Global Perfluorosulfonic Acid (PFSA) Membranes for Fuel Cell Market Size, Share, And Business Benefits By Thickness (Below 20 Microns, 20 to 50 Microns, 50 to 150 Microns, Above 150 Microns), By Application (Passenger Vehicle, Commercial Vehicle, Others), By Region and Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Trends, and Forecast 2025-2034

- Published date: November 2025

- Report ID: 165993

- Number of Pages: 274

- Format:

-

keyboard_arrow_up

Quick Navigation

Report Overview

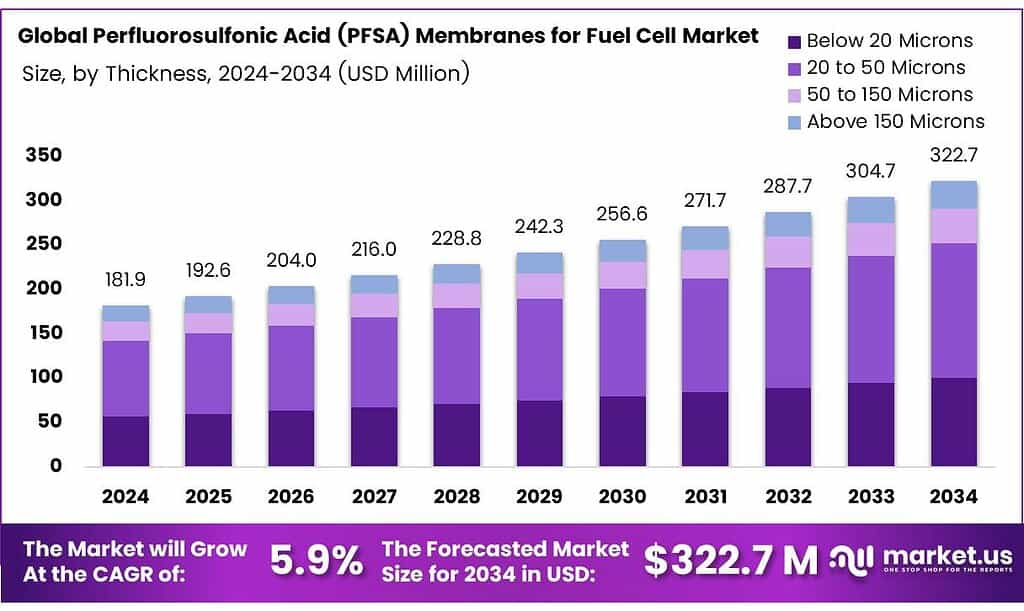

The Global Perfluorosulfonic Acid (PFSA) Membranes for Fuel Cell Market size is expected to be worth around USD 322.7 Million by 2034, from USD 181.9 Million in 2024, growing at a CAGR of 5.9% during the forecast period from 2025 to 2034.

Perfluorosulfonic acid (PFSA) membranes are widely recognized for their high mechanical stability, excellent chemical inertness, good thermal stability, and high proton conductivity, making them the material of choice for proton exchange membrane fuel cells (PEMFCs), particularly in automotive applications. The demand for PEMFC membranes capable of operating reliably at temperatures around 120 °C has grown significantly in the automotive sector.

This push is driven by the desire for higher efficiency, better tolerance to impurities (e.g., CO in reformate), and overall system simplification, including the ability to operate with little or no humidification of reactant gases. Conventional Nafion membranes, the most prominent PFSA example, begin to lose mechanical integrity above 100 °C and suffer drastic drops in proton conductivity when dehydrated.

- The proton conductivity of Nafion is highly dependent on its water content (expressed as the number of water molecules per sulfonic acid group, λ). For instance, at λ 22, conductivity can reach approximately 0.15 S cm⁻¹, but it drops sharply to around 0.06 S cm⁻¹ when λ decreases to 14. To maintain adequate hydration and conductivity, Nafion-based PEMFCs are typically restricted to operating temperatures below 100 °C.

Operating at such low temperatures, however, brings its own challenges, including cathode flooding due to excess liquid water and poorer heat rejection. These limitations highlight the clear need for proton-exchange membranes that can perform effectively above 100 °C under low-humidity conditions. Despite extensive research, very few high-temperature PEMFC systems have reached commercial maturity.

Membrane materials for fuel cells are generally classified into five main categories: perfluorinated ionomers, partially fluorinated polymers, non-fluorinated membranes with aromatic hydrocarbon backbones (sulfonated polyether ether ketone), non-fluorinated hydrocarbon polymers, and acid–base blends. Among these, perfluorosulfonic acid (PFSA) polymers remain the most commonly used and benchmark materials for PEMFC membranes due to their outstanding combination of chemical stability and proton-conducting performance under fully humidified conditions.

Key Takeaways

- The PFSA Membranes Market is projected to reach USD 322.7 million by 2034, rising from USD 181.9 million in 2024, at a CAGR of 5.9% during 2025–2034.

- In thickness segmentation, 20 to 50 Microns led with 47.2% share in 2024.

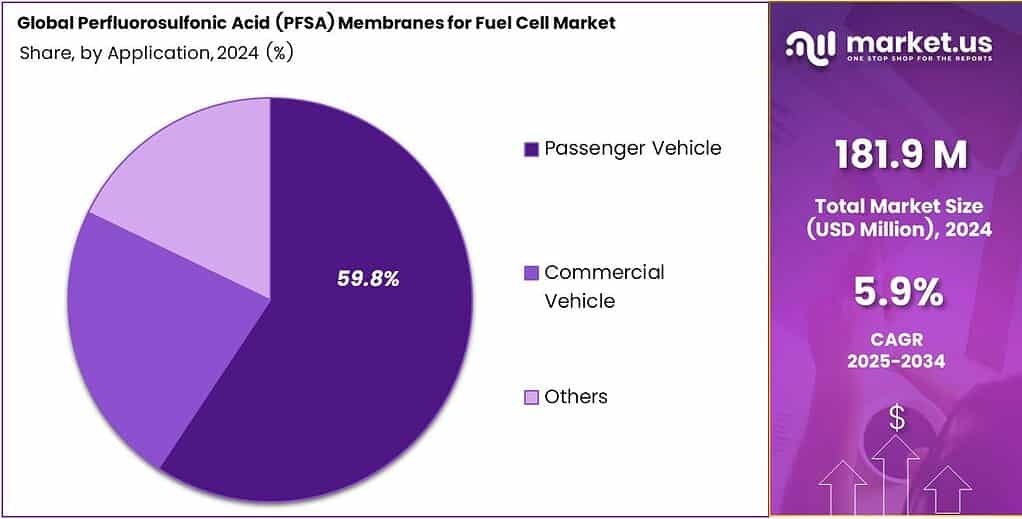

- In application segmentation, Passenger Vehicle dominated with a 59.8% share in 2024.

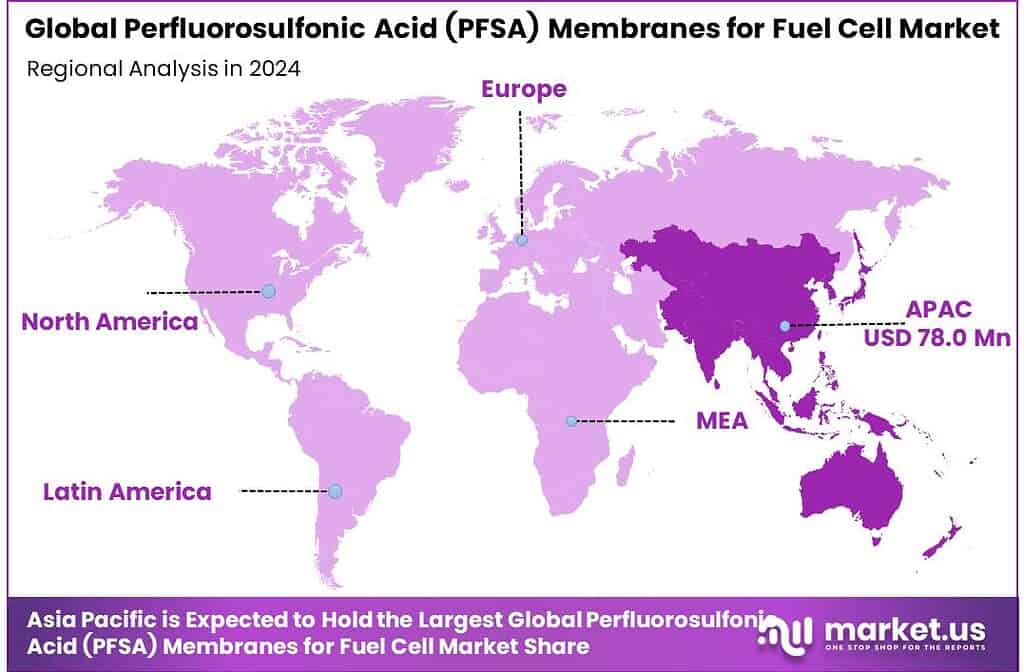

- Asia-Pacific was the leading region with 42.9% market share, valued at USD 78.0 million.

By Thickness Analysis

20 to 50 Microns dominate with 47.2% due to balanced durability and proton conductivity.

In 2024, 20 to 50 Microns held a dominant market position in the By Thickness Analysis segment of Perfluorosulfonic Acid (PFSA) Membranes for Fuel Cell Market, with a 47.2% share. This thickness range provides a stable balance between mechanical strength and ionic transmission, helping improve fuel cell lifespan and efficiency across multiple vehicle formats, boosting user confidence and adoption.

Below 20 Microns gained traction due to its lightweight structure and potential energy efficiency improvements. This thinner membrane targets advanced vehicle engineering where compact cell construction matters. However, durability challenges and chemical resistance limitations compared to mid-range thickness products slow down wider commercialization, but research collaborations continue for enhancing performance.

50 to 150 Microns focuses on heavy-duty reliability, offering higher mechanical stability and longer operating cycles in harsh vibration and temperature environments. This segment suits commercial and high-load systems where membrane replacement cost and serviceable life are critical. Even though thicker materials slightly lower proton exchange speed, they support long-term operational dependability.

Above 150 Microns remains a niche area serving specialized and experimental systems where extreme durability outweighs efficiency curves. It attracts interest from prototype developers focusing on long-range and high-load energy storage integrations. Manufacturers continue evaluating industrial fitment, but adoption remains low due to limited scalability and lower conductivity rates.

By Application Analysis

Passenger Vehicle dominates with 59.8% backed by rising urban clean-mobility adoption.

In 2024, Passenger Vehicle held a dominant market position in the By Application Analysis segment of Perfluorosulfonic Acid (PFSA) Membranes for Fuel Cell Market, with a 59.8% share. Demand rose due to clean mobility choices, government incentives, and interest in zero-emission personal transport. PFSA membranes support compact integration, fast response, and long cycle reliability.

Commercial Vehicle usage expanded gradually as industries explored hydrogen-powered fleets for logistics, buses, and municipal transport. PFSA membranes help achieve consistent high-load power delivery necessary for long-distance and continuous-use vehicles. Deployment improves fleet sustainability plans, and ongoing pilot projects shape long-term scaling prospects.

The other category covers research, defense, material testing, and customized fuel cell platforms. Adoption remains smaller but innovative, driven by technological experimentation and feasibility validation projects. These users leverage PFSA for training prototypes and next-phase industrial exploration, helping strengthen future application diversification.

Key Market Segments

By Thickness

- Below 20 Microns

- 20 to 50 Microns

- 50 to 150 Microns

- Above 150 Microns

By Application

- Passenger Vehicle

- Commercial Vehicle

- Others

Emerging Trends

Hydrogen Mobility Surge is Reshaping PFSA Fuel Cell Membranes

A clear emerging trend for Perfluorosulfonic Acid (PFSA) membranes is their rapid shift from niche lab material to a workhorse of hydrogen mobility and large-scale clean-energy projects. Governments are putting real numbers behind hydrogen plans, and every fuel cell stack in these projects relies on high-performance proton-exchange membranes, where PFSA is still the reference material.

- The European Union’s Hydrogen Strategy, for example, targets 40 GW of renewable hydrogen electrolysers and 10 million tonnes of renewable hydrogen production. These goals are written into EU policy under the Green Deal and REPowerEU frameworks, signalling long-term demand for PEM fuel cells and related PFSA membranes in industry and transport.

The International Energy Agency (IEA) estimates that, if announced projects proceed, installed electrolyser capacity could reach 230–520 GW, up from about 1.4 GW. These PEM-based systems use PFSA membranes very similar to those in fuel cells, so scaling green hydrogen production directly supports higher PFSA demand and encourages innovation in thinner, more durable, and higher-temperature grades.

Drivers

Rising Government-Backed Hydrogen Infrastructure Fuels PFSA Membrane Demand

One key driving factor for the increased demand for perfluorosulfonic acid (PFSA) membranes is the strong push by governments to build hydrogen fuel-cell ecosystems, especially hydrogen refuelling infrastructure and clean-hydrogen production hubs. In the United States, the U.S. Department of Energy (DOE) reports there are 54 publicly accessible hydrogen refuelling stations as of 2024, with more than 20 in planning or construction stages.

- These hydrogen stations are crucial because vehicles powered by proton exchange membrane fuel cells (PEMFCs) — which rely on PFSA membranes — require frequent hydrogen refuelling and will only scale if the infrastructure is present. The DOE also supports a Regional Clean Hydrogen Hubs initiative, backed by roughly USD 7 billion in funding, to create networks for clean-hydrogen production, storage, and distribution in a number of U.S. regions.

In parallel, states like California are deploying fuel-cell buses: for example, the Center for Transportation and the Environment and partner agencies under the ARCHES clean hydrogen hub scheme aim to deploy over 1,000 fuel-cell electric buses (FCEBs) across 13 transit agencies in the next 5-8 years.

Restraints

Regulatory Pressure on PFSA Membranes

One major restraint for the adoption of perfluorosulfonic acid (PFSA) membranes in fuel cells is the tightening regulatory environment around fluorochemicals, especially those in the broader PFAS (per- and polyfluoroalkyl substances) family. In the European Union, the European Chemicals Agency (ECHA) has issued a draft restriction covering all non-essential uses of PFAS.

This means that manufacturers of PFSA membranes, which rely on fluoropolymer chemistries, are facing heightened uncertainty about long-term raw material access, compliance costs, potential reformulation, and supply-chain disruption. For example, the restriction dossier notes that fluoropolymer supply chains may need to adapt, and lead times may increase.

From a cost perspective, older studies and industry reviews show that proton exchange membrane fuel cell (PEMFC) systems, of which PFSA membranes are a critical component, already had high cost hurdles. One technical cost analysis indicated that PEMFC module costs were near USD 200 kW⁻¹.

Opportunity

Transition of the Food Sector to Zero-Emission Logistics

A key growth factor for perfluorosulfonic acid (PFSA) membranes in fuel cells is the accelerating push within the food and agrifood supply chain to decarbonise logistics and support infrastructure. The food-system lens is especially relevant because agrifood systems are estimated to account for about one-third of total anthropogenic greenhouse-gas emissions.

To meet their net-zero commitments, many large food organisations and supply-chain participants are exploring fuel-cell electric vehicles (FCEVs) for trucking, onsite fuel-cell backup power, and clean-hydrogen supply. Because FCEVs frequently rely on proton-exchange-membrane fuel cells (PEMFCs), the demand for high-performance PFSA membranes rises in step with this transition.

- From a numbers perspective, the global demand for hydrogen reached 97 million tonnes (Mt), up by 2.5%. While much of that hydrogen today serves refining and chemicals, its expansion into logistics and transport (including food-chain use-cases) signals a broader shift. Governments are introducing frameworks to scale hydrogen-fuelled logistics, which in turn drives the upstream components such as PFSA membranes.

Regional Analysis

Asia-Pacific Dominates the PFSA Membranes for Fuel Cell Market with a Market Share of 42.9%, Valued at USD 78.0 Million

In the Asia-Pacific region, the adoption of fuel cell vehicles, stationary clean energy systems, and government-backed hydrogen transition programs has accelerated demand for premium membrane materials. The region’s share of 42.9% and value of USD 78.0 Million reflect stronger manufacturing bases, technology localization, and rising infrastructure investments.

North America is gaining steady traction driven by clean mobility pilots, steady scale-up of hydrogen fueling networks, and research-focused advancements in membrane durability. Strategic support for decarbonization and clean power models enhances technology commercialization. Demand is increasing for heavy-duty transport and aerospace applications.

Europe remains an active participant with policy-driven hydrogen economy frameworks, particularly around industrial energy reuse, maritime technology, and carbon-neutral industrial clusters. The region focuses on advanced membrane performance, circular production methodologies, and integration with renewable electrolysis platforms.

The Middle East & Africa region is witnessing preliminary adoption led by national hydrogen roadmaps and energy diversification programs, especially within Gulf Cooperation Council countries. Fuel cell technology is gaining visibility in long-term carbon neutrality plans supported by domestically available renewable energy sources.

The U.S. demonstrates notable interest through federal innovation grants, defense-aligned energy storage applications, and clean trucking transition agendas. Public-private innovation centers are promoting PFSA membrane efficiency, lifespan improvements, and next-gen clean fuel system integration.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Perfluorosulfonic Acid (PFSA) Membranes for Fuel Cell Company Insights

AGC is positioned as a key global supplier of advanced fluorochemical materials, and its PFSA membranes strategy reflects a focus on reliability and long-term partnerships with fuel cell OEMs. The company leverages its broader fluoropolymer and glass-chemistry capabilities to fine-tune membrane durability, proton conductivity, and chemical stability, helping automakers and stationary fuel cell players improve stack lifetimes and lower total cost of ownership.

Chemours remains a reference point in the PFSA membrane space, drawing on decades of ionomer and fluoropolymer expertise. In 2024, its strategy is centered on scaling high-performance membranes that can withstand demanding automotive and heavy-duty cycles, while also addressing cost and supply-security concerns for global customers. Chemours’ ability to align material development with tighter emissions rules and hydrogen roadmaps keeps it firmly embedded in next-generation fuel cell programs.

Shandong Hengyi New Material Technology Co., Ltd is an increasingly important Chinese PFSA supplier, benefiting from domestic investments in fuel cell vehicles and hydrogen infrastructure. The company focuses on offering cost-competitive membranes that meet local OEM performance benchmarks, allowing China to reduce reliance on imported materials. Its responsiveness to regional standards and fast commercialization timelines makes it a strategic partner in Asia’s hydrogen value chain.

Suzhou Thinkre New Material targets the PFSA market with a strong R&D angle, emphasizing customized membrane formulations for specific fuel cell architectures and operating conditions. By working closely with stack integrators, the firm aims to balance conductivity, mechanical strength, and chemical resistance for both mobility and stationary uses. This application-driven approach positions Suzhou Thinkre as a flexible, innovation-oriented player in a market that increasingly values tailored PFSA solutions.

Top Key Players in the Market

- AGC

- Chemours

- Shandong Hengyi New Material Technology Co., Ltd

- Suzhou Thinkre New Material

- ULTRANANOTECH PRIVATE Ltd

- Vritra Technologies

- Others

Recent Developments

- In 2024, Nissan Chemical’s website, under their Energy Materials Development Gr., they are developing PFAS-free ionomers for the catalyst layers of water electrolysis and fuel cell devices. This indicates the company is active in the hydrogen/fuel-cell materials space and is explicitly moving away from PFAS compounds to PFAS-free ionomers.

- In 2025, Croda Beauty (a division of Croda) announced that it already offers PFAS-free peptides and has committed to transitioning its entire peptide range to PFAS-free status. They explicitly cite the elimination of substances like trifluoroacetic acid (TFA) from their peptide synthesis process.

Report Scope

Report Features Description Market Value (2024) USD 181.9 Million Forecast Revenue (2034) USD 322.7 Million CAGR (2025-2034) 5.9% Base Year for Estimation 2024 Historic Period 2020-2023 Forecast Period 2025-2034 Report Coverage Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments Segments Covered By Thickness (Below 20 Microns, 20 to 50 Microns, 50 to 150 Microns, Above 150 Microns), By Application (Passenger Vehicle, Commercial Vehicle, Others) Regional Analysis North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East & Africa (GCC, South Africa, and Rest of MEA) Competitive Landscape AGC, Chemours, Shandong Hengyi New Material Technology Co., Ltd, Suzhou Thinkre New Material, ULTRANANOTECH PRIVATE Ltd, Vritra Technologies, Others Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited Users and Printable PDF)  Membranes for Fuel Cell Market") Perfluorosulfonic Acid (PFSA) Membranes for Fuel Cell MarketPublished date: November 2025add_shopping_cartBuy Now get_appDownload Sample

Perfluorosulfonic Acid (PFSA) Membranes for Fuel Cell MarketPublished date: November 2025add_shopping_cartBuy Now get_appDownload Sample -

-

- AGC

- Chemours

- Shandong Hengyi New Material Technology Co., Ltd

- Suzhou Thinkre New Material

- ULTRANANOTECH PRIVATE Ltd

- Vritra Technologies

- Others

Our Clients

- 165993

- November 2025