Global Sex Reassignment Surgery Market By Surgery Type (Male-to-Female (MTF) Surgery and Female-to-Male (FTM) Surgery), By Procedure Type (Facial Feminization / Masculinization Surgery, Breast Augmentation / Mastectomy, Hysterectomy / Orchidectomy, Vaginoplasty / Phalloplasty / Metoidioplasty and Others (Scrotoplasty, Body Contouring, Tracheal Shave)), By End User (Hospitals, Specialty Clinics and Ambulatory Surgical Centers), Region and Companies – Industry Segment Outlook, Market Assessment, Competition Scenario, Trends and Forecast 2026-2035

- Published date: March 2026

- Report ID: 182179

- Number of Pages: 358

- Format:

-

keyboard_arrow_up

Quick Navigation

Report Overview

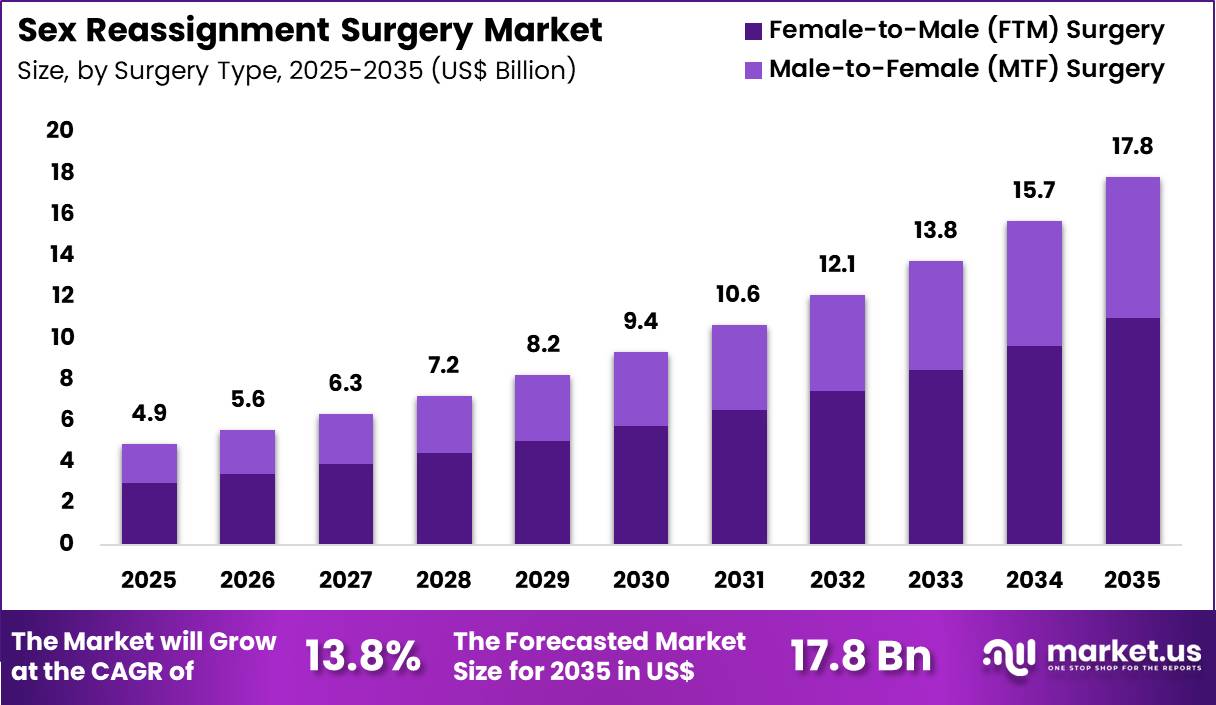

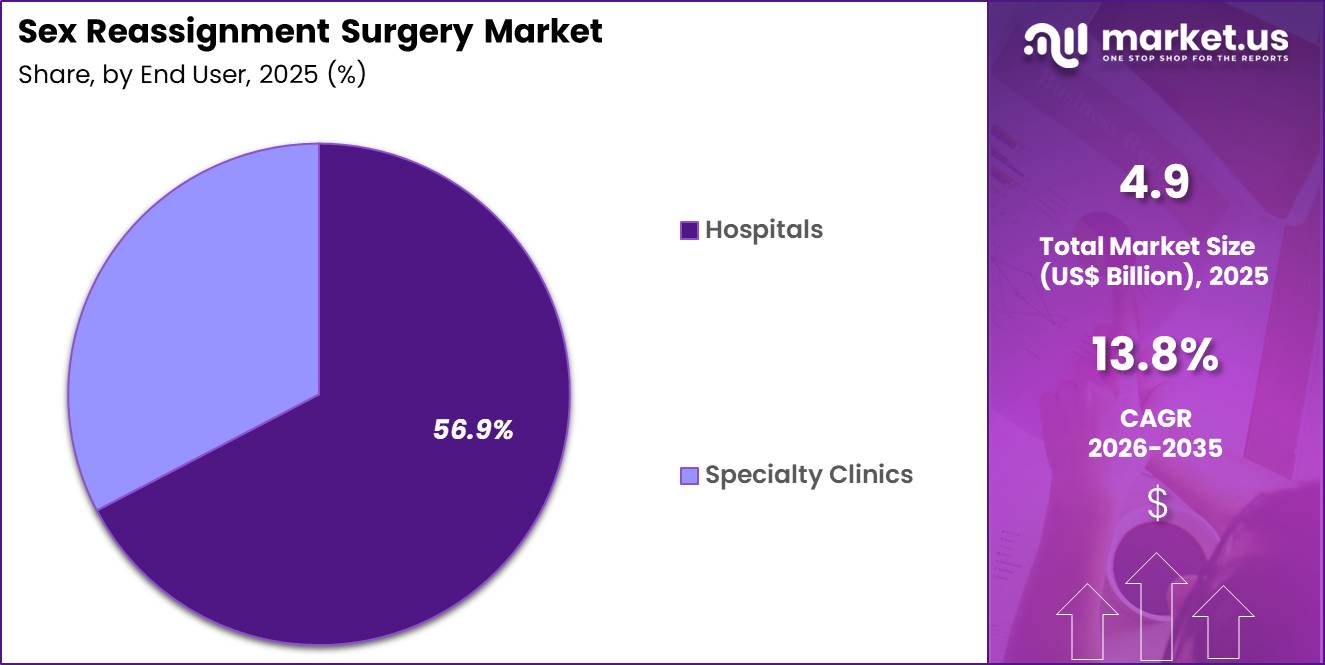

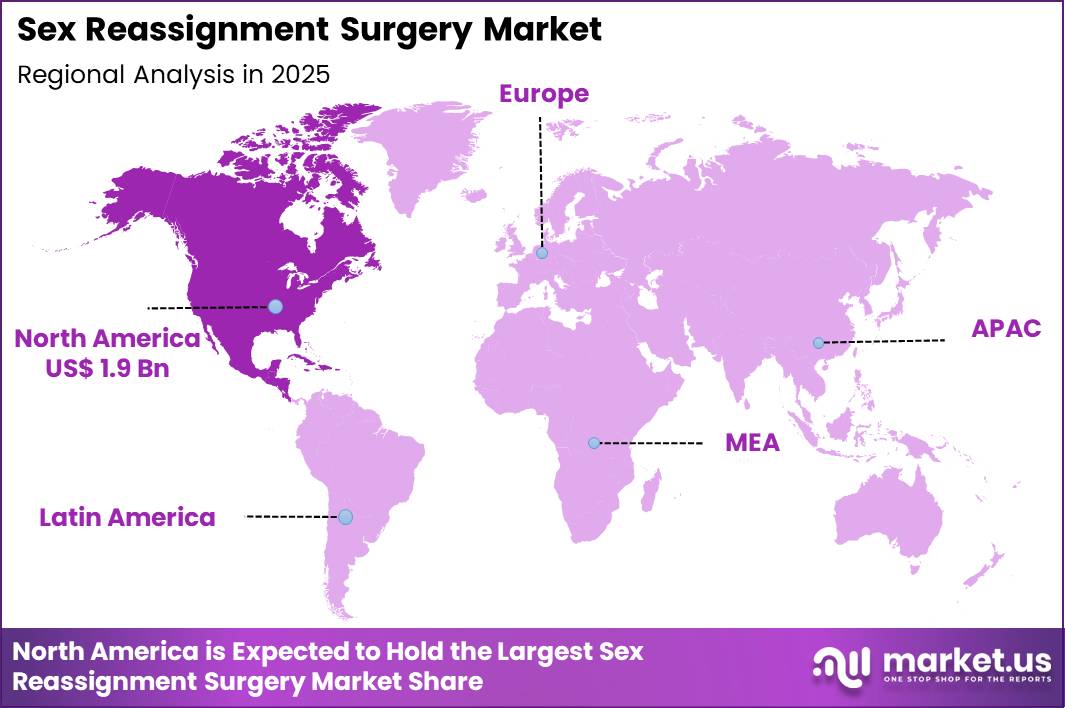

The Sex Reassignment Surgery Market size is expected to be worth around US$ 17.8 Billion by 2035 from US$ 4.9 Billion in 2025, growing at a CAGR of 13.8% during the forecast period 2026-2035. In 2025, North America led the market, achieving over 39.6% share with a revenue of US$ 1.9 Billion.

Growing recognition of gender-affirming care as an essential medical service propels the Sex Reassignment Surgery market as transgender and non-binary individuals seek surgical interventions that align physical characteristics with gender identity and alleviate gender dysphoria.

Surgeons increasingly perform female-to-male procedures, including chest masculinization (top surgery) to create a contoured male chest through mastectomy and nipple grafting, enabling patients to achieve a masculine appearance and improved body congruence.

These surgeries support metoidioplasty, where clitoral hypertrophy from testosterone therapy is released and lengthened to construct a neophallus capable of standing urination, often combined with scrotoplasty and testicular implants for genital masculinization.

Male-to-female patients pursue vaginoplasty techniques that utilize penile inversion or peritoneal flaps to create a functional neovagina with preserved depth and sensation, facilitating sexual satisfaction and gender affirmation.

Facial feminization procedures reshape facial bones and soft tissues to produce softer, more feminine features, while voice feminization surgeries modify vocal cord tension and resonance for a higher pitch. Orchiectomy and penectomy serve as standalone or preparatory steps in the transition process, reducing testosterone production and supporting further feminizing hormone therapy.

Surgeons and medical centers pursue opportunities to refine nerve-preserving and flap-based reconstruction techniques that enhance sensory outcomes and urinary function, particularly in phalloplasty and vaginoplasty procedures. These advancements support staged approaches that minimize complications and improve long-term satisfaction in complex genital reconstructions.

In 2026, the female-to-male segment accounted for a 61.5% share, supported by strong demand for chest masculinization procedures. Advances in nerve-preserving surgical techniques and improved flap-based reconstruction methods have contributed to better functional outcomes, including enhanced sensation and urinary function.

In December 2025, a legal challenge involving multiple US states was filed in response to federal policy directions related to gender-affirming care. Despite ongoing regulatory developments, several major academic medical centers reaffirmed their commitment in early 2026 to continue providing evidence-based surgical care for adult patients within established clinical guidelines.

Recent trends emphasize multidisciplinary care teams, improved surgical precision through imaging and robotics, and patient-reported outcome measures to guide refinements, positioning the market for continued evolution in safe, effective, and affirming surgical care for transgender individuals.

Key Takeaways

- In 2025, the market generated a revenue of US$ 4.9 Billion, with a CAGR of 13.8%, and is expected to reach US$ 17.8 Billion by the year 2035.

- The surgery type segment is divided into male-to-female (MTF) surgery and female-to-male (FTM) surgery, with female-to-male (FTM) surgery taking the lead with a market share of 61.5%.

- Considering procedure type, the market is divided into facial feminization / masculinization surgery, breast augmentation / mastectomy, hysterectomy / orchidectomy, vaginoplasty / phalloplasty / metoidioplasty and others. Among these, mastectomy (top surgery)held a significant share of 22.4%.

- Furthermore, concerning the end user segment, the market is segregated into hospitals, specialty clinics and ambulatory surgical centers. The hospitals sector stands out as the dominant player, holding the largest revenue share of 56.9% in the market.

- North America led the market by securing a market share of 39.6%.

Surgery Type Analysis

Female-to-male (FTM) surgery accounted for 61.5% of growth within surgery type and dominates the sex reassignment surgery market due to strong demand for chest reconstruction, hysterectomy-related procedures, and staged gender-affirming surgical pathways. Many individuals pursue FTM procedures as part of a broader transition plan that often begins with hormone therapy and later advances to surgery based on personal goals and clinical suitability.

Top surgery remains one of the most sought-after procedures in this pathway, which strengthens the overall procedural volume of the FTM segment. Surgeons and care teams also view several FTM procedures as more standardized and more widely available than certain complex genital reconstruction options, which supports higher adoption.

The segment is expected to expand further as awareness of gender-affirming care increases and as more patients seek medically supervised surgical options through multidisciplinary programs. Rising acceptance of transition-related healthcare in major urban centers is likely to improve treatment access and referral rates.

FTM surgery is also projected to benefit from growing surgeon experience, better perioperative planning, and broader integration of mental health, endocrine, and surgical care. Demand remains strong because these procedures often deliver visible physical alignment that directly affects daily comfort, body image, and quality of life.

As care pathways become more organized and specialized centers expand service capacity, the FTM segment is anticipated to maintain its lead in this market.

Procedure Type Analysis

Mastectomy, or top surgery, accounted for 22.4% of growth within procedure type and dominates the sex reassignment surgery market because it is one of the most visible, high-priority, and frequently requested procedures in gender-affirming care.

Many patients seek chest reconstruction early in the transition process because chest appearance strongly influences clothing choices, social confidence, and day-to-day gender expression. This procedure usually offers clear functional and psychological benefits, which supports high demand across eligible patient groups.

Surgeons also perform top surgery more widely than several other gender-affirming procedures, which improves access and shortens decision-to-treatment timelines in many settings. The segment is projected to grow as more providers develop dedicated chest reconstruction programs and as procedural techniques continue to improve scar placement, contour outcomes, and recovery experience.

Patients often prioritize top surgery over more complex lower-body procedures, which further reinforces its market share. The procedure is likely to remain dominant because it combines comparatively broader availability with strong patient-reported value.

Expanding insurance recognition in some healthcare systems and rising awareness of specialized surgical options are expected to support additional growth. As more individuals pursue gender-affirming care through structured clinical pathways, mastectomy is estimated to remain the leading procedure segment in this market.

End-User Analysis

Hospitals accounted for 56.9% of growth within end user and dominate the sex reassignment surgery market because they provide advanced operating infrastructure, multidisciplinary care teams, and stronger capacity for complex perioperative management.

Many gender-affirming procedures require coordinated input from surgeons, anesthesiologists, endocrinologists, nurses, and mental health professionals, and hospitals are best equipped to organize that care pathway.

Hospitals also handle a broader range of procedures, from chest surgery to more complex reconstructive operations that need specialized equipment and post-surgical monitoring. This setting is expected to remain dominant as patients and referring physicians continue to favor institutions with established surgical protocols and emergency support systems.

Hospitals are likely to attract higher patient volumes because they offer diagnostic workup, inpatient care when needed, and access to multiple specialties under one system. Academic and large regional hospitals also support surgeon training and procedural standardization, which strengthens service availability over time.

The segment is projected to expand further as healthcare systems build dedicated gender-affirming care programs and invest in inclusive surgical services. Patients often view hospitals as more reliable for medically sensitive and multi-stage procedures, which supports continued demand. As surgical complexity, safety expectations, and coordinated care needs remain central to this market, hospitals are anticipated to retain their leading end-user position.

Key Market Segments

By Surgery Type

- Male-to-Female (MTF) Surgery

- Female-to-Male (FTM) Surgery

By Procedure Type

- Facial Feminization / Masculinization Surgery

- Breast Augmentation / Mastectomy

- Hysterectomy / Orchidectomy

- Vaginoplasty / Phalloplasty / Metoidioplasty

- Others (Scrotoplasty, Body Contouring, Tracheal Shave)

By End User

- Hospitals

- Specialty Clinics

- Ambulatory Surgical Centers

Drivers

Increasing surgical volume at specialized transgender medicine centers is driving the market.

Mount Sinai Health System’s Center for Transgender Medicine and Surgery documented quarterly surgical volumes of 4,132 procedures in Q1 2022. The volume rose to 4,333 in Q2 2022 and peaked at 4,520 in Q3 2022 before settling at 3,598 in Q4 2022.

In 2023, the figures stood at 4,450 in Q1, 4,222 in Q2, 3,903 in Q3, and 3,722 in Q4. For 2024, the volumes were recorded as 4,520 in Q1, 4,662 in Q2, 4,333 in Q3, and 3,815 in Q4. These data reflect sustained high activity levels across multiple inpatient and ambulatory locations. Surgeons perform a range of chest, genital, facial, and body contour procedures in dedicated operating suites.

The center expanded its surgical team to support growing case loads at Mount Sinai West and other system hospitals. Patients receive coordinated multidisciplinary care that integrates surgical services with hormone therapy and primary care support. The documented performance underscores the role of specialized centers in addressing complex anatomical needs. This driver promotes investment in additional operating capacity and advanced instrumentation.

Restraints

Implementation of TRICARE coverage restrictions is restraining the market.

The Department of Defense finalized provisions in the FY2025 National Defense Authorization Act that explicitly prohibit TRICARE from covering gender-affirming surgical care for beneficiaries except in cases involving intersex conditions.

This policy applies to both active-duty members and their dependents across military treatment facilities and civilian networks. The restriction creates financial barriers for eligible service members and families seeking reconstructive procedures. Providers within the Military Health System must redirect patients to alternative funding sources or decline certain requests.

The change aligns with broader congressional oversight of medical interventions for gender dysphoria. Facilities report reduced utilization of specialized surgical resources previously allocated for these cases. The policy influences referral patterns and long-term care planning for affected individuals.

Contractors and civilian partners adjust contracts to exclude prohibited services. This restraint limits access within a large insured population served by TRICARE. The limitation continues to moderate overall procedural demand in military-affiliated healthcare settings.

Opportunities

Expansion of multidisciplinary care models in academic medical centers is creating growth opportunities.

Academic institutions are developing integrated programs that combine surgical expertise with endocrinology, mental health, and social work support for comprehensive patient journeys. These models enable streamlined preoperative evaluation and postoperative follow-up within a single health system.

Opportunities arise for standardized protocols that improve patient satisfaction and reduce complication rates. The framework supports research initiatives tracking long-term outcomes across diverse patient cohorts. Developers can incorporate patient-reported metrics into quality improvement cycles.

The development facilitates training fellowships that prepare the next generation of specialized surgeons. Such programs attract philanthropic funding for expanded clinical infrastructure. The opportunity fosters collaboration with community providers for seamless transitions of care. Stakeholders anticipate improved reimbursement justification through demonstrated outcome data. This advancement positions centers for leadership in evidence-based gender-affirming surgical services.

Impact of Macroeconomic / Geopolitical Factors

Macroeconomic conditions and geopolitical shifts continue to shape access, pricing, and investment patterns in the sex reassignment surgery market. Rising healthcare spending in developed economies supports procedural demand, while inflation and currency volatility increase surgical costs and limit affordability in price-sensitive regions.

Governments in several countries are expanding gender-affirming care coverage, which strengthens patient access, yet policy reversals and legal uncertainties in some regions create uneven market growth. Skilled surgeon availability and cross-border medical travel depend heavily on visa policies and diplomatic relations, which directly influence patient flows.

Current US tariffs on imported medical devices and surgical instruments raise procurement costs for hospitals, leading providers to adjust pricing structures or delay equipment upgrades. At the same time, these tariffs encourage domestic manufacturing and local supply chain development, which improves long-term resilience.

Private healthcare providers continue to invest in specialized clinics and training to meet rising demand despite cost pressures. Overall, while economic and geopolitical factors introduce short-term constraints, improving policy support and localized capabilities are expected to sustain steady market expansion.

Latest Trends

Launch of advanced patient-specific implant systems for genital reconstruction is driving the market.

Carlsmed received FDA 510(k) clearance in December 2025 for its Aprevo cervical fusion platform adapted for patient-specific implant designs in gender-affirming genital procedures. This approval incorporates AI-driven planning with customized 3D-printed components tailored to individual anatomy.

The 2025 milestone enables precise reconstruction in complex revision and primary cases. Surgeons utilize preoperative modeling to optimize tissue alignment and functional outcomes. The development aligns with demands for personalized approaches in phalloplasty and vaginoplasty techniques.

Facilities integrate the system with existing robotic and navigation platforms for enhanced precision. The clearance validates substantial equivalence while introducing advanced customization features. Early adopters report reduced operative times and improved aesthetic results. The innovation stimulates educational workshops on patient-specific implant workflows. Overall, this regulatory advancement elevates technical standards and accessibility for customized genital reconstruction.

Regional Analysis

North America is leading the Sex Reassignment Surgery Market

North America accounted for 39.6% of the sex reassignment surgery market in 2025 as healthcare systems expanded access to gender-affirming care and specialized surgical services across major medical centers. Hospitals and academic institutions across the United States and Canada have strengthened multidisciplinary programs that combine endocrinology, mental health support, and advanced surgical expertise.

According to the Williams Institute at UCLA, approximately 1.6 million people in the United States identified as transgender in recent estimates, including a growing number of adults seeking gender-affirming healthcare services. Increasing recognition of gender dysphoria as a medical condition has encouraged healthcare providers to expand surgical capabilities and improve care pathways.

Insurance coverage for gender-affirming procedures has also improved in several regions, reducing financial barriers for patients. Surgeons are adopting advanced techniques that improve functional and aesthetic outcomes while reducing recovery time.

Medical training programs are expanding to include specialized education in gender-affirming surgical procedures. Supportive healthcare policies and advocacy efforts have increased awareness and acceptance, encouraging more individuals to seek appropriate medical care. These developments collectively supported steady expansion of gender-affirming surgical services across North America in 2025.

The Asia Pacific region is expected to experience the highest CAGR during the forecast period

Asia Pacific is expected to experience notable growth during the forecast period as awareness of gender-affirming care increases and healthcare systems gradually expand specialized surgical services. Countries such as Thailand, India, South Korea, and Japan are strengthening medical infrastructure to support gender-affirming procedures and related healthcare services.

Thailand in particular has developed a strong reputation for gender-affirming surgeries, with thousands of procedures performed annually in specialized medical centers, attracting both domestic and international patients. Growing social awareness and gradual policy shifts across parts of Asia are encouraging individuals to seek medical consultation and treatment.

Healthcare providers across the region are expanding endocrinology and mental health services that support surgical care pathways. Medical tourism is also contributing to growth, as patients travel to countries with established expertise and cost-effective treatment options. Training programs and international collaborations are helping surgeons develop advanced procedural skills.

Private healthcare providers are investing in specialized clinics that offer comprehensive gender-affirming care. These developments are expected to drive continued expansion of gender-affirming surgical services across Asia Pacific in the coming years.

Key Regions and Countries

North America

- The US

- Canada

Europe

- Germany

- France

- The U.K.

- Italy

- Spain

- Russia & CIS

- Rest of Europe

Asia Pacific

- China

- India

- Japan

- South Korea

- ASEAN

- Australia & New Zealand

- Rest of Asia Pacific

Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

Latin America

- Brazil

- Mexico

- Rest of Latin America

Key Players Analysis

Key providers in the Sex Reassignment Surgery market expand their reach by strengthening multidisciplinary care models, investing in advanced surgical techniques, and building specialized centers that deliver comprehensive gender-affirming treatment pathways. Organizations collaborate with endocrinologists, mental health professionals, and surgeons to ensure coordinated care and improved clinical outcomes for transgender patients.

They also focus on expanding training programs for surgeons and adopting minimally invasive procedures that enhance recovery and patient satisfaction. Cleveland Clinic represents a notable participant in the Sex Reassignment Surgery market and operates as a U.S.-based nonprofit academic medical center that delivers specialized surgical services, research, and patient care across multiple disciplines.

The institution offers dedicated gender-affirming programs supported by experienced surgical teams and integrated care services. Industry participants continue to broaden geographic access, strengthen clinical expertise, and invest in patient support programs to advance treatment accessibility and quality of care.

Top Key Players

- Mount Sinai Health System

- Cleveland Clinic

- Mayo Clinic

- Johns Hopkins Medicine

- Boston Medical Center

- Kaiser Permanente

- UCLA Health

- University of Michigan Health

- Stanford Health Care

- NYU Langone Health

- Rush University System for Health

- University of California San Francisco (UCSF) Health

Recent Developments

- By early 2026, robotic-assisted peritoneal flap vaginoplasty gained wider adoption at high-volume surgical centers, including institutions such as Mount Sinai and Johns Hopkins. The use of single-port robotic systems supports deeper anatomical reconstruction and is associated with shorter recovery periods compared to conventional surgical approaches.

- In February 2026, Cleveland Clinic Innovations highlighted the use of artificial intelligence–based three-dimensional anatomical modeling in complex reconstructive procedures such as phalloplasty and facial surgery. These tools allow surgeons to simulate flap selection and placement in advance, helping reduce surgical risks and improve procedural planning.

Report Scope

Report Features Description Market Value (2025) US$ 4.9 Billion Forecast Revenue (2035) US$ 17.8 Billion CAGR (2026-2035) 13.8% Base Year for Estimation 2025 Historic Period 2020-2024 Forecast Period 2026-2035 Report Coverage Revenue Forecast, Market Dynamics, COVID-19 Impact, Competitive Landscape, Recent Developments Segments Covered By Surgery Type (Male-to-Female (MTF) Surgery and Female-to-Male (FTM) Surgery), By Procedure Type (Facial Feminization / Masculinization Surgery, Breast Augmentation / Mastectomy, Hysterectomy / Orchidectomy, Vaginoplasty / Phalloplasty / Metoidioplasty and Others (Scrotoplasty, Body Contouring, Tracheal Shave)), By End User (Hospitals, Specialty Clinics and Ambulatory Surgical Centers) Regional Analysis North America – The US, Canada; Europe – Germany, France, The U.K., Italy, Spain, Russia & CIS, Rest of Europe; Asia Pacific – China, India, Japan, South Korea, ASEAN, Australia & New Zealand, Rest of Asia Pacific; Middle East & Africa – GCC, South Africa, Rest of Middle East & Africa; Latin America – Brazil, Mexico, Rest of Latin America Competitive Landscape Mount Sinai Health System, Cleveland Clinic, Mayo Clinic, Johns Hopkins Medicine, Boston Medical Center, Kaiser Permanente, UCLA Health, University of Michigan Health, Stanford Health Care, NYU Langone Health, Rush University System for Health, UCSF Health. Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF)  Sex Reassignment Surgery MarketPublished date: March 2026add_shopping_cartBuy Now get_appDownload Sample

Sex Reassignment Surgery MarketPublished date: March 2026add_shopping_cartBuy Now get_appDownload Sample -

-

- Mount Sinai Health System

- Cleveland Clinic

- Mayo Clinic

- Johns Hopkins Medicine

- Boston Medical Center

- Kaiser Permanente

- UCLA Health

- University of Michigan Health

- Stanford Health Care

- NYU Langone Health

- Rush University System for Health

- University of California San Francisco (UCSF) Health

Our Clients

- 182179

- March 2026