Quick Navigation

Report Overview

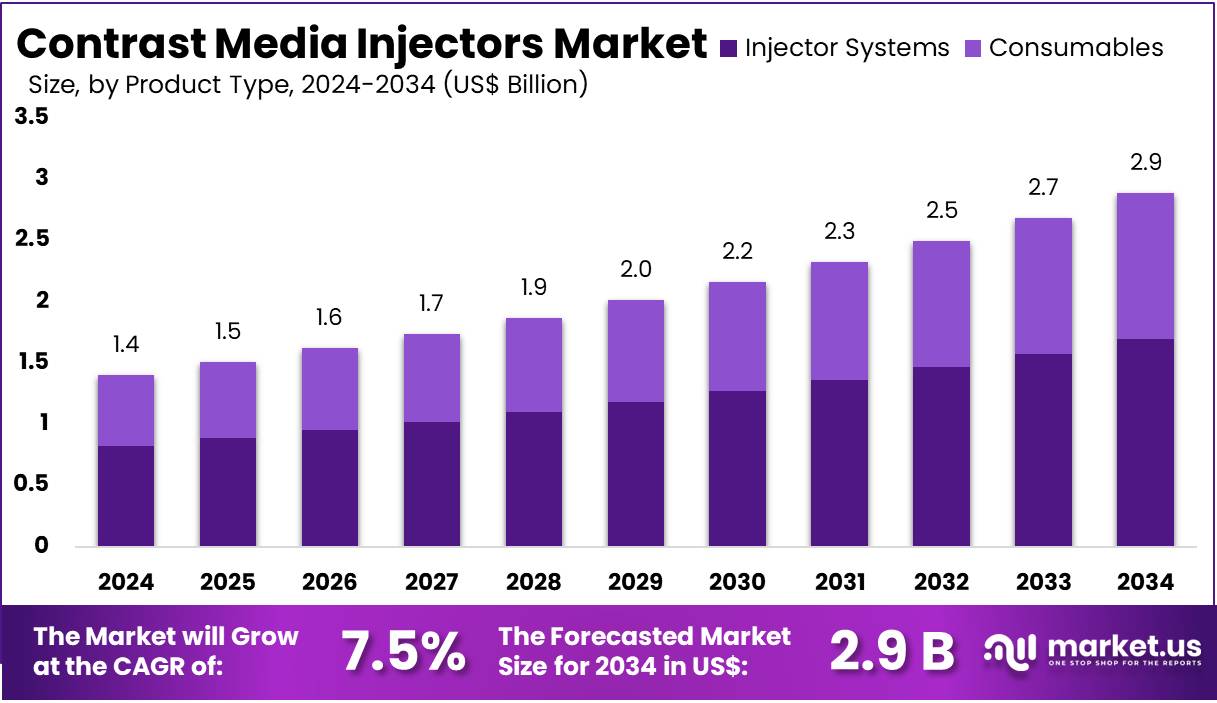

The Global Contrast Media Injectors Market size is expected to be worth around US$ 2.9 Billion by 2034, from US$ 1.4 Billion in 2024, growing at a CAGR of 7.5% during the forecast period from 2025 to 2034.

Rising demand for advanced diagnostic imaging procedures has spurred growth in the contrast media injectors market. As healthcare providers increasingly rely on imaging technologies like CT scans, MRIs, and angiography for diagnosing and monitoring medical conditions, the need for efficient and accurate contrast media delivery has intensified. These injectors play a crucial role in administering contrast agents that enhance the quality of images, leading to more accurate diagnoses and treatment plans.

Technological advancements in injector systems, such as automation, real-time monitoring, and enhanced safety features, are expected to drive further market growth. Additionally, the increasing prevalence of chronic diseases like cardiovascular conditions, cancer, and neurological disorders, which require frequent imaging tests, is creating new opportunities for the market.

Moreover, the growing demand for minimally invasive procedures and rising healthcare expenditure contribute to the adoption of advanced contrast media injectors. According to the National Institutes of Health (NIH), the global medical imaging market, which includes contrast media injectors, is projected to reach approximately US$45 billion by 2025, reflecting an increasing reliance on advanced imaging technologies for clinical diagnostics and treatment.

Key Takeaways

- In 2024, the market for contrast media injectors generated a revenue of US$ 1.4 billion, with a CAGR of 7.5%, and is expected to reach US$ 2.9 billion by the year 2034.

- The product type segment is divided into injector systems and consumables, with injector systems taking the lead in 2024 with a market share of 58.7%.

- Considering technology, the market is divided into single-head injectors, dual-head injectors, and syringeless injectors. Among these, single-head injectors held a significant share of 56.9%.

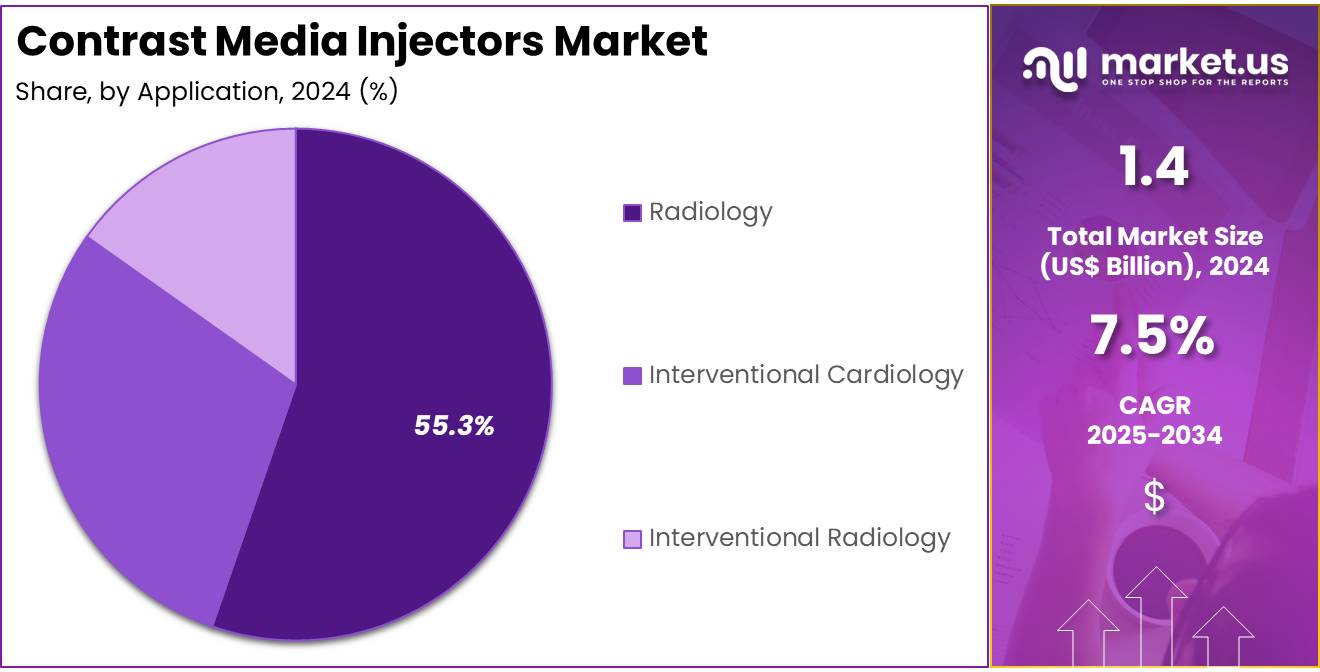

- Furthermore, concerning the application segment, the market is segregated into radiology, interventional cardiology, and interventional radiology. The radiology sector stands out as the dominant player, holding the largest revenue share of 55.3% in the contrast media injectors market.

- The end-user segment is segregated into hospitals, diagnostic centers, and ambulatory surgery centers, with the hospitals segment leading the market, holding a revenue share of 52.4%.

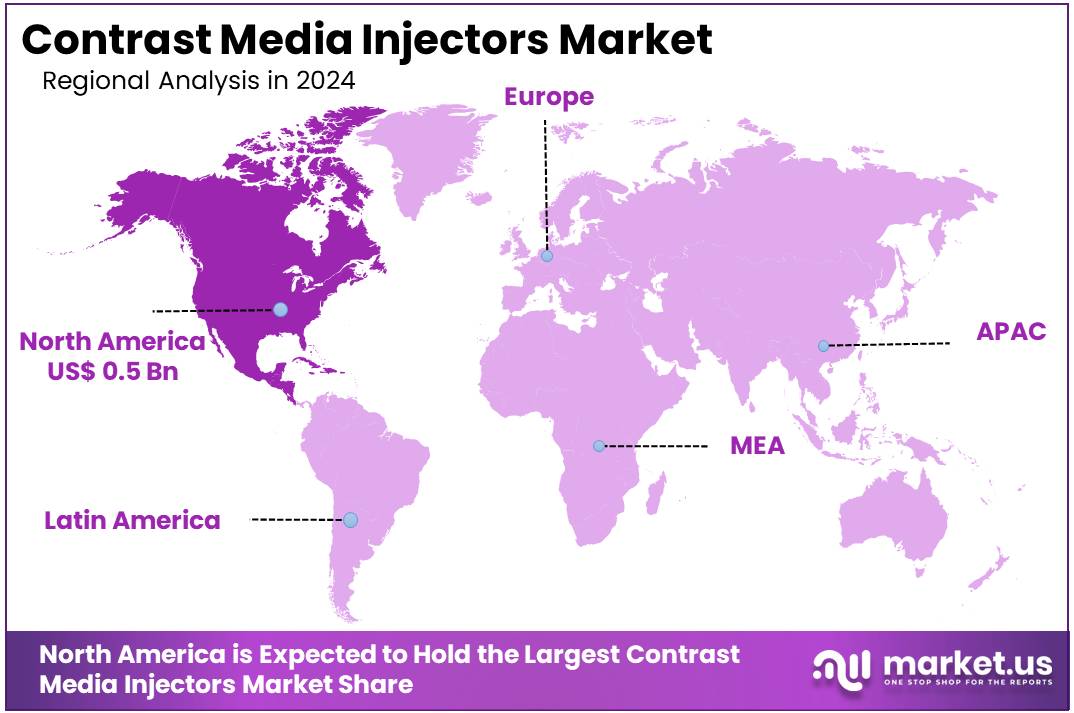

- North America led the market by securing a market share of 38.7% in 2024.

Product Type Analysis

The injector systems segment led in 2024, claiming a market share of 58.7% owing to the increasing demand for accurate and efficient contrast media delivery during imaging procedures. Injector systems are anticipated to become more popular as healthcare providers seek advanced technology to enhance diagnostic accuracy and improve patient outcomes.

The growing adoption of CT, MRI, and angiography procedures, which rely heavily on contrast media for enhanced imaging, is likely to drive the demand for injector systems. Additionally, innovations in injector system designs, such as automated and precise control mechanisms, are expected to improve operational efficiency and reduce complications, thereby contributing to the segment’s growth. As the need for reliable and safe contrast injection systems increases, this segment is projected to see continued expansion.

Technology Analysis

The single-head injectors held a significant share of 56.9% due to their widespread use in various imaging procedures. Single-head injectors are expected to remain in high demand as they offer cost-effective, compact, and user-friendly solutions for contrast media delivery. Their ability to inject contrast media at a consistent rate and pressure is likely to make them a preferred choice in routine diagnostic imaging settings.

Furthermore, the growing trend toward simpler, more efficient equipment for healthcare facilities with limited space or budget is anticipated to drive the adoption of single-head injectors. As healthcare providers focus on improving patient care and operational efficiency, the single-head injectors segment is expected to see continued growth, particularly in diagnostic imaging centers and hospitals.

Application Analysis

The radiology segment had a tremendous growth rate, with a revenue share of 55.3% owing to the increasing demand for advanced imaging techniques that require high-quality contrast media. As radiology plays a critical role in diagnosing a wide range of medical conditions, including cancer, cardiovascular diseases, and neurological disorders, the need for effective and efficient contrast media delivery systems is likely to grow.

The rise in imaging procedures, such as CT scans and MRIs, coupled with the growing focus on early diagnosis, is anticipated to drive demand for contrast media injectors in radiology. Moreover, the continuous advancements in imaging technologies, which require precise contrast media injection for optimal results, are expected to further fuel growth in this segment.

End-user Analysis

The hospitals segment grew at a substantial rate, generating a revenue portion of 52.4% as hospitals remain the primary locations for advanced diagnostic imaging procedures. Hospitals are projected to continue adopting state-of-the-art contrast media injectors to support their imaging departments, driven by the rising volume of diagnostic procedures like CT scans, MRIs, and angiograms.

The growing prevalence of chronic diseases that require frequent imaging for monitoring and diagnosis is likely to increase the demand for reliable and efficient contrast media injectors in hospitals. Additionally, hospitals’ need for high-throughput imaging equipment and improved patient care is expected to drive investments in advanced contrast injection technologies. As hospitals increasingly focus on enhancing operational efficiency and diagnostic precision, this segment is anticipated to expand.

Key Market Segments

By product Type

- Injector Systems

- CT injector systems

- MRI injector systems

- Cardiovascular/angiography injector systems

- Consumables

- Tubing

- Syringe

- Interventional Radiology

By Technology

- Single-head Injectors

- Dual-head Injectors

- Syringeless Injectors

By Application

- Radiology

- Interventional Cardiology

- Interventional Radiology

By End-user

- Hospitals

- Diagnostic Centers

- Ambulatory Surgery Centers

Drivers

Increasing Prevalence of Chronic Diseases is Driving the Market

The rising incidence of chronic diseases, particularly cancer and cardiovascular disorders, has significantly propelled the demand for advanced diagnostic imaging procedures, thereby driving the contrast media injectors market. According to the American Cancer Society, the number of cancer cases in the United States increased from 1,898,160 in 2021 to 1,958,310 in 2023, reflecting a growth of 3.16%.

Similarly, the World Heart Federation reported that over 500 million individuals globally were affected by cardiovascular diseases as of April 2023, leading to 20.5 million fatalities in 2021, constituting nearly one-third of total global mortality. These alarming statistics underscore the necessity for precise and efficient diagnostic tools, such as contrast media injectors, to enhance imaging quality and facilitate early disease detection.

The increasing burden of these diseases has led healthcare providers to adopt advanced imaging technologies, thereby boosting the market for contrast media injectors. This trend is expected to continue as the global population ages and the prevalence of chronic diseases rises, further driving market growth.

Restraints

High Costs of Contrast Media Injectors are Restraining the Market

Despite the growing demand, the high costs associated with contrast media injectors pose a significant restraint on market expansion. The initial investment required for procuring these advanced devices, coupled with the expenses for consumables and maintenance, can be substantial. This financial burden is particularly challenging for small and medium-sized healthcare facilities, especially in developing regions with limited budgets.

The high cost can deter these institutions from adopting the latest imaging technologies, thereby limiting the market’s growth potential. Additionally, the need for specialized training to operate these sophisticated injectors adds to the overall expenditure, further hindering widespread adoption. To mitigate this restraint, manufacturers and healthcare providers are exploring cost-effective solutions and financing options to make these essential diagnostic tools more accessible.

Opportunities

Technological Advancements are Creating Growth Opportunities

Technological innovations in contrast media injectors are opening new avenues for market growth. The development of automated and syringeless injectors has enhanced the efficiency and safety of contrast media administration. For instance, in November 2022, GE Healthcare partnered with ulrich medical to introduce multi-dose contrast media injectors in the US, aiming to reduce procedure setup time and increase patient throughput.

These advancements not only improve workflow efficiency but also minimize the risk of contamination and contrast media wastage. Moreover, the integration of artificial intelligence and IoT technologies allows for personalized contrast dosing and real-time monitoring, further enhancing diagnostic accuracy. As healthcare facilities increasingly adopt these cutting-edge solutions, the market for contrast media injectors is poised for significant expansion.

Impact of Macroeconomic / Geopolitical Factors

Macroeconomic and geopolitical factors play a crucial role in shaping the contrast media injectors market. Economic downturns often lead to budget cuts in healthcare, reducing investments in advanced medical equipment. This affects the demand for contrast media injectors, limiting market expansion. Geopolitical tensions disrupt global supply chains, delaying production and distribution. Trade restrictions and tariffs further increase manufacturing costs, leading to higher prices for end-users. These challenges make it difficult for healthcare facilities to adopt new imaging technologies, impacting overall market growth.

Despite these challenges, several opportunities exist in the market. Increased government spending on healthcare during public health crises can drive demand for diagnostic imaging equipment. International collaborations and trade agreements help companies expand distribution networks and foster innovation. Emerging economies are investing in healthcare infrastructure, boosting the demand for advanced diagnostic tools. This trend presents growth opportunities for market players, as healthcare providers seek more efficient imaging solutions to improve patient care and diagnostics.

Latest Trends

Strategic Collaborations are a Recent Trend in the Market

The contrast media injectors market is experiencing a rise in strategic collaborations among key players. These partnerships aim to improve product offerings and expand market reach. In November 2023, Bracco Imaging teamed up with ulrich medical to introduce syringeless magnetic resonance injectors in the U.S. This collaboration enhances accessibility to innovative imaging solutions. Additionally, in October 2022, GE Healthcare’s Pharmaceutical Diagnostics division secured a long-term agreement with SQM (Sociedad Química y Minera de Chile S.A.). This deal ensures a stable supply of iodine, a crucial ingredient in contrast media for X-ray and CT procedures.

These collaborations allow companies to leverage each other’s expertise and expand their market presence. They promote innovation and accelerate the launch of advanced products. Such alliances help firms meet the evolving needs of healthcare providers and patients more effectively. By pooling resources, companies develop safer, more efficient, and user-friendly injectors. This trend supports market growth by enhancing product reliability and improving imaging outcomes in medical diagnostics.

Regional Analysis

North America is leading the Contrast Media Injectors Market

North America dominated the market with the highest revenue share of 38.7% owing to technological innovations and the rising incidence of chronic illnesses. The market generated approximately USD 482.4 million in revenue in 2023 and is estimated to grow at a compound annual growth rate (CAGR) of 6.6% through 2030. The United States accounted for a significant portion, with revenues of about USD 401.8 million in 2023 and projections indicating an increase to USD 622.5 million by 2030.

This growth is primarily driven by the growing demand for advanced imaging procedures, fueled by the increasing prevalence of cancer and cardiovascular diseases. Furthermore, the integration of cutting-edge injector systems has enhanced diagnostic precision, further accelerating market expansion. Canada is anticipated to record the highest growth rate in the region, supported by its strong healthcare infrastructure and increased investments in medical technology.

The Asia Pacific region is expected to experience the highest CAGR during the forecast period

Asia Pacific is expected to grow with the fastest CAGR owing to the increasing burden of chronic diseases and improvements in healthcare systems. The market was valued at approximately USD 316.1 million in 2023 and is expected to reach USD 559.7 million by 2030, expanding at a CAGR of 8.5% from 2024 to 2030. China is likely to register the highest growth rate in the region due to substantial investments in healthcare and the adoption of advanced imaging technologies.

Additionally, the rising elderly population and greater awareness of early disease detection are fueling demand for diagnostic imaging. The expansion of medical tourism in countries such as India and Thailand is expected to contribute to market growth, as these nations provide cost-effective diagnostic services. The consumables segment is projected to witness the fastest growth, driven by the recurring need for syringes and tubing in medical imaging procedures.

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia

- Netherland

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- New Zealand

- Singapore

- Thailand

- Vietnam

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Key Players Analysis

Key players in the contrast media injectors market focus on strategic collaborations, technological advancements, and product innovations to drive growth. They invest in research and development to enhance injector efficiency, improve patient safety, and expand their product portfolios. Companies also engage in mergers and acquisitions to strengthen their market position and increase geographic reach. Regulatory compliance and strategic partnerships with healthcare providers help them gain a competitive edge. Expanding into emerging markets further supports revenue growth and enhances their global footprint.

Bayer AG is a global pharmaceutical and life sciences company headquartered in Leverkusen, Germany. The company operates through three main divisions: Pharmaceuticals, Consumer Health, and Crop Science. Its radiology division offers advanced medical imaging solutions, including injection systems for contrast agents. Bayer continuously invests in innovation to improve diagnostic imaging technologies and enhance patient care. With a strong global presence, the company focuses on sustainability and cutting-edge healthcare solutions to maintain industry leadership.

Top Key Players in the Contrast Media Injectors Market

- Ulrich Medical

- Medtron AG

- Hong Kong Medi Co Limited

- Guerbet Group

- GE Healthcare

- Bracco Group

- Bayer HealthCare LLC

Recent Developments

- In November 2023, Bracco formed a strategic alliance with Ulrich Medical to introduce a next-generation syringeless MRI injector system. This collaboration facilitated Bracco’s expansion into the US market, offering an innovative solution aimed at optimizing imaging workflows.

- In November 2022, GE Healthcare joined forces with Ulrich Medical to launch a multi-dose contrast injector for CT imaging applications in the US The advanced injector system enhances efficiency by streamlining contrast administration, minimizing preparation time, and improving overall patient throughput.

Report Scope

| Report Features | Description |

| Market Value (2024) | US$ 1.4 billion |

| Forecast Revenue (2034) | UL$ 2.9 billion |

| CAGR (2025-2034) | 7.5% |

| Base Year for Estimation | 2024 |

| Historic Period | 2020-2023 |

| Forecast Period | 2025-2034 |

| Report Coverage | Revenue Forecast, Market Dynamics, COVID-19 Impact, Competitive Landscape, Recent Developments |

| Segments Covered | By Product Type (Injector Systems (CT Injector Systems, MRI Injector Systems, and Cardiovascular/Angiography Injector Systems), Consumables (Tubing, Syringe, and Interventional Radiology)), By Technology (Single-head Injectors, Dual-head Injectors, and Syringeless Injectors), By Application (Radiology, Interventional Cardiology, and Interventional Radiology), By End-user (Hospitals, Diagnostic Centers, and Ambulatory Surgery Centers) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, New Zealand, Singapore, Thailand, Vietnam, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA |

| Competitive Landscape | Ulrich Medical, Medtron AG, Hong Kong Medi Co Limited, Guerbet Group, GE Healthcare, Bracco Group, and Bayer HealthCare LLC. |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |