Quick Navigation

Report Overview

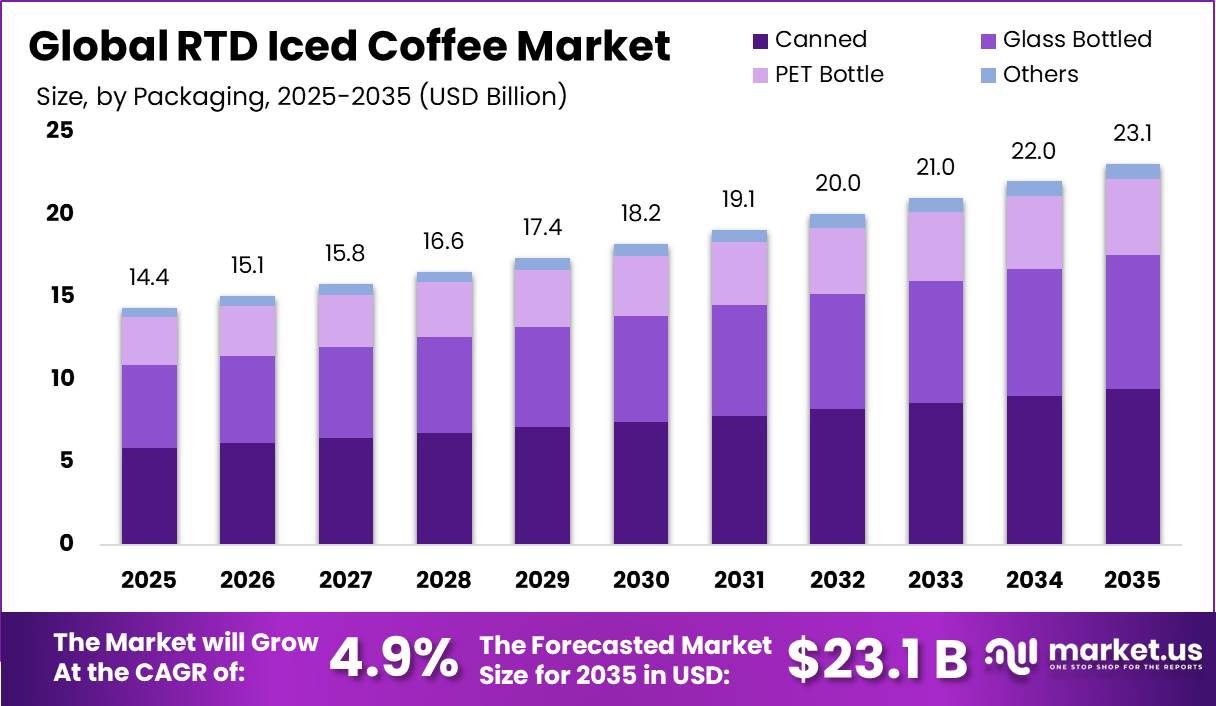

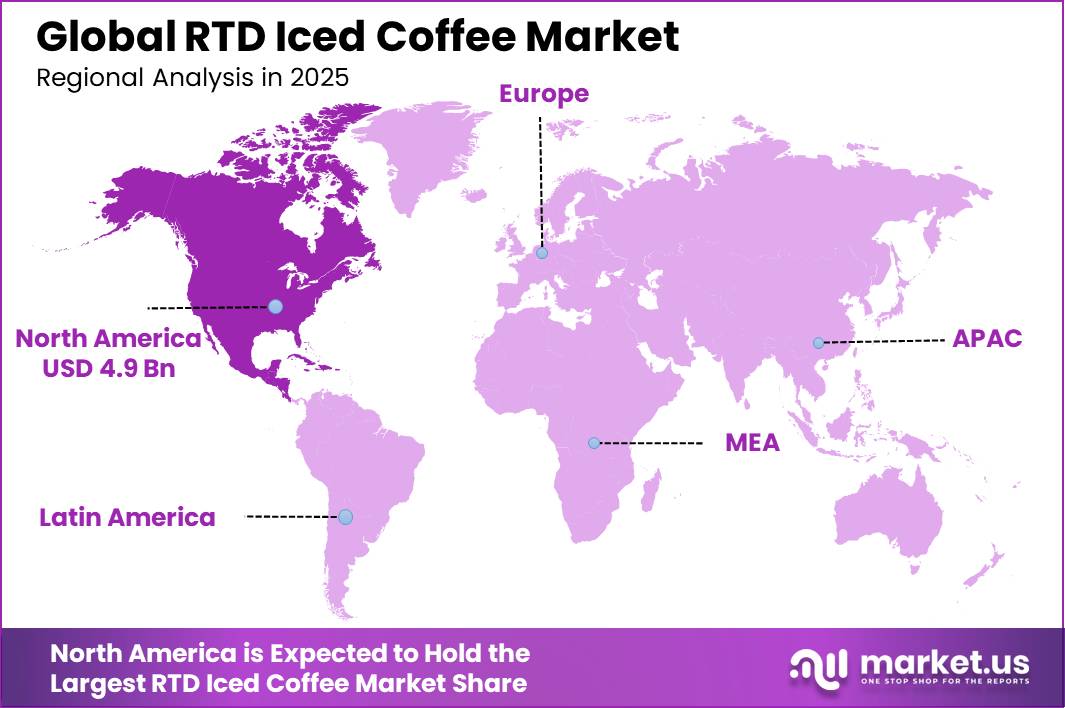

The Global RTD Iced Coffee Market was valued at USD 14.1 billion, and between 2026 and 2035, this market is estimated to register a CAGR of 4.9%, reaching about USD 23.1 billion by 2035. North America held a dominant market position, capturing more than a 34.8% share, holding USD 4.9 billion in revenue.

RTD iced coffee production is closely linked to upstream green coffee markets, where global coffee demand exceeds 170 million 60-kg bags annually, highlighting the scale of raw material dependency in beverage manufacturing ecosystems. The industry is characterized by high retail penetration across supermarkets, convenience stores, and e-commerce platforms, while innovation in cold brew, nitro coffee, and low-sugar formulations continues to redefine product portfolios.

From a consumption standpoint, global RTD coffee volume exceeded 31 billion liters in 2025, with canned RTD formats contributing 44% of total volume share, while PET bottles accounted for 29% of packaging demand, showing strong dominance of ready-packaged formats in retail distribution systems.

Industrial dynamics are further shaped by shifting beverage consumption patterns, where non-alcoholic beverage categories recorded 6.1% year-on-year dollar growth in early 2026, with RTD coffee maintaining positive but competitive positioning within the broader functional beverage segment. Growth is strongly influenced by rising demand for cold brew, nitro coffee, and low-sugar formulations, alongside increasing penetration of supermarket and convenience retail channels.

Key Takeaways

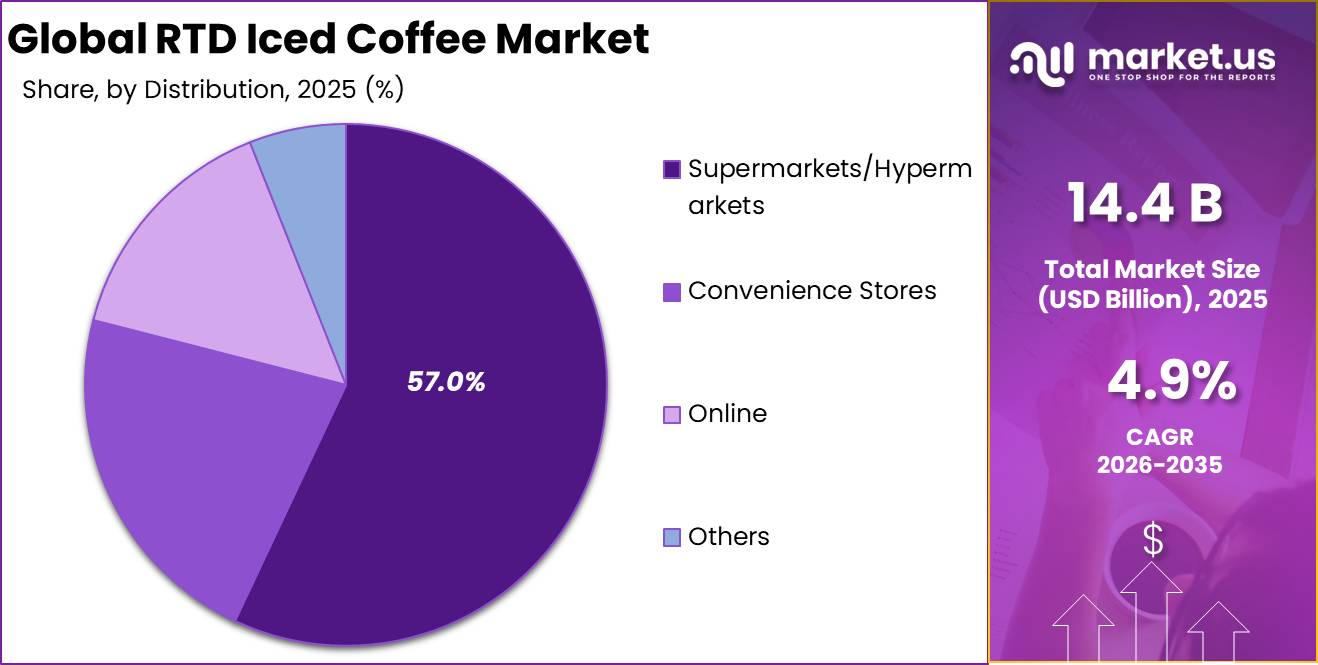

- The Global RTD Iced Coffee Market was valued at USD 14.4 billion in 2025.

- The market is projected to grow at a CAGR of 4.9% and is estimated to reach USD 23.1 billion by 2035.

- On the basis of packaging, the canned format dominated the market, constituting 41.0% of the total market share, owing to its portability, durability, and strong retail presence.

- Based on distribution channel, supermarkets and hypermarkets led the RTD iced coffee market with a substantial share of 57.0%, driven by wide product visibility and high consumer footfall.

- Based on price range, the mid-range segment led the market, comprising 45.0% of the total market, reflecting the broad consumer base seeking quality at an accessible price point.

- Among flavours, the classic flavour held a major share in the RTD iced coffee market, accounting for 48.0% of the market share, supported by consistent consumer preference for traditional cold coffee taste profiles.

- In 2025, North America was the most dominant region in the RTD iced coffee market, accounting for 34.8% of total global consumption, supported by high cold coffee penetration, established café culture, and strong retail infrastructure.

By Packaging

Canned Format Dominance in RTD Iced Coffee Packaging Landscape

The canned format dominates the RTD iced coffee packaging landscape, accounting for 41.0% of the market due to its superior portability, durability, extended shelf life, and strong retail presence across supermarkets and convenience stores. Because of its ability to preserve beverage freshness, maintain optimal temperature for longer periods of time, and withstand the rigors of transportation and retail handling, the canned format has emerged as the most popular packaging option among both manufacturers and consumers.

In March 2025, Starbucks launched its new Coffee & Protein RTD iced coffee range, rolling out cold brew and iced latte products in canned format across grocery and convenience stores including Walmart and Target nationwide in the United States, making Starbucks one of the most recognizable and widely distributed canned RTD iced coffee brands in the global market and further strengthening its retail leadership across both domestic and international channels.

By Distribution Channel

Supermarket and Hypermarket Leadership in RTD Iced Coffee Distribution Channels

Supermarkets and hypermarkets dominate the distribution landscape, accounting for 57.0% of total RTD iced coffee sales, thanks to high consumer footfall, widespread product visibility, and competitive shelf placement strategies. Supermarkets and hypermarkets offer RTD iced coffee brands a unique reach across diverse consumer demographics, with dedicated cold beverage sections, promotional shelf space, and multi-SKU product displays that promote both planned and spontaneous purchases.

In 2025, Nestlé’s Nescafé RTD iced coffee range expanded its distribution across Asia and Europe through leading supermarket chains such as Carrefour, Tesco, and Walmart, leveraging their extensive retail networks to achieve broad consumer reach and consistent sales volume across multiple geographies, further solidifying Nestlé’s position as one of the most widely available RTD iced coffee brands in the global market.

By Price Range

Mid-Range Pricing Segment Dominance in RTD Iced Coffee Market

The RTD iced coffee market’s price range is dominated by the mid-range segment, which accounts for 45.0% of the market, reflecting a broad consumer base seeking a balance of quality and affordability. The mid-range segment has emerged as the most commercially viable price tier for RTD iced coffee manufacturers, offering sufficient margin potential while remaining accessible to the broadest possible consumer base in both developed and emerging markets.

Products in this category typically have high-quality ingredients, recognizable brand identities, and a wide range of flavor options, making them the preferred choice for daily cold coffee consumption among working professionals, students, and urban millennials worldwide.

Blue Tokai Coffee Roasters in India began selling canned cold brew RTD products at a mid-range price point across urban supermarkets and online platforms in Bengaluru, Mumbai, and Delhi, successfully capturing a large and commercially active consumer segment and reflecting the growing appetite for affordable yet premium RTD iced coffee experiences among urban millennials and young professionals across India.

By Flavor

Prevalence of Classic Flavor Preference in RTD Iced Coffee Consumption

The classic flavor dominates the RTD iced coffee market, accounting for 48.0% of total market share, owing to consistent consumer preference for traditional cold coffee taste profiles across all age groups and geographies. The classic flavor’s enduring dominance reflects its universal appeal, providing a familiar, straightforward cold coffee experience that appeals to both occasional and frequent RTD iced coffee drinkers worldwide.

In 2025, Dunkin’ Donuts RTD iced coffee in its classic flavor variant continued to be the best-selling SKU in convenience stores and supermarkets across the United States, reflecting the enduring consumer preference for traditional taste profiles and demonstrating how classic flavors continue to anchor brand portfolios even as flavor innovation and premiumization accelerate rapidly across the RTD iced coffee category.

Key Market Segments

By Packaging

- Canned

- Glass Bottled

- PET Bottle

- Others

By Distribution Channel

- Supermarkets/Hypermarkets

- Convenience Stores

- Online

- Others

By Price Range

- Mid-Range

- Economy

- Premium

By Flavor

- Classic

- Caramel

- Vanilla

- Others

Market Dynamics

Challenges

Green coffee remains a persistent operating friction in the RTD iced coffee category because agricultural volatility is directly transmitted into packaged beverage margin instability, particularly for arabica-heavy chilled SKUs where formulation flexibility is limited without affecting taste. The ICO composite indicator averaged 296.89 US cents/lb in January 2026, declined to 267.57 cents/lb in February, and further to 256.05 cents/lb in May, reflecting a swing of more than 40 cents/lb within three months despite improving supply conditions.

At the same time, global green bean exports increased by 9.2% in December 2025 and 12.7% year-on-year in February 2026, indicating that supply expansion did not translate into procurement stability. For RTD producers, this mismatch creates elevated basis risk and contract timing uncertainty, with liquid coffee extract costs moving by roughly 6%–11% within two buying cycles.

The operational impact extends to strategy, reducing category growth potential by approximately 1.4 percentage points in 2026 in import-dependent markets. Mitigation requires deeper origin diversification across Brazil, Colombia, Vietnam, and robusta blends, shorter contract cycles, improved yield optimization from bean-to-extract processing, and increased use of flavor masking systems to stabilize formulation without relying purely on price pass-through.

| Challenge | (~) % CAGR Friction Drag | Geographic Relevance | Mitigation Horizon |

|---|---|---|---|

| Coffee input volatility | −1.4% | Latin America sourcing chains, North America core, EU import hubs, East Asia roasting centers | Medium term (2–4 years) |

| Packaging cost-compliance squeeze | −1.2% | EU regulatory hubs, North America core, UK retail channels | Medium term (2–4 years) |

| Cold-chain service inconsistency | −0.9% | North America convenience routes, APAC megacity corridors, GCC import logistics | Short term (≤ 2 years) |

| Functional reformulation complexity | −1.0% | U.S. premium retail, EU health-led channels, Japan-South Korea innovation markets | Medium term (2–4 years) |

| Aseptic capacity bottlenecks | −0.7% | Southeast Asia manufacturing bases, North America co-pack clusters, Western Europe | Long term (≥ 4 years) |

| Margin pressure in premiumization | −1.1% | North America core, Western Europe, urban China, developed APAC | Medium term (2–4 years) |

Opportunity

Functional protein RTD coffee represents a structural upside opportunity rather than a current demand driver, since most RTD iced coffee consumption still monetizes caffeine, flavor, and convenience rather than satiety or nutritional functionality. The category therefore remains under-penetrated relative to adjacent protein-heavy markets such as yogurt, protein snacks, and active nutrition, which already capture significant wellness-driven spending pools.

If even 6%–8% of mainstream RTD iced coffee volume shifts into higher-value functional SKUs priced 20%–35% above standard products, the category could generate a revenue uplift equivalent to roughly 120–180 basis points of incremental market CAGR. In addition, improved formulation economics and premium positioning could expand gross margins by approximately 200–400 basis points, particularly where pack sizing and ingredient systems support higher willingness to pay.

This opportunity is reinforced by existing consumption behavior patterns, such as cold beverages representing a dominant share of coffee-chain sales, with Starbucks reporting 75% of U.S. beverage sales from cold drinks and the scale of adjacent wellness categories. These dynamics indicate that demand for satiety and functional nutrition is already established, but not yet fully translated into the RTD coffee segment.

| Opportunity | (~) % Potential CAGR Upside | Geographic Relevance | Execution Window |

|---|---|---|---|

| Functional protein RTD coffee | +1.6% | North America core, EU, Japan, Korea, urban APAC | Short term (≤ 2 years) |

| At-home concentrate adjacencies | +1.3% | U.S., UK, China, Southeast Asia, GCC | Short term (≤ 2 years) |

| Affordable premium in tier-2/3 cities | +1.9% | India, Indonesia, Vietnam, Philippines, LatAm | Medium term (2–4 years) |

| Foodservice-exclusive refill systems | +0.9% | EU, UK, North America metros | Medium term (2–4 years) |

| Retail media and DTC data monetization | +0.8% | North America, Western Europe, developed APAC | Short term (≤ 2 years) |

| M&A roll-up of niche cold-coffee brands | +1.4% | U.S., EU, APAC selective | Medium term (2–4 years) |

Drivers

Packaging compliance and deposit-return schemes are becoming market-shaping forces in RTD coffee, increasingly favoring larger, better-capitalized brands. The EU packaging regulation entered into force in February 2025, with key requirements applying from August 12, 2026, introducing stricter recyclability standards and standardized recycling information requirements. Portugal’s deposit-return system also began in April 2026, with a €0.10 refundable deposit and a transition deadline after August 9, 2026, for registered packaging.

For RTD iced coffee, these changes require redesigning packaging specifications, updating labeling systems, and integrating deposit-return participation into route-to-market execution. This increases compliance costs and packaging qualification complexity, particularly around material approval, documentation, and recycling disclosures across regulated markets.

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cold beverage mainstreaming in coffee occasions | +1.6% | North America core, East Asia, urban APAC corridors, Western Europe catch-up | Short term (≤ 2 years) |

| Premium RTD format expansion via café-to-retail brand transfer | +1.3% | North America core, Japan/Korea, China metros, India premium spill-over, EU cities | Medium term (2–4 years) |

| Protein, low-sugar and functional formulation convergence | +1.1% | North America core, UK, Germany, Nordics, Australia, affluent APAC pockets | Medium term (2–4 years) |

| Convenience retail and immediate-consumption distribution density | +1.4% | Japan core, U.S. convenience/grocery, South Korea, Southeast Asia urban nodes, UK | Short term (≤ 2 years) |

| Packaging compliance and deposit-return transition favoring scaled brands | +0.8% | EU, UK-adjacent supply chains, Iberia, selected high-regulation markets | Medium term (2–4 years) |

| Coffee cost normalization after 2024–2025 spike improves promo economics | +0.9% | Global, strongest in import-dependent North America, EU, East Asia | Short term (≤ 2 years) |

Restraints

Coffee input volatility remains a key near-term restraint for RTD iced coffee because the category is directly exposed to green coffee price swings while operating in a highly price-transparent retail environment that limits full pass-through. The ICO Composite Indicator averaged 256.05 US cents/lb in May 2026, remaining elevated through late 2025 and early 2026 and still structurally above historical budgeting norms for beverage processors.

For mainstream RTD iced coffee, where coffee extract, dairy or plant-based, sweeteners, and packaging already create a tight cost stack, a sustained 15%–25% increase in bean and extract costs can translate into approximately 120–220 basis points of gross margin compression if only half is recovered through pricing. This pressure is most acute in multi-serve and convenience-channel SKUs that rely on frequent promotions and limited pricing flexibility.

As a result, brands often respond by delaying flavor extensions, reducing promotional intensity by 5%–10%, and rationalizing lower-velocity SKUs. Collectively, these adjustments contribute to an estimated −1.4 percentage point impact on 2026 baseline CAGR in key premium coffee markets such as North America, Europe, Japan, and Korea, where consumer sensitivity to repeated price increases is rising.

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Coffee input volatility | −1.4% | North America core, EU, Japan, Korea | Short term (≤ 2 years) |

| Aluminum can cost inflation | −1.1% | U.S., Canada-linked flows, LatAm export lanes | Short term (≤ 2 years) |

| Sugar and label compliance | −0.9% | U.S., UK, EU, developed APAC | Medium term (2–4 years) |

| Refrigerated shelf-life drag | −0.8% | North America premium, EU urban retail, Japan | Medium term (2–4 years) |

| Packaging regulation burden | −0.7% | EU core, UK adjacency | Long term (≥ 4 years) |

| Shelf-space substitution | −0.9% | North America, UK, Korea, urban APAC | Medium term (2–4 years) |

Geopolitical Impact Analysis

Changes in trade policy and the imposition of import tariffs on coffee beans, packaging materials, and finished beverage products have created significant cost pressures throughout the RTD iced coffee value chain. Uncertainty around import duties on aluminum, a key component in canned RTD iced coffee, has largely been driven by ongoing trade tensions between the United States and major coffee-producing countries, as well as between large economies like the United States and China.

The cross-border movement of finished RTD beverage products has also been impacted by retaliatory tariff measures between trading blocs, making it increasingly challenging for brands looking to expand their distribution across international supermarkets and hypermarkets.

Manufacturers are forced by these trade disruptions to reevaluate their sourcing strategies, diversify their supplier bases, and either absorb or pass on additional costs across premium and mid-range price segments. In order to avoid import taxes and maintain its competitive positioning in the rapidly expanding Asia Pacific RTD iced coffee market, Starbucks RTD accelerated local manufacturing partnerships in China during the 2018–2020 U.S.-China trade war.

Regional Analysis

North America remains the dominant regional market for RTD iced coffee, accounting for approximately 34.8% share in 2025, supported by highly automated beverage manufacturing systems and advanced cold-chain logistics networks. The region operates large-scale aseptic filling lines typically running at 6,000 to 48,000 units per hour, enabling continuous high-volume production of canned cold brew and flavored RTD coffee formats for national distribution.

Cold brew extraction systems widely deployed in the region function under controlled conditions of 8–24 hours steeping at 4–10°C, ensuring consistent flavor profiling across industrial batches. Shelf-life performance is also structurally strong, with aseptic RTD coffee achieving 6–12 months ambient stability, while refrigerated variants maintain 7–30 days stability at 0–4°C, supporting wide retail penetration across supermarkets and convenience stores (2025 food processing standards).

In contrast, Asia-Pacific is emerging as the fastest-expanding operational region for RTD iced coffee, driven by rapid scaling of production capacity and high-frequency consumption systems. Japan alone operates one of the densest vending ecosystems globally, dispensing approximately 5 million beverages per day, a significant share of which includes canned iced coffee formats, enabling continuous real-time consumption cycles.

Across China and Southeast Asia, RTD manufacturing facilities are increasingly deploying high-throughput aseptic bottling lines operating between 12,000 and 36,000 units per hour, reflecting rapid industrial scaling to meet urban demand growth.

Key Regions and Countries Covered in this Report

North America

- The US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia & CIS

- Rest of Europe

APAC

- China

- Japan

- South Korea

- India

- ASEAN

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

The global RTD iced coffee market reflects a consolidated market structure, where a small number of multinational giants such as Starbucks, Nestlé, The Coca-Cola Company, PepsiCo, and Suntory Holdings collectively dominate the majority of the market share. These players maintain their stronghold through wide-reaching distribution networks, strong brand equity, and continuous product innovation across flavors, packaging formats, and price segments.

However, the market is gradually witnessing disruption from emerging specialty and plant-based RTD coffee brands that are challenging established hierarchies by targeting premium and health-conscious consumers through unique formulations and direct-to-consumer digital strategies.

This dynamic is slowly shifting the competitive landscape from a purely consolidated format toward a more fragmented one in niche and premium segments, making the overall market behavior a blend of consolidated dominance at the mass level and growing fragmentation at the specialty and functional product level.

Key Players

- The Coca-Cola Company

- Starbucks Corporation

- Nestlé S.A.

- PepsiCo Inc.

- Suntory Holdings Limited

- Unilever PLC

- Danone S.A.

- Uni-President Enterprises Corp.

- Illycaffè S.p.A.

- Asahi Group Holdings, Ltd.

- Monster Beverage Corporation

- Califia Farms, LLC

- High Brew Coffee

- La Colombe Coffee Roasters

- Jacob Douwe Egberts (JDE)

- Coca-Cola Europacific Partners

- Starbucks Japan

- Keurig Dr Pepper Inc.

- Others

Key Development

- In March 2025, Starbucks announced two new ready-to-drink lines, RTD Starbucks Iced Energy and RTD Starbucks Frappuccino Lite, with an immediate rollout across the United States, targeting health-conscious and on-the-go consumers looking for lighter and more functional iced coffee options.

- In April 2025, Nestlé launched an expanded Nescafé Ready-to-Drink cold coffee range, introducing new RTD iced coffee variants designed for portable consumption and targeting growing demand for convenient chilled coffee beverages across global retail markets, including emerging and fast-growing regions such as India, Brazil, and the Middle East and North Africa.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 14.4 Bn |

| Forecast Revenue (2035) | USD 23.1 Bn |

| CAGR (2026–2035) | 4.9% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020–2024 |

| Forecast Period | 2026–2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Packaging (Canned, Glass Bottled, PET Bottle, and Others), By Distribution Channel (Supermarkets/Hypermarkets, Convenience Stores, Online, and Others), By Price Range (Premium, Mid-Range, and Economy), By Flavor (Classic, Caramel, Vanilla, and Others) |

| Regional Analysis | North America – The US & Canada; Europe – Germany, France, The UK, Spain, Italy, Russia & CIS, Rest of Europe; APAC – China, Japan, South Korea, India, ASEAN & Rest of APAC; Latin America – Brazil, Mexico & Rest of Latin America; Middle East & Africa – GCC, South Africa, & Rest of MEA |

| Competitive Landscape | The Coca-Cola Company, Starbucks Corporation, Nestlé S.A., PepsiCo Inc., Suntory Holdings Limited, Unilever PLC, Danone S.A., Uni-President Enterprises Corp., Illycaffè S.p.A., Asahi Group Holdings Ltd., Monster Beverage Corporation, Califia Farms LLC, High Brew Coffee, La Colombe Coffee Roasters, Jacob Douwe Egberts (JDE), Coca-Cola Europacific Partners, Starbucks Japan, Keurig Dr Pepper Inc., and others. |

| Customization Scope | Customization for segments and region- and country-level will be provided. Moreover, customization can be tailored to the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited Users and Printable PDF) |