Quick Navigation

Report Overview

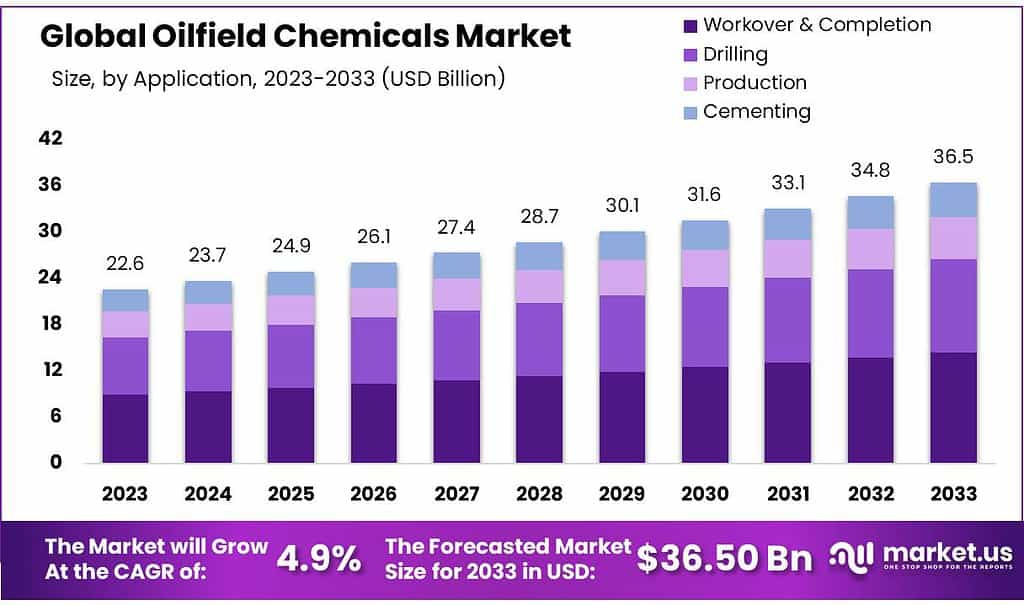

The global Oilfield Chemicals Market size is expected to be worth around USD 36.5 billion by 2033, from USD 22.6 billion in 2023, growing at a CAGR of 4.9% during the forecast period from 2023 to 2033.

The Oilfield Chemicals Market is a pivotal sector focused on producing chemicals crucial for optimizing the drilling, production, and maintenance processes in oil wells. These chemicals, including corrosion inhibitors, scale inhibitors, biocides, and demulsifiers, play essential roles in addressing challenges such as corrosion, scale formation, microbial growth, and oil-water emulsion in fields. The market’s dynamics are significantly shaped by factors like crude oil demand, advancements in extraction technologies, and stringent environmental regulations.

Regulatory frameworks and government initiatives greatly influence the adoption and innovation of oilfield chemicals. For example, the U.S. Environmental Protection Agency (EPA) enforces regulations promoting the shift towards environmentally friendly chemicals in the oil and gas industry. These measures aim to minimize pollution and protect ecosystems, encouraging the industry to adopt green chemicals.

Additionally, initiatives by entities such as the U.S. Department of Energy support enhancing oil and natural gas production from resources like shale. These efforts not only fulfill energy independence goals but also boost the demand for specialized chemicals used in processes like hydraulic fracturing.

In 2023, the U.S. government’s financial strategies included allocating over $600 million for research and development in energy-efficient and sustainable extraction technologies. This funding supports the creation of advanced chemical solutions that meet both efficacy and environmental standards, highlighting the government’s role in catalyzing industry growth and sustainability.

Key Takeaways

- The global Oilfield Chemicals Market is expected to grow from USD 22.6 billion in 2023 to USD 36.5 billion by 2033, with a CAGR of 4.9% during the forecast period.

- Rheology Modifiers held a dominant market position in the Oilfield Chemicals Market, capturing more than a 24.6% share.

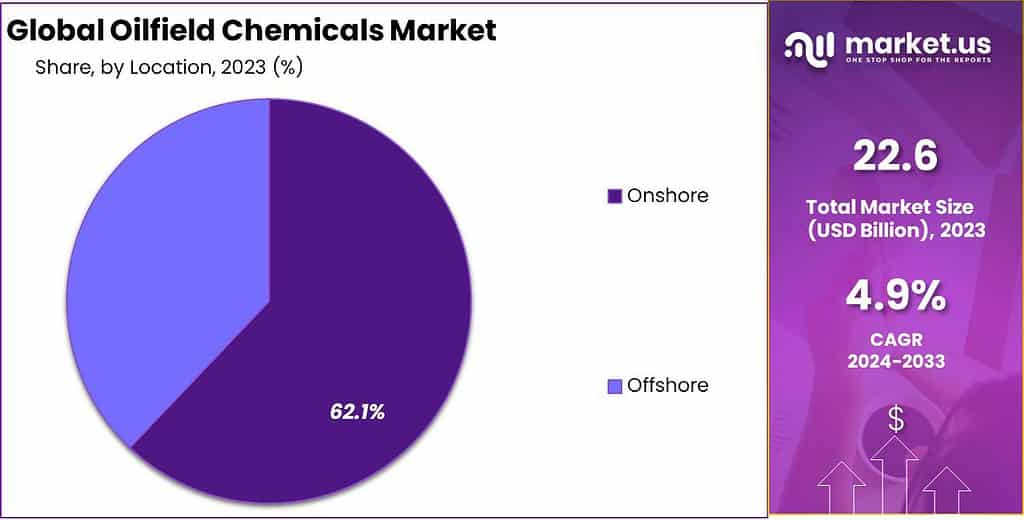

- Onshore Dominance: Onshore locations held a 62.1% market share in 2023, favored for their lower development costs compared to offshore fields.

- Workover & Completion: This segment captured 39.7% market share in 2023, focusing on chemicals for well preparation and maintenance to optimize production.

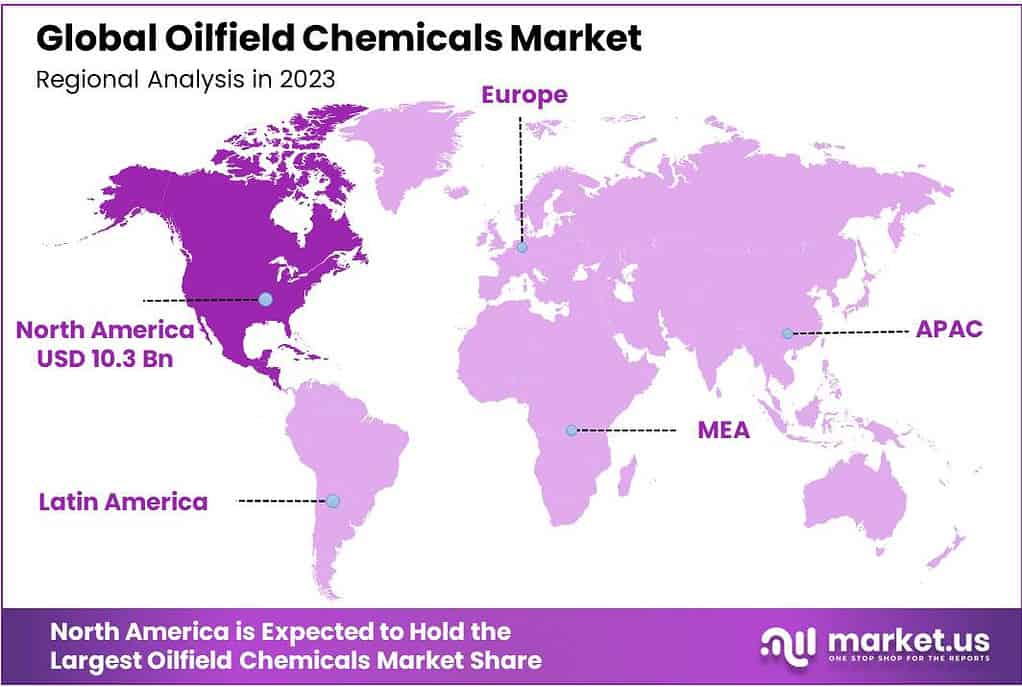

- North America Leads: North America, with a 45.6% share and valued at USD 10.30 billion in 2023, dominates due to advanced infrastructure and shale reserves.

By Product

In 2023, Rheology Modifiers held a dominant market position in the Oilfield Chemicals Market, capturing more than a 24.6% share. These products are crucial for enhancing the viscosity of drilling fluids, which improves the efficiency and stability of drilling operations. They are particularly valued for their ability to maintain the integrity of the fluid’s properties under the high-pressure and temperature conditions encountered during drilling.

Following closely are Corrosion Inhibitors, which are essential in preventing the degradation of metal equipment and pipelines exposed to corrosive substances in oilfields. These chemicals help extend the life of costly infrastructure and reduce maintenance needs, making them a vital component of oilfield operations.

Demulsifiers also play a significant role by effectively separating oil and water emulsions, a common occurrence in oil production. Their ability to enhance the quality of oil and facilitate easier processing makes them indispensable in the sector.

Friction Reducers are used to decrease the resistance encountered during fluid pumping through pipelines, enhancing flow and reducing the energy required for fluid transport. This not only optimizes production but also lowers operational costs.

Biocides protect against microbial growth that can cause bio-corrosion and fouling, ensuring the smooth operation of oilfield equipment and the prevention of production stoppages.

Surfactants contribute by lowering the surface tension between liquids, aiding in the efficient removal of oil from reservoir rocks, which improves extraction rates and recovery efficiency.

Foamers are another key product type, used to increase the lifting capacity of gases and liquids, which is particularly useful in cleaning out wells and improving production.

By Location

In 2023, Onshore locations held a dominant market position in the Oilfield Chemicals Market, capturing more than a 62.1% share. This prominence is due to the extensive and accessible nature of onshore oilfields, which are easier and less costly to develop compared to offshore fields. The chemicals used in these settings are crucial for optimizing the extraction and processing of oil and gas, enhancing production efficiency, and ensuring the longevity of the equipment through corrosion protection and scale inhibition.

Conversely, the Offshore segment, while smaller in market share, is marked by higher product demand per site due to the challenging and corrosive marine environment. Offshore operations require specialized oilfield chemicals that can withstand extreme pressures and temperatures, and combat the unique issues of saltwater corrosion and biofouling. The demand in this segment is driven by the need for highly effective biocides, corrosion inhibitors, and demulsifiers that ensure the smooth operation of equipment and pipelines situated in deep-water locations.

Both segments are integral to the global energy supply chain, with onshore activities providing a substantial volume of oil and gas and offshore fields offering access to untapped reserves in increasingly remote areas. The development and use of advanced chemical solutions in both settings are essential for meeting the world’s growing energy demands efficiently and sustainably.

By Application

In 2023, Workover & Completion held a dominant market position in the Oilfield Chemicals Market, capturing more than a 39.7% share. This segment focuses on chemicals used in the final stages of preparing a well for production or the procedures involved in repairing and enhancing existing wells. The high demand within this category is driven by the need for efficient stimulation and maintenance, ensuring optimal production levels and extending the operational life of wells.

Following closely is the Drilling segment, which utilizes specialized chemicals like drilling muds and fluids that are essential for lubricating, cooling, and supporting the drill bit and shaft during the drilling process. These chemicals are critical for maintaining bore stability and preventing blowouts, thereby ensuring safety and efficiency in complex drilling operations.

The Production segment also plays a crucial role, using oilfield chemicals to enhance the extraction of oil and gas. Chemicals in this category help optimize the flow and separation of oil, gas, and water, reduce viscosity, and prevent scale and corrosion, which are vital for maintaining uninterrupted production and reducing operational downtime.

Key Market Segments

By Product

- Inhibitors

- Demulsifiers

- Rheology Modifiers

- Friction Reducers

- Biocides

- Surfactants

- Foamers

- Others

By Location

- Onshore

- Offshore

By Application

- Workover & Completion

- Drilling

- Production

- Cementing

Drivers

The Synergistic Impact of Shale Gas Exploration, Fuel Demand, and Technological Innovations on the Oilfield Chemicals Market

The Oilfield Chemicals Market is increasing shale gas exploration and production, rising demand for petroleum-based fuels, and technological advancements in drilling and extraction. These factors not only foster market expansion independently but also create a synergistic effect that accelerates growth.

Increased Shale Gas Exploration and Production: The surge in shale gas projects, especially in North America, has been a significant driver. As these projects expand, the demand for specialized chemicals that facilitate efficient hydraulic fracturing and safe drilling operations increases. The chemicals used in these processes, such as biocides and friction reducers, are essential for optimizing production and minimizing environmental impact.

Rising Demand for Petroleum-Based Fuels: This demand, particularly from the transportation and industrial sectors, directly correlates with increased oil and gas extraction activities. As global economies grow and the need for energy escalates, the oilfield chemicals market benefits from heightened exploration activities aimed at meeting these energy demands.

Technological Advancements in Drilling and Extraction: Innovations in technology have revolutionized drilling and extraction processes, making them more efficient and less environmentally damaging. Advanced chemicals that enhance the efficacy of these processes are increasingly in demand. These advancements not only improve operational efficiency but also help in adhering to stringent environmental regulations by reducing hazardous emissions and optimizing resource use.

Restraints

The Impact of Environmental Regulations and Oil Price Volatility on the Oilfield Chemicals Market

The oilfield chemicals market faces significant challenges from two main fronts: stringent environmental regulations and the volatility of oil prices. These factors not only shape the operational strategies of companies within this industry but also influence the overall market trajectory, affecting innovation, cost, and demand dynamics.

Environmental Regulations

A Double-Edged Sword Environmental regulations are increasingly stringent in the oilfield sector, driven by global initiatives to reduce environmental footprints and combat climate change. These regulations mandate the use of environmentally safer chemicals, which are often more expensive to develop and implement.

For instance, the restrictions on volatile organic compounds (VOCs) and sulfates necessitate the reformulation of traditional products, driving research and development costs up. However, these regulations also open up opportunities for innovation in green chemical solutions. Companies are compelled to create biodegradable and less toxic formulations, leading to the emergence of new products that can command premium pricing and open new market segments.

Volatility in Oil Prices

A Catalyst for Uncertainty The volatility of oil prices directly impacts the oilfield chemicals market. High oil prices typically increase drilling and production activities, boosting the demand for oilfield chemicals. Conversely, low oil prices can lead to a reduction in exploration and production activities as oil companies cut costs, leading to a decreased demand for chemicals.

This price sensitivity introduces significant uncertainty in the market, affecting the planning and stock management strategies of chemical providers. For instance, during periods of low oil prices, there may be an oversupply of certain chemicals, leading to decreased prices and profit margins for manufacturers.

The intertwined effects of these factors create a complex market environment. On one hand, environmental regulations push for higher standards and cleaner operations, which drive innovation and can lead to market growth in the green segment.

On the other hand, the erratic nature of oil prices can cause market contractions and expansions, often unpredictably. Companies operating in this space must navigate these challenges carefully, leveraging periods of high oil prices to buffer against slower times and investing in sustainable product development to align with regulatory trends and consumer expectations.

Opportunity

Seizing Growth through Sustainability and Global Expansion in the Oilfield Chemicals Market

The oilfield chemicals market is poised for substantial growth, fueled by two primary factors: the development of eco-friendly chemicals and expansion into emerging markets. These elements are reshaping the landscape of the industry, catering to both evolving regulatory standards and the geographical diversification of market activities.

Development of Eco-Friendly Chemicals

Pioneering Sustainability in Oil Exploration The shift towards eco-friendly chemicals in the oilfield sector represents a significant transformation, driven by stringent environmental regulations and a growing corporate commitment to sustainability.

Regulatory bodies worldwide, such as the EPA in the United States and similar entities in Europe, have imposed tight restrictions on the environmental impact of oilfield operations, particularly focusing on reducing emissions and aquatic toxicity associated with chemical spills and leaks.

This regulatory landscape has created a fertile ground for innovation, pushing companies to develop chemicals that are not only effective but also minimize ecological footprints. The market for green oilfield chemicals is expanding as these innovations prove they can meet or even exceed the performance of traditional products.

For instance, the development of biodegradable surfactants and non-toxic corrosion inhibitors has opened new doors for compliance with environmental laws and corporate sustainability goals. Companies investing in these technologies are not only aligning with current regulatory demands but are also positioning themselves as leaders in a future where such standards are likely to become even more stringent.

Expansion in Emerging Markets

Tapping into New Frontiers Emerging markets represent a critical growth avenue for the oilfield chemicals industry. Regions such as Asia-Pacific, Latin America, and parts of Africa are experiencing rapid industrialization and urbanization, leading to increased energy demands. Countries like China, India, and Brazil are investing heavily in their oil and gas infrastructure, which in turn drives the demand for oilfield chemicals needed for both conventional and unconventional extraction methods.

The expansion into these markets is not just about selling existing products but also adapting offerings to meet local conditions such as varying types of oil reservoirs and environmental challenges. The growth in these regions is supported by local governments eager to harness their natural resources more effectively, often providing incentives for foreign investment in oil and gas production.

Moreover, companies that are early entrants into these markets can establish strong relationships with local industries and governments, creating barriers to entry for later competitors and setting standards with their eco-friendly innovations. This strategic positioning not only capitalizes on immediate opportunities but also ensures long-term profitability in a world where the energy landscape is rapidly evolving.

Trends

Growth through Sustainability, Technological Integration, and Geographical Expansion

The oilfield chemicals market is experiencing transformative growth, shaped by several forward-looking trends that address both operational efficiency and environmental responsibility. These trends include the increased use of biodegradable oilfield chemicals, expansion into emerging markets, and the integration of IoT and automation technologies in oilfield operations.

Increased Use of Biodegradable Oilfield Chemicals

A Green Revolution The shift towards biodegradable oilfield chemicals is a response to heightened global environmental awareness and stricter regulations that demand more sustainable practices in the oil and gas industry. This trend is significantly influencing market growth as industry players seek to reduce their ecological footprints while maintaining operational efficiency.

Biodegradable chemicals minimize the long-term impact on the ecosystems where drilling operations occur, reducing pollution and potential legal and cleanup costs associated with spills or leaks. Companies investing in these green solutions are not only complying with global standards but are also appealing to environmentally conscious stakeholders and investors, enhancing their brand reputation and competitive edge.

Expansion in Emerging Markets

Accessing New Frontiers Emerging markets represent a lucrative growth opportunity for the oilfield chemicals industry due to their increasing energy demands driven by rapid industrialization and urbanization. Countries in regions such as Asia-Pacific, Latin America, and Africa are seeing significant increases in oil and gas exploration activities.

This expansion is supported by local governments that are keen on developing their energy resources to fuel economic growth, offering incentives and support for foreign investments. Companies that can navigate these markets effectively are finding not only new customers but also opportunities to establish local production facilities to reduce logistics costs and increase market responsiveness.

Integration of IoT and Automation in Oilfield Operations

Enhancing Efficiency and Safety The integration of IoT and automation technologies into oilfield operations marks a pivotal trend in the industry, aimed at boosting operational efficiency and safety. IoT devices and automation systems enable real-time monitoring and management of oilfield operations, providing critical data that can be used to optimize chemical usage, monitor equipment health, and predict maintenance needs.

This technological integration helps reduce downtime and operational costs while improving the accuracy and efficiency of chemical treatments. The data collected through these technologies also supports better decision-making and can lead to the development of new, more effective chemical formulations.

Regional Analysis

In the global Oilfield Chemicals Market, North America emerges as a dominant force with a substantial market share of 45.6%, valued at USD 10.30 billion. This region’s leadership is underscored by its advanced oil and gas infrastructure, extensive shale oil reserves, and significant investments in unconventional drilling techniques.

The presence of major oilfield services companies and technological advancements in hydraulic fracturing (“fracking”) contribute to North America’s robust demand for oilfield chemicals. Key products such as drilling fluids, corrosion inhibitors, and biocides are in high demand here, driven by the expansive operations in the United States and Canada.

Europe follows with a notable market presence, supported by mature oilfields in the North Sea and ongoing exploration activities in Eastern Europe. The region benefits from stringent environmental regulations that drive demand for eco-friendly and efficient chemical solutions in oil and gas extraction processes. Market growth in Europe is also fueled by increasing offshore drilling activities and the adoption of enhanced oil recovery (EOR) techniques.

Asia Pacific (APAC) emerges as a significant growth region, driven by rapid industrialization and urbanization in countries like China and India. APAC’s oilfield chemicals market is propelled by expanding energy demand, substantial investments in upstream activities, and government initiatives to boost domestic oil production. Moreover, technological advancements and increasing exploration efforts in Southeast Asia contribute to the region’s expanding market share.

The Middle East & Africa (MEA) region showcases strong potential, supported by vast hydrocarbon reserves and ongoing investments in oilfield infrastructure. Countries like Saudi Arabia, UAE, and Nigeria are key contributors to the market, leveraging advanced drilling technologies and substantial reserves to drive demand for specialized chemicals that enhance extraction efficiency and operational safety.

Latin America, characterized by major oil producers like Brazil and Venezuela, also plays a crucial role in the global oilfield chemicals market. The region benefits from extensive offshore reserves and significant investments in deepwater drilling projects. Despite challenges such as political instability and environmental concerns, Latin America continues to attract investments in oilfield operations, stimulating demand for chemicals that optimize production and ensure sustainable resource utilization.

Key Regions and Countries

- North America

- The US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia & CIS

- Rest of Europe

- APAC

- China

- Japan

- South Korea

- India

- ASEAN

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

The global Oilfield Chemicals Market features a competitive landscape shaped by key players known for their extensive contributions and technological innovations. DowDuPont Inc. stands out with a diverse portfolio of chemicals essential for drilling, production, and reservoir stimulation.

BASF SE, another major player, leverages its expertise in chemical solutions across various industries to offer tailored products for oilfield applications. Halliburton Co. and Schlumberger Limited are prominent service providers offering integrated solutions that include oilfield chemicals, equipment, and services, enhancing operational efficiency and productivity in oil and gas extraction.

Companies like Albemarle Corporation and Akzo Nobel N.V. specialize in providing additives and specialty chemicals critical for optimizing oilfield operations. Baker Hughes, a GE Company LLC, and Chevron Phillips Chemical Company LLC. are recognized for their comprehensive offerings in drilling fluids, completion chemicals, and production chemicals, catering to diverse operational needs in the oilfield sector.

Ashland Inc., Solvay SA, and Clariant AG contribute with their expertise in specialty chemicals and additives, supporting enhanced performance and sustainability in oil and gas operations.

Additionally, Flotek Industries, Inc., Innospec Incorporated, and GEO Drilling Fluids, Inc. play pivotal roles with their specialized solutions, focusing on innovation and technological advancements to meet evolving industry requirements.

Market Key Players

- DowDuPont Inc.

- BASF SE

- Halliburton Co.

- Albemarle Corporation

- Akzo Nobel N.V.

- Schlumberger Limited

- Baker Hughes, a GE Company LLC

- Chevron Phillips Chemical Company LLC.

- Ashland Inc.

- Solvay SA

- Clariant AG

- Flotek Industries, Inc.

- Innospec Incorporated

- GEO Drilling Fluids, Inc

Recent Development

By December 2023, DowDuPont reported a revenue increase of 12%, reaching USD 2.5 billion, underscoring its commitment to sustainable growth and technological leadership in the competitive oilfield chemicals market.

By December 2023, BASF SE reported a revenue growth of 10%, reaching USD 2.2 billion, underscoring its commitment to driving innovation and sustainability in the competitive oilfield chemicals landscape.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2023) | US$ 22.6 Bn |

| Forecast Revenue (2033) | US$ 36.5 Bn |

| CAGR (2024-2033) | 4.9% |

| Base Year for Estimation | 2023 |

| Historic Period | 2020-2022 |

| Forecast Period | 2024-2033 |

| Report Coverage | Revenue Forecast, Market Dynamics, COVID-19 Impact, Competitive Landscape, Recent Developments |

| Segments Covered | By Product(Inhibitors, Demulsifiers, Rheology Modifiers, Friction Reducers, Biocides, Surfactants, Foamers, Others), By Location(Onshore, Offshore), By Application(Workover and Completion, Drilling, Production, Cementing) |

| Regional Analysis | North America – The US & Canada; Europe – Germany, France, The UK, Spain, Italy, Russia & CIS, Rest of Europe; APAC– China, Japan, South Korea, India, ASEAN & Rest of APAC; Latin America– Brazil, Mexico & Rest of Latin America; Middle East & Africa– GCC, South Africa, & Rest of MEA |

| Competitive Landscape | DowDuPont Inc., BASF SE, Halliburton Co., Albemarle Corporation, Akzo Nobel N.V., Schlumberger Limited, Baker Hughes, a GE Company LLC, Chevron Phillips Chemical Company LLC., Ashland Inc., Solvay SA, Clariant AG, Flotek Industries, Inc., Innospec Incorporated, GEO Drilling Fluids, Inc |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |

Frequently Asked Questions (FAQ)

Oilfield Chemicals Market size is expected to be worth around USD 36.5 billion by 2033, from USD 22.6 billion in 2023

DowDuPont Inc., BASF SE, Halliburton Co., Albemarle Corporation, Akzo Nobel N.V., Schlumberger Limited, Baker Hughes, a GE Company LLC, Chevron Phillips Chemical Company LLC., Ashland Inc., Solvay SA, Clariant AG, Flotek Industries, Inc., Innospec Incorporated, GEO Drilling Fluids, Inc