also reflects the growing trust consumers place in large retail chains for product authenticity and quality. The format enables easy product comparison, aiding informed decision-making, especially for new buyers. Moreover, supermarkets often serve as trial points for emerging brands, helping them gain visibility and customer traction.

The foot traffic in these stores, combined with seasonal promotions and wine-tasting events, further fuels product adoption. The dominance of this channel showcases how traditional retail continues to play a critical role in influencing beverage purchase decisions, even in a digitally evolving marketplace.

Key Market Segments

By Product Type

- Sparkling Wine

- Still White Wine

- Still Red Wine

- Rosé

- Others

By Package Size

- 250 ml (8.4 oz)

- 375 ml (12.7 oz)

- 187 ml (6.3 oz)

By Sales Channel

- Hypermarket/supermarket

- Wine Shops and Specialty Stores

- Club Stores

- Liquor Stores

- Online Retail

- Others

Driving Factors

Rising Demand for Convenient Alcoholic Beverage Formats

One of the top driving factors for the Canned Wines Market in 2024 is the growing consumer demand for convenience. People now want ready-to-drink alcoholic options that fit into their fast-paced lifestyles.

Canned wines are easy to carry, quick to chill, and simple to open—making them perfect for casual gatherings, picnics, festivals, and travel. Unlike traditional glass bottles, they are lightweight and portable, reducing the risk of breakage.

The single-serve format also appeals to consumers looking for portion control and reduced waste. As a result, many wine brands are launching canned options to meet this trend. This shift in drinking habits, especially among young adults, is fueling strong growth across global markets for canned wines.

Restraining Factors

Perception of Lower Quality Compared to Bottled Wine

A significant challenge facing the canned wine market is the widespread consumer belief that wine in cans is of inferior quality compared to traditional bottled wine. This perception stems from longstanding associations of premium wine with glass bottles and corks, leading many to view canned options as less sophisticated or mass-produced. Despite advancements in canning technology that preserve the wine’s integrity, overcoming this bias remains difficult.

Producers are addressing this by emphasizing the quality of the wine inside the can, highlighting awards, and educating consumers about the benefits of canned packaging. However, changing entrenched perceptions takes time, and this skepticism continues to restrain the market’s growth potential.

Growth Opportunity

Expanding Product Variety to Attract Consumers

A significant growth opportunity in the canned wine market lies in diversifying product offerings to cater to evolving consumer tastes. Introducing a range of wine styles, such as sparkling, rosé, and unique blends, can appeal to a broader audience seeking novelty and variety.

Additionally, offering organic, low-alcohol, or infused options aligns with health-conscious trends and attracts consumers looking for healthier alternatives. Innovative packaging designs and collaborations with artists can further enhance shelf appeal and brand differentiation.

By expanding and innovating their product lines, producers can tap into new market segments and drive growth in the canned wine industry.

Latest Trends

Growing Popularity of Low-Alcohol Canned Wines

A notable trend in the canned wine market is the increasing demand for low-alcohol options. Health-conscious consumers are seeking beverages that allow them to enjoy social occasions without the full effects of traditional alcohol content. Low-alcohol canned wines cater to this preference by offering lighter alternatives that align with wellness-focused lifestyles.

This shift is particularly evident among younger demographics who prioritize moderation and mindful consumption. Producers are responding by expanding their portfolios to include a variety of low-alcohol canned wines, featuring diverse flavors and styles to appeal to this growing segment.

Regional Analysis

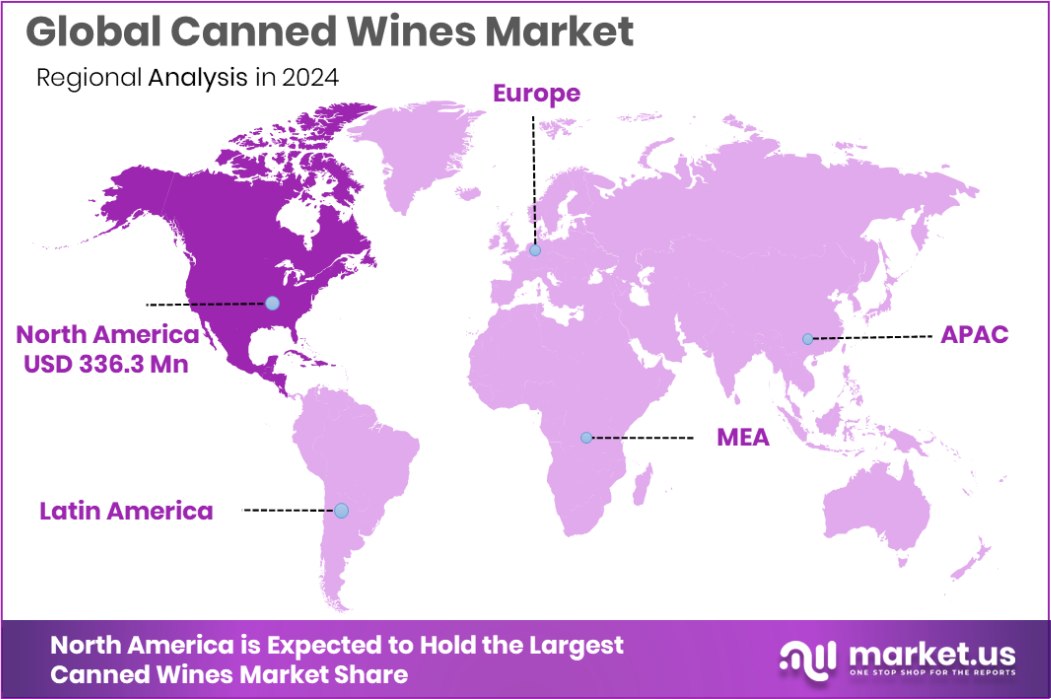

In 2024, North America led the Canned Wines Market with a 45.20% share.

The canned wines market exhibits varied regional dynamics, with North America leading the global landscape. In 2024, North America accounted for the largest market share of 45.20%, valued at USD 336.3 million. This dominance is attributed to growing consumer preference for convenient alcoholic beverages and increased adoption among millennials and outdoor enthusiasts.

Europe follows closely, driven by the evolving drinking culture and rising demand for sustainable packaging across countries like Germany, France, and the UK. Asia Pacific is emerging as a promising market, supported by the rising urban population, expanding middle class, and increasing awareness of Western lifestyle trends, particularly in Japan, South Korea, and Australia. The Middle East & Africa market remains relatively niche but shows potential in premium product segments within urban centers.

Latin America is witnessing steady growth, especially in countries like Brazil and Argentina, where wine consumption is culturally embedded, and younger consumers are open to alternative wine formats. Overall, the market is benefiting from lifestyle shifts, portability demands, and the growing popularity of single-serve alcohol solutions.

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

In 2024, the global canned wines market is expected to continue its expansion, with brands like JOIY Wine, Lila Wines, and Maker Wine Company playing crucial roles in shaping consumer preferences and market dynamics.

JOIY Wine is positioning itself as a premium player in the canned wine space. Known for its high-quality, sustainably sourced products, JOIY Wine capitalizes on the growing demand for eco-friendly and convenient wine options. Its product portfolio emphasizes a mix of accessible flavors with a focus on health-conscious choices, appealing to younger, environmentally aware consumers.

By combining superior packaging with excellent taste profiles, JOIY Wine sets a high standard in the canned wine market, attracting both casual drinkers and wine aficionados seeking a portable yet premium experience.

Lila Wines, another significant player, focuses on innovation within the canned wine sector. With a strong emphasis on organic, sustainable, and small-batch production, Lila Wines appeals to a niche market of eco-conscious and health-conscious consumers. Its unique offerings challenge traditional wine perceptions, driving growth in markets where consumers are increasingly interested in artisanal and craft options.

Maker Wine Company, distinguished by its commitment to collaborating with small wineries, takes a community-driven approach to the canned wine market. By offering wines from boutique wineries, Maker Wine caters to consumers seeking distinct, high-quality wines with a story behind them. This strategy builds loyalty among niche consumers who value both quality and sustainability.

Top Key Players in the Market

- Archer Roose Wines

- Babe Wine

- Canned Wine Co.

- E. & J. Gallo Winery

- House Wine

- JOIY Wine

- Lila Wines

- Maker Wine Company

- Ramona

- Sans Wine Co.

- SUNTORY HOLDINGS LIMITED

- The Infinite Monkey Theorem

- Underwood

Recent Developments

- In March 2025, Archer Roose expanded its product line by introducing an Australian Pinot Noir crafted by winemaker Courteney Wills in Victoria. This 13% ABV wine marked the brand’s first national launch, aiming to diversify its offerings and appeal to a broader audience.

- In December 2024, Full Glass Wine Co. expanded its direct-to-consumer presence by acquiring Wine Access and Cameron Hughes Wine, projecting sales to exceed $200 million by the end of 2025.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2024) | USD 744.2 Million |

| Forecast Revenue (2034) | USD 2,907.6 Million |

| CAGR (2025-2034) | 14.6% |

| Base Year for Estimation | 2024 |

| Historic Period | 2020-2023 |

| Forecast Period | 2025-2034 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Product Type (Sparkling Wine, Still White Wine, Still Red Wine, Rosé, Others), By Package Size (250 ml (8.4 oz), 375 ml (12.7 oz), 187 ml (6.3 oz)), By Sales Channel (Hypermarket/supermarket, Wine Shops and Specialty Stores, Club Stores, Liquor Stores, Online Retail, Others) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – GCC, South Africa, Rest of MEA |

| Competitive Landscape | Archer Roose Wines, Babe Wine, Canned Wine Co., E. & J. Gallo Winery, House Wine, JOIY Wine, Lila Wines, Maker Wine Company, Ramona, Sans Wine Co., SUNTORY HOLDINGS LIMITED, The Infinite Monkey Theorem, Underwood |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |