Global Sapphire Market Size, Share, And Industry Analysis Report By Form (Wafers, Sapphire Boules, Sheets), By Type (Synthetic, Natural), By End-Use (Electronics and Energy, Aerospace and Defense, Medical, Semiconductor Equipment, Others), By Region and Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Statistics, Trends and Forecast 2026-2035

- Published date: April 2026

- Report ID: 184127

- Number of Pages: 198

- Format:

-

keyboard_arrow_up

Quick Navigation

Report Overview

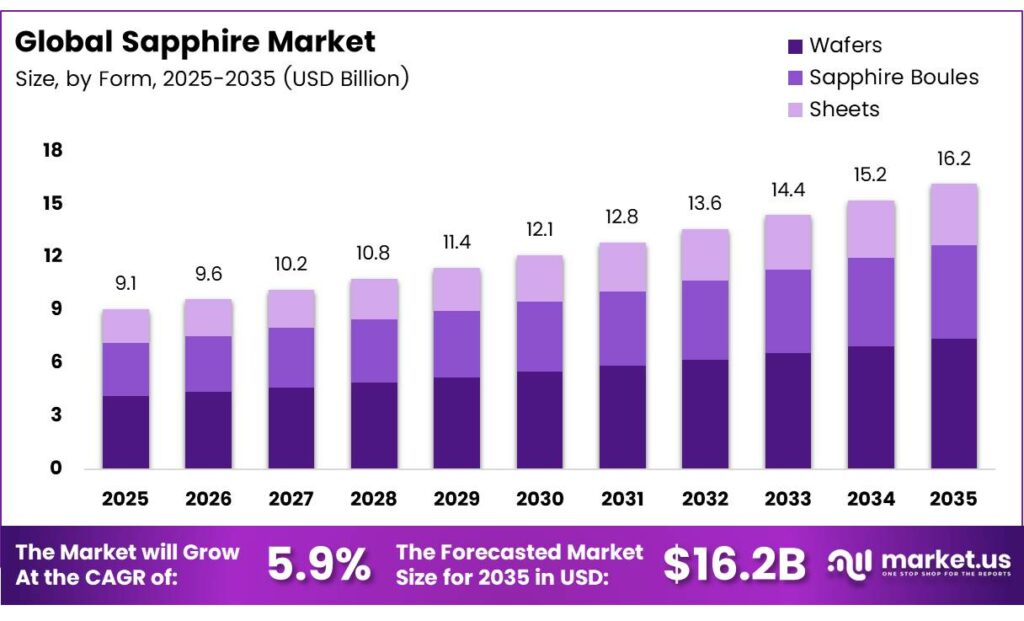

The Global Sapphire Market size is expected to be worth around USD 16.2 billion by 2035 from USD 9.1 billion in 2025, growing at a CAGR of 5.9% during the forecast period 2026 to 2035.

Sapphire refers to a high-durability crystalline form of aluminum oxide. Manufacturers use it for demanding industrial and electronic applications due to its exceptional hardness and thermal stability. Market growth directly links to the rising demand for energy-efficient lighting solutions. Specifically, high-brightness LED fabrication requires sapphire substrates, which dominate current production needs.

The sapphire market is expanding steadily as manufacturers scale crystal growth capacity to meet rising demand from LEDs, semiconductor equipment, optics, and industrial applications. A major 2025 milestone was the launch of a KY (Kyropoulos) sapphire growth furnace capable of producing 800–1000 kg per cycle, enabling stable large-boule output for high-volume LED and optical uses.

Production remains highly energy-intensive, especially for monocrystalline sapphire fabricated from large KY boules of up to 350 kg. The prolonged high-temperature growth cycles require significant electricity and thermal energy, increasing the carbon footprint of facilities powered by non-renewable sources. Sapphire’s exceptional hardness, thermal stability, and optical clarity continue to make it a critical material for advanced electronics and precision technology components.

Asia Pacific remains the leading region for sapphire production and consumption, supported by strong electronics supply chains, semiconductor infrastructure investments, and government backing for energy-efficient technologies. Growth opportunities are accelerating through emerging applications such as microLED displays, EV lighting systems, RF devices, wafers, and medical implants, where sapphire’s durability and performance advantages are essential.

Key Takeaways

- The Global Sapphire Market grows from USD 9.1 billion in 2025 to USD 16.2 billion by 2035 at a 5.9% CAGR.

- Wafers form the leading product segment with a 49.6% market share.

- Synthetic sapphire captures the majority by type, holding 93.5% of the market.

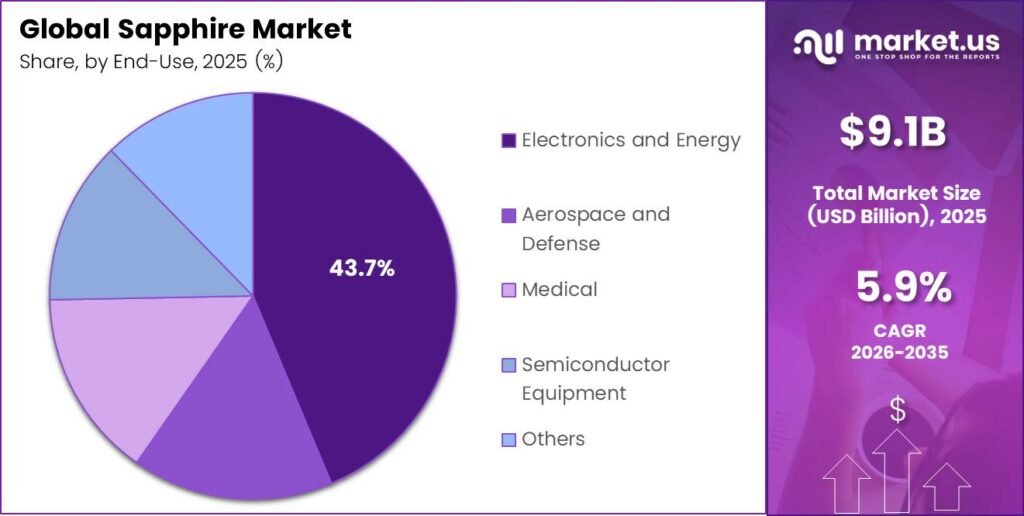

- Electronics and Energy leads end-use applications with a 43.7% share.

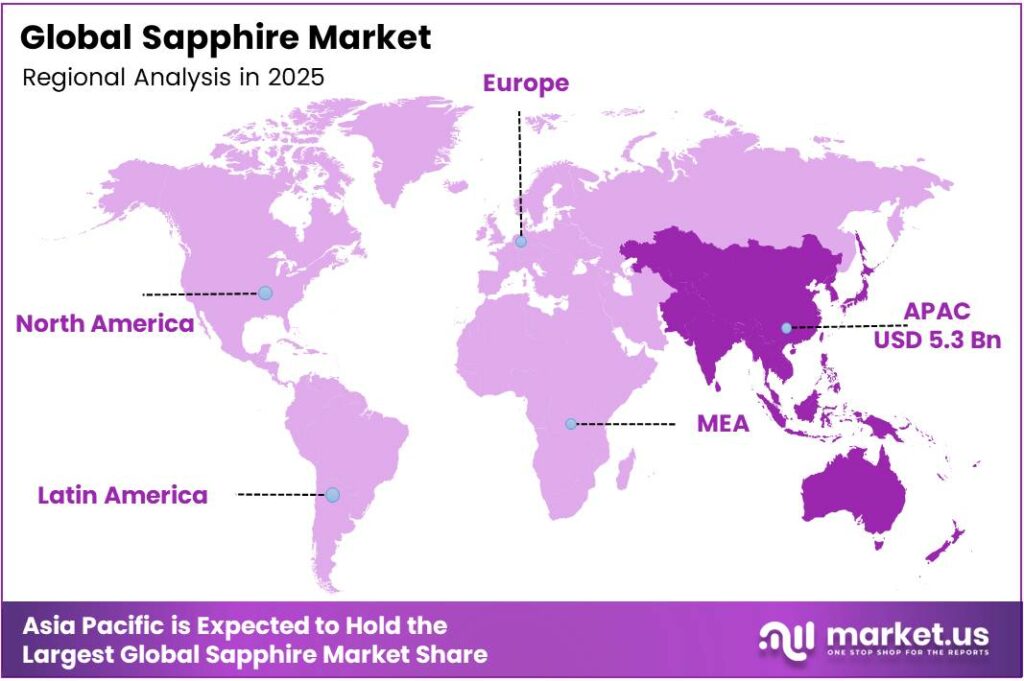

- Asia Pacific dominates with a 57.9% share, valued at USD 5.3 billion.

Form Analysis

Wafers dominate with 49.6% due to high demand for LED and semiconductor substrates.

In 2025, Wafers held a dominant market position in the By Form segment of the Sapphire Market, with a 49.6% share. Their thin, circular shape makes them ideal for high-brightness LED production. Producers prefer wafers for LED substrates and semiconductor applications. They deliver precise lattice matching and high yield rates. Moreover, semiconductor manufacturers rely on wafers for power device applications.

The Sapphire Boules segment serves as the primary raw material form. Producers grow these large cylindrical crystals using the Kyropoulos or Czochralski methods. Consequently, boules get sliced into wafers or other shapes for further processing. Sheets represent a growing form for specialized optical and cover applications. Manufacturers prefer sheets for smartphone screens and watch crystals.

Type Analysis

Synthetic dominates with 93.5% due to consistent quality and cost-effective production.

In 2025, Synthetic sapphire held a dominant market position in the By Type segment of the Sapphire Market, with a 93.5% share. This man-made material offers superior uniformity and fewer defects. Therefore, industries choose synthetic materials for high-precision electronic and optical components.

Natural sapphire occupies a niche segment for luxury and decorative uses. Its limited availability and higher cost restrict widespread industrial adoption. However, some premium jewelry and collector markets still demand natural stones for their unique characteristics.

End-Use Analysis

Electronics and Energy dominate with 43.7% due to LED and semiconductor demand.

In 2025, Electronics and Energy held a dominant market position in the By End-Use segment of the Sapphire Market, with a 43.7% share. This sector uses sapphire wafers extensively for LED lighting and power electronics. Additionally, energy applications include high-voltage insulating components.

The Aerospace and Defense segment values sapphire for its thermal stability and RF transparency. Manufacturers produce durable sensor windows and radomes using this material. Consequently, military systems require sapphire for reliable performance in extreme conditions. Medical applications leverage sapphire’s biocompatibility and optical clarity. Surgical tools and biomedical implants benefit from its non-reactive surface.

Semiconductor Equipment relies on sapphire for wafer handling and processing components. Its hardness and chemical resistance protect sensitive manufacturing environments. Therefore, equipment makers specify sapphire for critical wear parts. Others include luxury watches, smartphones, and industrial sensors. These applications demand scratch-resistant and transparent cover solutions.

Key Market Segments

By Form

- Wafers

- Sapphire Boules

- Sheets

By Type

- Synthetic

- Natural

By End-Use

- Electronics and Energy

- Aerospace and Defense

- Medical

- Semiconductor Equipment

- Others

Emerging Trends

Shift to Larger-Diameter Wafers and Advanced Processes

Manufacturers rapidly shift toward larger-diameter sapphire wafers for improved yield. This trend reduces per-unit costs for LED and microLED production. The fabricated sapphire structures maintained a 98.7% dust-free surface area solely using gravity. Consequently, advanced yield-optimization processes become standard across new manufacturing lines.

Adoption of Patterned Substrates and 5G Integration

Patterned sapphire substrates gain widespread adoption to enhance light extraction efficiency in LEDs. This technology boosts brightness without increasing power consumption. Additionally, sapphire finds growing use in 5G and 6G RF power devices for superior signal performance.

Drivers

LED Demand from Energy-Efficiency Mandates Drives Substrate Sales

Escalating global demand for sapphire substrates in high-brightness LED fabrication fuels market growth. Government energy-efficiency mandates directly push lighting manufacturers toward LED solutions. The nanostructured sapphire sample exhibited enhanced transmission of up to 95.8% at a wavelength of 1360 nm.

Consumer Electronics and Aerospace Applications Expand

Proliferating integration of sapphire in consumer electronics for scratch-resistant camera lenses drives adoption. Moreover, expanding use across aerospace, defense, and power electronics requires superior thermal stability. These performance benefits make sapphire essential for 5G infrastructure rollout and semiconductor miniaturization. Consequently, sapphire substrate orders increase substantially for residential and commercial lighting.

Restraints

High Production Costs Limit Market Accessibility

Persistently high production costs, coupled with energy-intensive Kyropoulos and EFG crystal growth methods, restrain market expansion. Process optimization of temperature gradients and furnace thermal fields is documented to directly control sapphire crystal growth rate and quality; furnace design notes from 2024–2025 emphasize that precise thermal‑field configuration and atmosphere control (argon/vacuum) are now standard to reduce defects and improve yield in crystal growth applications, including sapphire.

Alternative Substrates Challenge Sapphire Adoption

Rising market penetration of cost-effective alternative substrates such as silicon carbide and GaN-on-silicon creates strong competition. These materials offer similar performance at lower production costs. Therefore, price-sensitive buyers may switch away from sapphire for certain applications. These methods require prolonged high-temperature cycles and specialized equipment. Consequently, new entrants face significant capital barriers to compete effectively.

Growth Factors

MicroLED and Medical Breakthroughs Create New Demand

Breakthrough applications in microLED displays drive precision sapphire wafer demand for next-generation visual technologies. Additionally, accelerating use in medical devices and biomedical implants leverages exceptional biocompatibility. The fabricated sapphire nanostructures demonstrated a period of 330 nm and an aspect ratio of 2.1, the highest reported for sapphire thus far.

Automotive and Wearable Sectors Accelerate Adoption

Expanding role in automotive LED lighting and sensor systems amid electric vehicle proliferation boosts market prospects. Furthermore, emerging potential in high-end wearables requires premium scratch-resistant sapphire components. These consumer-driven segments grow faster than traditional industrial applications. These emerging sectors provide high-margin growth opportunities for specialized sapphire products.

Regional Analysis

Asia Pacific Dominates the Sapphire Market with a Market Share of 57.9%, Valued at USD 5.3 Billion

Asia Pacific leads the sapphire market with a 57.9% share valued at USD 5.3 billion. Strong electronics manufacturing and semiconductor investments drive this position. China and other nations expand production capacity rapidly. Moreover, government policies support technology self-reliance. Consequently, the region maintains clear leadership. The region benefits from lower production costs and proximity to major LED and consumer electronics brands.

North America focuses on high-value sapphire applications for defense, aerospace, and medical devices. Manufacturers here prioritize quality and performance over volume production. Additionally, research institutions drive innovation in large-diameter crystal growth methods. Additionally, innovation in medical devices boosts regional consumption. Producers invest in quality improvements.

Europe shows steady demand for sapphire in automotive lighting, industrial sensors, and luxury optics. German and French manufacturers lead in precision engineering applications. Europe prioritizes energy-efficient technologies and industrial uses. Automotive and medical sectors adopt sapphire components steadily.

The Middle East and Africa represent a smaller but growing market for sapphire. Regional demand focuses on LED lighting for infrastructure projects and telecommunications equipment. However, limited local manufacturing means most products are imported. The Middle East and Africa explore energy and industrial applications. Defense needs support to meet the demand.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

Rubicon Technology, LLC, focuses on producing large-diameter sapphire substrates for LED and optical applications. The company emphasizes advanced crystal growth techniques to improve yield and reduce costs. Consequently, Rubicon maintains a strong position in the high-end wafer market segment.

Monocrystal specializes in synthetic sapphire for electronics and LED lighting solutions. The company operates large-scale production facilities with optimized Kyropoulos furnaces. Moreover, Monocrystal invests heavily in R&D for patterned sapphire substrate technologies.

Kyocera Corporation leverages its broader ceramics expertise to deliver sapphire components for industrial and consumer markets. The company integrates sapphire into smartphone covers, semiconductor equipment, and precision optics. Therefore, Kyocera benefits from diversified application exposure across multiple sectors.

Orbray Co. Ltd focuses on high-precision sapphire components for medical devices and aerospace systems. The company excels in machining complex shapes with tight tolerances. Additionally, Orbray serves the luxury watch market with premium sapphire crystals.

Top Key Players in the Market

- Rubicon Technology, LLC

- Monocrystal

- Kyocera Corporation

- Orbray Co. Ltd

- Chatham Created Gems and Diamonds

- Swiss Jewel Company

- Crystalwise Technology

- SCHOTT AG

- Topco Scientific

Recent Developments

- In 2025, Kyocera announced it would showcase its single-crystal sapphire engineering solutions at Pittcon 2025 (March 3–5, Boston). Highlights included laser-processed sapphire apertures for blood-analysis devices (using sheath-flow DC detection for precise cell sizing), sapphire wafers with fine-hole processing for hermetic sealing/electrical insulation, and other laser-processed sapphire components.

- In 2025, the successful development of the world’s largest self-standing single-crystal diamond substrates (20 mm × 20 mm, twin-free). Uses Orbray’s proprietary Step-Flow Growth Method on specially designed misoriented sapphire substrates. This reduces heteroepitaxial stress and enables larger, defect-free crystals.

Report Scope

Report Features Description Market Value (2025) USD 9.1 billion Forecast Revenue (2035) USD 16.2 billion CAGR (2026-2035) 5.9% Base Year for Estimation 2025 Historic Period 2020-2024 Forecast Period 2026-2035 Report Coverage Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments Segments Covered By Form (Wafers, Sapphire Boules, Sheets), By Type (Synthetic, Natural), By End-Use (Electronics and Energy, Aerospace and Defense, Medical, Semiconductor Equipment, Others) Regional Analysis North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East & Africa (GCC, South Africa, and Rest of MEA) Competitive Landscape Rubicon Technology, LLC, Monocrystal, Kyocera Corporation, Orbray Co., Ltd., Chatham Created Gems and Diamonds, Swiss Jewel Company, Crystalwise Technology, SCHOTT AG, Topco Scientific Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited Users and Printable PDF)

-

-

- Rubicon Technology, LLC

- Monocrystal

- Kyocera Corporation

- Orbray Co. Ltd

- Chatham Created Gems and Diamonds

- Swiss Jewel Company

- Crystalwise Technology

- SCHOTT AG

- Topco Scientific

Our Clients

- 184127

- April 2026