Quick Navigation

Report Overview

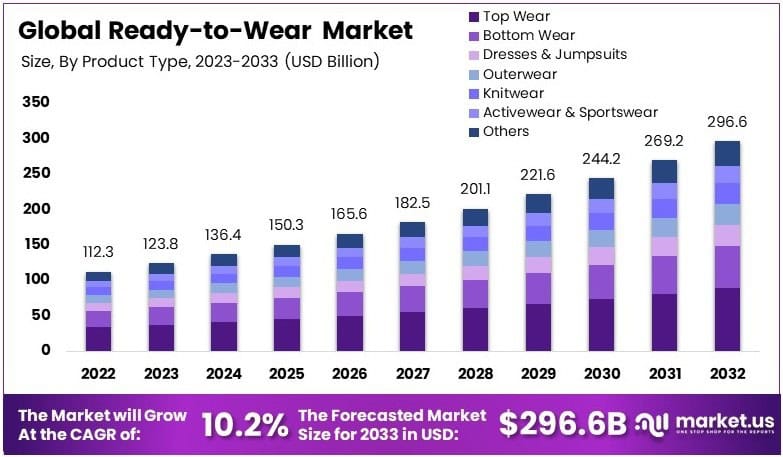

The Global Ready-to-Wear Market size is expected to be worth around USD 296.6 Billion by 2033, from USD 112.3 Billion in 2023, growing at a CAGR of 10.2% during the forecast period from 2024 to 2033.

Ready-to-wear refers to clothing that is mass-produced and sold in standard sizes. These garments are designed for immediate wear without the need for customization or tailoring. They cater to a wide audience and are made using efficient production methods. The focus is on convenience, affordability, and style.

The ready-to-wear market includes the global trade of pre-manufactured apparel designed for direct consumer purchase. It encompasses various segments like casual, formal, and seasonal clothing. The market is driven by consumer demand for affordable, fashionable, and ready-to-wear options.

The ready-to-wear market is growing due to increasing consumer preference for convenience and affordability. In 2023, global apparel exports reached $435 billion, with China leading at $293.6 billion. Moreover, government incentives like the Production Linked Incentive (PLI) scheme aim to boost exports to $50 billion by 2030, enhancing market competitiveness.

Bangladesh, the third-largest exporter, earns 83% of total export revenue from RMG, with $27.4 billion in exports by 2020, capturing 6.3% of the global market. Additionally, major brands like H&M, sourcing from 1,000 factories, demonstrate demand. As a result, the sector supports global supply chains while driving local economic growth.

Sustainability is a major driver. Notably, the EU Strategy for Sustainable and Circular Textiles promotes durable, recyclable textiles by 2030. Companies like H&M and Inditex invest in startups like Circ to advance circular fashion. Consequently, demand for sustainable garments is increasing, creating opportunities for innovation and investment in eco-friendly production methods.

The market remains competitive yet fragmented. However, overproduction and microplastics release challenge sustainability efforts. Meanwhile, regions like China dominate, with 8.7% of GDP tied to textiles. In contrast, smaller markets face saturation. Thus, maintaining competitiveness requires diversification and adopting sustainability-focused initiatives.

Governments play a vital role in shaping the market. Specifically, the PLI scheme allocates $2.37 billion to enhance technical textiles and man-made fibers. Furthermore, EU regulations aim to reduce environmental harm by 2030, influencing global and local markets. Consequently, regulatory support bolsters growth while driving innovation.

Key Takeaways

- The Global Ready-to-Wear Market was valued at USD 112.3 Billion in 2023 and is expected to reach USD 296.6 Billion by 2033, with a CAGR of 10.2% during the forecast period.

- In 2023, Tops & T-Shirts dominated the product type segment due to their versatility and widespread appeal, becoming wardrobe staples globally.

- In 2023, Cotton led the material segment, valued for its comfort, breathability, and growing demand for sustainable and organic variants.

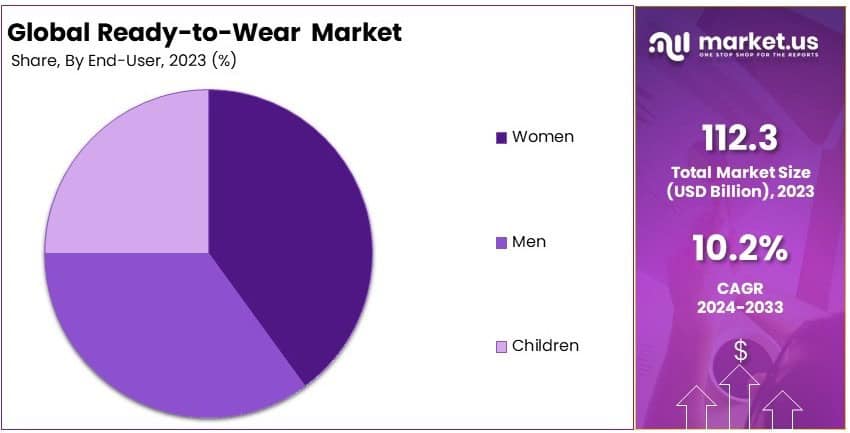

- In 2023, Women dominated the end-user segment, driven by their broader range of clothing needs and higher engagement with fashion trends.

- In 2023, Mid-range pricing led the price range segment, balancing affordability and quality, appealing to a large consumer base.

- In 2023, North America held 38.4% of the market share, supported by its advanced retail infrastructure and high disposable incomes driving fashion demand.

Product Type Analysis

Tops & T-Shirts dominate due to their versatility and widespread appeal.

The Ready-to-Wear market’s Product Type segment showcases a diverse range of clothing items tailored to various consumer preferences. Among these, Tops & T-Shirts stand out as the dominant sub-segment. This dominance is primarily driven by their versatility, affordability, and the ability to cater to a broad demographic.

Tops and t-shirts are staple items in most wardrobes, offering endless styling possibilities for different occasions, whether casual or semi-formal. The ease of customization and the continuous introduction of new designs and prints also contribute to their popularity. Additionally, the rise of fast fashion brands has made trendy tops and t-shirts more accessible to consumers, further fueling their demand.

Moreover, advancements in fabric technology, such as moisture-wicking and stretchable materials, have enhanced the functionality and comfort of tops and t-shirts, making them even more appealing to a health-conscious and active consumer base.

Other sub-segments within Product Type include Bottom Wear, Dresses and Jumpsuits, Outerwear, Knitwear, Activewear and Sportswear, and Others. Bottom Wear, encompassing jeans, trousers, and skirts, supports growth by offering essential wardrobe pieces that complement tops and t-shirts. Dresses and Jumpsuits appeal to consumers seeking ready-made outfits for various occasions, while Outerwear, including jackets and coats, is driven by seasonal demand and the need for functional yet stylish outer garments.

Material Analysis

Cotton dominates due to its comfort and breathability.

In the Ready-to-Wear market, the Material segment plays a crucial role in defining product quality, consumer preference, and overall market dynamics. Cotton emerges as the leading material, valued for its natural comfort, breathability, and versatility, making it a preferred choice for a wide range of clothing items.

Cotton fabrics are highly favored for their softness and ability to keep the wearer comfortable in various climates, which enhances their appeal across different regions and demographics. Additionally, cotton is easy to dye and print on, allowing for vibrant and diverse designs that attract fashion-conscious consumers.

The sustainability aspect of cotton also contributes to its market leadership, as consumers increasingly seek eco-friendly and natural materials. Organic cotton, in particular, has gained traction due to growing environmental awareness and the demand for sustainable fashion.

Other materials in the Ready-to-Wear market include Wool, Silk, Denim, Synthetic Fabrics, and Others. Wool is prized for its warmth and durability, making it essential for outerwear and winter collections. Silk is favored for its luxurious feel and sheen, often used in high-end and formal wear. Denim holds significant popularity in casual and versatile clothing such as jeans and jackets.

Synthetic Fabrics, including polyester and nylon, are valued for their durability, elasticity, and cost-effectiveness, extensively used in activewear and sportswear due to their performance-enhancing properties. The Others category encompasses a variety of niche materials that cater to specific market needs, such as linen for summer wear and blends that combine different fibers to enhance fabric performance and aesthetics.

End-User Analysis

Women dominate due to their higher engagement with fashion trends and diversity in clothing needs.

The End-User segment of the Ready-to-Wear market highlights the distinct preferences and purchasing behaviors of different consumer groups. Women represent the largest sub-segment, driven by their broader range of clothing needs and greater engagement with fashion trends compared to other demographics.

Women’s apparel includes a variety of styles, colors, and designs, catering to different occasions, seasons, and personal preferences. Additionally, the rise of social media and influencer culture has significantly influenced women’s fashion choices, driving demand for the latest trends and innovative designs.

Marketing strategies targeted at women often emphasize style, versatility, and quality, resonating well with their preferences and enhancing brand loyalty. The increasing participation of women in the workforce and the growing trend of casual and athleisure wear also contribute to the sustained demand in this sub-segment.

Other sub-segments within End-User include Men and Children. Men account for a substantial portion of the market, driven by a steady demand for essentials such as shirts, trousers, and outerwear. The men’s segment is expanding as more brands introduce a variety of styles and cater to the increasing interest in fashion among men.

Children represent another significant sub-segment, with demand driven by the need for durable, comfortable, and stylish clothing that caters to the active lifestyles of younger consumers. This sub-segment benefits from the constant growth in birth rates and the trend of parents investing in high-quality, fashionable clothing for their children.

Price Range Analysis

Mid-Range dominates due to its balance of quality and affordability.

The Price Range segment in the Ready-to-Wear market is pivotal in determining consumer purchasing decisions and overall market accessibility. The Mid-Range category emerges as the dominant sub-segment, offering a balanced combination of quality and affordability, making it appealing to a broad consumer base.

Mid-Range products provide consumers with stylish and durable clothing without the premium price tag associated with high-end brands. This makes mid-range options particularly attractive to value-conscious shoppers who seek both fashion and functionality.

The widespread availability of mid-range clothing through various retail channels, including online platforms and brick-and-mortar stores, further enhances its market presence. Brands in the mid-range segment often invest in maintaining a strong brand image and customer loyalty by offering consistent quality, trendy designs, and frequent collections that keep up with changing fashion trends.

Other price ranges include Low, Premium, and Luxury. The Low Price segment caters to budget-conscious consumers and those looking for basic, everyday wear. The affordability of low-priced clothing makes it a critical component of the market, especially in price-sensitive regions and among younger consumers.

Premium clothing appeals to consumers seeking higher quality, exclusive designs, and brand prestige. This sub-segment attracts those who are willing to pay more for superior materials and unique styles. The Luxury segment, with prices exceeding typical market ranges, represents high-end fashion houses offering unparalleled craftsmanship, unique designs, and superior materials.

Key Market Segments

By Product Type

- Top Wear

- Bottom Wear

- Dresses and Jumpsuits

- Outerwear

- Knitwear

- Activewear and Sportswear

- Others

By Material

- Cotton

- Wool

- Silk

- Denim

- Synthetic Fabrics

- Others

By End-User

- Men

- Women

- Children

By Price Range

- Low (< USD 50)

- Medium (USD 50 – 150)

- Premium (USD 150 – 500)

- Luxury (> USD 500)

Drivers

Evolving Consumer Preferences Drive Market Growth

Consumer preferences are shifting rapidly, driving significant growth in the Ready-to-Wear Market. The increasing demand for sustainable clothing is a key factor. Consumers, especially younger demographics, prefer garments made from organic or recycled fabrics. This trend pushes brands to adopt eco-friendly production methods, leading to innovative offerings in the market.

Fast fashion also supports market expansion by providing trendy and affordable apparel. This segment appeals to customers who prioritize frequent wardrobe updates without high costs. Additionally, gender-neutral fashion is gaining traction, catering to a more inclusive audience and expanding the potential customer base.

E-commerce platforms further amplify this growth. Online retailers provide convenience, extensive collections, and competitive pricing, allowing consumers to shop anytime and anywhere. Virtual try-on features and personalized recommendations enhance customer satisfaction, increasing sales.

Cultural shifts, such as the influence of celebrity and social media trends, also boost market dynamics. Ready-to-wear brands leverage these platforms for marketing, reaching millions of potential customers instantly.

Restraints

Supply Chain Challenges Restrain Market Growth

The Ready-to-Wear Market faces considerable restraints due to supply chain issues. Rising raw material costs, particularly for sustainable fabrics, significantly impact production expenses. These higher costs reduce profit margins and limit the affordability of eco-friendly clothing, which remains a priority for many consumers.

Supply chain disruptions, caused by geopolitical tensions and pandemics, pose another challenge. These disruptions lead to delays in production and distribution, affecting inventory levels and causing financial strain on retailers. Furthermore, the labor-intensive nature of garment manufacturing adds pressure, as increasing labor costs in production hubs drive up overall expenses.

Counterfeit products also undermine market growth by eroding consumer trust and diverting revenue from genuine brands. This issue affects both the reputation and profitability of established players. Additionally, overproduction leads to unsold inventory, creating waste and financial losses that discourage investors and brands.

Environmental concerns regarding waste and pollution in the manufacturing process further restrict growth. Companies must allocate resources to address these issues, diverting funds from other business areas.

Opportunity

Emerging Markets Provide Opportunities

Emerging markets present vast opportunities for the Ready-to-Wear Market, driven by rising disposable incomes and urbanization in regions like Asia-Pacific and Latin America. These regions are experiencing a growing middle class with a stronger purchasing power, increasing the demand for fashionable yet affordable apparel. The influence of Western fashion trends further fuels this demand.

Technological advancements in manufacturing also create growth opportunities. Automated production reduces costs and shortens production cycles, enabling brands to introduce collections faster. This aligns with the fast-changing preferences of consumers in emerging markets, who often seek the latest trends at competitive prices.

Collaborations with local designers in these regions offer another avenue for expansion. By incorporating cultural elements into designs, brands can cater to regional tastes while enhancing their appeal. Furthermore, the adoption of e-commerce in these areas expands access to ready-to-wear clothing, especially in previously underserved markets.

Sustainability is another growth driver in emerging markets. Consumers are increasingly drawn to brands that promote ethical and transparent practices, creating room for sustainable ready-to-wear products. These factors collectively position emerging markets as lucrative growth territories for global brands.

Challenges

Shifting Consumer Behavior Challenges Market Growth

Shifting consumer behavior presents challenges to the Ready-to-Wear Market, disrupting traditional business models. Increasing demand for transparency and ethical practices pressures brands to re-evaluate their supply chains. Companies that fail to meet these expectations risk losing customer loyalty, negatively impacting their market share.

The rise of personalized and customized clothing adds complexity to mass production. Consumers increasingly seek unique, tailor-made garments, forcing brands to invest in advanced technology and logistics.

Additionally, the second-hand and rental clothing markets are growing rapidly. These options appeal to eco-conscious consumers and those seeking affordability, reducing the demand for new ready-to-wear apparel. This trend intensifies competition and diverts revenue from established brands.

Economic instability also affects market growth. During financial downturns, consumers prioritize essential spending, limiting their investment in non-essential clothing. These challenges require ready-to-wear brands to adapt quickly to changing consumer behaviors while balancing costs and innovation.

Growth Factors

Sustainability and Innovation Are Key Growth Factors

Sustainability and innovation are driving significant growth in the Ready-to-Wear Market. The growing consumer preference for eco-friendly clothing encourages brands to invest in sustainable practices. From using organic cotton and recycled fabrics to adopting water-efficient and low-emission production techniques, these initiatives align with environmental values and appeal to a broader audience.

Innovative technologies, such as 3D printing and AI-driven design, also fuel market expansion. These advancements streamline production, reduce waste, and enable faster development of new collections.

Additionally, brands are adopting circular economy models, where clothes are designed for durability, recyclability, and reuse. This approach not only reduces waste but also resonates with eco-conscious consumers seeking long-lasting and responsible fashion choices.

The integration of smart clothing is another growth driver. Wearable technology embedded in garments, such as fitness trackers and temperature-regulating fabrics, captures consumer interest and expands the market’s reach into tech-savvy segments. Moreover, the rise of omni-channel retail strategies, combining physical stores with e-commerce platforms, enhances accessibility and consumer convenience.

Emerging Trends

Digital Transformation Is the Latest Trending Factor

Digital transformation is reshaping the Ready-to-Wear Market, driving significant growth through technological advancements. Artificial intelligence (AI) is revolutionizing retail by offering personalized recommendations and improving inventory management. This enhances the shopping experience and boosts sales.

Augmented reality (AR) features allow consumers to virtually try on garments, increasing confidence in online purchases. These innovations reduce return rates and build trust in e-commerce platforms. Furthermore, blockchain technology ensures transparency in supply chains, addressing consumer concerns about ethical and sustainable practices.

Social media platforms play a pivotal role in shaping fashion trends. Influencer marketing showcases ready-to-wear collections to global audiences, driving instant demand. Viral campaigns and collaborations with social media personalities amplify brand visibility and sales.

Additionally, the rise of digital-only fashion marks a futuristic trend. Virtual garments for avatars in gaming and social media platforms introduce a new revenue stream, especially among younger consumers. These advancements highlight the growing importance of digital transformation in the market’s evolution.

Regional Analysis

North America Dominates with Major Market Share

North America leads the Ready-to-Wear Market with a significant share, driven by a well-established retail sector, high disposable income, and strong consumer demand for fashion-forward apparel. The region’s dominance is fueled by a robust presence of global brands and a widespread culture of e-commerce adoption, which streamlines the accessibility of ready-to-wear products.

The region benefits from technological advancements in textile manufacturing, innovative marketing strategies, and a well-developed infrastructure for retail and logistics. Consumer preferences for premium and sustainable clothing further enhance market growth. Additionally, the influence of pop culture and fashion trends originating in North America helps sustain the demand for diverse ready-to-wear offerings.

North America’s influence is expected to grow, driven by evolving consumer expectations and continued innovation in sustainable fabrics and designs. The rise of AI-driven personalization in retail and increasing investments in omni-channel strategies will likely cement the region’s position as a market leader in the coming years.

Regional Mentions:

- Europe: Europe holds a significant share in the Ready-to-Wear Market, characterized by its heritage of high fashion and growing demand for sustainable clothing. The region’s focus on quality and craftsmanship drives consumer loyalty, while the expansion of luxury and mid-range apparel bolsters its market presence.

- Asia Pacific: Asia Pacific is a rapidly growing market, driven by rising disposable incomes, urbanization, and a younger population keen on global fashion trends. The strong manufacturing base in countries like China and India supports affordable ready-to-wear production, while e-commerce boosts accessibility.

- Middle East & Africa: The Middle East and Africa are emerging markets for ready-to-wear apparel, with increasing demand for modest fashion and premium clothing. Growth is driven by urbanization and a growing middle class, alongside investments in retail infrastructure.

- Latin America: Latin America is progressively adopting ready-to-wear trends, driven by growing urban populations and an interest in affordable, stylish clothing. Countries like Brazil and Mexico are key contributors, with a focus on casual and functional apparel suited to local climates and lifestyles.

Key Regions and Countries covered in the report

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Key Players Analysis

The Ready-to-Wear Market is driven by four dominant companies: Inditex, LVMH, Fast Retailing, and H&M Group. These global leaders maintain a strong presence through innovative strategies, broad product portfolios, and advanced retail networks. Their ability to adapt to consumer trends and expand into emerging markets solidifies their market dominance.

Inditex, known for Zara, excels in fast fashion with a highly efficient supply chain. The company’s quick response to changing trends and its global retail footprint make it a market leader. Similarly, LVMH commands a significant share by focusing on premium ready-to-wear collections. The luxury segment benefits from LVMH’s strong brand reputation and high consumer loyalty.

Fast Retailing, through Uniqlo, emphasizes functional and sustainable fashion. Its focus on basics and innovative fabric technology attracts a diverse customer base. Meanwhile, H&M Group offers affordable, trendy clothing and has expanded its sustainability efforts to meet rising consumer expectations.

These companies also leverage e-commerce and digital marketing to enhance customer engagement. Their strong presence in online and physical stores ensures market resilience. Together, they shape the Ready-to-Wear Market by setting benchmarks in quality, innovation, and accessibility, ensuring sustained growth and global influence.

Top Key Players in the Market

- Inditex (Zara)

- LVMH (Louis Vuitton Moët Hennessy)

- Fast Retailing (Uniqlo)

- H&M Group

- Gap Inc.

- Kering (Gucci, Saint Laurent)

- PVH Corp. (Calvin Klein, Tommy Hilfiger)

- Ralph Lauren Corporation

- VF Corporation (The North Face, Timberland)

- Prada Group

- Hermès International

- Burberry Group

- Chanel

- Dolce & Gabbana

- Armani Group

Recent Developments

- Moncler and Willow Smith: In November 2024, Moncler unveiled a ready-to-wear collection in collaboration with Willow Smith. The collection blends minimalism with utilitarian elements, offering versatile designs for urban and outdoor settings. Its monochromatic palette and innovative style reflect Smith’s personality and Moncler’s heritage.

- Richard Anderson: In May 2024, Richard Anderson expanded on Savile Row by launching a ready-to-wear store. The store introduced casual garments like dressing gowns and sweaters while maintaining Savile Row’s craftsmanship. This move highlights a strategic shift to modern fashion trends without losing traditional values.

- Valentino and Alessandro Michele: In September 2024, Alessandro Michele debuted as Valentino’s creative director at Paris Fashion Week. The collection featured a maximalist aesthetic, combining Gucci’s exuberance with Valentino’s ethereal legacy. Michele’s approach signals a transformative vision by reinterpreting the brand’s heritage with modern eclecticism.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2023) | USD 112.3 Billion |

| Forecast Revenue (2033) | USD 296.6 Billion |

| CAGR (2024-2033) | 10.2% |

| Base Year for Estimation | 2023 |

| Historic Period | 2019-2022 |

| Forecast Period | 2024-2033 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Product Type (Top Wear, Bottom Wear, Dresses and Jumpsuits, Outerwear, Knitwear, Activewear and Sportswear, Others), By Material (Cotton, Wool, Silk, Denim, Synthetic Fabrics, Others), By End-User (Men, Women, Children), By Price Range (Low (< USD 50), Medium (USD 50–150), Premium (USD 150–500), Luxury (> USD 500)) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA |

| Competitive Landscape | Inditex (Zara), LVMH (Louis Vuitton Moët Hennessy), Fast Retailing (Uniqlo), H&M Group, Gap Inc., Kering (Gucci, Saint Laurent), PVH Corp. (Calvin Klein, Tommy Hilfiger), Ralph Lauren Corporation, VF Corporation (The North Face, Timberland), Prada Group, Hermès International, Burberry Group, Chanel, Dolce & Gabbana, Armani Group |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |