Quick Navigation

Report Overview

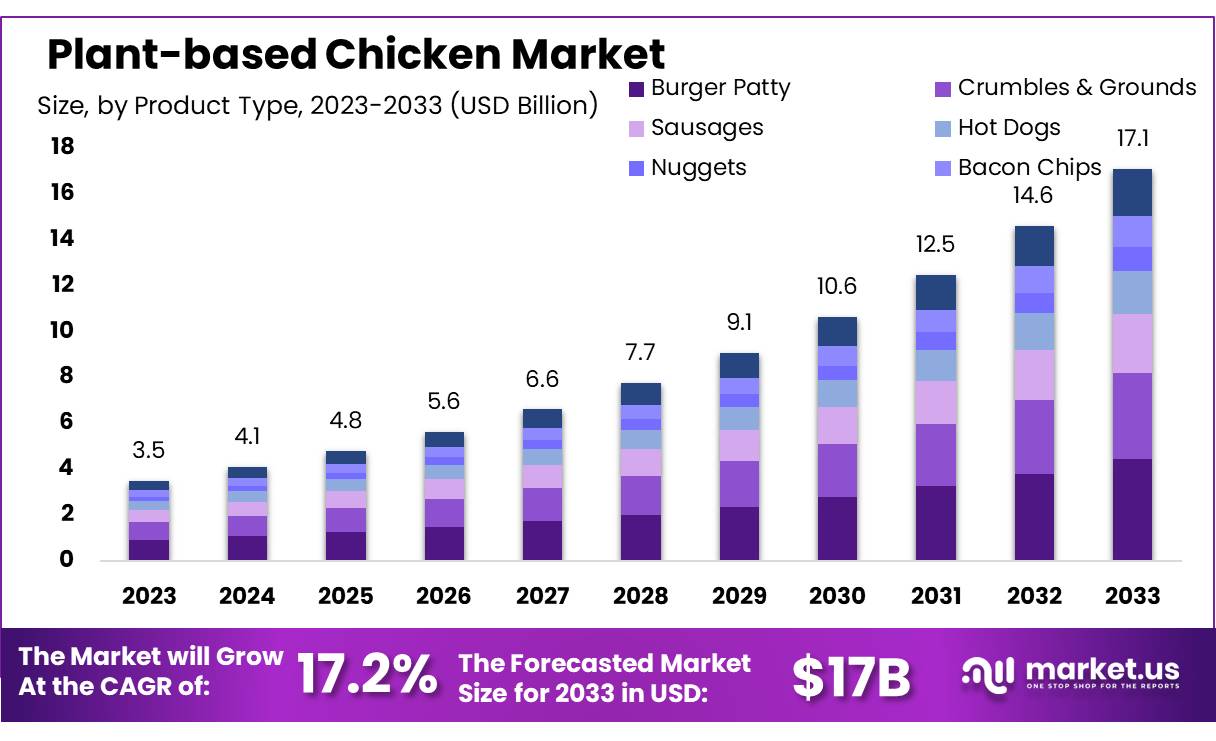

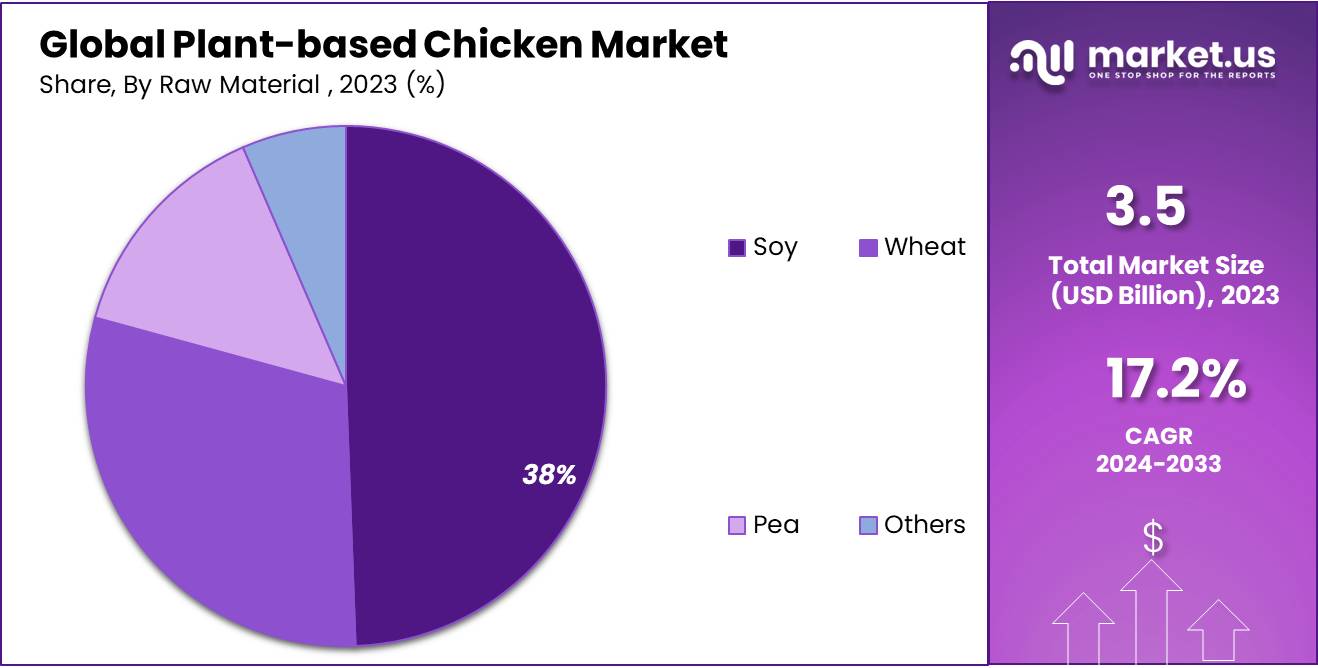

The Global Plant-based Chicken Market size is expected to be worth around USD 17.1 Bn by 2033, from USD 3.5 Bn in 2023, growing at a CAGR of 17.2% during the forecast period from 2024 to 2033.

Plant-based chicken is a type of meat substitute designed to replicate the taste, texture, and appearance of traditional chicken using plant-derived ingredients. These products are typically made from protein-rich plants like soy, peas, and wheat, often combined through advanced food processing techniques to mimic the fibers and chewiness of real chicken.

Plant-based chicken has gained significant popularity among individuals following vegetarian, vegan, and flexitarian diets, as well as those looking to reduce their consumption of animal products for health, environmental, or ethical reasons.

The market for plant-based meat, including plant-based chicken, is experiencing strong growth. According to the Good Food Institute (GFI), plant-based meat sales in the U.S. grew by 27% between 2020 and 2021. Within this broader category, plant-based chicken products specifically saw a remarkable 33% increase in sales.

This surge in demand is largely driven by the food service industry, where restaurants, fast-food chains, and quick-service restaurants (QSRs) are increasingly offering plant-based options to cater to consumer preferences. Major food chains, such as KFC, Burger King, and McDonald’s, have expanded their plant-based menu offerings, signaling a broader acceptance of plant-based substitutes in mainstream foodservice.

Governments in various regions have also recognized the role of plant-based products in promoting sustainability and reducing environmental impact. In the European Union, the European Commission has set ambitious goals to reduce the environmental footprint of food production, with a target to cut emissions by 50% by 2030.

Several countries, including the U.K., have introduced policies to encourage reduced meat consumption and promote plant-based alternatives. Some governments offer tax credits, grants, and other incentives to plant-based food producers, further boosting innovation in the sector.

Internationally, the demand for plant-based chicken is rising, especially in emerging markets. The U.S. is a major exporter of plant-based meat products, with exports reaching approximately $1.5 billion in 2022, according to the U.S. Department of Agriculture (USDA).

Countries in Asia, particularly China and Southeast Asia, are becoming key markets for plant-based products, driven by the growing popularity of plant-based diets and local demand for meat substitutes. The expansion into these regions presents significant growth opportunities for the plant-based chicken market globally.

Key Takeaways

- Plant-based Chicken Market size is expected to be worth around USD 17.1 Bn by 2033, from USD 3.5 Bn in 2023, growing at a CAGR of 17.2%.

- Burger Patty held a dominant market position, capturing more than a 26.4% share.

- Soy-based Protein held a dominant market position, capturing more than a 38.1% share.

- Soy held a dominant market position, capturing more than a 45.1% share.

- Refrigerated Plant-based Meat held a dominant market position, capturing more than a 49.1% share.

- Hypermarkets/Supermarkets held a dominant market position, capturing more than a 46.3% share.

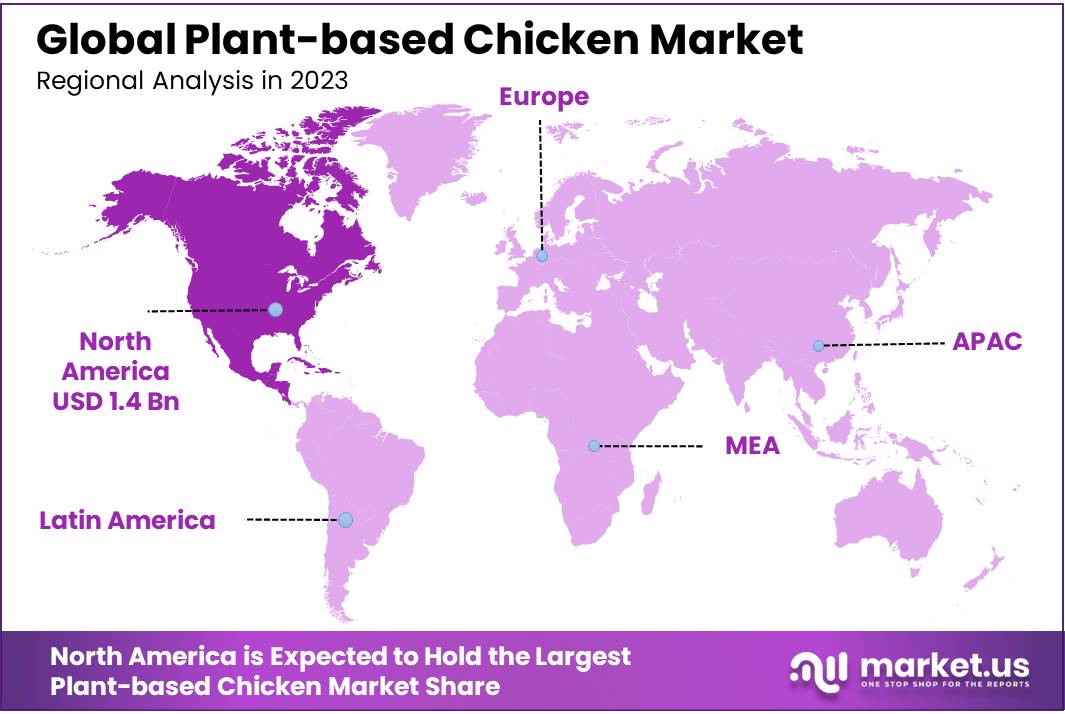

- North American region dominated the plant-based chicken market in 2023, capturing a significant share of 43.3%, with a market value of approximately USD 1.4 billion.

By Product Type

In 2023, Burger Patty held a dominant market position, capturing more than a 26.4% share. This segment benefits from increasing demand for plant-based alternatives in fast food and quick-service restaurants. Burger patties offer a familiar, convenient option for consumers transitioning to plant-based diets, driving their popularity in both retail and foodservice sectors.

Crumbles and Grounds followed closely, accounting for a significant portion of the market. These products are highly versatile, used in a variety of dishes like tacos, pasta, and stir-fries. They are gaining traction due to their flexibility and ease of use in home cooking, making them a favorite choice among plant-based consumers.

The Sausages segment has seen notable growth, driven by the increasing demand for meat-free breakfast and snack options. Plant-based sausages offer a familiar taste and texture, attracting consumers looking to reduce their meat intake without compromising on flavor. The market for plant-based sausages is expanding rapidly, especially in regions with high vegetarian and vegan populations.

Hot Dogs also represent a significant part of the plant-based chicken market. With a growing number of consumers seeking plant-based alternatives for traditional BBQ and sporting events, this segment continues to experience steady growth. Hot dog sales are increasingly driven by the shift toward healthier, more sustainable eating habits.

Plant-based Chicken Nuggets are a popular choice, particularly among younger consumers and families. In 2023, they accounted for a substantial share of the market. Their taste, texture, and convenience make them a preferred option for both home cooking and fast-food chains. As more brands introduce innovative flavors and coatings, the demand for nuggets continues to rise.

Bacon Chips, though a smaller segment compared to others, are seeing a rise in popularity. These plant-based products appeal to consumers craving the smoky, savory flavor of bacon without the animal-based ingredients. As plant-based snack options grow in demand, bacon chips are carving out their niche in the market.

By Source

In 2023, Soy-based Protein held a dominant market position, capturing more than a 38.1% share. Soy protein is widely used in plant-based chicken products due to its strong nutritional profile and ability to mimic the texture of meat. It remains the preferred choice among manufacturers for its affordability and established supply chain.

Wheat-based Protein, often found in seitan, is another key player in the plant-based chicken market. It holds a significant market share due to its chewy texture, which closely resembles meat. Wheat-based protein is popular for its versatility and is commonly used in a range of plant-based meat alternatives.

Pea-based Protein has gained rapid traction in recent years, capturing a growing share of the market. Known for its high protein content and neutral taste, pea protein is a key ingredient in many plant-based chicken products. Its use is expected to expand further as consumer demand for allergen-free and sustainable ingredients rises.

Canola-based Protein is a smaller but emerging source in the plant-based chicken market. It is valued for its high-quality amino acid profile and its neutral taste, making it suitable for a variety of plant-based meat products. As consumers become more aware of sustainable sources, canola protein is expected to grow in popularity.

Fava Bean-based Protein is a newer addition to the market, but it has gained attention for its potential health benefits and sustainability. Fava beans are rich in protein and fiber, and their use in plant-based chicken products is expected to rise as consumers look for alternative, nutrient-dense sources of protein.

Potato-based Protein is used in select plant-based chicken products, especially in regions where potatoes are a key agricultural product. While still a niche segment, its popularity is growing due to its natural, clean label appeal. Potato protein is seen as an excellent source of high-quality, digestible protein.

Rice-based Protein is becoming increasingly popular, especially for those with soy or gluten sensitivities. It offers a hypoallergenic alternative and is valued for its mild flavor and digestibility. As consumer preferences shift toward allergen-free products, rice-based protein is expected to gain a larger market share.

Lentil-based Protein is a rising star in the plant-based chicken market. Lentils are a sustainable and nutrient-dense source of protein, making them a favorite for health-conscious consumers. The segment is growing as more manufacturers seek to diversify their protein sources and appeal to eco-conscious buyers.

Flax-based Protein is gaining popularity due to its rich omega-3 fatty acids and fiber content. While its market share remains smaller compared to other sources, flax protein is valued for its health benefits and its potential to appeal to consumers looking for functional, plant-based ingredients in their food.

Chia-based Protein is a niche segment but is growing due to the increasing popularity of chia seeds as a superfood. Known for its omega-3 content and fiber, chia protein is appealing to health-focused consumers. It is mainly used in small quantities as part of blended protein formulations in plant-based chicken products.

Corn-based Prottent. Though it holds a smaller market share, it is gaining traction in markets where corn is an abundant crop. The demand for corn-based protein is expected to grow as more sustainable and locally sourced ingredients are prioritized.

By Raw material

In 2023, Soy held a dominant market position, capturing more than a 45.1% share. Soy is the most commonly used raw material in plant-based chicken products due to its high protein content and ability to replicate the texture of meat. It remains a preferred choice for manufacturers due to its cost-effectiveness and established supply chain.

Wheat is another key raw material in the plant-based chicken market, particularly in the form of seitan. This raw material is known for its firm, meat-like texture, which is highly valued in the production of plant-based meat alternatives. Wheat-based products are popular for their versatility and ability to be used in a variety of plant-based chicken offerings.

Pea protein is gaining significant ground, driven by its allergen-free nature and high nutritional value. This raw material is used in a growing number of plant-based chicken products, especially as consumers increasingly seek alternatives to soy and wheat. Pea protein’s neutral taste and strong protein profile make it an attractive option for plant-based food manufacturers.

By Storage

In 2023, Refrigerated Plant-based Meat held a dominant market position, capturing more than a 49.1% share. This segment is driven by the increasing demand for fresh, ready-to-cook plant-based products. Refrigerated plant-based chicken is popular in grocery stores and supermarkets, offering consumers the convenience of fresh alternatives with a short shelf life. Its position as a fresh product category helps maintain its leading share in the market.

Frozen Plant-based Meat represents a significant portion of the market, catering to consumers seeking longer shelf life and bulk purchase options. Frozen plant-based chicken products are widely available and often sold in larger quantities, making them ideal for families and restaurants. This segment benefits from the convenience of storage and transportation, as well as the growing demand for frozen meat substitutes.

Shelf-stable Plant-based Meat is a smaller but growing segment in the market. These products, which do not require refrigeration or freezing, appeal to consumers who prioritize convenience and long shelf life. They are particularly popular in regions with limited access to refrigerated storage or for consumers who want to stock up on plant-based options for extended periods. While the segment is still emerging, its potential for growth is strong, especially in the online retail and emergency food markets.

By Distribution Channel

In 2023, Hypermarkets/Supermarkets held a dominant market position, capturing more than a 46.3% share. These large retail outlets are the primary distribution channel for plant-based chicken products, offering a wide variety of options to meet growing consumer demand.

Supermarkets and hypermarkets attract a broad range of customers, making them key locations for plant-based brands to reach mainstream consumers. The convenience of one-stop shopping and the availability of fresh and frozen plant-based products contribute to the continued dominance of this channel.

Convenience Stores have a smaller but steadily growing share in the plant-based chicken market. These stores cater to consumers seeking quick and easy meals, making them an ideal location for ready-to-eat or heat-and-eat plant-based chicken products. The convenience factor, combined with an increasing number of plant-based options, is driving growth in this segment, especially in urban areas where consumers value quick access to plant-based foods.

Specialty Food Stores, including organic and health-focused retailers, are an important channel for plant-based chicken products. Although this segment holds a smaller share compared to hypermarkets and supermarkets, it is growing rapidly as health-conscious and environmentally aware consumers seek higher-quality, niche products. These stores often carry premium, locally-sourced, or specialty plant-based chicken options, appealing to a specific demographic interested in sustainable and ethical food choices.

Online Retail is experiencing significant growth in the plant-based chicken market, particularly driven by the rise of e-commerce and direct-to-consumer sales. With the convenience of home delivery, more consumers are choosing to purchase plant-based chicken products online. The ease of shopping and the growing availability of plant-based options on major platforms like Amazon, as well as brand-specific websites, make online retail a vital and expanding channel for plant-based food sales.

Key Market Segments

By Product Type

- Burger Patty

- Crumbles & Grounds

- Sausages

- Hot Dogs

- Nuggets

- Bacon Chips

- Others

By Source

- Soy-based Protein

- Wheat-based Protein

- Pea-based Protein

- Canola-based Protein

- Fava Bean-based Protein

- Potato-based Protein

- Rice-based Protein

- Lentin-based Protein

- Flax-based Protein

- Chia-based Protein

- Com-based Protein

By Raw material

- Soy

- Wheat

- Pea

- Others

By Storage

- Refrigerated Plant-based Meat

- Frozen Plant-based Meat

- Shelf-stable Plant-based Meat

By Distribution Channel

- Hypermarkets/Supermarkets

- Convenience Stores

- Specialty Food Stores

- Online Retail

- Others

Drivers

Growing Consumer Demand for Sustainable and Healthier Food Options

The increasing awareness of the environmental impact of animal agriculture is one of the key drivers for the rise in plant-based chicken consumption. A 2021 study by the Food and Agriculture Organization (FAO) of the United Nations found that livestock production accounts for around 14.5% of global greenhouse gas emissions, which is more than the entire transportation sector combined.

As consumers become more concerned about sustainability and the environmental footprint of their diets, plant-based alternatives are increasingly seen as a healthier and more eco-friendly choice.

According to a report by The Good Food Institute (GFI), plant-based meat sales in the U.S. alone grew by 27% in 2020, surpassing $1 billion in total sales, driven largely by consumers shifting towards plant-based diets to reduce their environmental impact.

Moreover, a 2020 survey by Nielsen found that 39% of consumers said they were actively trying to reduce their consumption of animal-based products for environmental reasons. The demand for plant-based products has also been boosted by the younger, more eco-conscious generations, with Mintel reporting that 44% of Millennials are more likely to choose plant-based foods than older generations.

Government Support and Policy Initiatives Promoting Plant-Based Alternatives

Government initiatives and policy support are also playing a significant role in driving the growth of the plant-based chicken market. Many governments around the world have recognized the environmental, health, and sustainability benefits of plant-based products and are taking action to encourage their production and consumption.

For instance, the European Union has been actively promoting plant-based food products as part of its Green Deal. The Farm to Fork Strategy released by the European Commission in 2020 aims to make food systems fair, healthy, and environmentally-friendly. One of the goals is to reduce the EU’s consumption of animal-based products by promoting alternatives such as plant-based proteins.

In the U.S., federal policies are beginning to support plant-based food innovation through grants and subsidies. In 2021, the U.S. Department of Agriculture (USDA) announced it would support the development of plant-based proteins and meat alternatives, as part of a broader effort to diversify food sources and reduce the carbon footprint of the food industry.

Additionally, several state-level initiatives, such as in California, have incentivized plant-based product development through tax credits and subsidies. These policies not only make plant-based chicken products more affordable but also create a more favorable environment for their growth.

Rising Health Awareness and Dietary Shifts Toward Plant-based Foods

Health considerations continue to be a significant driver behind the adoption of plant-based chicken. Many consumers are moving away from traditional meat products due to concerns about the link between red meat consumption and health issues such as heart disease, obesity, and cancer. A study by the American Institute for Cancer Research found that consumption of red and processed meats is linked to an increased risk of colorectal cancer, a key factor motivating consumers to explore healthier alternatives like plant-based chicken.

The rising popularity of plant-based diets is also influenced by the increasing availability of nutritionally fortified plant-based products. Manufacturers are developing plant-based chicken products with added vitamins, minerals, and proteins to ensure that they meet the dietary needs of consumers. According to the World Health Organization (WHO), plant-based diets that are well-planned are often more nutrient-dense, lower in saturated fats, and provide beneficial compounds such as fiber and antioxidants.

Restraints

High Price of Plant-based Chicken Products

One of the primary restraining factors for the growth of the plant-based chicken market is the high price compared to traditional meat products. Plant-based meats generally cost more to produce due to the need for specialized ingredients, processing technologies, and smaller production scales.

According to a 2021 report by the European Commission, plant-based products are still approximately 20% to 40% more expensive than their animal-based counterparts in most European markets. In the United States, the price of plant-based chicken products can be up to 50% higher than traditional poultry, according to data from the U.S. Department of Agriculture (USDA). This price disparity presents a significant barrier, particularly in emerging markets or price-sensitive consumer segments.

While prices for plant-based products have been decreasing due to technological advances and economies of scale, the cost remains a concern for mainstream adoption.

For instance, in the U.S., plant-based chicken alternatives like those from brands such as Beyond Meat or Impossible Foods typically retail for $6 to $8 per pound, while conventional chicken prices are closer to $2 to $3 per pound for frozen products. Despite some efforts to reduce costs, the higher price point continues to limit the accessibility of these products to a wider audience, especially in lower-income regions.

Limited Availability and Accessibility

Another challenge hindering the growth of the plant-based chicken market is the limited availability and accessibility of plant-based chicken products in certain regions and retail outlets. While major cities and developed markets have seen an increase in the availability of plant-based products, smaller cities and rural areas often have limited access.

A 2020 study by Nielsen found that 63% of U.S. consumers were still unable to find plant-based alternatives in their local grocery stores, particularly in areas outside of metropolitan centers. Similarly, in countries like India and parts of Southeast Asia, where traditional meat consumption is higher, plant-based chicken options are not as widely available.

The distribution network for plant-based meats still faces challenges related to shelf space in supermarkets, especially in regions where traditional meat consumption is culturally ingrained. According to The Good Food Institute (GFI), despite the rapid growth in plant-based product categories, plant-based meat still accounts for only 2.7% of the total U.S. meat market by volume. This lack of availability in mainstream grocery stores and limited product offerings can discourage consumers from trying plant-based alternatives.

Additionally, not all foodservice outlets are offering plant-based chicken alternatives, with many still slow to introduce plant-based options on their menus. This lack of availability across both retail and foodservice channels restricts the overall market potential for plant-based chicken products.

Consumer Perception and Familiarity with Plant-based Chicken

Consumer perception remains one of the major barriers to the widespread adoption of plant-based chicken. Despite growing awareness of the environmental and health benefits of plant-based diets, many consumers remain skeptical about the taste, texture, and nutritional value of plant-based chicken products.

According to a 2021 survey by The Vegetarian Resource Group, 51% of U.S. consumers expressed concerns about the taste and texture of plant-based meat alternatives, with some questioning whether plant-based products could truly replicate the experience of eating animal-based chicken.

While the quality of plant-based chicken has significantly improved in recent years, with new innovations in texture and flavor, the perception that these products are “less satisfying” or “artificial” continues to challenge growth.

A study from the University of California, Berkeley found that only 20% of people who tried plant-based chicken for the first time were completely satisfied with the taste. The remaining 80% of participants noted that the taste and texture did not fully mimic their expectations of real chicken. This reluctance to embrace plant-based alternatives, combined with long-standing consumer habits surrounding traditional meat consumption, is holding back further market penetration.

Additionally, some consumers remain unaware of the health benefits of plant-based chicken, with many still associating plant-based foods with processed or “unnatural” ingredients. This perception, if not addressed, may hinder the adoption of plant-based alternatives.

Supply Chain and Ingredient Sourcing Issues

The plant-based chicken market also faces challenges related to the sourcing and supply chain of key ingredients, which can affect product consistency, availability, and pricing. Key ingredients like pea protein, soy, and wheat are vital for the production of plant-based meat, and the growing demand for these ingredients is creating supply chain constraints.

According to FAO, the global demand for plant-based proteins is expected to outpace supply, leading to potential shortages of key ingredients. As the production of plant-based chicken grows, the pressure on the agricultural industry to meet demand for high-quality plant-based protein ingredients intensifies.

Opportunity

Expansion of Product Offerings and Innovation in Plant-based Chicken

One of the most significant growth opportunities for the plant-based chicken market lies in the ongoing innovation and diversification of plant-based products. As consumers continue to seek more variety in plant-based foods, manufacturers are increasingly developing new types of plant-based chicken products to meet different culinary preferences.

For example, Beyond Meat and Impossible Foods are expanding their product lines beyond simple patties and nuggets to include plant-based chicken tenders, fillets, and other forms of chicken meat that better mimic the texture, flavor, and appearance of traditional chicken.

According to The Good Food Institute (GFI), the U.S. plant-based meat market is expected to reach $35 billion by 2027, driven by new product innovations and greater consumer interest in plant-based diets.

Additionally, new formulations are being developed using alternative protein sources like fava beans, chickpeas, and lentils, as these ingredients not only offer variety but also appeal to different dietary preferences such as gluten-free or soy-free diets.

According to the FAO, there is a growing global interest in alternative proteins, with demand for plant-based proteins expected to increase by 7% annually over the next decade. As companies continue to innovate with new plant-based chicken formats and flavors, the market will see increased consumer engagement and expanded options, boosting overall growth.

Rising Demand in Emerging Markets

Emerging markets represent a significant growth opportunity for the plant-based chicken sector, particularly in regions like Asia-Pacific and Latin America. The shift toward plant-based diets is still in its early stages in many developing countries, but rapid urbanization, rising middle-class populations, and increased awareness of the environmental and health benefits of plant-based foods are driving growth in these regions.

For example, in China, the plant-based food market has seen a rapid increase, with The Good Food Institute noting that plant-based meat consumption grew by 21% in 2020 alone. With over 1.4 billion people in China, the potential market for plant-based alternatives is immense. Similarly, India, with its large vegetarian population, offers a unique opportunity for plant-based chicken products tailored to local tastes and preferences.

The FAO predicts that the plant-based food market in the Asia-Pacific region will grow at a CAGR (Compound Annual Growth Rate) of 8.6% from 2022 to 2027, as consumers in these markets become more aware of the environmental impact of traditional meat consumption and are increasingly willing to explore plant-based alternatives

Governments in these regions are also becoming more supportive of sustainable food systems, offering subsidies and policy incentives for the production of plant-based products. As plant-based chicken products are introduced and marketed in culturally relevant ways, their appeal in these emerging markets is expected to grow, presenting a major opportunity for manufacturers to scale their businesses internationally.

Increased Adoption in Foodservice and Quick-Service Restaurants (QSRs)

The foodservice sector, especially quick-service restaurants (QSRs), presents a significant growth opportunity for plant-based chicken. The demand for plant-based menu options is rapidly increasing, with major global QSR chains like McDonald’s, KFC, Burger King, and Subway introducing plant-based chicken products to cater to the growing demand for meat alternatives.

In 2020, McDonald’s launched its first-ever plant-based burger in partnership with Beyond Meat, and KFC introduced plant-based chicken nuggets in select markets. The expansion of plant-based offerings in fast food and casual dining restaurants is a key trend that could drive the growth of the plant-based chicken market.

Trends

Increasing Popularity of Plant-based Chicken in Fast Food and Quick-Service Restaurants (QSRs)

One of the most notable trends in the plant-based chicken market is the growing popularity of plant-based options in fast food and quick-service restaurants (QSRs). Major global QSR chains, such as KFC, McDonald’s, and Burger King, have recognized the rising consumer demand for plant-based alternatives and have started adding plant-based chicken products to their menus.

According to a report from The Good Food Institute (GFI), plant-based meat sales in foodservice grew by 43% in 2020, reflecting the growing shift toward plant-based options in the restaurant industry.

In particular, KFC launched plant-based chicken in select markets, starting in 2020, with overwhelming success in countries like the UK and Canada. In the U.S., Burger King also introduced the “Impossible Whopper,” and many other QSRs followed suit by incorporating plant-based chicken nuggets, sandwiches, and wraps into their menus.

As more chains continue to embrace plant-based alternatives, the plant-based chicken market is expected to see continued growth in foodservice. A 2021 survey by Mintel found that 39% of U.S. consumers said they would be more likely to visit a restaurant offering plant-based meat options, demonstrating a significant opportunity for plant-based chicken in this segment.

The growing inclusion of plant-based chicken on restaurant menus is a clear indication of the broader shift in consumer preferences, with more people seeking sustainable, health-conscious food options. As more QSRs adopt plant-based offerings, the accessibility of plant-based chicken is set to expand significantly, making it a key trend in the market.

Expansion of Plant-based Chicken into Retail and Supermarkets

Another major trend for plant-based chicken is the expansion of plant-based products into mainstream retail and supermarkets. Consumers are increasingly seeking plant-based alternatives in grocery stores, and plant-based chicken is no exception.

A report from the U.S. Department of Agriculture (USDA) noted that plant-based meat sales in grocery stores surpassed $1.4 billion in 2020, with plant-based chicken representing a significant portion of those sales. This trend is being driven by both growing demand for plant-based products and the increasing availability of these products in supermarkets.

In particular, supermarkets in North America and Europe have been stocking more plant-based chicken products in the refrigerated and frozen sections, making it easier for consumers to access plant-based alternatives. Whole Foods and Walmart are among the retailers that have significantly expanded their plant-based meat offerings.

The plant-based chicken category includes a variety of products such as nuggets, tenders, patties, and fillets, giving consumers multiple choices when shopping for meat alternatives. According to a 2021 survey by Nielsen, 59% of U.S. consumers had purchased plant-based products, and nearly 20% of them purchased plant-based meat from supermarkets. This indicates the growing acceptance of plant-based foods in mainstream retail outlets.

As more supermarket chains introduce plant-based chicken options, the availability and visibility of these products are expected to increase, further driving market growth and consumer adoption. Retailers are also expanding their plant-based product ranges to include plant-based chicken, positioning it as a mainstream food option.

Focus on Clean Label and Natural Ingredients

A growing trend in the plant-based chicken market is the increasing emphasis on clean-label, natural, and minimally processed ingredients. Consumers are becoming more aware of the ingredients in their food and are increasingly looking for products that are free from artificial additives, preservatives, and chemicals.

According to The Good Food Institute (GFI), one of the key consumer preferences driving the plant-based food sector is the demand for clean-label products. The trend toward clean-label foods is particularly strong among Millennials and Gen Z consumers, who are more likely to choose products with simple, recognizable ingredients.

Regional Analysis

The North American region dominated the plant-based chicken market in 2023, capturing a significant share of 43.3%, with a market value of approximately USD 1.4 billion. This growth is driven by increasing consumer awareness regarding health, sustainability, and animal welfare, as well as a strong presence of leading plant-based brands like Beyond Meat and Impossible Foods.

The U.S., in particular, is witnessing a rapid surge in demand for plant-based chicken alternatives, as reflected in the growing presence of these products in supermarkets and quick-service restaurants (QSRs). Additionally, governmental support for plant-based food innovation and sustainability initiatives is further propelling the market in North America.

In Europe, the plant-based chicken market is expanding, driven by a growing trend towards plant-based diets and climate-conscious consumer behavior. Countries like the UK, Germany, and France are seeing strong growth in plant-based food adoption, with major foodservice chains and retailers adding plant-based chicken options to their menus and shelves. The market is projected to grow at a CAGR of 8.6% from 2023 to 2027, supported by initiatives like the EU’s Farm to Fork Strategy aimed at reducing animal protein consumption.

In the Asia Pacific region, the plant-based chicken market is still in the nascent stages but has immense potential, particularly in countries like China and India, where traditional meat consumption is high. With increasing urbanization and changing dietary preferences, the demand for plant-based alternatives is growing rapidly. However, the market share remains relatively smaller compared to North America and Europe but is expected to witness significant growth over the next few years, driven by rising health awareness and environmental concerns.

The Middle East & Africa and Latin America regions present promising opportunities, particularly in markets with growing middle-class populations and increasing health-consciousness. While these regions currently contribute a smaller share to the global plant-based chicken market, rising awareness and adoption of plant-based diets could spur future growth.

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Key Players Analysis

The plant-based chicken market is highly competitive, with key players continually innovating to meet the growing consumer demand for plant-based alternatives. Beyond Meat, Inc. and Impossible Foods Inc. are two of the leading brands driving the market, with their well-established presence in both retail and foodservice sectors.

Beyond Meat, known for its plant-based burger patties and sausages, has expanded its offerings to include plant-based chicken, while Impossible Foods, with its signature plant-based meat products, is also broadening its portfolio to capture more market share in the plant-based chicken segment. Both companies benefit from strong retail distribution networks and partnerships with major food chains, propelling their growth.

Other significant players in the market include Atlantic Natural Foods LLC, which offers the Loma Linda brand of plant-based products, and Conagra Brands, which owns Gardein, a leading brand of plant-based meat alternatives. Kellogg’s owns MorningStar Farms, a longstanding player in the plant-based food industry, while Maple Leaf Foods and Monde Nissin are expanding their portfolios in response to the growing demand for plant-based products.

Unilever and Tyson Foods have also entered the market with their own plant-based brands, such as The Vegetarian Butcher and Raised & Rooted, respectively. Quorn Foods and Tofurky are known for their diverse range of plant-based meat alternatives and have a strong foothold in both North American and European markets.

Additional players such as Ingredion Inc., Alpha Foods, and Puris Proteins focus on ingredient innovation and the development of plant-based protein sources, contributing to the overall growth and evolution of the plant-based chicken market. As consumer preferences continue to shift toward more sustainable and healthier options, these companies are poised to expand their reach and influence across global markets.

Top Key Players in the Market

- Atlantic Natural Foods LLC

- Beyond Meat, Inc.

- Impossible Foods Inc.

- CHS INC,

- Conagra Foods

- Gardein (Conagra Brands)

- Ingredion Inc.

- Kellogg Company

- Lightlife Foods Alpha Foods

- Maple Leaf Foods

- Monde Nissin

- MorningStar Farms (A subsidiary of Kellogg Company)

- Puris Proteins, LLC,

- Quorn Foods

- Sunfed

- Sweet Earth Foods (A subsidiary of Nestlé)

- No Evil Foods

- Tofurky

- Tyson Foods, Inc

- Unilever

Recent Developments

In 2023, Atlantic Natural Foods continued to expand its product portfolio, capitalizing on the rising consumer demand for sustainable, plant-based proteins.

In 2023, Beyond Meat reported total revenues of approximately USD 400 million, with a significant portion of that coming from their plant-based chicken products, including nuggets, tenders, and strips. These products are available across major retailers, fast food chains, and foodservice channels

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2023) | USD 3.5 Bn |

| Forecast Revenue (2033) | USD {{val2}} |

| CAGR (2024-2033) | 17.2% |

| Base Year for Estimation | 2023 |

| Historic Period | 2019-2022 |

| Forecast Period | 2024-2033 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Product Type (Burger Patty, Crumbles and Grounds, Sausages, Hot Dogs, Nuggets, Bacon Chips, Others), By Source (Soy-based Protein, Wheat-based Protein, Pea-based Protein, Canola-based Protein, Fava Bean-based Protein, Potato-based Protein, Rice-based Protein, Lentin-based Protein, Flax-based Protein, Chia-based Protein, Com-based Protein), By Raw material (Soy, Wheat, Pea, Others), By Storage (Refrigerated Plant-based Meat, Frozen Plant-based Meat, Shelf-stable Plant-based Meat), By Distribution Channel (Hypermarkets/Supermarkets, Convenience Stores, Specialty Food Stores, Online Retail, Others) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA |

| Competitive Landscape | Atlantic Natural Foods LLC, Beyond Meat, Inc., Impossible Foods Inc., CHS INC,, Conagra Foods, Gardein (Conagra Brands), Ingredion Inc., Kellogg Company, Lightlife Foods Alpha Foods, Maple Leaf Foods, Monde Nissin, MorningStar Farms (A subsidiary of Kellogg Company), Puris Proteins, LLC,, Quorn Foods, Sunfed, Sweet Earth Foods (A subsidiary of Nestlé), No Evil Foods, Tofurky, Tyson Foods, Inc, Unilever |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |