Quick Navigation

- Report Overview

- Key Takeaways

- Business Benefits of Aluminium Conductors

- By Type Analysis

- By Capacity Analysis

- By Voltage Level Analysis

- By Application Analysis

- By End-Use Analysis

- Key Market Segments

- Driving Factors

- Restraining Factors

- Growth Opportunity

- Latest Trends

- Regional Analysis

- Key Players Analysis

- Recent Developments

- Report Scope

Report Overview

The Global Aluminium Conductors Market is expected to be worth around USD 78.8 Billion by 2033, up from USD 43.6 Billion in 2023, and grow at a CAGR of 6.1% from 2024 to 2033. Asia-Pacific holds 51.4% share, valued at USD 22.4 billion.

Aluminium conductors are integral to electrical transmission and distribution networks, serving as the primary medium for conveying electricity from generation facilities to end-users. Their prominence is attributed to aluminium’s favourable properties, including high conductivity, lightweight, and corrosion resistance.

In India, the production of aluminium conductors is governed by standards such as IS 398 (Part 2):1996 and IS 398 (Part 4):1994, ensuring quality and reliability in transmission applications.

The Indian aluminium industry is robust, with major producers like National Aluminium Company Limited (NALCO), Hindalco Industries Limited, Bharat Aluminium Company Limited (BALCO), and Vedanta Aluminium Limited (VAL) leading production.

These companies have established significant capacities for manufacturing various aluminium products, including conductors. For instance, Hindalco’s Renukoot plant has a conductor redraw capacity of 56,400 tonnes per year, contributing substantially to the domestic supply of aluminium conductors.

The demand for aluminium conductors in India is closely linked to the nation’s economic growth and expanding population. As the economy develops, the need for electrical power escalates, necessitating extensive transmission and distribution infrastructure. Government initiatives aimed at rural electrification and commitments to provide electricity to every household have further propelled the demand for aluminium conductors.

The projected increase in power generation capacity to 205,000 MW by 2012 underscored the need for a substantial network of transmission and distribution systems, thereby driving the aluminium conductor market.

A notable trend in the aluminium conductor market is the emphasis on energy efficiency and technological advancements. The Bureau of Energy Efficiency (BEE) in India has implemented measures to enhance energy conservation within the aluminium sector.

During the Perform, Achieve, and Trade (PAT) Cycle-I, the aluminium sector achieved energy savings of 0.730 million tonnes of oil equivalent, surpassing the notified target by 60%. This achievement was facilitated by investments in energy conservation measures, amounting to ₹140 crore.

Looking ahead, the aluminium conductor market in India presents significant growth opportunities. The ongoing expansion of the power sector, coupled with government policies focusing on infrastructure development and electrification, is expected to sustain the demand for aluminium conductors.

Additionally, the global shift towards renewable energy sources and the integration of smart grid technologies may further augment the need for efficient and reliable transmission solutions, positioning aluminium conductors as a critical component in future energy infrastructure.

Key Takeaways

- The Global Aluminium Conductors Market is expected to be worth around USD 78.8 Billion by 2033, up from USD 43.6 Billion in 2023, and grow at a CAGR of 6.1% from 2024 to 2033.

- Aluminum Conductor Steel Reinforced (ACSR) dominates, accounting for 37.4% of the total share.

- The 200A to 750A capacity range leads, representing 44.1% of market demand.

- High Voltage applications comprise 37.1%, showcasing the market’s focus on transmission efficiency.

- Overhead transmission remains critical, securing 43.2%, reflecting robust infrastructure expansion.

- Energy and utilities drive demand, contributing 43.2%, emphasizing the sector’s reliance on conductors.

- Asia-Pacific dominates the Aluminium Conductors Market, holding 51.4%, worth USD 22.4 billion.

Business Benefits of Aluminium Conductors

Aluminium conductors offer several business benefits, particularly in the energy and utilities sector, where they play a critical role in power transmission and distribution. According to a report by the U.S. Department of Energy (DOE), aluminium conductors are highly valued for their lightweight, cost-effectiveness, and superior conductivity, making them a preferred choice for modernizing and expanding electrical grids.

These conductors enable businesses to reduce material costs while maintaining high performance over long distances, which is especially crucial in large-scale infrastructure projects.

One key benefit is their cost-efficiency. Compared to copper, aluminium conductors are less expensive, making them an attractive option for companies looking to optimize expenses in large-scale power networks. The lower weight of aluminium also translates to easier handling and installation, which reduces labour costs and speeds up construction timelines.

Aluminium conductors also support sustainability initiatives, as their use aligns with the increasing global emphasis on reducing carbon emissions. According to the International Energy Agency (IEA), using lightweight, durable materials like aluminium contributes to more efficient energy transmission, reducing overall energy loss during transportation.

Moreover, the durability and corrosion resistance of aluminium ensures long-term performance with minimal maintenance, offering businesses significant savings over the product lifecycle. These attributes make aluminium conductors an essential investment for companies focused on operational efficiency and meeting evolving energy demands.

By Type Analysis

Aluminum Conductor Steel Reinforced (ACSR) holds a 37.4% share, showcasing industry preference.

In 2023, the “By Type” segment of the Aluminium Conductors Market was led by Aluminum Conductor Steel Reinforced (ACSR), which held a dominant position with a 37.4% market share. This segment is followed by All Aluminum Alloy Conductor (AAAC) and Aluminum Conductor Aluminum-Alloy Reinforced (ACAR), underscoring a diverse range of products catering to various electrical transmission needs.

ACSR conductors are particularly valued for their high tensile strength and reliability, making them ideal for long-distance power distribution with minimal sagging. Their construction, combining aluminum’s conductivity with the robustness of steel, addresses both the need for efficiency and durability in challenging environments.

Furthermore, the adoption of AAAC is also significant due to its enhanced corrosion resistance and lighter weight compared to ACSR, which makes it suitable for coastal areas and industrial environments where corrosion could pose a problem. Meanwhile, ACAR, though less common, is gaining traction for its balanced attributes of strength and conductivity.

Together, these conductor types are pivotal in meeting the expanding demands of modern electrical infrastructure, driven by increasing electrification and renewable energy integration across global markets. Their application versatility and performance characteristics continue to influence market dynamics and technological advancements within the sector.

By Capacity Analysis

The 200A to 750A segment leads with 44.1%, meeting diverse electrical demands.

In 2023, the “By Capacity” segment of the Aluminium Conductors Market was led by the 200A to 750A range, which held a dominant market share of 44.1%. This capacity range is preferred for a wide array of medium-to-large-scale power transmission and distribution applications, offering a balance between efficiency, cost-effectiveness, and performance.

Conductors in the 200A to 750A capacity range are particularly suited for urban grids and regional distribution networks, where both high current handling and structural integrity are critical.

The “Up to 200A” segment follows, catering to smaller-scale applications such as residential power supply and low-voltage distribution systems. While this category holds a smaller market share, it is witnessing steady growth due to increasing demand for residential and commercial energy solutions.

On the higher end, the “750A and above” segment represents the most heavy-duty applications, including industrial power transmission and high-voltage networks. Although it holds a smaller share compared to the 200A to 750A range, this segment is projected to grow steadily, driven by the expansion of infrastructure in emerging markets and the demand for high-capacity transmission lines.

Overall, the By Capacity segment of the Aluminium Conductors Market is driven by diverse needs, with each range catering to specific electrical grid requirements across sectors.

By Voltage Level Analysis

High voltage applications dominate, representing 37.1% of the aluminum conductor market.

In 2023, High Voltage held a dominant market position in the By Voltage Level segment of the Aluminium Conductors Market, with a 37.1% share. This was closely followed by Medium Voltage at 29.6%, Low Voltage at 19.4%, and Extra-High Voltage at 13.9%.

High Voltage conductors are primarily used in long-distance power transmission, where energy loss needs to be minimized over vast distances. Their substantial market share can be attributed to the increasing demand for reliable electricity grids, as well as the ongoing infrastructure investments to support power generation and distribution networks in both developed and emerging economies.

Medium Voltage conductors, which cater to both urban and rural distribution systems, are witnessing growth due to the rising adoption of renewable energy sources and the expansion of electricity networks. Low Voltage conductors, though having a smaller share, play a vital role in residential and commercial electrical systems, where power distribution is localized.

Extra-High Voltage conductors, essential for ultra-long transmission lines and large-scale power grids, are growing steadily as countries focus on strengthening their energy infrastructure to meet the demand for clean and efficient power.

Overall, the Aluminium Conductors market is experiencing a shift towards higher voltage levels, driven by infrastructure development, technological advancements, and the global push for renewable energy integration.

By Application Analysis

Overhead transmission utilizes 43.2% of aluminium conductors, ensuring reliable power delivery infrastructure.

In 2023, Overhead Transmission held a dominant market position in the By Application segment of the Aluminium Conductors Market, with a 43.2% share. This was followed by Underground Cables at 28.5%, Building Wiring at 17.8%, and Automotive at 10.5%.

Overhead transmission lines continue to lead the market due to their widespread use in long-distance electricity transmission, where aluminum conductors offer a balance of cost-effectiveness, lightweight, and conductivity. These lines are particularly favoured for their ability to cover vast areas without the need for extensive infrastructure, making them ideal for both rural and urban grid expansions.

The underground cables segment is experiencing significant growth as utilities and municipalities prioritize the need for more resilient and aesthetic power distribution systems. Underground cables are less susceptible to environmental factors like storms and extreme weather, thus ensuring greater reliability and longevity, contributing to their increasing adoption.

Building wiring remains a crucial segment due to the continual construction of residential, commercial, and industrial infrastructure. Aluminium’s low cost and lightweight properties make it a preferred material for electrical wiring in these applications.

The automotive sector is also growing steadily as electric vehicles (EVs) demand efficient, lightweight wiring solutions, further driving the overall market for aluminum conductors.

By End-Use Analysis

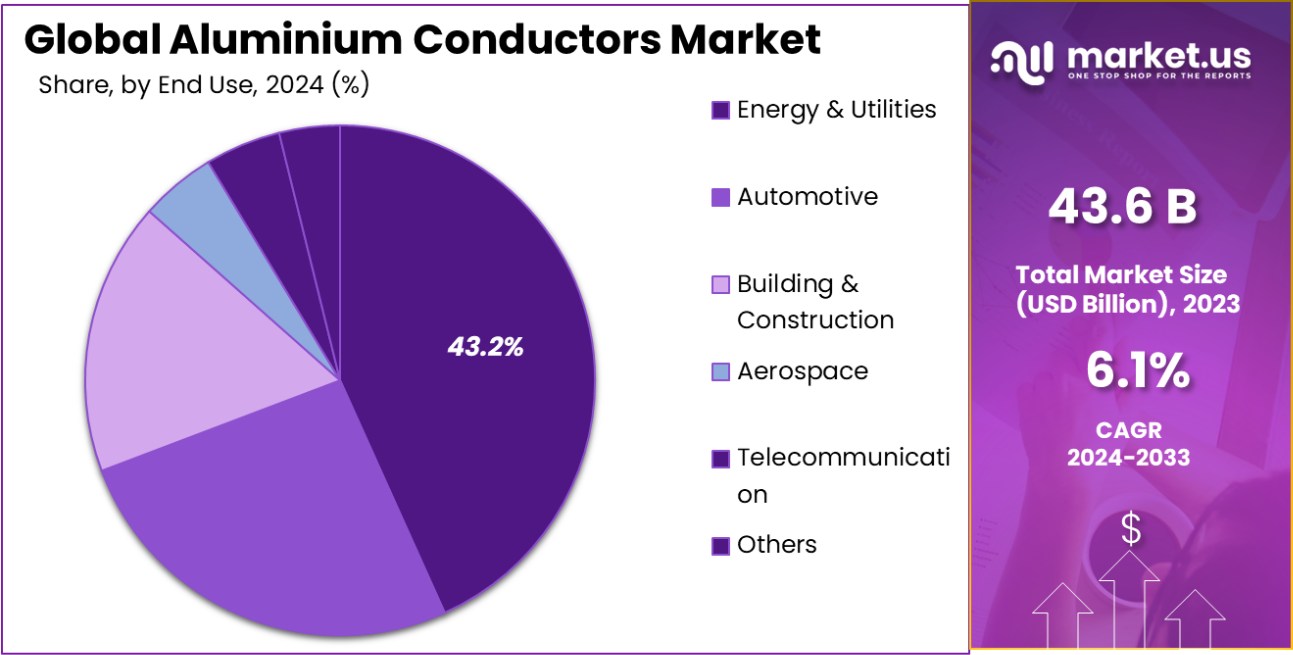

Energy and utilities sectors account for 43.2%, emphasizing growing electricity consumption trends globally.

In 2023, Energy and Utilities held a dominant market position in the By End-Use segment of the Aluminium Conductors Market, with a 43.2% share. This was followed by Building and Construction at 25.6%, Telecommunication at 16.7%, Automotive at 9.1%, and Aerospace at 5.4%.

The energy and utilities sector remains the largest consumer of aluminum conductors due to the growing demand for efficient power transmission and distribution networks. Aluminium’s lightweight, cost-effective, and highly conductive properties make it an ideal choice for the construction of overhead transmission lines, substations, and power grid infrastructure.

The building and construction sector is also a significant contributor, driven by the increasing need for electrical wiring in residential, commercial, and industrial buildings. As urbanization expands, the demand for robust electrical systems grows, further bolstering the market for aluminum conductors in this space.

In the Telecommunication sector, the use of aluminum conductors in the development of communication lines and data transmission infrastructure continues to expand, driven by the increasing need for high-speed connectivity.

The Automotive and Aerospace sectors, though smaller in comparison, are also contributing to the demand, particularly in electric vehicle manufacturing and aircraft electrical systems, where lightweight materials are crucial.

Key Market Segments

By Type

- All Aluminum Alloy Conductor

- Aluminum Conductor Steel Reinforced

- Aluminum Conductor Aluminum-Alloy Reinforced

- Others

By Capacity

- Up to 200A

- 200A to 750A

- 750A and above

By Voltage Level

- Low Voltage

- Medium Voltage

- High Voltage

- Extra-High Voltage

By Application

- Overhead Transmission

- Underground Cables

- Building Wiring

- Automotive

- Others

By End-Use

- Aerospace

- Automotive

- Building and Construction

- Energy and Utilities

- Telecommunication

- Others

Driving Factors

Growing Demand for Efficient Power Transmission Systems

The need for reliable and cost-effective power transmission is driving the growth of the aluminium conductors market. Aluminium’s lightweight, high conductivity and cost-effectiveness make it ideal for long-distance transmission, especially in regions with growing energy demand.

As countries and industries invest in modernizing their electricity grids to support renewable energy and reduce transmission losses, the demand for aluminium conductors continues to rise. This trend is further supported by increasing infrastructure development in both developed and emerging economies.

Expansion of Renewable Energy Projects

The global shift towards renewable energy sources such as smart solar, wind, and hydropower is fueling the demand for aluminium conductors. Renewable energy projects require robust and efficient transmission lines to transport electricity from remote locations to urban centres.

Aluminium conductors, being lightweight and durable, are increasingly being used in these installations due to their excellent performance in both low and high-voltage applications. As governments push for clean energy initiatives, the growth in renewable energy infrastructure directly boosts the demand for aluminium conductors.

Rising Urbanization and Infrastructure Development

Urbanization and ongoing infrastructure development are key drivers of the aluminium conductors market. As cities expand and more residential and commercial buildings are constructed, there is an increased need for electrical wiring, both for power distribution and building systems.

Aluminium conductors are ideal for wiring systems due to their lightweight, high conductivity, and corrosion resistance. The growing demand for modern infrastructure and energy-efficient building solutions is expected to keep pushing the market for aluminium conductors forward in both urban and rural settings.

Restraining Factors

High Initial Cost of Aluminium Conductors

While aluminium conductors offer long-term cost savings, their initial installation cost can be relatively high compared to alternative materials like copper. This upfront expense may deter some businesses and governments, particularly in regions where budget constraints are a concern.

Additionally, the costs associated with raw material extraction, manufacturing, and transportation can further increase the overall price. Although the price of aluminium has been stable in recent years, the high initial investment remains a challenge for widespread adoption in certain market segments.

Competition from Alternative Materials

Aluminium conductors face competition from other materials such as copper and fiber-optic cables. Copper, although more expensive, offers superior conductivity and is still widely used in specific high-performance applications. Moreover, the increasing adoption of fibre-optic cables for communication infrastructure in various industries, such as telecommunications and data transmission, poses a potential threat to the growth of aluminium conductors.

As a result, manufacturers must focus on innovations that enhance the performance of aluminium while addressing the benefits of alternative materials to stay competitive.

Environmental Concerns Over Aluminium Production

Aluminium production is an energy-intensive process, contributing to carbon emissions and environmental degradation. With increasing global focus on sustainability and reducing carbon footprints, industries are under pressure to minimize the environmental impact of their operations.

Although aluminium is recyclable, its production still raises concerns, particularly in markets where environmental regulations are tightening. As more countries implement stricter sustainability guidelines, aluminium producers may face additional challenges in complying with these standards, potentially slowing market growth and increasing operational costs for manufacturers.

Growth Opportunity

Rising Investments in Smart Grid Infrastructure

The global push towards modernizing electrical grids presents a significant growth opportunity for the aluminium conductors market. Smart grids, which integrate advanced digital technologies for more efficient electricity distribution, require high-quality conductors to handle increased data flow and energy demand.

Aluminium’s lightweight and conductive properties make it an ideal choice for upgrading and expanding smart grid systems. As countries prioritize energy efficiency and grid resilience, the demand for aluminium conductors will continue to rise, offering new opportunities for manufacturers and suppliers to capitalize on this growing market.

Increasing Demand for Renewable Energy Solutions

With the global shift toward renewable energy, the demand for aluminium conductors is expected to grow substantially. Solar, wind, and hydropower projects require efficient, long-distance power transmission to connect renewable energy sources to national grids.

Aluminium’s cost-effectiveness and light weight make it an ideal choice for these applications, particularly in remote locations where infrastructure is limited. As governments and organizations invest more in renewable energy, the need for aluminium conductors to support these initiatives is projected to expand, creating a promising growth opportunity.

Expansion in Emerging Market Economies

Emerging economies in regions such as Asia-Pacific, Africa, and Latin America represent a significant growth opportunity for the aluminium conductors market. As these regions urbanize and industrialize, their demand for electricity infrastructure is growing rapidly.

Aluminium conductors are increasingly being adopted due to their affordability and efficiency in large-scale transmission and distribution projects. The expansion of power grids, particularly in rural and remote areas, provides an opportunity for aluminium conductors to play a critical role in meeting these regions’ energy needs.

Latest Trends

Shift Towards Aluminum-Alloy Conductors for Enhanced Performance

A growing trend in the aluminium conductors market is the increasing adoption of aluminium-alloy conductors, which offer improved strength and better performance compared to standard aluminium conductors. These alloys can withstand higher temperatures and provide better durability, making them more suitable for high-load applications in power transmission and distribution networks.

The trend is being driven by the need for more reliable and longer-lasting solutions, especially in regions with harsh environmental conditions, and by the demand for higher transmission capacities with reduced energy losses.

Integration of Sustainable and Eco-Friendly Practices

Sustainability is becoming a key consideration in the aluminium conductors market, with manufacturers increasingly focusing on producing more environmentally friendly products. This includes using recycled aluminium in conductor production, which reduces the environmental impact of mining and manufacturing processes.

Additionally, there is a growing demand for aluminium conductors in renewable energy projects, such as solar and wind farms, where sustainability is a priority. The shift towards eco-friendly materials and practices is expected to drive future growth in the aluminium conductors market, especially as environmental regulations become stricter.

Adoption of Advanced Manufacturing Technologies

The aluminium conductors market is seeing a trend towards the adoption of advanced manufacturing technologies, such as automation, robotics, and 3D printing. These innovations help improve the efficiency, precision, and scalability of conductor production, reducing costs and enhancing product quality.

Manufacturers are also exploring new methods to produce lighter and more flexible conductors without compromising performance. As demand for aluminium conductors grows across various industries, these technological advancements are enabling companies to meet increasing production requirements while maintaining competitive pricing and meeting high-quality standards.

Regional Analysis

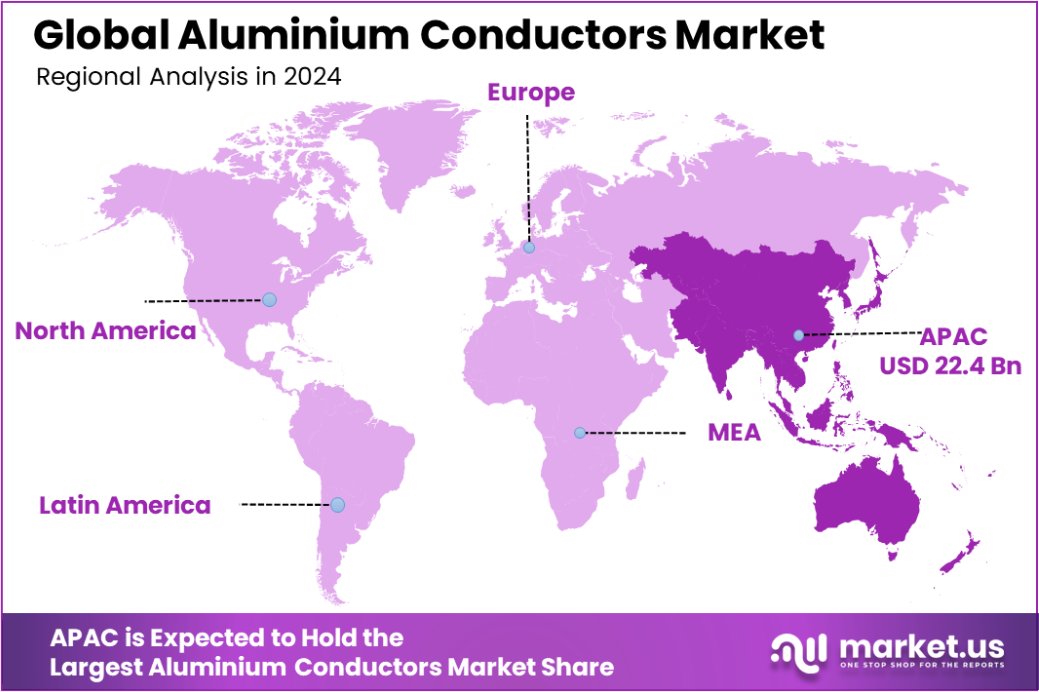

The Asia-Pacific region holds a 51.4% share in the Aluminium Conductors Market, worth USD 22.4 billion.

In 2023, Asia-Pacific dominated the global aluminium conductors market, holding a significant share of 51.4%, valued at USD 22.4 billion. The region’s dominance is primarily driven by rapid industrialization, increasing urbanization, and extensive infrastructure development in countries like China, India, and Japan.

Asia-Pacific’s growing demand for energy, particularly from power transmission and renewable energy projects, continues to boost the market for aluminium conductors. Additionally, government investments in smart grid infrastructure and modernizing electrical networks support sustained growth in the region.

North America holds the second-largest market share, accounting for approximately 23.6% of the market, valued at USD 10.1 billion. The region’s demand is driven by robust energy infrastructure, especially in the United States, and a significant push towards renewable energy integration. The shift towards electric vehicles and the expansion of smart grids further fuel the market for aluminium conductors in North America.

Europe follows with a market share of 14.2%, valued at USD 6.1 billion. The growing emphasis on renewable energy projects and grid modernization initiatives within the European Union supports this growth.

Middle East & Africa and Latin America represent smaller shares, at 7.3% and 3.5%, respectively. However, both regions are witnessing increasing investments in energy and infrastructure, which could drive future demand for aluminium conductors.

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Key Players Analysis

In 2023, the global aluminium conductors market continues to be highly competitive, with key players driving innovation and market expansion across various regions. Companies like APAR Industries Limited and Arfin India Limited lead the market, capitalizing on their robust manufacturing capabilities and strategic presence in emerging markets such as India and Southeast Asia.

APAR Industries, for instance, has strengthened its position through continuous product development in high-performance aluminium conductors, catering to the growing demand in power transmission and distribution.

Baotou Aluminium (Group) Co. Ltd. and Norsk Hydro ASA, both based in Asia, continue to lead the market with their large-scale production capabilities, leveraging their expertise in aluminium extraction and processing.

Norsk Hydro, known for its eco-friendly production methods, is also contributing to the trend of sustainable aluminium sourcing, positioning itself as a preferred supplier of energy-efficient solutions.

Ducab Aluminium Company and KEI Industries Ltd. are among the dominant players in the Middle East and India, respectively, serving regional demand for aluminium conductors in both industrial and utility-scale projects. Ducab’s focus on expanding its portfolio of advanced conductors and KEI Industries’ strategic alliances with global energy companies give it an edge in terms of market reach and technological expertise.

Companies like Galaxy Transmissions Pvt. Ltd., MWS Wire Industries, and Kaiser Aluminium Corporation are also expanding their footprint by tapping into niche markets such as building wiring and automotive applications, diversifying their product offerings to cater to a broader range of end-users.

The increasing focus on high-quality, cost-effective solutions, along with sustainability, will likely continue to drive innovation and competition among these key players in the coming years. The market is expected to witness further consolidation as these players strengthen their global supply chains to meet the rising demand for aluminium conductors across both traditional and emerging sectors.

Top Key Players in the Market

- APAR Industries Limited

- Arfin India Limited

- Baotou Aluminium (Group) Co. Ltd.

- Ducab Aluminium Company.

- Galaxy Transmissions Pvt. Ltd.

- Group Nirmal

- Heraeus Holding

- Hindusthan Urban Infrastructure Ltd

- JSk Industries Pvt. Ltd

- Kaiser Aluminium Corporation

- KEI Industries Ltd.

- Lumino Industries Limited

- MWS Wire Industries, Inc.

- Norsk Hydro ASA

- Novametal SA

- OBO Bettermann Holding GmbH & Co. KG

- Oswal Cables Pvt Ltd

- RusAL

- Shanghai Metal Corporation

- Southern Cable Group

- Southwire Company, LLC

- Sturdy Industries Ltd.

- Sumitomo Electric Industries, Ltd.

- Taihan Electric Wire Co. Ltd

- TOTOKU INC

- Transrail Lighting Limited

- TRIMET Aluminium SE

- TT Cables

- UC Rusal

- Vimetco NV.

Recent Developments

- In 2023, APAR Industries Limited focused on advancing aluminium conductors with improved energy efficiency and reduced environmental impact. They introduced new conductor technologies for enhanced grid performance and supported renewable energy, particularly in solar power infrastructure.

- In 2023, Arfin India Limited expanded its production capacity and improved product quality in the aluminium conductors sector. The company also focused on strategic partnerships and innovation, enhancing energy efficiency and using eco-friendly materials for sustainable development.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2023) | USD 43.6 Billion |

| Forecast Revenue (2033) | USD 78.8 Billion |

| CAGR (2024-2033) | 6.1% |

| Base Year for Estimation | 2023 |

| Historic Period | 2019-2022 |

| Forecast Period | 2024-2033 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Type (All Aluminum Alloy Conductor, Aluminum Conductor Steel Reinforced, Aluminum Conductor Aluminum-Alloy Reinforced, Others), By Capacity (Up to 200A, 200A to 750A, 750A and above), By Voltage Level (Low Voltage, Medium Voltage, High Voltage, Extra-High Voltage), By Application (Overhead Transmission, Underground Cables, Building Wiring, Automotive, Others), By End-Use (Aerospace, Automotive, Building and Construction, Energy and Utilities, Telecommunication, Others) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA |

| Competitive Landscape | APAR Industries Limited, Arfin India Limited, Baotou Aluminium (Group) Co. Ltd., Ducab Aluminium Company., Galaxy Transmissions Pvt. Ltd., Group Nirmal, Heraeus Holding, Hindusthan Urban Infrastructure Ltd, JSk Industries Pvt. Ltd, Kaiser Aluminium Corporation, KEI Industries Ltd., Lumino Industries Limited, MWS Wire Industries, Inc., Norsk Hydro ASA, Novametal SA, OBO Bettermann Holding GmbH & Co. KG, Oswal Cables Pvt Ltd, RusAL, Shanghai Metal Corporation, Southern Cable Group, Southwire Company, LLC, Sturdy Industries Ltd., Sumitomo Electric Industries, Ltd., Taihan Electric Wire Co. Ltd, TOTOKU INC, Transrail Lighting Limited, TRIMET Aluminium SE, TT Cables, UC Rusal, Vimetco NV. |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |