Quick Navigation

Report Overview

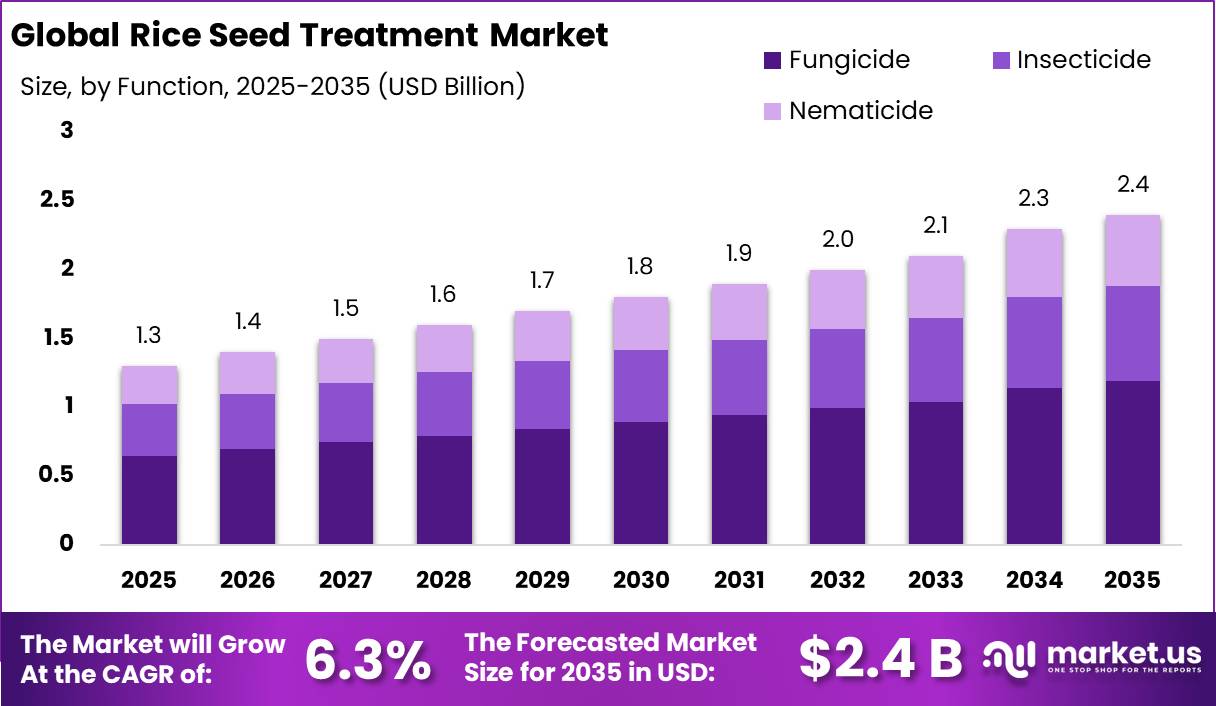

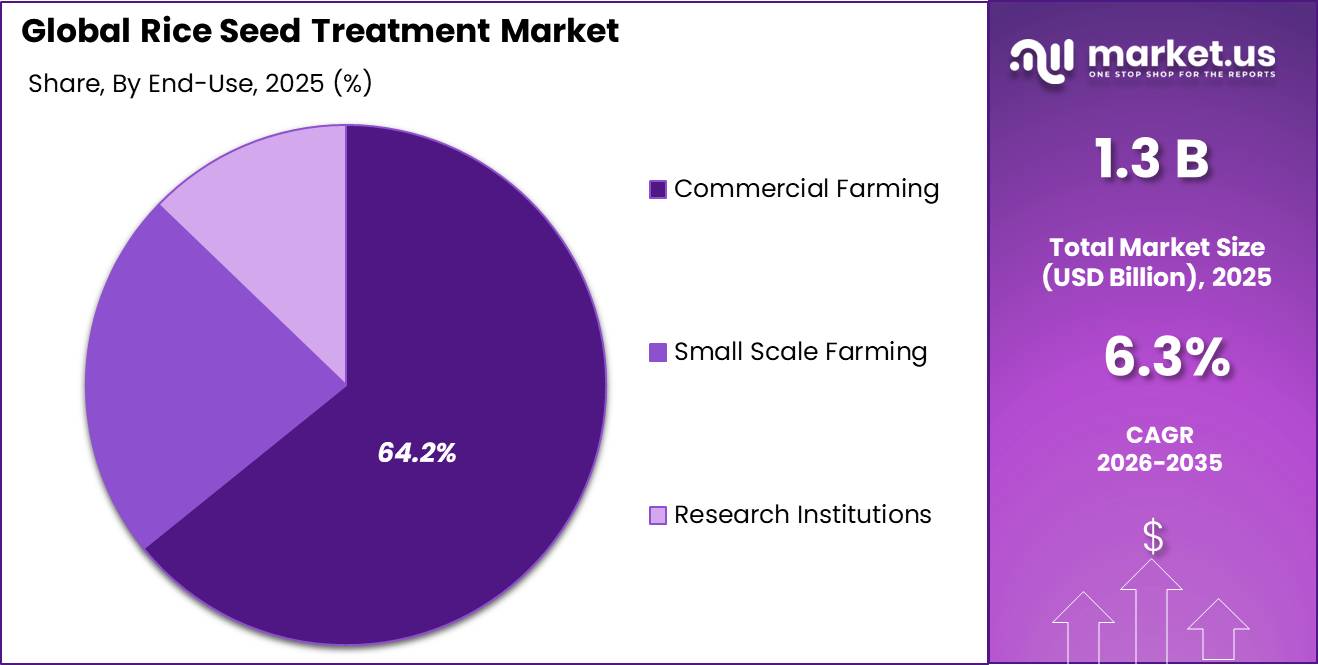

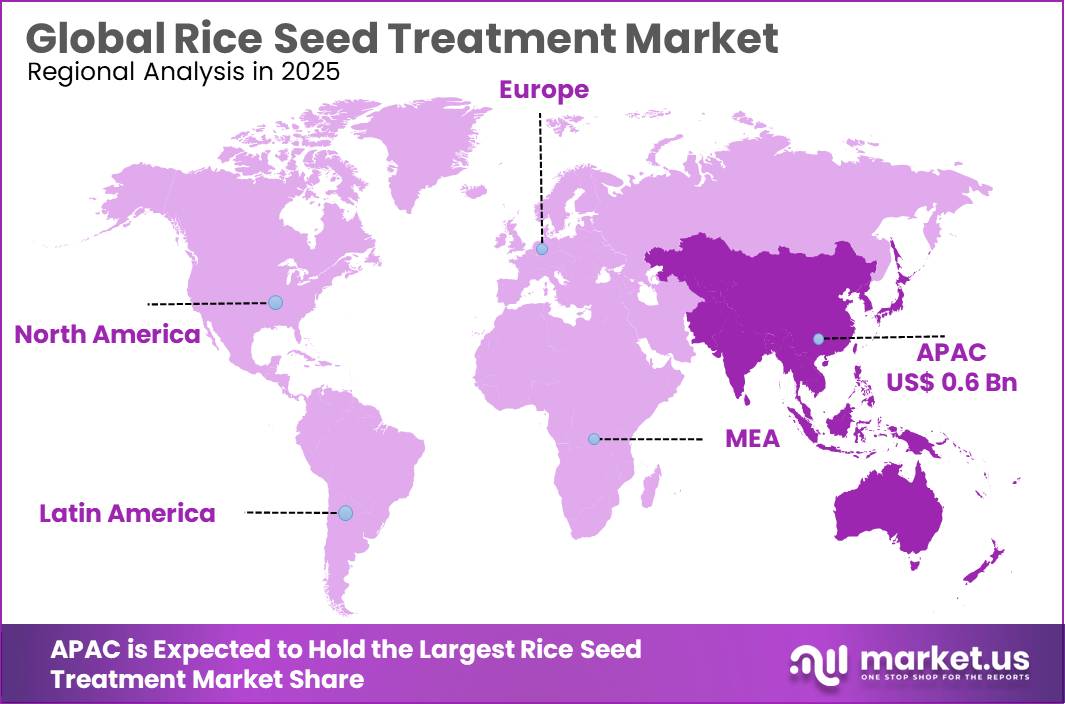

The Global Rice Seed Treatment Market size is expected to be worth around USD 2.4 Billion by 2035, from USD 1.3 Billion in 2025, growing at a CAGR of 6.3% during the forecast period from 2026 to 2035. In 2025, Asia Pacific held a dominant market position, capturing more than a 51.3% share, holding USD 0.6 Billion revenue.

Rice seed treatment is gaining industrial relevance as growers seek stronger crop establishment, lower early-stage disease losses, and more efficient input use. Globally, rice remains a strategic food crop, with FAO forecasting 2025/26 rice output at a record 563.4 million tonnes, up 2.0% year over year, creating a large base for seed-applied fungicides, insecticides, biologicals, micronutrients, and polymer coatings.

Key Takeaways

- Rice Seed Treatment Market size is expected to be worth around USD 2.4 Billion by 2035, from USD 1.3 Billion in 2025, growing at a CAGR of 6.3%.

- Fungicide held a dominant market position, capturing more than a 49.6% share in the rice seed treatment market.

- Chemical Treatment held a dominant market position, capturing more than a 59.2% share in the rice seed treatment market.

- Seed Coating held a dominant market position, capturing more than a 43.5% share in the rice seed treatment market.

- Commercial Farming held a dominant market position, capturing more than a 64.2% share in the rice seed treatment market.

- Asia-Pacific emerged as the dominant region in the Rice Seed Treatment Market, accounting for 51.3% of the total market share and reaching a value of USD 0.6 Billion.

The industry scenario is shaped by high planting intensity, climate stress, and pressure to protect yield from seed- and soil-borne pathogens. USDA-linked rice outlook data projects global 2025/26 rice consumption at 541.7 million tonnes and ending stocks at 190.9 million tonnes, indicating that food-security buffers remain important but still depend on stable crop establishment. Seed treatment therefore functions as a preventive, low-dose technology applied before sowing, supporting uniform germination and early vigor.

Driving factors include expanding food demand, weather volatility, pesticide-efficiency goals, and regulatory preference for targeted application rather than broad field spraying. OECD-FAO projects rice yields to reach around 3.5 tonnes/hectare by the end of the decade, implying that productivity gains will increasingly depend on seed quality, crop protection precision, and integrated agronomy.

In the United States, EPA continues to provide technical guidance for occupational exposure assessment in seed-treatment operations, showing that treated seed remains a recognized crop-protection pathway under regulated handling systems. The European Commission’s Farm to Fork framework targets a 50% reduction in chemical pesticide use and risk and a 50% reduction in more hazardous pesticides by 2030, encouraging more precise technologies such as seed treatment and biological seed-applied solutions.

Government and institutional programs are also supporting adoption. In the Philippines, the RCEF seed program distributed about 2.5 million bags of certified inbred rice seed for the 2025 wet season, supporting over 1 million farmers and around 1.06 million hectares. In Viet Nam, a World Bank-supported low-carbon rice initiative received a US$1.5 million grant to support policy and advisory work for green agriculture transformation.

Bayer AG remains relevant through its Crop Science platform, which links seeds, crop protection, biological products, and digital tools. Bayer reported 2025 group sales of €45.575 billion and EBITDA before special items of €9.669 billion, showing continued financial scale behind agricultural innovation. In 2025, Bayer also decided to exit the U.S. seed-treatment equipment business while stating continued commitment to seed treatments, indicating portfolio focus rather than withdrawal from seed-applied crop protection.

By Function Analysis

Fungicide dominates with 49.6% share due to its strong role in protecting rice seeds from fungal diseases and improving early crop establishment.

In 2025, Fungicide held a dominant market position, capturing more than a 49.6% share in the rice seed treatment market by function. This leadership was mainly supported by the growing need to protect rice seeds from fungal infections during storage, germination, and early plant growth stages. Farmers continued to prefer fungicide-based seed treatment because it offers an effective first layer of protection against seed-borne and soil-borne diseases, helping improve seed performance and reduce crop losses. The increasing focus on achieving better crop quality and stable yield outcomes further strengthened its use across rice-producing regions.

By Type of Treatment Analysis

Chemical Treatment dominates with 59.2% share due to its reliable seed protection and consistent support for healthy rice crop establishment.

In 2025, Chemical Treatment held a dominant market position, capturing more than a 59.2% share in the rice seed treatment market by type of treatment. Its strong market presence was supported by its wide adoption for protecting rice seeds against diseases, pests, and early-stage crop stress before planting. Farmers continued to prefer chemical treatment methods because they provide targeted protection at the seed level, helping improve germination rates and support uniform crop growth. The approach also remained practical due to its ease of application and ability to reduce early field losses, making it an important part of rice cultivation practices.

By Application Analysis

Seed Coating dominates with 43.5% share due to its effective delivery of seed protection and support for uniform crop emergence.

In 2025, Seed Coating held a dominant market position, capturing more than a 43.5% share in the rice seed treatment market by application. Its strong market presence was driven by its ability to apply protective and performance-enhancing materials directly onto rice seeds before planting. Seed coating continued to gain preference among growers because it supports better seed handling, improves treatment coverage, and helps maintain consistent seed quality. The method also contributed to improved germination and stronger early-stage crop establishment, making it a practical choice across rice cultivation activities.

By End Use Analysis

Commercial Farming dominates with 64.2% share due to its higher focus on productivity, crop protection, and large-scale rice cultivation practices.

In 2025, Commercial Farming held a dominant market position, capturing more than a 64.2% share in the rice seed treatment market by end use. This leading position was supported by the increasing adoption of treated rice seeds across large-scale farming operations focused on improving yield consistency and reducing crop risks. Commercial growers continued to invest in seed treatment solutions to strengthen crop establishment, protect seed quality, and improve field performance from the early growth stages. The use of treated seeds also supported better operational efficiency and helped optimize agricultural inputs across larger cultivation areas.

Key Market Segments

By Function

- Fungicide

- Insecticide

- Nematicide

By Type of Treatment

- Chemical Treatment

- Biological Treatment

- Physical Treatment

- Integrated Treatment

By Application

- Seed Coating

- Seed Dressing

- Seed Pelleting

By End Use

- Commercial Farming

- Small Scale Farming

- Research Institutions

Emerging Trends

Shift Toward Low-Dose, Targeted Seed Protection

A major latest trend in rice seed treatment is the move toward low-dose, targeted products that protect the seed and root zone early, instead of relying only on repeated field spraying. This trend is growing because rice demand is still rising. FAO forecasts global rice production at 563.4 million tonnes in 2025/26, up 2.0%, which keeps pressure on farmers to protect every plant stand from the start.

Syngenta’s VICTRATO, based on TYMIRIUM technology, is one example of this shift. The company says it targets nematodes and soil-borne fungal diseases and can be used in crops including rice, cereals, corn, soybean and cotton. This shows how seed treatment is becoming more precise, root-focused and sustainability-linked.

Stronger Focus on Seed Health and Early Disease Control

Another important trend is the stronger focus on seed health, especially against early rice diseases such as rice blast and bakanae. Bayer’s Routine Start is described as a specialized rice seed treatment that enhances resistance to 2 key diseases: rice blast and bakanae, using 2 active ingredients, trifloxystrobin and isotianil.

This reflects a practical industry direction: companies are trying to give seedlings better protection before stress becomes visible in the field. The need is also supported by long-term food security demand. OECD-FAO projects global rice production to reach 598 million tonnes by 2034, with growth mainly coming from yield improvement. In simple terms, treated seed is becoming a small but important tool to help farmers protect crop potential from the first stage.

Drivers

Rising Global Rice Production and the Need to Protect Seed Quality is Driving Rice Seed Treatment Adoption

Rice continues to be one of the most important food crops in the world, and increasing production targets are creating stronger demand for technologies that improve crop establishment from the beginning of the growing cycle. According to the Food and Agriculture Organization (FAO), global rice production is projected to reach a record 543 million tonnes (milled equivalent) in the 2024/25 season. This growth is being supported by major rice-producing countries that are focusing on improving productivity and reducing field losses.

As rice cultivation expands and farmers aim for stable output, seed quality has become more important than ever. Seed treatment is increasingly used because it helps protect seeds from fungal infection, pest damage, and poor germination during the early growth period. Healthy seed performance at planting directly supports better crop establishment and more reliable yields, especially in large-scale rice farming systems. These factors are creating steady demand for rice seed treatment solutions across producing regions.

Government Seed Improvement Programs and Certified Seed Promotion Supporting Market Growth

Government-led initiatives and seed quality improvement programs are also becoming an important force behind the rice seed treatment market. In India, the National Food Security Mission (NFSM) supported the distribution of nearly 74 lakh quintals of certified seeds of improved crop varieties between 2014–15 and 2019–20 to strengthen seed replacement and increase agricultural productivity.

The program has placed strong attention on improving access to quality seeds and promoting better seed management practices across farming communities. In addition, national seed development efforts continue to support infrastructure for seed cleaning, grading, processing, seed treatment, packaging, and storage. These initiatives are encouraging growers to adopt treated and certified seeds to improve field performance and reduce early-stage crop risk.

Restraints

Strict Regulatory Controls and Higher Compliance Costs are Limiting Wider Adoption of Rice Seed Treatment

One of the major factors restricting the growth of the rice seed treatment market is the increasing regulatory pressure around the use of chemical crop protection products and treated seeds. The Food and Agriculture Organization (FAO) highlights that pesticide management now requires stricter regulatory and technical measures across the entire product lifecycle to reduce risks to human health and ecosystems.

For seed treatment manufacturers and distributors, these requirements often translate into higher development costs and longer commercialization timelines. In some regions, farmers also face limitations in accessing certain treatment products due to evolving regulations. Although these measures support sustainable agriculture, they can slow product adoption and reduce flexibility for growers seeking cost-effective crop protection options.

Higher Treatment Costs and Limited Adoption Among Small Farmers Create Growth Challenges

Another important restraint comes from the cost sensitivity of agricultural operations, especially among small and medium-scale farmers. FAO notes that high adoption costs remain one of the key barriers to implementing advanced agricultural technologies at the farm level. Many growers prioritize immediate production expenses over preventive seed investments, particularly when margins are uncertain.

In addition, FAO guidance for treated seeds indicates that high-quality seed coatings and improved treatment practices are often required to reduce environmental exposure and improve performance. While these standards can reduce dust dispersion by up to 90% when combined with proper coating and drilling practices, they may also increase the overall cost of treated seeds and supporting equipment.

Opportunity

Growth Opportunity: Rising Need for Better Rice Productivity Through Seed Protection

Rice remains the main food for more than half of the world’s population, which means even small improvements in crop performance create a large impact on food availability. Because of this, rice seed treatment is becoming an important growth opportunity. Seed treatment means protecting seeds before sowing through biological, physical, or approved chemical methods so that young plants start healthy and grow stronger.

According to the Food and Agriculture Organization (FAO), rice is cultivated on nearly 146 million hectares globally and demand for rice continues to rise as population grows. FAO projections indicate that global rice demand could reach around 880 million tons, increasing pressure on farmers to produce more from existing farmland.

Research highlighted by FAO and agricultural institutions shows that seed-borne pathogens reduce seed quality, weaken germination, and lower yields. Studies indicate that healthy seed management and treatment can improve crop establishment while reducing dependency on repeated pesticide applications later in the season. In severe situations, seed-borne diseases may lead to 15–90% yield losses, making preventive treatment economically valuable.

Government and Institutional Push Toward Quality Seed Systems

Another major growth opportunity for rice seed treatment comes from government and international efforts focused on seed quality and food security. Across many countries, agricultural programs are moving from simply increasing cultivated area to improving the quality of inputs used by farmers—and seed quality sits at the center of that strategy.

FAO states that quality seed must meet standards for germination, physical purity, and phytosanitary health, because stronger seed quality directly supports reliable food production. Seed testing and treatment are now recognized as essential parts of modern agriculture and national seed systems.

Governments and public agricultural institutions are also encouraging lower crop losses and more efficient farming. FAO estimates that around 14% of food produced globally is lost before reaching retail, showing why early-stage interventions such as quality seed and seed treatment are receiving more attention.

Regional Insights

Asia-Pacific dominates the Rice Seed Treatment Market with a 51.3% share, valued at USD 0.6 Billion, supported by large-scale rice cultivation and rising focus on seed quality improvement.

Asia-Pacific emerged as the dominant region in the Rice Seed Treatment Market, accounting for 51.3% of the total market share and reaching a value of USD 0.6 Billion. The region’s leadership is strongly connected to its position as the world’s largest rice-producing and rice-consuming area. Countries including China, India, Indonesia, Vietnam, Thailand, and Bangladesh continue to depend heavily on rice as a staple crop, creating consistent demand for technologies that improve crop establishment and productivity.

The region contributes the majority of global rice production, which supports continuous investment in agricultural inputs and seed improvement practices. According to international agricultural estimates, Asia produces nearly 90% of the world’s rice output, making seed performance and crop protection critical priorities across farming systems. Seed treatment has gained wider acceptance as growers increasingly focus on reducing seed loss, improving germination rates, and strengthening early crop growth.

Key Regions and Countries Insights

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

Bayer AG remains one of the recognized participants in the rice seed treatment market through its broad agricultural portfolio and focus on seed and crop protection technologies. The company operates in more than 80 countries and generated approximately EUR 46 billion in total revenue in 2025 across its business segments. Through its agricultural division, Bayer continues investing in seed protection solutions designed to improve seed performance and reduce early crop losses.

Syngenta Group continues to maintain a strong position in the rice seed treatment market with extensive offerings across crop protection and seed technologies. The company operates in over 100 countries and reported annual sales exceeding USD 32 billion across its business operations. Syngenta focuses on improving seed health and early-stage crop development through advanced treatment approaches.

Corteva Inc. remains an important player in the rice seed treatment market through its integrated seed and crop protection portfolio. The company recorded annual net sales of approximately USD 17 billion and supports agricultural operations across more than 140 countries. Corteva continues focusing on research-driven seed solutions aimed at improving crop establishment and seed performance.

Top Key Players Outlook

- Bayer AG

- Syngenta Group

- Corteva Inc.

- BASF SE

- UPL Limited

- Nufarm Limited

- FMC Corporation

- Croda International Plc

- Koppert Biological Systems BV

- Verdesian Life Sciences, LLC

- Crystal Crop Protection Limited

Recent Industry Developments

In 2026, Nufarm reported half-year underlying EBITDA of AUD 243 million, up 18%, and underlying NPAT of AUD 52 million, up 35%, supported by better portfolio mix and cost control. On partnership and agreement, Nufarm expanded its bp partnership to 2050 for seed technology development, while its 2026 strategy focused on external innovation partnerships, selective exits, and higher-return markets.

In 2026, UPL reported FY26 revenue of ₹51,839 crore, with performance supported by crop protection, seeds, and Asia-Pacific demand. On expansion, UPL continued strengthening its crop protection platform and announced restructuring plans to create a focused listed crop protection entity.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 1.3 Bn |

| Forecast Revenue (2035) | USD 2.4 Bn |

| CAGR (2026-2035) | 6.3% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Function (Fungicide, Insecticide, Nematicide), By Type of Treatment (Chemical Treatment, Biological Treatment, Physical Treatment, Integrated Treatment), By Application (Seed Coating, Seed Dressing, Seed Pelleting), By End Use (Commercial Farming, Small Scale Farming, Research Institutions) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – GCC, South Africa, Rest of MEA |

| Competitive Landscape | Bayer AG, Syngenta Group, Corteva Inc., BASF SE, UPL Limited, Nufarm Limited, FMC Corporation, Croda International Plc, Koppert Biological Systems BV, Verdesian Life Sciences, LLC, Crystal Crop Protection Limited |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |