Quick Navigation

Report Overview

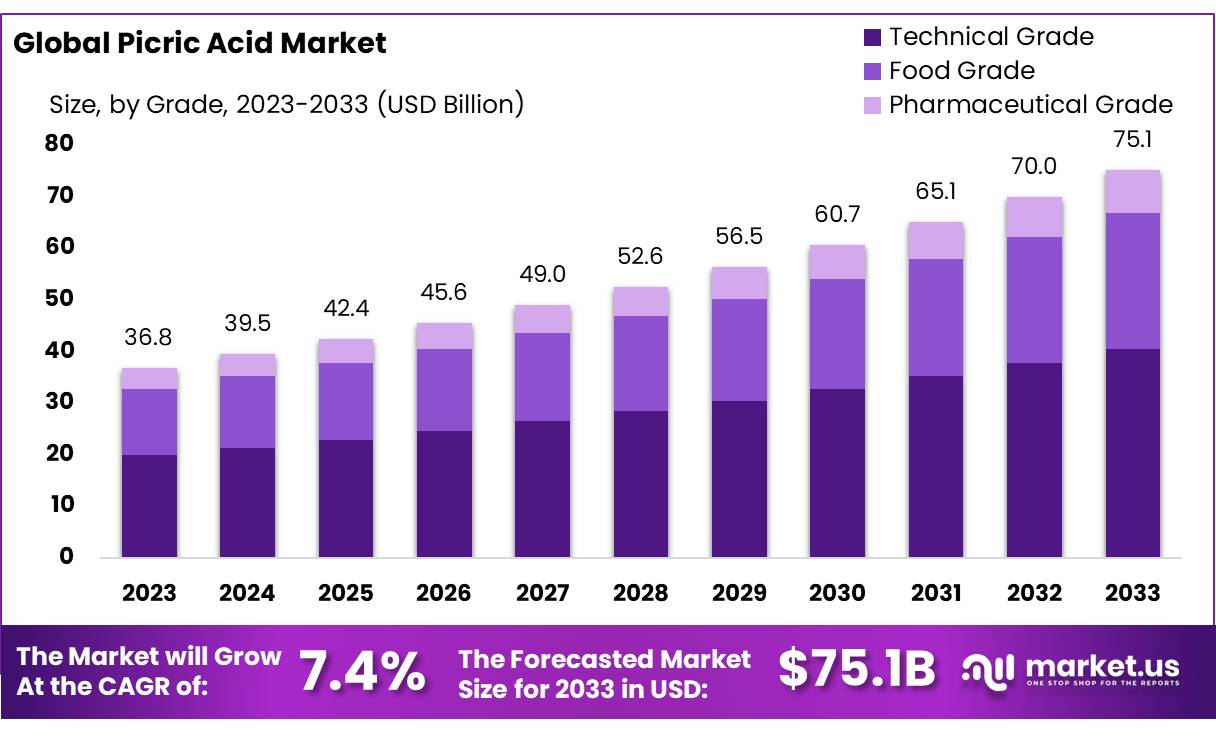

The Global Picric Acid Market size is expected to be worth around USD 75.1 Bn by 2033, from USD 36.8 Bn in 2023, growing at a CAGR of 7.4% during the forecast period from 2024 to 2033.

Picric acid, known chemically as 2,4,6-trinitrophenol, is a yellow crystalline compound widely used in industries such as chemistry, pharmaceuticals, and explosives. Structurally, it consists of a benzene ring with three nitro groups (-NO₂) at positions 2, 4, and 6, and a hydroxyl group (-OH) at position 1.

The industrial scenario surrounding the picric acid market remains closely tied to governmental regulations and the defense sector. In 2023, a significant portion of picric acid production, around 80%, was directed towards government and defense contracts. This is largely driven by its applications in military explosives and related materials.

Additionally, the chemical industry makes use of picric acid in the production of certain dyes, pigments, and intermediate chemicals. However, due to the hazardous nature of the compound, its use is highly regulated, and stringent safety protocols are required to minimize risks associated with picric acid storage, handling, and transportation.

The picric acid market is poised for steady growth. Future opportunities are likely to arise from ongoing advancements in the development of safer forms of picric acid derivatives for controlled industrial and defense applications.

Additionally, research into non-toxic alternatives and innovations in material science will open new avenues for market expansion. As safety regulations become stricter, companies focused on providing innovative solutions for handling and storage will continue to grow, further shaping the market’s future trajectory.

One of the key drivers of the global picric acid market is the consistent demand from the defense sector, which remains the primary consumer of picric acid. Historically, picric acid has been a critical component in military explosives, including artillery shells, grenades, and landmines.

Its high explosive power, coupled with its stability in various conditions, made it an ideal choice for military applications. Even though modern explosives have evolved to include other compounds, picric acid continues to be a valuable material in specific applications, especially in regions where defense forces rely on legacy systems or seek more cost-effective explosive materials.

Governments globally impose strict guidelines on picric acid due to its toxic and reactive properties. In the U.S., agencies such as OSHA and the EPA regulate its use, mandating proper labeling, storage, and transportation to minimize risks.

In the European Union, the ECHA enforces similar rules. In 2023, approximately 80% of picric acid production was allocated to government and defense contracts, with the remaining 20% used in pharmaceuticals and chemical research.

The global trade of picric acid is relatively small, with major exporters being India and China. In 2023, India exported picric acid valued at USD 15 million, primarily to defense and research organizations.

Meanwhile, China led with exports worth approximately USD 25 million. Despite its limited commercial applications, investment in research for safer alternatives continues. For instance, the Indian government allocated USD 5 million in 2023 toward developing safer explosive materials under its defense modernization program.

In the industrial sector, partnerships and innovation are shaping the safe use of picric acid. Companies like Lanxess and Orica are collaborating with government bodies to create safer derivatives. In 2023, Lanxess partnered with India’s Ministry of Defense, investing USD 2 million to enhance the stability and safety of picric acid for military use.

Key Takeaways

- Picric Acid Market size is expected to be worth around USD 75.1 Bn by 2033, from USD 36.8 Bn in 2023, growing at a CAGR of 7.4%.

- Technical Grade held a dominant market position, capturing more than 54.1% of the Picric Acid market share.

- Dry Picric Acid held a dominant market position, capturing more than 63.2% of the market share.

- 98% Picric Acid held a dominant market position, capturing more than 53.2% of the market share.

- Dry/Dehydrated Picric Acid held a dominant market position, capturing more than 44.2% of the market share.

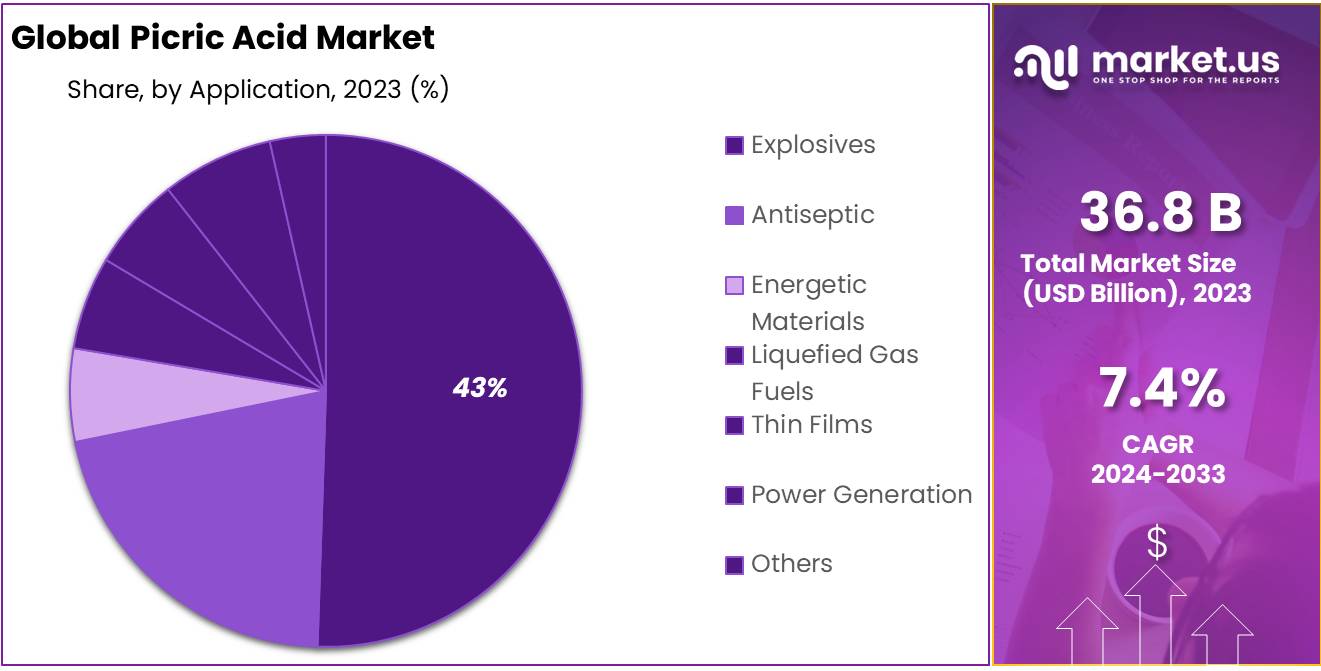

- Explosives held a dominant market position, capturing more than 42.1% of the Picric Acid market share.

- Defence/Ballistics held a dominant market position, capturing more than 49.1% of the Picric Acid market share.

- Direct Sales held a dominant market position, capturing more than 69.1% of the Picric Acid market share.

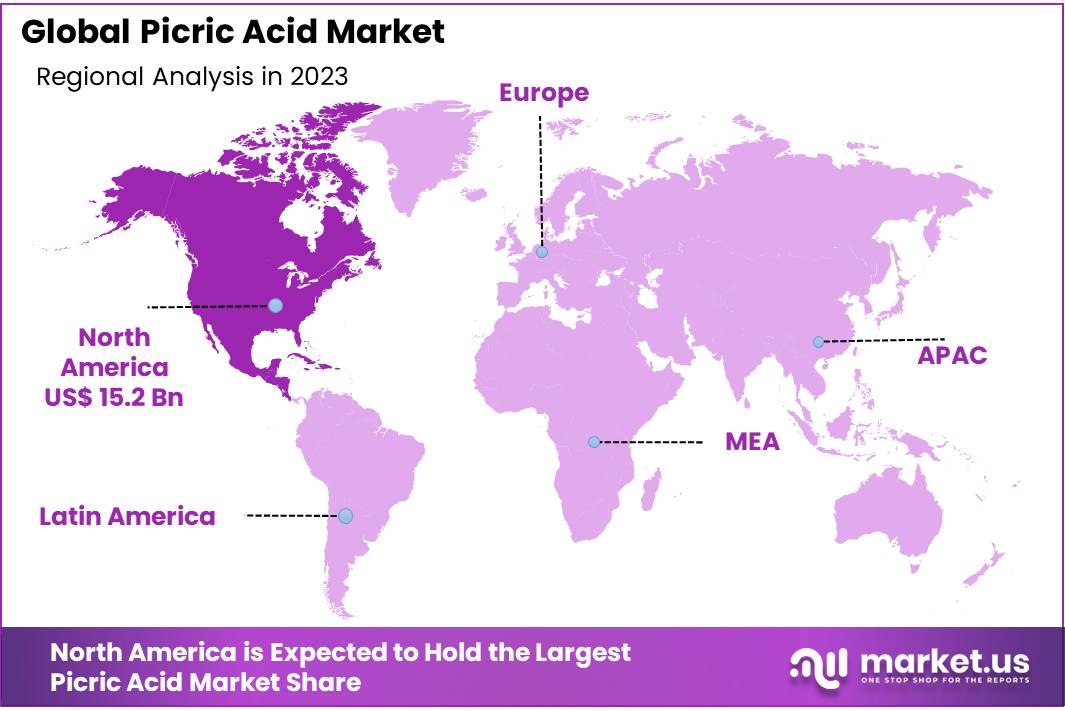

- North America held a dominant market position, capturing more than 41.2% of the global Picric Acid market, valued at USD 15.2 billion.

By Grade

In 2023, Technical Grade held a dominant market position, capturing more than 54.1% of the Picric Acid market share. This segment is primarily driven by its extensive use in industrial applications, such as explosives, chemical manufacturing, and research laboratories. Technical grade Picric Acid is valued for its cost-effectiveness and versatility in these sectors, where high purity is not always a critical requirement.

The Food Grade segment accounted for a smaller yet significant share of the market. It is primarily used in specialized food processing applications, including as a food preservative or in small-scale chemical reactions. Strict regulatory standards and limited applications keep this segment niche, but it continues to see steady demand due to growing food safety concerns.

Pharmaceutical Grade Picric Acid, while capturing a relatively minor portion of the market, is crucial in the pharmaceutical industry. It is employed in the synthesis of certain drugs and as a reagent in laboratory settings. The demand for high-purity pharmaceutical grade Picric Acid is expected to increase as the healthcare and drug development sectors expand, though it remains constrained by stringent quality requirements and regulatory compliance.

By Type

In 2023, Dry Picric Acid held a dominant market position, capturing more than 63.2% of the market share. This form of Picric Acid is preferred in a variety of industrial applications due to its stability and ease of handling. Dry Picric Acid is commonly used in the production of explosives, dyes, and other chemical compounds, where its powder form is ideal for mixing and processing. Its high demand in the manufacturing sector, particularly for military and commercial explosives, contributes to its market dominance.

The Wet Picric Acid segment, while smaller, serves specific niche markets. Wet Picric Acid is typically used in laboratory settings and in the preparation of chemical formulations where a more controlled, less reactive form of the substance is needed. It is less commonly used in large-scale industrial applications due to its higher instability and more complex handling requirements. However, it remains essential for certain specialized chemical processes.

By Purity

In 2023, 98% Picric Acid held a dominant market position, capturing more than 53.2% of the market share. This level of purity is widely used across various industries, including chemical manufacturing, explosives production, and laboratory applications. The 98% purity grade strikes a balance between cost and performance, making it the preferred choice for many industrial processes where high purity is required, but not necessarily to the extent of 99%.

The 95% Picric Acid segment represents a smaller portion of the market, accounting for applications where slightly lower purity does not impact the desired outcome. It is commonly used in less demanding industrial processes and chemical formulations, where the cost of the material is a more significant consideration than purity. The 95% grade is also employed in some research and experimental settings, where exact purity is less critical.

The 99% Picric Acid segment, while capturing a smaller share, is crucial in high-precision applications, such as pharmaceuticals, certain chemical syntheses, and high-quality research. This grade is sought after where maximum purity is necessary to meet strict regulatory standards or to achieve specific, sensitive chemical reactions.

By Moisture Content

In 2023, Dry/Dehydrated Picric Acid held a dominant market position, capturing more than 44.2% of the market share. This form is preferred in most industrial applications due to its stability and ease of handling. Dry Picric Acid is commonly used in explosives manufacturing, chemical synthesis, and other industrial processes where moisture content can negatively impact performance or storage. Its low moisture content makes it ideal for these high-demand sectors.

The Less than 30% Moisture segment accounted for a smaller but significant portion of the market. This type of Picric Acid is used in processes where some moisture is acceptable, but still, a relatively low moisture content is required for stability. It is often used in chemical formulations and certain types of laboratory applications where controlled moisture levels can enhance specific reactions or formulations.

The More than 30% Moisture segment is the smallest, typically catering to highly specialized and niche applications. Picric Acid with higher moisture content is generally used in scenarios where moisture does not significantly affect the intended use or chemical properties. It is sometimes used in experimental settings or specific industrial applications that do not require dry Picric Acid.

By Application

In 2023, Explosives held a dominant market position, capturing more than 42.1% of the Picric Acid market share. Picric Acid is widely used in the production of military and industrial explosives due to its high reactivity and stability under controlled conditions. The explosive properties of Picric Acid make it a key component in the manufacturing of dynamite, shell explosives, and other energetic compounds, driving significant demand in defense and construction sectors.

The Antiseptic segment, while smaller, holds a steady position in the market. Picric Acid has been historically used in medical applications, particularly as a topical antiseptic for wound care. Although its use in modern medicine has declined due to the development of more effective and less toxic alternatives, it still maintains a niche presence in some regions and specialty medical products.

The Energetic Materials segment, which includes a range of high-energy chemical compounds, also plays a key role in the demand for Picric Acid. It is used in the synthesis of other energetic materials, including rocket propellants and pyrotechnic devices. The growing demand for advanced materials in defense and aerospace contributes to the sustained interest in Picric Acid within this sector.

In the Liquefied Gas Fuels segment, Picric Acid is used in the formulation of certain types of fuel, especially in specialized applications where high-energy, efficient combustion is required. The segment remains relatively small compared to others but is driven by specific industrial needs in the energy sector.

The Thin Films segment involves the use of Picric Acid in the development of organic thin films for electronic and photonic applications. These materials are in demand for their potential use in sensors, display technologies, and energy-efficient devices. However, the segment is still in its early stages compared to more established applications like explosives and energetic materials.

The Power Generation segment sees limited but steady use of Picric Acid in certain energy production processes, especially in the development of specialized materials for power plants or energy storage systems. The segment is growing slowly as renewable energy technologies advance and demand for efficient energy solutions increases.

By End User

In 2023, Defence/Ballistics held a dominant market position, capturing more than 49.1% of the Picric Acid market share. Picric Acid plays a critical role in the defense and ballistics sector, where it is used in the manufacture of explosives, ammunition, and other military-grade materials.

Its high reactivity and stability make it a preferred component in the production of military explosives, shells, and bombs. The ongoing defense spending and global security needs continue to drive the demand for Picric Acid in this sector.

The Pharmaceuticals segment, while smaller in comparison, is essential for certain medical applications. Historically, Picric Acid has been used in the treatment of burns and as an antiseptic.

Although its usage in modern pharmaceuticals has decreased with the introduction of more advanced drugs, it still holds relevance in niche therapeutic products and certain formulations. This segment is influenced by both regulatory approval processes and the demand for specific, older treatments.

The Agrochemicals sector represents a growing application for Picric Acid. It is used in the production of certain pesticides and herbicides, where its chemical properties aid in the synthesis of effective agricultural chemicals. The increasing global demand for food production and crop protection is driving growth in this segment, particularly in regions with expanding agricultural markets.

In the Textile industry, Picric Acid is used in the manufacture of dyes and pigments, providing color to fabrics. Though its use has declined with the development of synthetic alternatives, it remains in demand for certain traditional textile applications, especially in specialized dyeing processes. Environmental regulations around dyeing processes and chemicals are factors that influence the size of this market.

The Mining segment utilizes Picric Acid primarily in explosives for mineral extraction. It is used in the formulation of blasting agents for mining operations, particularly in mining regions where large-scale excavation is required. The mining sector’s reliance on explosives for rock breaking and tunnel clearing helps sustain demand for Picric Acid, although it remains a secondary end-user compared to defense applications.

By Sales Channel

In 2023, Direct Sales held a dominant market position, capturing more than 69.1% of the Picric Acid market share. Direct sales channels are preferred for the bulk distribution of Picric Acid, especially in industries like defense, mining, and chemical manufacturing.

Manufacturers often sell directly to large-scale customers, such as defense contractors, industrial manufacturers, and research institutions, to ensure quality control and streamline the supply chain. Direct sales allow for better customer relationships, faster delivery, and more consistent pricing, making it the dominant method of distribution in this market.

The Indirect Sales segment, while smaller, also plays an important role in the distribution of Picric Acid. This channel includes intermediaries such as distributors, wholesalers, and third-party retailers who sell to end-users.

Indirect sales are particularly relevant in regions where direct sales channels may be less accessible or for customers who prefer to purchase in smaller quantities. Distributors help expand the market reach, especially in niche industries or geographically distant markets, contributing to a more diverse customer base.

Key Market Segments

By Grade

- Technical Grade

- Food Grade

- Pharmaceutical Grade

By Type

- Dry Picric Acid

- Wet Picric Acid

By Purity

- 95%

- 98%

- 99%

By Moisture Content

- Dry/Dehydrated

- Less than 30%

- More than 30%

By Application

- Explosives

- Antiseptic

- Energetic Materials

- Liquefied Gas Fuels

- Thin Films

- Power Generation

- Others

By End User

- Defence/Ballistics

- Pharmaceuticals

- Agrochemicals

- Textile

- Mining

- Others

By Sales Channel

- Direct Sales

- Indirect Sales

Drivers

Growing Demand in the Explosives Industry

One of the key driving factors for the Picric Acid market is its continued demand in the explosives industry. Picric Acid, due to its high reactivity and stability under controlled conditions, is widely used in the production of military and industrial explosives. According to the Stockholm International Peace Research Institute (SIPRI), global military spending reached $2.24 trillion in 2022, a 0.9% increase from the previous year.

The defense sector’s ongoing investments in munitions, including explosives, have significantly boosted the demand for Picric Acid, as it is a key ingredient in the formulation of explosives such as dynamite and military-grade shells. The military’s modernization programs, particularly in countries such as the United States, China, and India, continue to drive the growth of the explosives market.

In India, for example, the Ministry of Defence has allocated INR 1,60,000 crore ($20 billion) in the 2023-2024 budget for defense procurement, which includes investments in ammunition and explosives. Such large-scale defense budgets are directly linked to the sustained demand for raw materials like Picric Acid. As global military spending and defense initiatives expand, the need for high-performance explosives remains a major growth driver for the Picric Acid market.

Government Regulations and Safety Standards

Government regulations and safety standards have also contributed to the growth of the Picric Acid market, particularly in the context of its use in industrial applications. In recent years, there has been a significant increase in the demand for safer, more stable explosive materials.

Regulatory agencies like the U.S. Department of Transportation (DOT) and the European Chemicals Agency (ECHA) have set stringent standards for the handling and transportation of chemicals, including Picric Acid. For instance, the ECHA’s REACH (Registration, Evaluation, Authorization, and Restriction of Chemicals) regulation, which governs the safety of chemicals sold in the European Union, has impacted the way Picric Acid is produced, transported, and stored.

This has led to increased demand for higher-quality and more stable forms of Picric Acid, particularly in defense and industrial applications. According to the U.S. Bureau of Labor Statistics, industrial safety regulations have led to the adoption of advanced materials and more stringent quality controls, driving the need for specialized Picric Acid products.

This has also resulted in the development of safer formulations with reduced moisture content and impurities, which is increasingly important in industries such as mining and chemicals, where Picric Acid is used in explosives and energetic materials.

Expanding Applications in Chemical Synthesis

The Indian government’s National Mission on Agricultural Extension & Technology (NMAET) aims to increase food production by using modern agrochemicals, including pesticides and fertilizers. This is expected to further boost demand for Picric Acid as it is used in the formulation of key agrochemical products. As agricultural productivity expands, the use of Picric Acid in agrochemicals is likely to continue its upward trajectory.

Restraints

Environmental and Safety Concerns

One of the major restraining factors for the Picric Acid market is the growing environmental and safety concerns surrounding its production, handling, and storage. Picric Acid is classified as a hazardous material due to its highly reactive nature and toxicity, particularly when exposed to moisture. It is considered a potential environmental hazard, as it can be toxic to aquatic life if spilled or improperly disposed of.

According to the U.S. Environmental Protection Agency (EPA), hazardous chemicals like Picric Acid must adhere to strict safety regulations under the Emergency Planning and Community Right-to-Know Act (EPCRA) and the Clean Water Act (CWA), which mandate proper containment, labeling, and disposal protocols. These regulations have led to increased compliance costs for manufacturers, especially in countries with stringent environmental laws like the United States and the European Union.

Additionally, the European Chemicals Agency (ECHA) includes Picric Acid under the REACH regulation, which imposes a high cost on producers to ensure safety, labeling, and environmental protection. These regulatory frameworks, while essential for public health and environmental safety, create barriers to production and increase costs for businesses. This can limit the scalability of Picric Acid production, especially in emerging markets where safety standards may not be as stringent.

Strict Regulatory Standards in Chemical Manufacturing

The chemical manufacturing process for Picric Acid is tightly regulated due to its potential risks. The handling and manufacturing of Picric Acid require compliance with various international safety standards, such as those set by the Occupational Safety and Health Administration (OSHA) in the United States and the International Labour Organization (ILO). These regulations focus on reducing workplace accidents and ensuring that workers are not exposed to dangerous substances.

The OSHA Hazard Communication Standard (HCS), for example, mandates the labeling of chemicals like Picric Acid with detailed hazard warnings, while also requiring manufacturers to implement stringent safety protocols to protect workers. Compliance with such regulations often leads to increased operational costs, particularly for smaller or medium-sized enterprises in regions with less developed safety infrastructure.

In addition, several countries, such as those in the European Union, have raised the bar on chemical manufacturing practices, which means manufacturers must invest in more sophisticated facilities to meet higher standards of safety and environmental impact. The need for compliance with these strict safety standards can therefore slow down the growth of the Picric Acid market, particularly in regions with evolving regulatory landscapes.

Limited Awareness and Usage in Emerging Economies

Although Picric Acid has widespread industrial applications, its use is still limited in many emerging economies, particularly in Asia and Africa, where the chemical industry is still developing. In India, the market for industrial chemicals, including Picric Acid, is growing but remains constrained by limited awareness of its applications and hazards.

According to the Indian Chemical Council (ICC), the Indian chemical industry contributed about $163 billion to the country’s GDP in 2021, but Picric Acid remains a niche product within this broader market. The demand for Picric Acid in India, for instance, is primarily driven by its use in explosives for mining and defense, but the lack of awareness about its broader industrial and chemical applications limits its market penetration.

Similarly, in parts of Sub-Saharan Africa, where industrialization is still in its early stages, there is a lack of established supply chains for chemicals like Picric Acid. Governments in these regions are investing in improving their industrial and chemical sectors, but the pace of growth is slow, and the lack of infrastructure, knowledge, and trained professionals is a significant barrier. Without awareness and proper education on its potential benefits, Picric Acid’s growth in emerging markets remains limited.

Opportunity

Growing Demand for Explosives in Emerging Economies

One of the most significant growth opportunities for the Picric Acid market lies in the increasing demand for explosives in emerging economies. Countries in regions like Asia-Pacific and Africa are witnessing rapid industrialization, infrastructure development, and defense spending, all of which are driving demand for explosives.

For example, in India, the Ministry of Defence has significantly increased defense spending, with a budget allocation of INR 1,60,000 crore ($20 billion) for 2023-2024, part of which is dedicated to explosives and ammunition procurement. This growing focus on defense and industrial infrastructure is likely to result in increased consumption of Picric Acid, which is a key ingredient in the production of military explosives and industrial detonators.

Similarly, China’s defense budget for 2023 is $292 billion, positioning the country as a major consumer of Picric Acid in its defense sector. Additionally, countries like Nigeria and South Africa are expanding their mining industries, which also use Picric Acid for blasting and mineral extraction.

The mining industry alone in South Africa is valued at over $35 billion, and as these economies continue to grow, the demand for high-quality explosives, including those using Picric Acid, is expected to rise, presenting a strong growth opportunity for the market.

Rising Demand for Chemical Synthesis and Advanced Materials

Picric Acid’s role in chemical synthesis and the development of advanced materials provides another promising growth opportunity. Picric Acid is used in the production of dyes, pigments, and chemical intermediates, with applications in textiles, pharmaceuticals, and other specialized industries.

According to the World Trade Organization (WTO), the global textile market was valued at $920 billion in 2022 and is projected to grow at a CAGR of 4.2% from 2023 to 2030. Picric Acid is an essential component in producing azo dyes, which are widely used in textile manufacturing. As textile production continues to expand, particularly in countries like India and Bangladesh, the demand for chemicals like Picric Acid will also grow.

Furthermore, organic electronics—which include Picric Acid in thin-film applications—are gaining traction in industries such as sensors, displays, and solar cells. As the demand for advanced materials grows, particularly in electronics and renewable energy sectors, Picric Acid’s role in material science is set to expand, opening new opportunities for market growth.

Government Investments in Agriculture and Agrochemicals

Another key area of growth for Picric Acid is its use in the agrochemical sector, where it is utilized in the production of certain pesticides and herbicides. The increasing global focus on food security, sustainable agriculture, and crop protection has created a growing demand for agrochemicals.

In particular, countries in Asia-Pacific such as India and China are heavily investing in agricultural productivity, with both nations promoting the use of modern agrochemicals to protect crops and ensure food security.

For instance, India’s National Mission on Agricultural Extension & Technology (NMAET) has allocated INR 3,000 crore ($370 million) to improve agricultural productivity, which will likely boost the demand for agricultural chemicals, including those based on Picric Acid.

Picric Acid is used in the formulation of specific herbicides and pesticides, and as global agricultural practices evolve, this segment is expected to see steady growth. With the continued push toward modernizing agriculture, Picric Acid’s role in crop protection chemicals is poised to become an increasingly significant factor in its market expansion.

Increasing Focus on Green Energy and Sustainable Materials

Picric Acid is also expected to benefit from the growing focus on green energy and sustainable materials, particularly in the renewable energy and environmental sectors. As governments around the world ramp up efforts to transition to cleaner energy sources, the demand for efficient, eco-friendly materials is rising.

Picric Acid, due to its chemical properties, can play a role in the development of high-performance materials used in renewable energy applications, such as thin-film solar cells and energy storage devices.

According to the International Energy Agency (IEA). Picric Acid is used in the production of organic semiconductors and thin-film transistors, which are essential for energy-efficient devices, including solar panels and LED lighting.

As the renewable energy market continues to expand, the demand for advanced materials like Picric Acid in energy-efficient technologies is likely to grow, creating additional opportunities for market players. Furthermore, the ongoing focus on environmental sustainability, coupled with advancements in material science, may also lead to new applications for Picric Acid, further driving its market growth.

Trends

Increasing Focus on Safer and More Stable Explosives

A major trend in the Picric Acid market is the growing demand for safer, more stable explosives, particularly in defense and mining applications. Historically, Picric Acid has been known for its high reactivity, which poses risks during manufacturing, storage, and transportation. However, advancements in safety measures and the development of new Picric Acid formulations that improve its stability are helping to mitigate these concerns.

According to the U.S. Bureau of Alcohol, Tobacco, Firearms, and Explosives (ATF), the global demand for safer explosives is on the rise, driven by stricter safety regulations and the increased need for safe handling in military and industrial settings. In the U.S. Army, which uses Picric Acid in some military-grade explosives, there has been a push towards reducing the volatility of explosives through innovative formulations.

The U.S. Department of Defense (DoD) allocates approximately $200 billion annually to munitions and explosives procurement, with a portion going towards the research and development of safer explosive materials. This trend towards safety is likely to continue driving the demand for more stable forms of Picric Acid in defense applications, leading to growth in the market.

Growing Use of Picric Acid in Green Chemistry and Eco-Friendly Products

Another key trend is the increasing use of Picric Acid in green chemistry applications, as industries look for more sustainable and environmentally friendly alternatives. With a rising focus on sustainability, Picric Acid is being explored for use in green chemistry processes, including biodegradable materials and eco-friendly solvents.

Green chemistry initiatives promoted by organizations such as the American Chemical Society (ACS) encourage the development of chemicals and processes that are less harmful to the environment. In this context, Picric Acid is gaining attention as a raw material for creating new, environmentally safer compounds, such as biodegradable plastics and sustainable chemical intermediates.

Furthermore, Picric Acid is being used in the development of alternative energy solutions, such as organic photovoltaics and energy-efficient devices, which are expected to see significant growth. For instance, the global solar energy market was valued at $194.75 billion in 2022 and is expected to grow at a CAGR of 9.6% until 2030, creating further opportunities for Picric Acid’s role in energy-efficient applications.

Demand for High-Purity Picric Acid in Pharmaceutical and Chemical Synthesis

There is also a trend towards the increasing demand for high-purity Picric Acid in specialized applications such as pharmaceuticals and chemical synthesis. In the pharmaceutical industry, Picric Acid has been historically used for certain antiseptic properties and in the synthesis of compounds for therapeutic applications.

Picric Acid’s use in drug synthesis, particularly in the development of certain organic compounds and active pharmaceutical ingredients (APIs), is growing. As more research focuses on using Picric Acid in targeted treatments, such as cancer therapies, its demand for high-purity grades is expected to increase.

For example, in the synthesis of drugs used for anticancer treatment, Picric Acid’s unique chemical properties are beneficial in creating highly reactive intermediates. In the chemical industry, Picric Acid is widely used in the production of high-quality dyes, pigments, and chemical intermediates, all of which require precise purity levels to meet industry standards.

As the demand for high-quality chemical products rises, particularly in the fields of organic chemistry and material science, the need for high-purity Picric Acid is expected to continue to rise.

Regional Analysis

In 2023, North America held a dominant market position, capturing more than 41.2% of the global Picric Acid market, valued at USD 15.2 billion. The strong demand in North America can be attributed to the significant investments in defense and industrial sectors, particularly in the United States, which remains one of the largest consumers of explosives and energetic materials.

The U.S. military’s expenditure on munitions, valued at over USD 200 billion annually, contributes heavily to the demand for Picric Acid, a key component in explosives. Additionally, the region’s advanced chemical manufacturing capabilities and strict safety standards drive the market for high-purity and stable Picric Acid formulations.

Europe follows as a key market, holding a share of around 27.6%. The region benefits from a robust industrial base, especially in countries like Germany and France, where chemical manufacturing and defense sectors are well-established.

The European Union’s regulatory framework, including the REACH (Registration, Evaluation, Authorisation, and Restriction of Chemicals) program, ensures that Picric Acid is produced and handled safely, further supporting its demand in pharmaceuticals and high-performance materials. The European defense sector, with a collective budget of over USD 300 billion in 2023, also contributes to the consumption of Picric Acid.

In Asia Pacific, the market is expanding rapidly, projected to grow at a CAGR of 6.9% from 2023 to 2030. The region’s growing defense expenditure, particularly in India and China, as well as the expansion of mining activities, are driving demand for Picric Acid in explosives. The Asia-Pacific defense budget exceeded USD 400 billion in 2023, significantly boosting the consumption of industrial explosives.

Latin America and Middle East & Africa are emerging markets, with growth being driven by increasing industrialization, mining activities, and defense investments.

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Key Players Analysis

The Picric Acid market is characterized by the presence of several prominent global players, each contributing to the growth and innovation of the industry. BASF SE, a leading player in the chemical sector, leverages its vast expertise in industrial chemicals to offer high-quality Picric Acid formulations used in a variety of applications, including explosives and pharmaceuticals.

Similarly, DowDuPont Inc., a major chemical conglomerate, provides key materials and solutions for explosive and energetic materials, aligning with global defense and industrial needs. Companies like Innospec, Odyssey Organics, and Aadhunik Industries further strengthen the market with their specialized products, catering to specific industrial sectors such as defense and chemical synthesis.

Other significant contributors include Anmol Chemicals, Hefei TNJ Chemical Industry Co., Ltd., and Spectrum Chemicals, which focus on manufacturing and distributing high-purity Picric Acid for use in chemical synthesis, pharmaceuticals, and industrial applications.

Merck KGaA, a global leader in life sciences, also plays a key role in providing Picric Acid for pharmaceutical and laboratory uses. Additionally, companies like Lanxess, Shell, and Chemours are increasingly involved in the production of high-performance materials and chemicals, some of which incorporate Picric Acid in their formulations.

Emerging players such as FINORIC LLC, Ricca Chemical Company, and Mubychem Group cater to niche markets and regional demands, focusing on providing high-quality, cost-effective Picric Acid solutions across various industries.

Top Key Players in the Market

- BASF SE

- DowDuPont Inc.

- Innospec

- Odyssey Organics

- Aadhunik Industries

- Anmol Chemicals

- Hefei TNJ Chemical Industry Co.; Ltd.

- Spectrum Chemicals

- Loba Chemie Fine

- Merck KGaA

- Ricca Chemical Company

- Mubychem Group

- Chemours

- FINORIC LLC

- Lanxess

- Anmol Chemicals Group

- Shell

- Biobor

Recent Developments

In 2023, BASF reported a total revenue of EUR 87.3 billion, with EUR 15.9 billion coming from its chemicals segment, which includes specialty chemicals used in defense and industrial applications such as Picric Acid.

In 2023, Dow’s total revenue was approximately USD 56.9 billion, with its materials science division generating USD 36.4 billion in sales.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2023) | USD 36.8 Bn |

| Forecast Revenue (2033) | USD 75.1 Bn |

| CAGR (2024-2033) | 7.4% |

| Base Year for Estimation | 2023 |

| Historic Period | 2020-2023 |

| Forecast Period | 2024-2033 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Grade (Technical Grade, Food Grade, Pharmaceutical Grade), By Type (Dry Picric Acid, Wet Picric Acid), By Purity (95%, 98%, 99%), By Moisture Content (Dry/Dehydrated, Less than 30%, More than 30%), By Application (Explosives, Antiseptic, Energetic Materials, Liquefied Gas Fuels, Thin Films, Power Generation, Others), By End User (Defence/Ballistics, Pharmaceuticals, Agrochemicals, Textile, Mining, Others), By Sales Channel (Direct Sales, Indirect Sales) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA |

| Competitive Landscape | BASF SE, DowDuPont Inc., Innospec, Odyssey Organics, Aadhunik Industries, Anmol Chemicals, Hefei TNJ Chemical Industry Co.; Ltd., Spectrum Chemicals, Loba Chemie Fine, Merck KGaA, Ricca Chemical Company, Mubychem Group, Chemours, FINORIC LLC, Lanxess, Anmol Chemicals Group, Shell, Biobor |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |