Quick Navigation

Report Overview

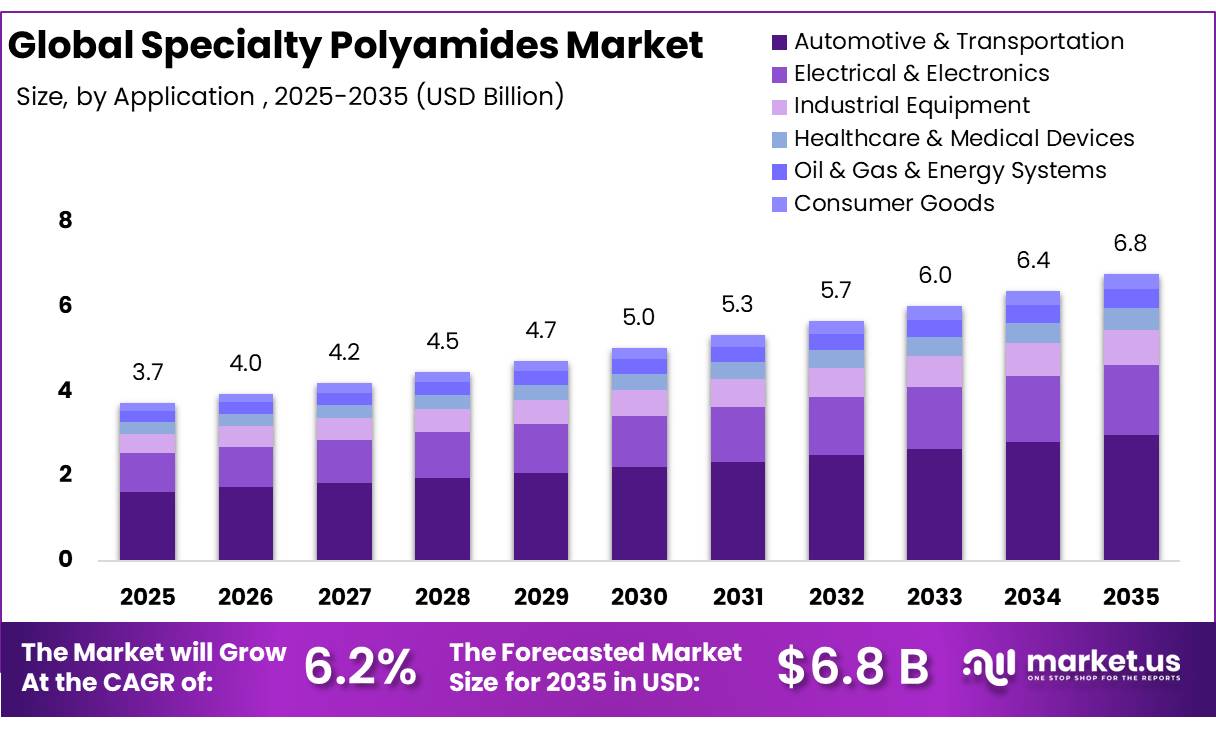

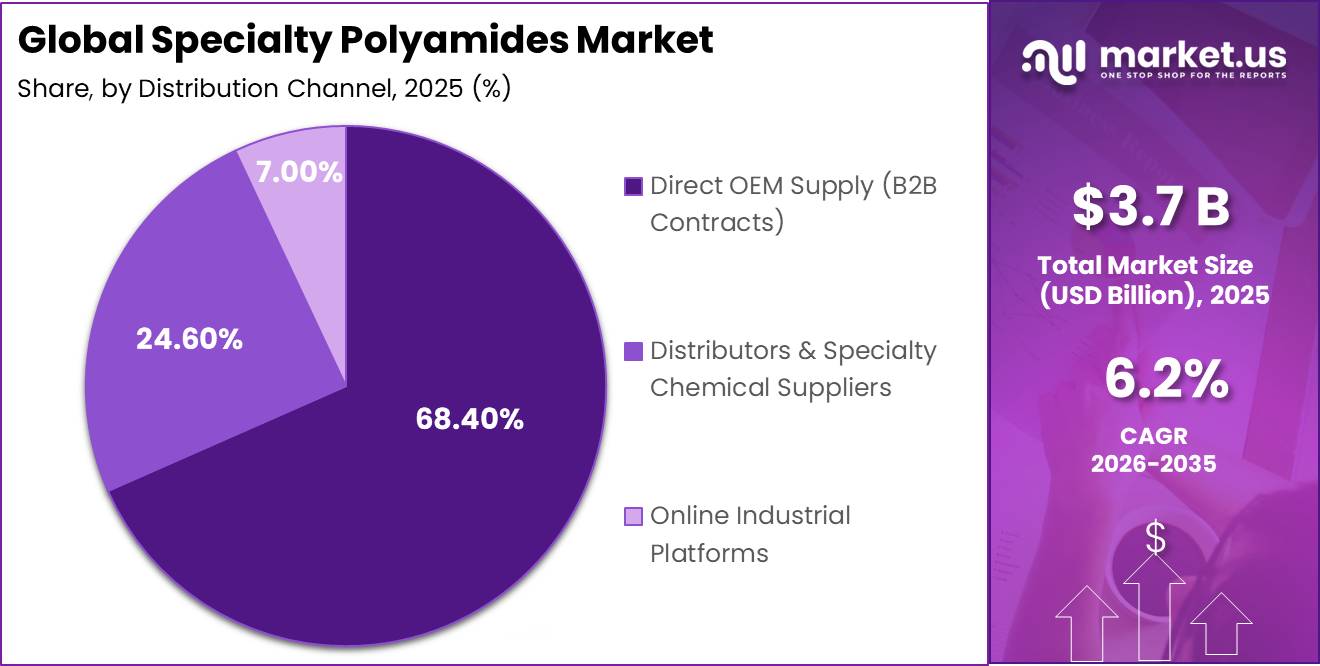

In 2025, the Global Specialty Polyamides Market was valued at US$3.7 billion, and between 2026 and 2035, this market is estimated to register a CAGR of 6.2%, reaching about US$6.8 billion by 2035.

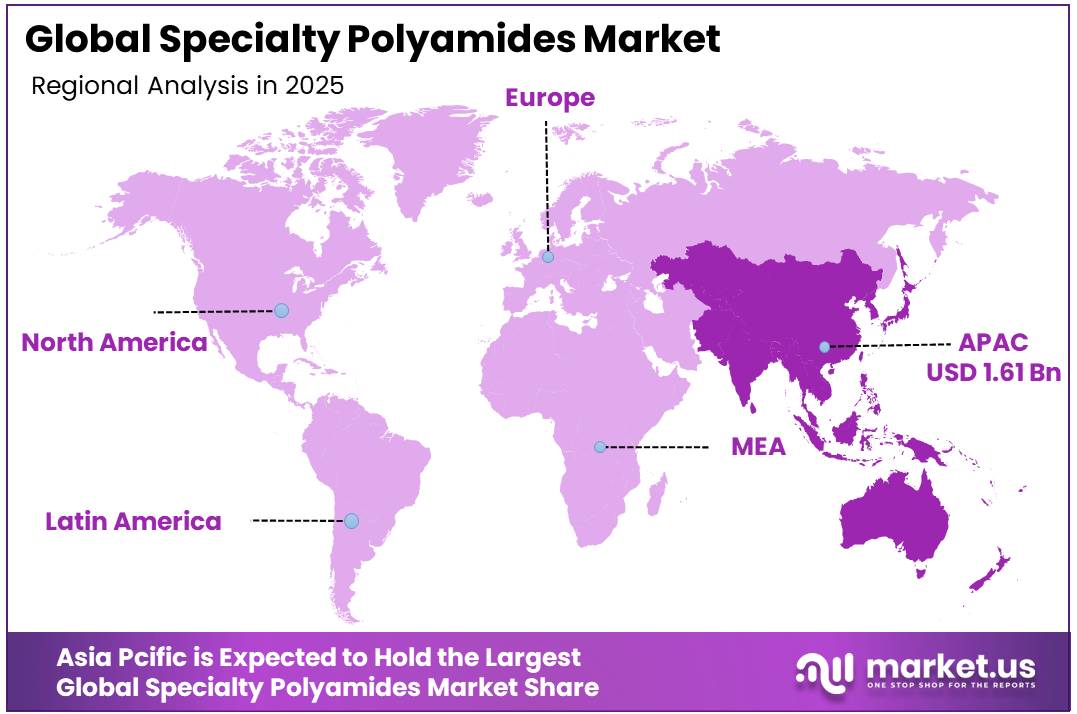

Asia Pacific held a dominant market position, capturing more than a 43.2% share, holding USD 1.61 billion in revenue.

Key Takeaways

- The global Specialty Polyamides Market was valued at US$3.7 billion in 2025.

- The global Specialty Polyamides Market is projected to grow at a CAGR of 6.2% and is estimated to reach US$6.8 billion by 2035.

- On the basis of product type, high-temperature polyamides dominated the market, constituting 47.2% of the total market share.

- Based on polyamide type by grade, PA12 led the specialty polyamides market, comprising 41.6% of the total market.

- Among the applications, automotive and transportation held a major share in the specialty polyamides market, accounting for 44.1% of the market share.

- Based on end user, automotive original equipment manufacturers dominated the market, with a substantial market share of around 39.8%.

- Based on form type, injection molding grades were the most prominent within the market, accounting for around 52.3% of the revenue.

- Among the functionalities, high heat resistance materials dominated the market, constituting 45.6% of the total market share.

- Based on processing type, injection molding led the specialty polyamides market, comprising 63.1% of the total market.

- Among the distribution channels, direct original equipment manufacturer supply through business-to-business contracts held the largest share, accounting for 68.4% of the market.

- In 2025, Asia-Pacific was the most dominant region in the specialty polyamides market, accounting for 43.2% of the total global market.

Specialty polyamides are high-performance engineering thermoplastics designed for demanding environments requiring heat stability, chemical resistance, dimensional control, low moisture uptake, and mechanical strength. They are used in automotive systems, electrical connectors, industrial components, medical devices, energy equipment, and precision molded parts.

- PlasticsEurope reported that global plastics production increased 1% in 2024 and 16.3% from 2018, while Europe’s production share declined from 22% in 2006 to 12% in 2024, affecting global resin producers, compounders, processors, and component suppliers.

Industrial demand is closely linked to vehicle production and the replacement of metal components with lighter polymers. The International Organization of Motor Vehicle Manufacturers reported that global vehicle output rose from 92.7 million units in 2024 to 96.4 million in 2025, an increase of 3.9%, while sales reached 99.8 million units. Specialty polyamides support under-hood parts, fuel systems, battery components, thermal-management assemblies, and structural applications requiring durability under elevated temperatures and exposure to aggressive fluids.

Electrical and electronics manufacturing provides another major growth platform. World Semiconductor Trade Statistics reported global semiconductor sales of USD 795.6 billion in 2025, up 26.2% year over year, with fourth-quarter revenue reaching USD 238.9 billion. Expanding data centers, artificial intelligence hardware, electrified vehicles, miniaturized connectors, and high-voltage systems increase the need for flame-resistant, dimensionally stable, and high-temperature polymer grades that can maintain performance during repeated electrical and thermal loading worldwide.

Government policy is creating opportunities in lightweighting, recycling, and renewable feedstocks. European Union rules require carbon dioxide emissions from new cars to fall 15% during 2025 to 2029, 55% during 2030 to 2034, and 100% from 2035. A provisional European agreement also requires 15% recycled plastic in new vehicle types within six years and 25% within ten years. European Commission research states that bio-based products could avoid 2.5 billion tonnes of carbon dioxide equivalent annually by 2030.

Specialty Polyamides Market Segmentation

Product Type Analysis

High-Temperature Polyamides Lead Product Demand with a 47.20% Share

In 2025, High-Temperature Polyamides (PA6T, PA9T, PA46, etc.) held a dominant market position, capturing more than a 47.20% share. In December 2025, these materials remained widely preferred because they retain strength, stiffness, and dimensional stability under high temperatures and continuous mechanical stress. Their resistance to fuels, oils, chemicals, and repeated thermal cycles supports use in automotive parts, electrical connectors, industrial equipment, and precision components. Manufacturers also select these grades for metal replacement, compact component design, and lightweight structures where standard polyamides may lose performance. Their molding behavior also helps producers maintain component quality across large-volume manufacturing operations and complex designs.

Long Chain Polyamides (PA11, PA12, PA610, PA612) are expected to be the fastest-growing product segment as demand rises for flexible, lightweight, and chemically resistant polymers. Their low moisture absorption, impact strength, and durability support applications in fuel lines, pneumatic tubes, cable protection, medical components, and consumer products. Growing interest in renewable material options also strengthens the position of PA11, while PA12 continues to gain use in demanding industrial and transportation systems.

Polyamide Type (By Grade) Analysis

PA12 Leads the Market with a 41.60% Share

In 2025, PA12 held a dominant market position, capturing more than a 41.60% share. In December 2025, the grade remained widely used because it combines low moisture absorption, strong chemical resistance, flexibility, and dependable dimensional stability. These properties support its use in automotive fuel lines, pneumatic tubing, electrical cable protection, medical components, industrial parts, and additive manufacturing materials. PA12 also performs well under repeated mechanical stress and changing temperatures, helping manufacturers produce lightweight components with long service lives. Its balanced processing behavior supports injection molding, extrusion, and powder-based production, which further strengthens its position across transportation, electronics, healthcare, and industrial applications.

PA11 is expected to be the fastest-growing grade as manufacturers increase their focus on renewable raw materials and durable engineering polymers. The material offers strong impact resistance, flexibility, low density, and resistance to fuels, oils, and chemicals. These features make it suitable for automotive tubing, electrical protection systems, sporting goods, medical products, and industrial components. Its bio-based origin also supports corporate sustainability goals and broader demand for lower-carbon material solutions globally.

Application Analysis

Automotive and Transportation Leads with a 44.10% Share

In 2025, Automotive & Transportation held a dominant market position, capturing more than a 44.10% share. In December 2025, specialty polyamides remained widely used in fuel lines, air brake tubes, cooling systems, under-the-hood components, cable protection, and lightweight structural parts. Their strong resistance to heat, fuels, oils, chemicals, and repeated mechanical stress supports reliable vehicle performance under demanding operating conditions. These materials also help manufacturers reduce component weight, improve design flexibility, and replace selected metal parts without weakening durability. Their suitability for injection molding and extrusion further supports high-volume production across passenger vehicles, commercial vehicles, and other transportation equipment.

Electrical & Electronics is expected to be the fastest-growing application as demand rises for compact, heat-resistant, and dimensionally stable materials. Specialty polyamides are increasingly selected for connectors, switches, circuit protection parts, sensor housings, cable accessories, and high-voltage components. Their electrical insulation, flame resistance, low moisture absorption, and ability to maintain shape under thermal stress make them suitable for advanced electronic systems, electric mobility platforms, industrial controls, and connected devices during extended service periods.

End User Analysis

Automotive OEMs Lead with a 39.80% Share

In 2025, Automotive OEMs held a dominant market position, capturing more than a 39.80% share. In December 2025, these manufacturers remained the largest users of specialty polyamides because the materials support lighter, stronger, and more durable vehicle components. They are widely selected for fuel lines, cooling systems, air intake parts, electrical housings, cable protection, and under-the-hood assemblies. Their resistance to heat, fuels, oils, chemicals, and repeated vibration helps original equipment manufacturers improve component reliability while reducing vehicle weight. Their compatibility with injection molding and extrusion also supports efficient production of complex parts across passenger and commercial vehicle platforms.

Electrical & Electronics Manufacturers are expected to be the fastest-growing end-user segment as demand increases for compact, heat-resistant, and electrically stable materials. Specialty polyamides are increasingly used in connectors, switches, sensor housings, circuit protection parts, cable accessories, and high-voltage systems. Their dimensional stability, insulation performance, flame resistance, and low moisture absorption make them suitable for advanced electronics, industrial controls, connected devices, and electric mobility applications requiring consistent performance throughout extended operating periods and demanding environments.

Form Type Analysis

Injection Molding Grades Lead with a 52.30% Share

In 2025, Injection Molding Grades held a dominant market position, capturing more than a 52.30% share. In December 2025, these grades remained widely preferred because they allow manufacturers to produce complex, precise, and lightweight components at high production volumes. Their strong flow behavior, dimensional stability, heat resistance, and compatibility with reinforced formulations support use in automotive parts, electrical connectors, medical devices, industrial housings, and consumer products. Injection molding also helps reduce material waste, improve repeatability, and shorten production cycles, making these grades suitable for applications that demand consistent quality and reliable performance.

Extrusion Grades, including tubes, pipes, and films, are expected to be the fastest-growing form type as demand rises for flexible, durable, and chemically resistant components. These grades support continuous production of fuel lines, pneumatic tubes, protective coverings, industrial hoses, medical tubing, and specialty films. Their low moisture absorption, smooth processing, and ability to maintain strength under pressure and temperature changes make them suitable for transportation, healthcare, electronics, and industrial systems requiring long service life and dependable performance in demanding environments.

Functionality Analysis

High Heat Resistance Materials Lead with a 45.60% Share

In 2025, High Heat Resistance Materials held a dominant market position, capturing more than a 45.60% share. In December 2025, these materials remained widely preferred because they retain strength, stiffness, and dimensional stability under elevated temperatures. Their resistance to thermal aging, chemicals, fuels, and repeated mechanical stress supports use in automotive parts, electrical connectors, industrial equipment, medical devices, and energy systems. Manufacturers also select these grades for compact components that must operate reliably near engines, batteries, electronic circuits, and heated machinery. Their suitability for precision molding further supports consistent quality across demanding production environments.

Lightweight Structural Materials are expected to be the fastest-growing functionality as industries seek lower component weight without reducing strength or durability. Specialty polyamides support metal replacement in housings, brackets, tubing, connectors, and structural assemblies. Their low density, impact resistance, design flexibility, and processing efficiency help manufacturers improve product performance while reducing material use. Demand is increasing across transportation, electronics, industrial equipment, and consumer goods where lighter components can support easier handling, efficient operation, and longer service life.

Processing Type Analysis

Injection Molding Leads with a 63.10% Share

In 2025, Injection Molding held a dominant market position, capturing more than a 63.10% share. In December 2025, the process remained widely used because it supports fast, repeatable production of complex specialty polyamide components with tight dimensions and consistent surface quality. It is suitable for automotive housings, electrical connectors, medical parts, industrial components, and consumer products that require heat resistance, chemical durability, and mechanical strength. Manufacturers also favor injection molding for its design flexibility, compatibility with reinforced grades, and ability to reduce finishing work during large production runs. These advantages strengthen its role across high-volume and precision manufacturing applications.

Extrusion is expected to be the fastest-growing processing segment as demand increases for continuous profiles, tubes, pipes, films, and protective coverings. The process supports steady material flow, uniform wall thickness, and efficient production of long components. Specialty polyamides processed through extrusion are used in fuel lines, pneumatic tubing, cable protection, medical tubing, and industrial hoses where flexibility, chemical resistance, and dependable performance are required under demanding operating conditions and repeated mechanical or thermal stress.

Distribution Channel Analysis

Direct OEM Supply Leads with a 68.40% Share

In 2025, Direct OEM Supply (B2B Contracts) held a dominant market position, capturing more than a 68.40% share. In December 2025, this channel remained preferred because it gives manufacturers direct access to consistent material quality, technical support, customized grades, and reliable delivery schedules. Automotive, electronics, healthcare, and industrial companies often purchase specialty polyamides through long-term agreements to secure approved formulations and maintain production continuity. Direct relationships also allow suppliers to work closely with original equipment manufacturers on testing, performance requirements, regulatory compliance, and product development. This approach strengthens supply security and supports large-volume procurement for demanding applications.

Distributors & Specialty Chemical Suppliers are expected to be the fastest-growing channel as smaller and medium-sized buyers seek wider product access and flexible order volumes. These suppliers help customers compare grades, source materials from multiple producers, and obtain technical guidance without managing direct contracts. Their regional warehouses, local sales networks, and faster order handling improve material availability for prototype development, maintenance needs, and short production runs across automotive, electronics, medical, and industrial applications across global markets.

Key Market Segments

Product Type

- High-Temperature Polyamides (PA6T, PA9T, PA46, etc.)

- Long Chain Polyamides (PA11, PA12, PA610, PA612)

- Polyphthalamides (PPA / MXD6-based)

- Bio-based Polyamides (PA11, renewable PA grades)

By Polyamide Type (By Grade)

- PA12

- PA11

- PA6/12 & Copolyamides

- PA6T / PA9T

By Application

- Automotive & Transportation

- Electrical & Electronics

- Industrial Equipment

- Healthcare & Medical Devices

- Oil & Gas & Energy Systems

- Consumer Goods

By End User

- Automotive OEMs

- Electrical & Electronics Manufacturers

- Industrial Manufacturing Companies

- Healthcare & Pharmaceutical Firms

By Form Type

- Injection Molding Grades

- Extrusion Grades (Tubes, Pipes, Films)

- Additive Manufacturing (3D Printing Powders/Filaments)

By Functionality

- High Heat Resistance Materials

- Lightweight Structural Materials

- Chemical & Fuel Resistant Polymers

By Processing Type

- Injection Molding

- Extrusion

- Blow Molding & Specialty Processing

By Distribution Channel

- Direct OEM Supply (B2B Contracts)

- Distributors & Specialty Chemical Suppliers

- Online Industrial Platforms

Driver Analysis

EV battery housings, connectors, and thermal-electrical parts mix-upgrade

The strongest 2026 demand impulse comes from electrification not just through vehicle count but through material intensity per vehicle, because specialty polyamides are increasingly specified in battery pack frames, busbar carriers, HV connectors, cooling line interfaces, and flame-retardant electrical modules where heat resistance, dielectric performance, and dimensional stability are worth more than commodity nylon pricing.

In Europe alone, battery-electric car registrations reached 1,880,370 units in 2025 and the BEV share rose to 17.4% from 13.6% in 2024, which indicates a 3.8 percentage-point mix shift in one year; even without assuming a fixed resin loading per vehicle, that scale change materially lifts demand for higher-value PA6T, PA9T, PA10T, PA11, PA12, and specialty compounds used around high-voltage architectures. This also improves gross-margin quality because the value capture shifts from pure tonnage to certified formulation packages, especially as Regulation (EU) 2023/1542 makes carbon-footprint declaration, conformity marking, and downstream traceability more material to battery-system sourcing decisions.

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| EV battery housings, connectors, and thermal-electrical parts mix-upgrade | +1.4% | EU core, China, North America, Korea-Japan | Medium term (2-4 years) |

| Grid modernization and transformer/electrical insulation demand | +1.1% | North America core, EU, India, Middle East spill-over | Medium term (2-4 years) |

| Automotive lightweighting and high-temperature metal replacement | +1.0% | EU, North America, China, ASEAN corridors | Short term (≤ 2 years) |

| Electronics miniaturization and high-heat connector demand | +0.9% | East Asia core, EU, North America | Short term (≤ 2 years) |

| Manufacturing recovery and industrial capex normalization | +0.8% | APAC broad base, North America, EU | Short term (≤ 2 years) |

| Circularity and compliance-led material redesign | +0.7% | EU core, UK spill-over, export-oriented Asian suppliers | Long term (≥ 4 years) |

Restraint Analysis

Feedstock volatility

Specialty polyamides depend on petrochemical and intermediate feedstocks whose pricing still moves with crude, naphtha, and broader energy cycles; the IEA notes oil markets remain sensitive even as demand growth moderates, which keeps resin economics exposed to margin swings and procurement re-pricing. In practice, a 8%-12% swing in upstream input costs can compress converter margins by 150-250 bps when customer price-reset windows lag by one quarter, especially for PA11, PA12, PA6T, and copolyamides where smaller production volumes reduce hedging efficiency and reduce the ability to absorb volatility through scale.

The growth hit is concentrated in APAC import corridors and EU manufacturers that rely on imported intermediates, because longer replenishment cycles, inventory builds, and spot-buy dependence raise working capital intensity by roughly 5%-8% of annual material spend, delaying CapEx and pushing customers toward lower-cost engineering polymers, which is why this restraint is a near-term -1.2% drag on baseline CAGR.

Restraint Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Feedstock volatility | -1.2% | Global, APAC, EU | Short term (≤ 2 years) |

| BPA/FCM compliance | -0.9% | EU core, UK-linked supply, export lines | Short term (≤ 2 years) |

| PFAS packaging curbs | -0.7% | EU, EEA, multinational converters | Medium term (2-4 years) |

| Tariff friction | -0.8% | US, EU trade lanes, China-linked flows | Short term (≤ 2 years) |

| Fragmented non-harmonized rules | -1.0% | EU peripheral markets, multi-country exporters | Medium term (2-4 years) |

| Recycled-input quality gaps | -0.6% | EU, NA, APAC industrial users | Long term (≥ 4 years) |

Opportunity Analysis

EV lightweighting polyamide platforms

The EV lightweighting opportunity for specialty polyamides represents incremental upside above current automotive demand because most OEM lightweighting programs still rely primarily on metals and generic engineering plastics, leaving high-performance polyamide platforms underpenetrated in critical structural, under-the-hood, and thermal-management parts. According to the U.S. Department of Energy, a 10% reduction in vehicle weight can improve fuel economy by roughly 6–8%, highlighting the economic pressure on EV and hybrid platforms to pursue aggressive lightweighting in parallel with battery cost reductions and range enhancement targets by 2030–2035.

If specialty polyamides capture even an additional 5–7% share in lightweight structural and semi-structural components in global EV and hybrid production assuming roughly 150–170 million EVs and hybrids cumulatively produced between 2026 and 2035 and polymer-intensive value of 150–250 USD per vehicle for advanced materials the incremental TAM for high-performance polyamide compounds could conservatively expand by 1.5–2.5 billion USD above current projections, producing 20–30% higher margins versus commodity plastics through improved heat resistance, creep performance, and metal-replacement capabilities.

Unit economics are attractive: for every 1 kg of high-performance polyamide replacing metal or conventional plastics in structures or thermal management, OEMs can unlock 0.5–1.0 kg equivalent weight reduction, and systems-level design integration (e.g., integrated brackets, housings, busbars) can reduce part count per assembly by 10–20% and assembly labor time by 5–10%, bringing down per-vehicle manufacturing cost by 40–80 USD while still allowing suppliers to sustain contribution margins of 18–25%.

This is an opportunity rather than a current driver because DOE-backed lightweight materials programs and national laboratories are still focusing largely on carbon fiber and metals; polyamide-centric platforms are not yet embedded as standard in major regulatory or procurement frameworks, meaning targeted co-development with OEMs and Tier-1s anchored in 10–15 large platform programs could add around 2.0 percentage points of CAGR upside over the 2026–2035 window if executed at scale.

Opportunity Impact Analysis

| Opportunity | (~) % Potential CAGR Upside | Geographic Relevance | Execution Window |

|---|---|---|---|

| EV lightweighting polyamide platforms | +2.0% | North America, EU, China, Japan | Medium term (2–4 years) |

| Bio-based specialty polyamides scale-up | +1.8% | EU, North America, Japan, Brazil | Medium term (2–4 years) |

| Advanced e-mobility and battery systems | +1.5% | China, EU, Korea, NAFTA | Short–Medium (≤ 3 years) |

| High-barrier packaging and circularity | +1.3% | EU, North America, APAC emerging | Medium–Long (3–6 years) |

| Industrial 3D printing and digital fabrication | +1.0% | North America, EU, Japan, ASEAN | Long term (≥ 4 years) |

| Specialty polyamides for hydrogen & new energy | +0.9% | EU, Middle East, China, Australia | Long term (≥ 4 years) |

Challenges Analysis

Escalating sustainability compliance load

Regulatory pressure on plastics and high‑performance polymers has intensified, with frameworks such as the EU’s chemicals and circular economy packages, extended producer responsibility (EPR) schemes, and national strategies to prevent plastic pollution in the US and other OECD markets driving a steady increase in compliance workload and capital allocation for specialty polyamide producers, causing an estimated 1.1 percentage point drag on achievable CAGR as firms divert resources from pure market expansion to regulatory navigation.

Requirements now frequently include cradle‑to‑grave lifecycle assessments for specialty polyamide grades, reporting on greenhouse gas emissions in Scopes 1–3, and demonstrable recycling or recovery pathways, pushing compliance teams from typical 5–10 FTEs to 15–25 FTEs in mid‑size firms, and adding 2–4% to SG&A costs; in parallel, regulatory-driven product redesign programs can require 10–20% reformulation of portfolios to reduce hazardous intermediates or improve end‑of‑life performance, each reformulation project consuming 6–12 months of lab work and pilot runs.

Environmental regulations targeting emissions of toxic air pollutants and hazardous substances at plastic and polymer facilities have imposed stricter monitoring, flare reduction and treatment standards, necessitating investments of USD 10–30 million per major complex to upgrade emission control and wastewater treatment, which, while essential to long‑term license to operate, temporarily reallocates 20–40% of annual capital budgets away from capacity growth.

Strategically, specialty polyamide producers must integrate sustainability-by-design principles targeting at least 20–30% recycled or bio‑based content for select grades by 2030, aligning with national plastic pollution targets, and building robust EPR and circularity partnerships with downstream OEMs, which collectively reduce regulatory risk but lock the challenge into a long‑term mitigation horizon due to the multi‑decade nature of policy convergence and infrastructure build‑out.

Challenges Impact Analysis

| Challenge | (~) % CAGR Friction Drag | Geographic Relevance | Mitigation Horizon |

|---|---|---|---|

| Volatile petro-feedstock chain | -1.3% | APAC export hubs, EU industry belts, North America | Medium term (2-4 years) |

| Tight high-performance talent pool | -0.8% | EU R&D clusters, Japan & South Korea, US Gulf Coast | Long term (≥ 4 years) |

| Escalating sustainability compliance load | -1.1% | EU regulatory hubs, North America core, OECD Asia | Long term (≥ 4 years) |

| Biobased precursor scale-up bottlenecks | -0.9% | EU bio-chem corridors, Brazil, India, ASEAN | Medium term (2-4 years) |

| Logistics and energy cost volatility | -1.0% | Global trade lanes, APAC logistics corridors | Short term (≤ 2 years) |

| End-use qualification cycle elongation | -0.7% | Global automotive & electronics OEMs | Medium term (2-4 years) |

Geopolitical Impact Analysis

Trade Tensions and Regional Supply Shifts Reshape the Specialty Polyamides Market

The Specialty Polyamides Market remains sensitive to geopolitical changes because production depends on petrochemical feedstocks, specialty monomers, additives, compounding operations, and international transportation networks. Political tensions between major manufacturing regions can affect raw-material availability, supplier contracts, lead times, and production costs. Manufacturers are therefore reducing dependence on single-country sourcing and building relationships with suppliers across several regions.

Energy price volatility also influences specialty polyamide production because polymerization and compounding require stable supplies of electricity, natural gas, and chemical intermediates. Conflicts, sanctions, and restrictions affecting oil and gas trade can raise operating expenses for resin producers. These pressures may be passed through the value chain to automotive, electronics, healthcare, and industrial customers through higher material prices or revised supply agreements.

Trade restrictions and export controls are encouraging producers to establish regional manufacturing and warehousing networks closer to major customers. Automotive and electronics companies increasingly prefer locally available materials to reduce transportation risk and protect production continuity. This trend creates opportunities for specialty polyamide suppliers to expand local compounding capacity, provide customized grades, and strengthen direct technical support for original equipment manufacturers.

Geopolitical uncertainty is also increasing interest in bio-based polyamides and alternative feedstocks. Companies seeking greater supply security are evaluating renewable raw materials that can reduce dependence on imported fossil-based inputs. Different chemical regulations across Europe, Asia-Pacific, and North America also increase testing, documentation, and compliance requirements.

Regional Analysis

Asia Pacific Held the Largest Share of the Global Battery Separator Market.

In 2025, Asia-Pacific held a dominant position in the Specialty Polyamides Market, capturing 43.20% of global revenue, valued at US$1.61 billion. Regional leadership was supported by large automotive, electronics, electrical equipment, and industrial manufacturing bases that consume PA12, PA11, high-temperature polyamides, and polyphthalamides.

The International Organization of Motor Vehicle Manufacturers reported in April 2026 that Asia-Pacific produced about 59.2 million vehicles in 2025, rising 7.6% and representing more than 61% of global output. World Semiconductor Trade Statistics reported in February 2026 that semiconductor sales in Asia-Pacific and other markets increased 45.4% during 2025, while China recorded 17.9% growth.

China’s National Bureau of Statistics also reported that new-energy vehicle production reached 16.524 million units in 2025, increasing 25.1%. These manufacturing trends support demand for heat-resistant connectors, fuel-system parts, tubing, sensor housings, battery components, and lightweight structural applications across major end-use industries, strengthening the region’s position in specialty polyamide consumption and processing.

Key Regions and Countries Covered

- North America

- The US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia & CIS

- Rest of Europe

- APAC

- China

- Japan

- South Korea

- India

- ASEAN

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

Specialty polyamide manufacturers focus on product specialization, application development, and dependable customer support to protect their market position. A major priority is the expansion of high-performance grade portfolios, including long-chain polyamides, polyphthalamides, reinforced compounds, and bio-based formulations developed for specific processing and durability requirements. Leading companies also invest in advanced compounding, additive systems, and testing capabilities to deliver consistent resin performance across complex applications.

Close cooperation with component designers and processors helps suppliers secure early-stage material approvals and maintain long-term commercial relationships. Producers further strengthen competitiveness through backward integration into monomers, regional technical centers, and flexible production lines that can handle customized formulations and smaller order volumes. Patent protection, regulatory documentation, quality certification, and reliable after-sales assistance remain important differentiators. Strategic partnerships with distributors, compounders, and original equipment manufacturers improve market access, while investments in recycling compatibility and renewable feedstocks support positioning in premium and sustainability-focused segments.

Market Key Players

- Arkema S.A.

- Evonik Industries AG

- BASF SE

- DSM Engineering Materials

- EMS-GRIVORY

- Solvay S.A.

- DuPont de Nemours, Inc.

- Ube Industries Ltd.

- Kuraray Co., Ltd.

- RadiciGroup

- Asahi Kasei Corporation

- Toray Industries Inc.

- Shandong Dongchen Engineering Plastics

- Ascend Performance Materials

- Kolon Industries Inc.

Key Development

- In January 2026, Arkema started operations at its new Rilsan Clear transparent polyamide production unit in Singapore. The US$20 million facility tripled the company’s global production capacity for transparent polyamides and strengthened regional supply for electronics, healthcare devices, industrial filtration, eyewear, and home appliances.

- In January 2026, Asahi Kasei developed a new per- and polyfluoroalkyl substances-free polyamide 66 material for demanding low-friction applications. The grade maintains stable performance under high-load and high-temperature conditions and is intended for gears, chain guides, and other sliding components.

- In February 2026, Toray Industries developed spherical polyamide 12 particles for powder-based three-dimensional printing. The material was designed to provide improved surface quality and high impact strength in finished printed components.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | US$3.7 Bn |

| Forecast Revenue (2035) | US$6.8 Bn |

| CAGR (2026-2035) | 6.2% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Product Type (High-Temperature Polyamides, Long Chain Polyamides, Polyphthalamides, and Bio-based Polyamides), By Polyamide Type (By Grade) (PA12, PA11, PA6/12 and Copolyamides, and PA6T/PA9T), By Application (Automotive and Transportation, Electrical and Electronics, Industrial Equipment, Healthcare and Medical Devices, Oil and Gas and Energy Systems, and Consumer Goods), By End User (Automotive OEMs, Electrical and Electronics Manufacturers, Industrial Manufacturing Companies, and Healthcare and Pharmaceutical Firms), By Form Type (Injection Molding Grades, Extrusion Grades, and Additive Manufacturing), By Functionality (High Heat Resistance Materials, Lightweight Structural Materials, and Chemical and Fuel Resistant Polymers), By Processing Type (Injection Molding, Extrusion, and Blow Molding and Specialty Processing), By Distribution Channel (Direct OEM Supply, Distributors and Specialty Chemical Suppliers, and Online Industrial Platforms). |

| Regional Analysis | North America – The US & Canada; Europe – Germany, France, The UK, Spain, Italy, Russia & CIS, Rest of Europe; APAC– China, Japan, South Korea, India, ASEAN & Rest of APAC; Latin America– Brazil, Mexico & Rest of Latin America; Middle East & Africa– GCC, South Africa, & Rest of MEA |

| Competitive Landscape | Arkema S.A., Evonik Industries AG, BASF SE, DSM Engineering Materials, EMS-GRIVORY, Solvay S.A., DuPont de Nemours, Inc., Ube Industries Ltd., Kuraray Co., Ltd., RadiciGroup, Asahi Kasei Corporation, Toray Industries Inc., Shandong Dongchen Engineering Plastics, Ascend Performance Materials, and Kolon Industries Inc. |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited Users and Printable PDF) |