Quick Navigation

Report Overview

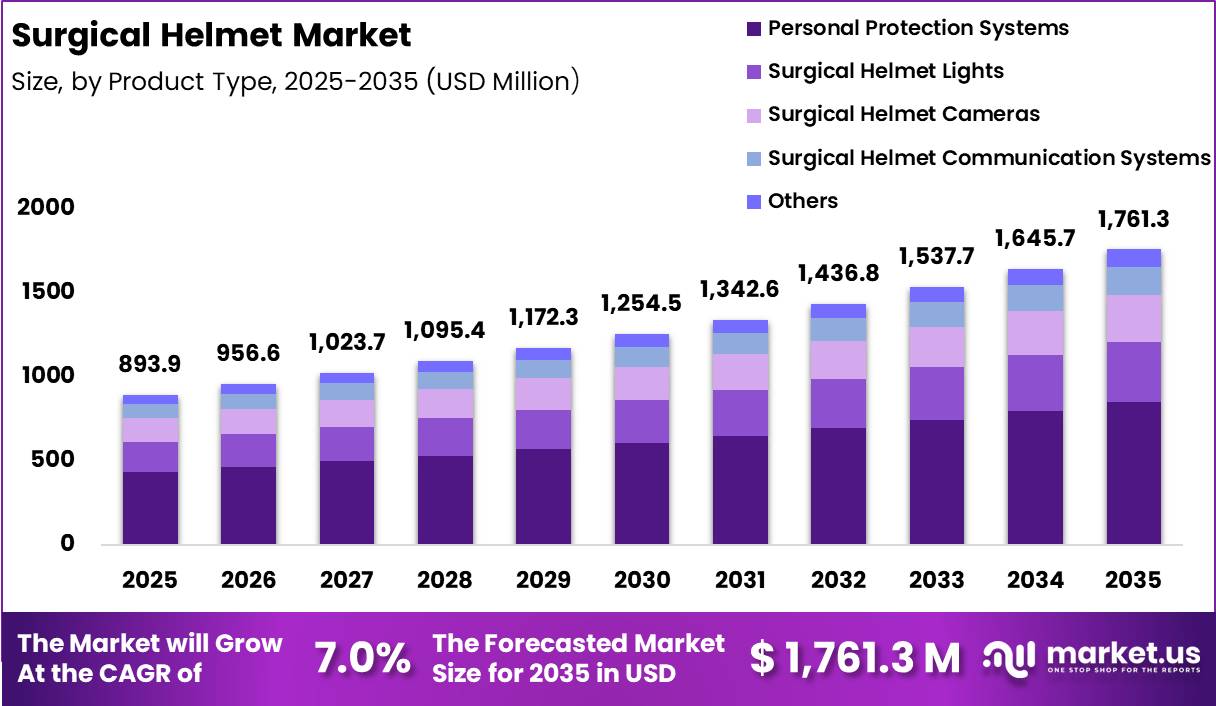

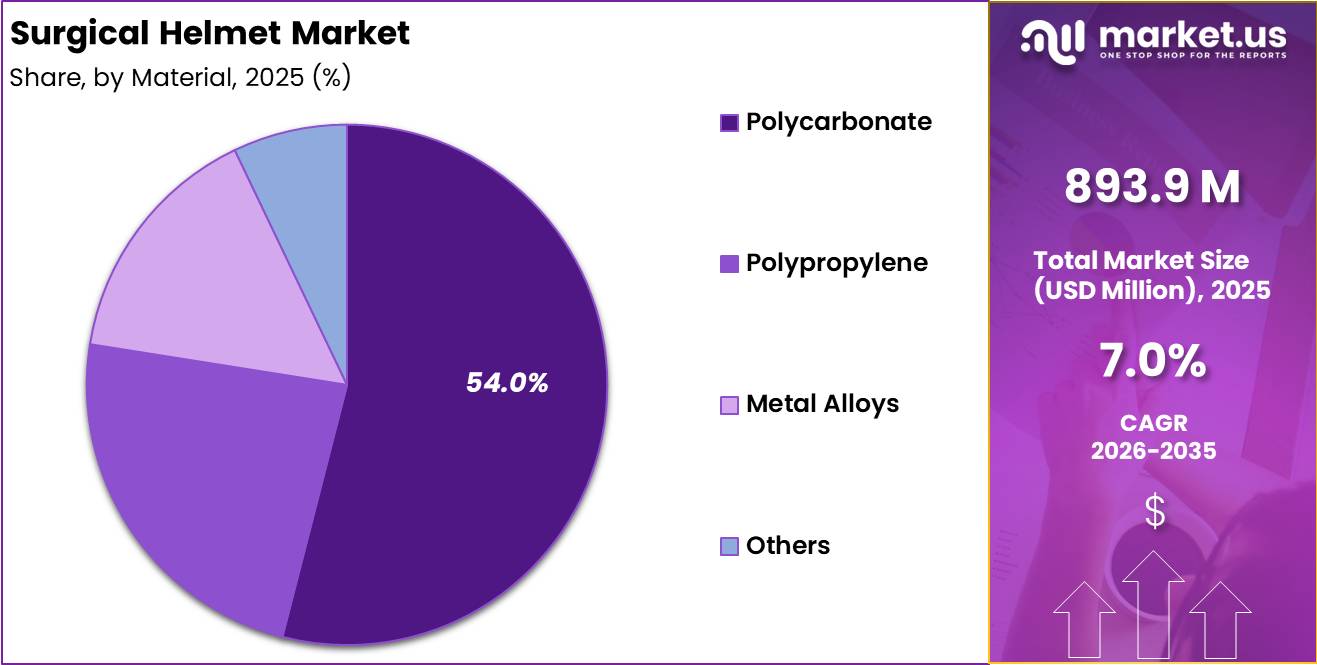

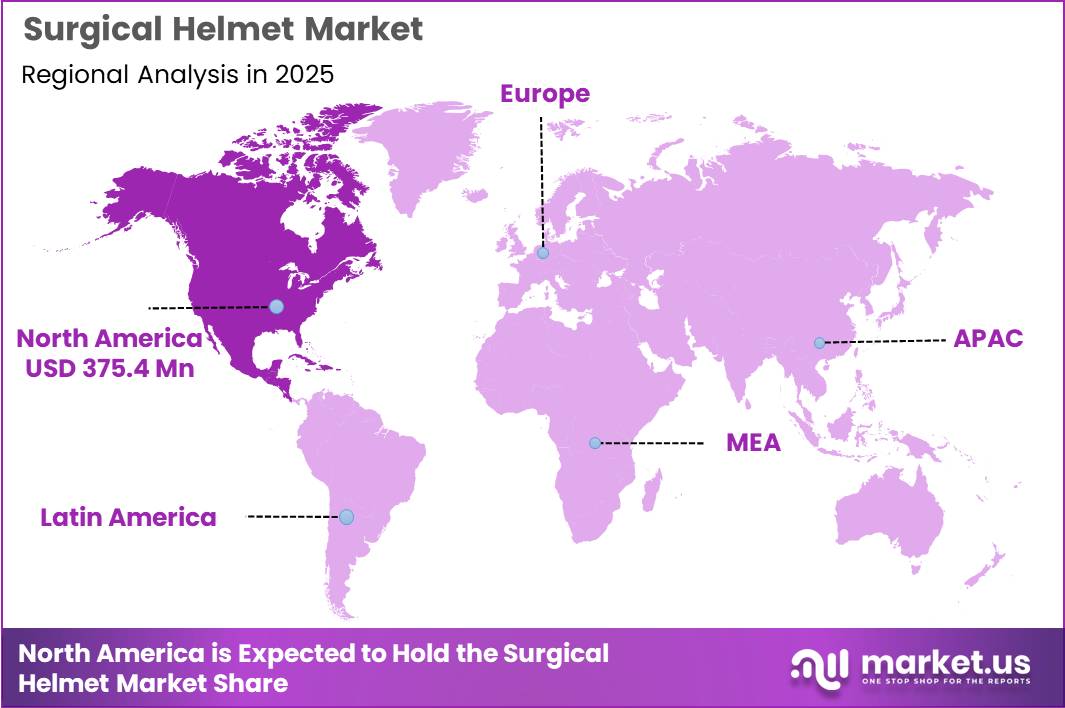

Global Surgical Helmet Market size is expected to be worth around US$ 1,761.3 Million by 2035 from US$ 893.9 Million in 2025, growing at a CAGR of 7.0% during the forecast period from 2026 to 2035. In 2025, North America led the market, achieving over 42.0% share with a revenue of US$ 375.4 Million.

The Surgical Helmet Market is witnessing steady growth due to the rising emphasis on infection prevention, occupational safety, and sterile operating environments across healthcare facilities worldwide. Surgical helmets are specialized protective headgear systems used by surgeons and operating room personnel during complex surgical procedures, particularly orthopedic, trauma, neurosurgical, and joint replacement surgeries.

These systems are designed to minimize exposure to bloodborne pathogens, surgical smoke, and airborne contaminants while maintaining a sterile surgical field. Modern surgical helmets are increasingly integrated with powered air-purifying respirators (PAPRs), anti-fog face shields, cooling systems, and communication modules to improve both safety and comfort for healthcare professionals.

The increasing incidence of surgical site infections (SSIs) remains a major factor supporting market expansion. According to the World Health Organization (WHO), surgical site infections affect millions of patients annually, with approximately 11% of surgical patients in low- and middle-income countries developing infections during hospitalization.

In the United States alone, SSIs contribute to more than 400,000 additional hospital days and nearly US$900 million in extra healthcare costs every year. These concerns have significantly increased the adoption of advanced protective equipment, including surgical helmets, across hospitals and ambulatory surgical centers.

Growing awareness regarding the hazards of surgical smoke and airborne contaminants is further accelerating demand. The U.S. Centers for Disease Control and Prevention (CDC) and Occupational Safety and Health Administration (OSHA) reported that more than 500,000 healthcare workers are exposed annually to surgical smoke generated during laser and electrosurgical procedures. Surgical smoke may contain toxic gases, viral particles, and harmful bioaerosols that can negatively impact respiratory health. Consequently, hospitals are increasingly investing in advanced surgical helmet systems with respiratory protection features.

The rising volume of orthopedic and trauma surgeries is also contributing to market growth. Increasing road accidents, sports injuries, and age-related musculoskeletal disorders are driving the demand for surgical interventions globally. Additionally, the rapidly aging population continues to increase the burden of chronic diseases requiring surgery.

According to the United Nations, the global population aged 65 years and above is expected to rise significantly, with one in six individuals projected to be over 65 years old by 2050. This demographic trend is expected to sustain long-term demand for surgical procedures and associated infection prevention equipment, including surgical helmets.

Key Takeaways

- Market Size: Global Surgical Helmet Market size is expected to be worth around US$ 1,761.3 Million by 2035 from US$ 893.9 Million in 2025.

- Market Share: The market growing at a CAGR of 7.0% during the forecast period from 2026 to 2035.

- Product Type Analysis: Personal Protection Systems accounted for the largest market share of 48.5% in 2025.

- End User Analysis: Hospitals dominated the market with a 55.9% share in 2025.

- Material Analysis: Polycarbonate emerged as the dominant material segment, accounting for 54.0% of the market share in 2025.

- Regional Analysis: In 2025, North America led the market, achieving over 42.0% share with a revenue of US$ 375.4 Million.

Product Type Analysis

The product type segment of the Surgical Helmet Market is categorized into Personal Protection Systems, Surgical Helmet Lights, Surgical Helmet Cameras, Surgical Helmet Communication Systems, and Others. Personal Protection Systems accounted for the largest market share of 48.5% in 2025, owing to their critical role in minimizing contamination risks and enhancing surgeon safety during complex surgical procedures.

The increasing emphasis on infection prevention protocols in operating rooms, particularly during orthopedic and trauma surgeries, has significantly supported the adoption of advanced personal protection systems. These systems provide integrated airflow management, face shielding, and respiratory protection, thereby improving surgical efficiency and comfort.

Surgical Helmet Lights are witnessing growing demand due to the rising requirement for improved surgical visibility and precision in minimally invasive and long-duration procedures. Surgical Helmet Cameras are increasingly being adopted for medical training, documentation, and remote consultation applications, supporting procedural transparency and educational purposes.

Meanwhile, Surgical Helmet Communication Systems are gaining traction as healthcare facilities focus on improving coordination among surgical teams in high-noise operating environments. The Others segment includes customized accessories and integrated components designed to enhance operational convenience and ergonomic performance in surgical settings.

End User Analysis

Based on end user, the Surgical Helmet Market is segmented into Hospitals, Ambulatory Surgical Centers, Specialty Orthopedic Centers, and Others. Hospitals dominated the market with a 55.9% share in 2025, primarily due to the high volume of surgical procedures conducted in multi-specialty and tertiary healthcare facilities.

The availability of advanced surgical infrastructure, skilled healthcare professionals, and stringent infection control standards has accelerated the adoption of surgical helmet systems across hospitals globally. Furthermore, the increasing prevalence of orthopedic disorders, trauma injuries, and joint replacement procedures continues to support segment growth.

Ambulatory Surgical Centers are experiencing notable expansion due to the growing preference for outpatient surgical procedures and cost-effective healthcare delivery models. These facilities increasingly utilize surgical helmet systems to maintain sterile conditions and improve procedural safety during same-day surgeries.

Specialty Orthopedic Centers also represent a significant segment, driven by the rising number of sports injuries, musculoskeletal disorders, and complex orthopedic interventions requiring enhanced protective equipment. The Others segment comprises military healthcare facilities, academic medical institutions, and specialty clinics where surgical helmet systems are utilized for infection prevention and surgical precision enhancement in specialized procedures.

Material Analysis

Based on material, the Surgical Helmet Market is segmented into Polycarbonate, Polypropylene, Metal Alloys, and Others. Polycarbonate emerged as the dominant material segment, accounting for 54.0% of the market share in 2025. The segment growth is attributed to the material’s superior impact resistance, lightweight structure, optical clarity, and durability, making it highly suitable for surgical helmet manufacturing.

Polycarbonate-based helmets provide enhanced visibility and comfort for surgeons during extended procedures while maintaining high safety standards in operating environments. Additionally, the increasing focus on ergonomically designed protective equipment has further supported the adoption of polycarbonate materials.

Polypropylene is gaining steady demand due to its cost-effectiveness, chemical resistance, and lightweight properties, which make it suitable for disposable or semi-reusable helmet components. Metal Alloys are primarily utilized in structural reinforcement applications where durability and long-term performance are essential.

These materials are preferred in high-performance surgical systems requiring enhanced stability and mechanical strength. The Others segment includes composite materials and advanced polymers designed to improve airflow management, thermal resistance, and user comfort. Continuous innovations in material engineering are expected to support the development of more efficient and lightweight surgical helmet systems over the forecast period.

Application Analysis

Based on application, the Surgical Helmet Market is segmented into Orthopedic Surgery, Trauma Surgery, Dental Surgery, Joint Replacement, and Others. Orthopedic Surgery held the leading market share of 58.0% in 2025, driven by the increasing number of musculoskeletal procedures, fracture treatments, and spinal surgeries performed worldwide.

Surgical helmet systems are widely adopted in orthopedic surgeries due to the high risk of exposure to blood particles, bone fragments, and airborne contaminants during lengthy procedures. The growing aging population and rising incidence of osteoporosis and degenerative bone disorders have further contributed to segment expansion.

Trauma Surgery represents a significant application segment owing to the increasing incidence of road accidents, sports injuries, and emergency surgical interventions requiring enhanced protective equipment. Dental Surgery is witnessing gradual adoption of surgical helmet systems as infection prevention and operator safety become increasingly important in specialized dental procedures.

Joint Replacement procedures are also contributing substantially to market growth due to the rising demand for hip and knee replacement surgeries among elderly populations. The Others segment includes neurosurgery, cardiovascular surgery, and specialized surgical applications where advanced protective systems are utilized to maintain sterile operating environments and improve surgical safety.

Key Market Segments

By Product Type

- Personal Protection Systems

- Surgical Helmet Lights

- Surgical Helmet Cameras

- Surgical Helmet Communication Systems

- Others

By End User

- Hospitals

- Ambulatory Surgical Centers

- Specialty Orthopedic Centers

- Others

By Material

- Polycarbonate

- Polypropylene

- Metal Alloys

- Others

By Application

- Orthopedic Surgery

- Trauma Surgery

- Dental Surgery

- Joint Replacement

- Others

Driving Factors

A key driver for surgical helmets is the rising incidence of airborne and splash-borne infections during orthopedic and trauma surgeries, which generate high-velocity aerosols and blood splatter. For example, the U.S. Centers for Disease Control and Prevention (CDC) emphasizes head and eye protection in operating-room protocols to reduce exposure to bloodborne pathogens such as HIV, HBV, and HCV, whose transmission risk can reach 1–3% per sharps injury or splash to mucous membranes.

Surgical helmets with filtered ventilation and visors lower droplet contamination by up to 90% compared with standard caps and eyewear in certain high-energy procedures like percutaneous nephrolithotomy. India’s National Health Mission and Ministry of Health guidelines also stress improved personal protective equipment (PPE) in operative settings, especially in understaffed tertiary centers that report higher nosocomial infection rates.

As surgical volumes rise globally for instance, India performs over 20 million inpatient surgeries annually demand for helmets that integrate airflow, lighting, and ergonomic fit grows, reinforcing their role as a core infection-control investment rather than optional gear.

Trending Factors

Current trends show a shift from simple caps and face shields to integrated helmet systems that combine ventilation, LED illumination, and anti-fog visors, particularly in orthopedics, neurosurgery, and spine procedures. The World Health Organization’s “Safe Surgery Saves Lives” initiative highlights that laminar-air-flow-equipped helmets can cut microbial contamination of the surgical field by around 40–60% compared with conventional garments, especially in high-dust environments such as joint-replacement surgeries.

In India, the National Health Systems Resource Centre and Ministry of Health recommend airflow-assisted PPE for high-aerosol procedures, aligning with global OR-safety guidelines. Peer-reviewed studies, including those referenced via open-science portals, observe that surgeons using helmet systems report 20–30% lower heat-stress scores and around 15% fewer intraoperative fogging-related interruptions, improving procedural continuity.

These helmets are increasingly adopted in tier-2 and tier-3 hospitals where infection-control infrastructure is being upgraded under national health-system-strengthening programs. As tele-surgery and augmented-reality-assisted operations grow, helmets with in-helm-display feeds and camera integration are emerging as standard adjuncts, further embedding airflow-protected headgear into modern surgical practice.

Restraining Factors

A major restraint on surgical-helmet adoption is cost, particularly in low- and middle-income settings such as much of India’s public-health network. A single advanced helmet system, including filtered ventilation, LED headlamp, and reusable visor assembly, can cost several hundred U.S. dollars, with separate expenses for disposable hoods, filters, and battery packs, pushing total-cost-of-ownership per unit into the thousands of dollars over five years.

Government-run tertiary hospitals under schemes such as the Central Government Health Scheme and Employees’ State Insurance Corporation often prioritize capital expenditure on imaging and dialysis equipment over protective headgear, given constrained budgets. In addition, regulatory and maintenance complexity slows rollout: India’s Central Drugs Standard Control Organisation and similar regulators require conformity-assessment and periodic re-testing of medical-device-style helmets, which many small- and mid-size hospitals lack in-house capacity to manage.

Clinical studies from government-affiliated registries, such as those in New Zealand, also note that poorly maintained or low-quality helmet systems can paradoxically increase contamination if airflow is suboptimal or visors are not properly sanitized between cases. These factors collectively limit helmets to reference-tertiary centers and high-volume private hospitals, leaving many public-sector facilities reliant on basic caps and goggles despite higher exposure risk.

Opportunity

The opportunity lies in aligning surgical-helmet deployment with national-level infection-control and surgical-safety programs in countries such as India, where public-sector restructuring emphasizes standardized PPE and OR-safety protocols. India’s Ayushman Bharat and National Health Mission initiatives have funded over 150,000 new health-and-wellness centers and upgraded hundreds of district hospitals, creating a natural pipeline for approved helmet systems as part of bundled OR-safety packages.

Globally, healthcare agencies project that, if infection-control equipment is prioritized, helmet penetration could rise from single-digit percentages in many public hospitals today to over 30% of high-aerosol procedures by 2030–2034, driven by evidence linking airflow-protected headgear to 20–40% lower surgical-site-infection rates in certain orthopedic and trauma cohorts.

For manufacturers, this opens scope for tiered, government-procurement-friendly models lower-cost, modular helmets with standardized filters and rechargeable batteries that comply with India’s Medical Device Rules while remaining affordable for district-level hospitals. Public-private partnerships can further scale access: for example, bundling helmet systems with national-level surgical-training programs or WHO-backed “surgical safety checklist” rollouts can accelerate adoption while generating real-world data on infection and staff-compliance outcomes.

Regional Analysis

In 2025, North America dominated the Surgical Helmet Market, accounting for over 42.0% of the global market share and generating revenue of approximately US$ 375.4 million. The regional market growth is primarily supported by the strong presence of advanced healthcare infrastructure, high surgical procedure volumes, and increasing adoption of technologically advanced surgical safety equipment across hospitals and ambulatory surgical centers.

The United States represented the largest contributor within the region due to rising awareness regarding infection prevention and occupational safety among healthcare professionals. In addition, favorable reimbursement policies and significant healthcare expenditure have accelerated the adoption of surgical helmets in orthopedic, neurosurgical, and trauma-related procedures.

The growing prevalence of musculoskeletal disorders and sports injuries has further increased the demand for joint replacement and minimally invasive surgeries, thereby supporting market expansion. Moreover, the presence of leading medical device manufacturers and continuous investments in product innovation have strengthened the regional competitive landscape.

Canada also contributed steadily to market growth owing to improvements in surgical facilities and increasing government initiatives focused on healthcare modernization. Furthermore, stringent regulatory standards related to surgical hygiene and patient safety continue to encourage healthcare institutions across North America to adopt advanced surgical helmet systems, supporting sustained market growth throughout the forecast period.

Key Regions and Countries

North America

- The US

- Canada

Europe

- Germany

- France

- The U.K.

- Italy

- Spain

- Russia & CIS

- Rest of Europe

Asia Pacific

- China

- India

- Japan

- South Korea

- ASEAN

- Australia & New Zealand

- Rest of Asia Pacific

Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

Latin America

- Brazil

- Mexico

- Rest of Latin America

Key Players Analysis

The Surgical Helmet Market is moderately consolidated, with competition characterized by product innovation, strategic partnerships, and expansion of distribution networks. Key market players are focusing on developing advanced surgical helmet systems with improved ventilation, lightweight materials, enhanced visibility, and integrated infection control features to strengthen their market presence. Companies are also investing significantly in research and development activities to improve surgeon comfort and operational efficiency during lengthy surgical procedures.

Major manufacturers are increasingly adopting merger and acquisition strategies to expand their product portfolios and geographical reach. In addition, collaborations with hospitals and healthcare institutions are supporting product adoption and long-term supply agreements. The competitive landscape is further influenced by stringent regulatory requirements and the growing emphasis on surgical safety standards across healthcare facilities.

Leading players are also concentrating on expanding their presence in emerging economies, where healthcare infrastructure development and rising surgical volumes are creating new growth opportunities. Continuous technological advancements and increasing demand for disposable and reusable surgical helmet systems are expected to intensify market competition over the forecast period.

Market Key Players

- Stryker Corporation

- Mölnlycke Health Care AB

- Zimmer Biomet Holdings, Inc.

- Microtek Medical (Ecolab)

- Surgitel

- Integra LifeSciences Corporation

- BVI Medical

- Clariton

- Sklar Surgical Instruments

- Ossur hf.

- Hologic Inc.

- B. Braun Melsungen AG

- Synergy Health

- Aspen Surgical

- Paul Hartmann AG

- Others

Recent Developments

- March 2025 – Stryker Corporation launched the Steri-Shield 8 Personal Protection System, a next-generation surgical helmet and protection solution designed to improve surgeon comfort, airflow management, and infection prevention during orthopedic and high-risk procedures. The launch reflects growing investment in advanced surgical PPE technologies.

- January 2025 – Zimmer Biomet Holdings, Inc. announced plans to acquire Paragon 28 in a deal valued at approximately USD 1.1 billion. The acquisition was aimed at strengthening the company’s orthopedic surgery and extremities portfolio, particularly in foot and ankle reconstruction technologies.

- Mölnlycke Health Care AB – 2025 – Mölnlycke Health Care AB continued to strengthen its infection prevention and surgical safety portfolio through ongoing investments in surgical solutions and healthcare efficiency initiatives.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | US$ 893.9 Million |

| Forecast Revenue (2035) | US$ 1,761.3 Million |

| CAGR (2026-2035) | 7.0% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Product Type (Personal Protection Systems, Surgical Helmet Lights, Surgical Helmet Cameras, Surgical Helmet Communication Systems, Others) By End User (Hospitals, Ambulatory Surgical Centers, Specialty Orthopedic Centers, Others) By Material (Polycarbonate, Polypropylene, Metal Alloys, Others) By Application (Orthopedic Surgery, Trauma Surgery, Dental Surgery, Joint Replacement, Others) |

| Regional Analysis | North America – The US, Canada; Europe – Germany, France, U.K., Italy, Spain, Russia & CIS, Rest of Europe; Asia Pacific – China, India, Japan, South Korea, ASEAN, Australia & New Zealand, Rest of Asia Pacific; Middle East & Africa – GCC, South Africa, Rest of Middle East & Africa; Latin America – Brazil, Mexico, Rest of Latin America |

| Competitive Landscape | Stryker Corporation, Mölnlycke Health Care AB, Zimmer Biomet Holdings, Inc., Microtek Medical (Ecolab), Surgitel, Integra LifeSciences Corporation, BVI Medical, Clariton, Sklar Surgical Instruments, Ossur hf., Hologic Inc., B. Braun Melsungen AG, Synergy Health, Aspen Surgical, Paul Hartmann AG, Others |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |