Quick Navigation

Report Overview

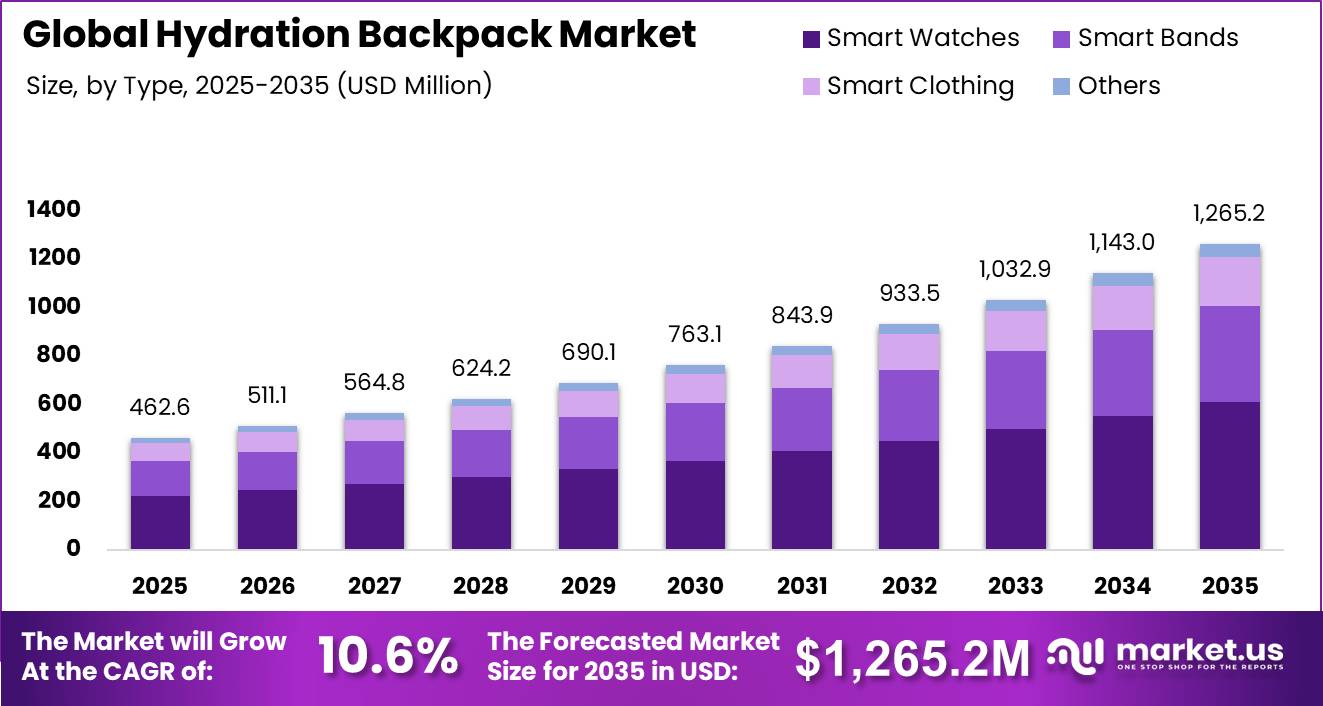

Global Hydration Backpack Market size is expected to be worth around USD 1,265.20 Million by 2035 from USD 462.6 Million in 2025, growing at a CAGR of 10.60% during the forecast period 2026 to 2035. This growth reflects a structural shift in how outdoor consumers approach endurance activities, where hands-free hydration is no longer optional equipment but a category standard.

The hydration backpack market covers wearable packs and vest-style carriers designed to hold fluid reservoirs, drinking tubes, and bite valves for active use during trail running, cycling, hiking, and military operations. The market spans a range of product formats from compact running vests under one liter to multi-liter tactical load-carriage systems. Distribution operates across both online retail and specialty outdoor channels globally.

Key Takeaways

- Market value in 2025: USD 462.6 Million

- Forecast market value by 2035: USD 1,265.20 Million

- CAGR for the period 2026 to 2035: 10.60%

- Dominant segment by Type: Smart Watches with 48.50% share

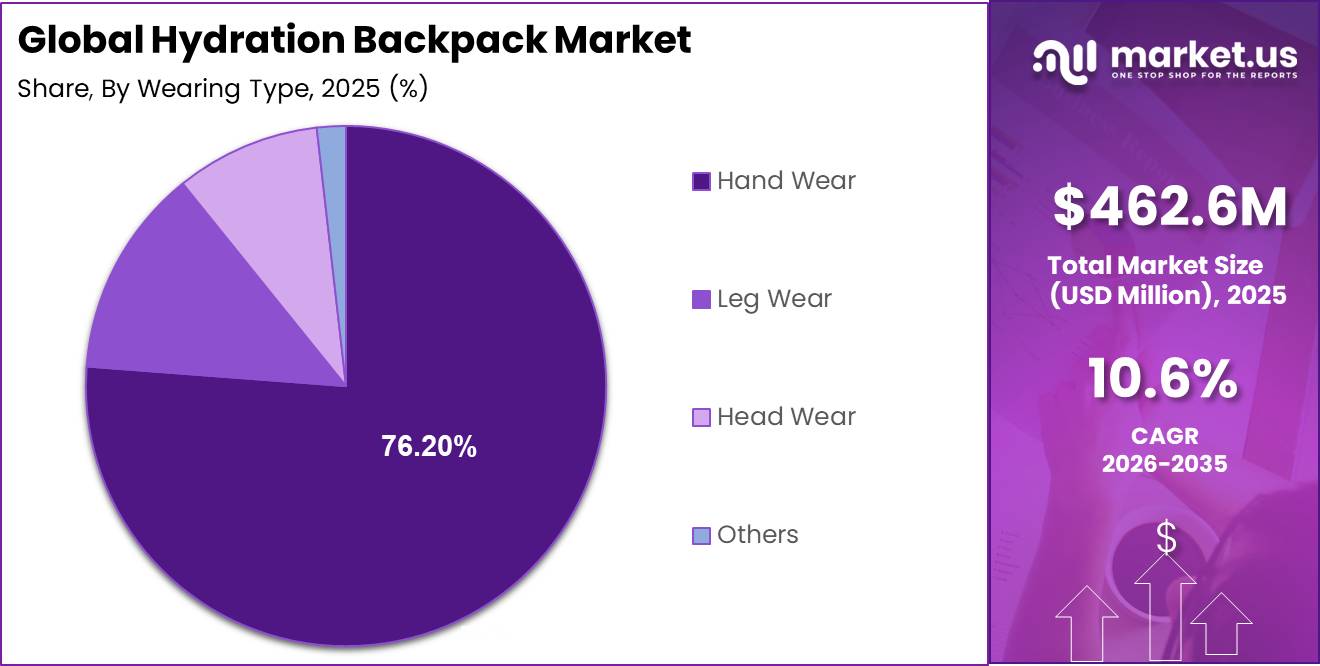

- Dominant segment by Wearing Type: Hand Wear with 76.20% share

- Dominant segment by Application: Heart Rate Tracking with 23.80% share

- Dominant segment by Distribution Channel: Online with 59.90% share

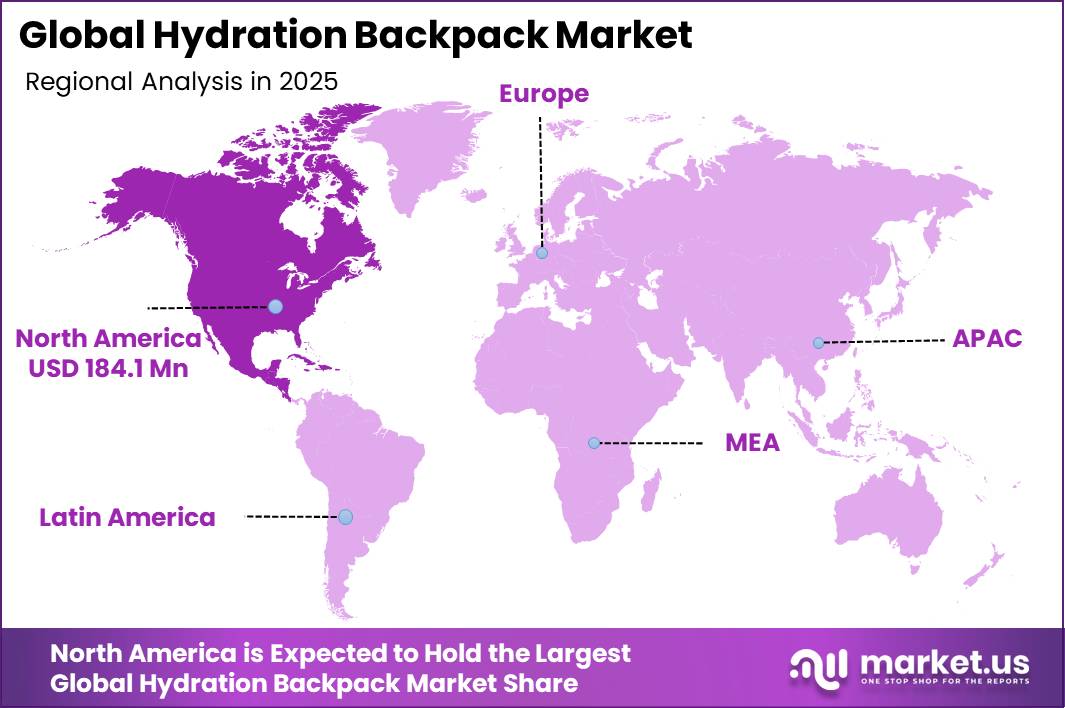

- Dominant region: North America with 39.80% market share, valued at USD 184.11 Million

According to the Outdoor Industry Association, outdoor recreation participation in the United States reached 175.8 million participants, equal to 57.3% of the population, in 2023. This large active consumer base directly supports demand for endurance gear including hydration backpacks, giving brands a broad addressable market across beginner and performance segments.

Data from the Outdoor Industry Association shows participation expanded by 22.2 million people between 2019 and 2023, covering hiking, biking, and running activities. This multi-year expansion indicates sustained structural demand rather than a post-pandemic spike, which reduces forecast risk for manufacturers and investors committing to this category through 2035.

As reported by the Bureau of Economic Analysis, outdoor recreation contributed USD 696.7 billion to U.S. GDP in 2024, representing 2.4% of total GDP. This economic scale confirms that outdoor gear including hydration backpacks sits within a federally measured, high-value consumption category, supporting premium pricing power and retail infrastructure investment.

Type Analysis

Smart Watches dominates with 48.50% due to wrist-based convenience and broad consumer adoption.

In 2025, Smart Watches held a dominant market position in the By Type segment of the Hydration Backpack Market, with a 48.50% share. Consumer preference for wrist-worn devices with multi-function display and GPS capability drives this position. Brands investing in smartwatch-integrated hydration alert features gain access to the largest and most purchase-active segment in the category.

Smart Bands hold a 31% share of the By Type segment, serving fitness-focused buyers who prioritize lightweight form over screen size. As per our research the University of Texas at Austin published a prototype wearable bioimpedance device in July 2025 targeting outdoor workers and athletes for real-time fluid tracking, validating the convergence of band-style wearables and hydration monitoring as a near-term product direction. Brands in this sub-segment face pressure to add sensing capability or risk commoditization.

Smart Clothing captures a 16% share of the By Type segment, reflecting early-stage adoption among performance endurance athletes. The category has not yet reached mainstream price points, which limits volume potential in the short term. However, brands that secure fabric sensor IP partnerships now will hold a defensible advantage as material costs decline through 2028.

Wearing Type Analysis

Hand Wear dominates with 76.20% due to established wearable form factor preference.

In 2025, Hand Wear held a dominant market position in the By Wearing Type segment of the Hydration Backpack Market, with a 76.20% share. The wrist and hand remain the primary wearable real estate for activity tracking and hydration alerts across consumer and professional use cases. Any new entrant targeting volume must address hand wear before expanding to secondary form factors.

Leg Wear accounts for 13% of the By Wearing Type segment, driven by compression garment brands adding biometric sensing layers. Outdoor recreation contributed USD 696.7 billion to U.S. GDP in 2024, confirming a deep consumer base with spending capacity to adopt specialized leg wear products at premium price points. This sub-segment rewards specialist positioning over generalist product strategies.

Head Wear holds a 9% share of the By Wearing Type segment, covering helmet-mounted sensors and smart cap applications primarily used in military and extreme sport contexts. The niche positioning limits mass market volume but supports high average selling prices. Tactical and defense procurement cycles give head wear brands more stable demand patterns than consumer-facing segments.

Application Analysis

Heart Rate Tracking leads with 23.80% due to universal fitness monitoring demand.

In 2025, Heart Rate Tracking held a dominant market position in the By Application segment of the Hydration Backpack Market, with a 23.80% share. The metric is the most requested biometric across beginner and advanced athlete populations, making it the default anchor application for hydration-wearable crossover products. Brands that embed heart rate data into hydration intake recommendations create a defensible personalization layer competitors cannot easily replicate.

Sleep Monitoring and Glucose Monitoring represent adjacent applications within the By Application segment that are gaining traction among health-conscious consumers beyond traditional athletic use cases. These applications extend daily wear time beyond active sessions, increasing device stickiness and subscription revenue potential. Brands that solve for continuous wear comfort will convert occasional users into daily users across these categories.

Sports sub-applications including Running Tracking and Cycling Tracking address the highest-value outdoor endurance users, who show the strongest overlap with core hydration backpack buyers. These users already invest in premium gear across multiple categories, making them receptive to bundled hydration-wearable system propositions. This creates a clear cross-sell channel for brands operating in both wearable and pack product lines.

Distribution Channel Analysis

Online channel dominates with 59.90% due to specialty product discovery and review-driven purchasing.

In 2025, Online held a dominant market position in the By Distribution Channel segment of the Hydration Backpack Market, with a 59.90% share. Digital-first purchasing reflects the technically informed buyer base in this category, where product specifications and user reviews drive conversion more than in-store trial. Brands with strong SEO, video content, and DTC storefronts capture this channel more efficiently than those relying on third-party retail relationships.

Offline retail retains the remaining share of distribution, serving buyers who require fit assessment, reservoir compatibility checks, and hands-on volume testing before purchase. Specialty outdoor and running retailers provide this service layer, which supports premium pack sales that online channels cannot replicate at scale. Brands should treat offline as a trial-conversion channel feeding online repeat purchases rather than a standalone revenue source.

Key Market Segments

By Type

- Smart Watches

- Smart Bands

- Smart Clothing

- Others

By Wearing Type

- Hand Wear

- Leg Wear

- Head Wear

- Others

By Application

- Heart Rate Tracking

- Sleep Monitoring

- Glucose Monitoring

- Sports

- Running Tracking

- Cycling Tracking

- Others

By Distribution Channel

- Online

- Offline

Drivers

EU Commission Regulation (EU) 2024/3190, published on 31 December 2024 and in force since 20 January 2025, formally prohibits BPA and its salts across all food contact materials in the EU, including reusable drink containers and hydration system components. The European Food Safety Authority’s 2023 assessment triggered this mandate after confirming endocrine disruption risks across all consumer age groups. Transitional periods allow non-compliant single-use articles already on market until 20 July 2026 and professional equipment until 20 January 2028.

India’s Food Safety and Standards Authority issued a draft notification on 6 October 2025 proposing a full ban on BPA and PFAS in all food contact materials manufactured from polycarbonate and epoxy resins. Compliance requires LC-MS/MS migration testing at a 1 µg/kg detection limit alongside Declarations of Conformity across entire product BOMs. For hydration pack manufacturers, this dual EU and India regulatory pressure is accelerating industry-wide transition to food-grade TPU, HDPE, and LDPE bladder materials. Established players with pre-certified supply chains gain a durable moat over non-certified private label competitors in both jurisdictions.

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Outdoor Recreation Boom: Record 183.2M U.S. participants in 2025; gateway activities each gaining 2M+ users | +2.2% | North America core; EU (UK, DACH, Nordics); APAC emerging corridors | Short term (≤ 2 years) |

| Health and Wellness Megatrend: Active lifestyle shift driving hydration consciousness; smart bottle market at 12.3 to 19.5% CAGR | +1.5% | North America; Western Europe; Urban APAC | Short to Medium term (1 to 4 yrs) |

| Smart Hydration Technology: IoT flow sensors, app-connected reservoirs; smart bottle market from USD 149.1M (2025) to USD 885.8M (2035) | +1.8% | North America; EU tech-forward; East Asia (South Korea, Japan) | Medium term (2 to 4 years) |

| Regulatory Mandate: BPA/PFAS-Free Materials: EU Reg. 2024/3190 in force since 20 Jan 2025; FSSAI draft ban notified 6 Oct 2025 | +1.2% | EU mandatory compliance; North America voluntary; India regulatory spill-over | Short to Medium term (1 to 3 yrs) |

| Sustainability-Led Innovation: ~42% of global consumers prefer recycled-material gear; EU Circular Economy Action Plan compliance as prerequisite | +1.0% | EU (sustainable products = 47% outdoor gear revenue); North America; Australia | Medium term (2 to 4 years) |

| E-Commerce and DTC Expansion: Online outdoor retail growing at 7.12% CAGR (2026 to 2031); APAC digital commerce fastest-growing channel | +1.3% | APAC (India, China, SEA); Latin America spill-over; Eastern Europe | Medium to Long term (2 to 5 yrs) |

Restraints

Thermoplastic Polyurethane (TPU), the primary feedstock for hydration pack reservoirs, bite valves, and tube assemblies, faces structural input cost inflation driven by competing end markets including automotive lightweighting, wearable medical devices, and flexible solar modules. The global TPU market is expanding at 6.4 to 6.78% CAGR through 2030, with Asia Pacific controlling 57 to 58.6% of global output near full capacity. Food-grade, BPA-compliant formulations command the upper end of the USD 3.50 to USD 7.00 per kg 2025 spot price band.

Crude oil price oscillations between USD 68 and USD 85 per barrel throughout 2025 introduced quarterly raw material cost variability of approximately 12 to 18% for polymer converters. Isocyanate and polyol precursors, which together constitute the majority of TPU production cost, track WTI movements closely. This variability compresses gross margins available to fund innovation CapEx, slowing the R&D investment that sustains CAGR velocity in a category increasingly driven by product differentiation.

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| TPU and Polymer Raw Material Cost Inflation | -1.4% | Global; APAC manufacturing core, North America/EU brand margin exposure | Medium term (2 to 4 years) |

| US Trade Tariff Escalation and Import Cost Shock | -1.2% | North America primary; EU spillover via price benchmarking | Short term (≤ 2 years) |

| BPA / Chemical Migration Regulatory Compliance | -0.8% | EU (Regulation 2024/3190), North America (NSF/ANSI), India (PWM Rules 2025) | Medium term (2 to 4 years) |

| Consumer Discretionary Spending Compression | -0.9% | North America, Western Europe (EU-5); moderate APAC exposure | Short term (≤ 2 years) |

| China-Centric Manufacturing Concentration Risk | -0.7% | Global supply chain; US and EU import-dependent brands | Medium term (2 to 4 years) |

| Competitive Substitution by Smart Water Bottles | -0.5% | North America, EU, Urban APAC corridors | Long term (≥ 4 years) |

Challenges

Consumer demand for smart hydration packs integrating volume sensing, temperature monitoring, GPS trail tracking, and wearable platform connectivity is accelerating product development bifurcation between R&D-capable incumbents and volume-oriented mid-tier manufacturers. As of March 2025, 449,000 U.S. manufacturing jobs remained unfilled per Bureau of Labor Statistics data, with the sector maintaining approximately 500,000 unfilled positions per month as a structural baseline for the past six years. The 2024 Deloitte and Manufacturing Institute report warns the sector may need 3.8 million new employees by 2033.

Hydration pack OEMs attempting to build smart pack capability in-house face a binary choice. Organic capability build-out carries a 24 to 30-month timeline in a hyper-competitive talent market where 65% of manufacturers cite attracting and retaining talent as their primary business challenge. Co-development licensing partnerships introduce IP sharing complexity and commercialization lead times of 12 to 18 months. World Economic Forum data indicates 40% of skills required in advanced manufacturing will change within five years, making static R&D investment a continuously depreciating asset.

| Challenge | (~) % CAGR Friction Drag | Geographic Relevance | Mitigation Horizon |

|---|---|---|---|

| TPU/MDI Raw Material Cost Volatility | -1.2% | APAC manufacturing hubs; EU and North America OEM buyers | Medium term (2 to 4 years) |

| Trade Tariff and Sourcing Disruption | -1.0% | Vietnam, Bangladesh, China export corridors; U.S. import market | Medium term (2 to 4 years) |

| BPA/PFAS Regulatory Compliance Burden | -0.8% | California, New York, Colorado; EU REACH jurisdictions | Short to Medium term (1 to 3 years) |

| Seasonal Demand and Inventory Volatility | -0.9% | North America, Europe (temperate-climate core markets) | Medium term (2 to 4 years) |

| Counterfeit Proliferation in Digital Channels | -0.7% | APAC e-commerce corridors; global online marketplaces | Long term (≥ 4 years) |

| Smart-Tech Integration and R&D Capability Gap | -0.8% | North America (innovation core); EU; APAC mid-tier OEMs | Long term (≥ 4 years) |

Opportunities

Smart hydration packs with embedded bioimpedance sensors represent the single largest unmonetized product category in the market today. The revenue architecture would combine a hardware premium of 35 to 55% over standard pack ASPs, lifting average unit values from approximately USD 85 toward USD 130 to 135, layered with a SaaS app subscription tier. This dual revenue model targets the 16.1 million active U.S. trail runners, of whom 66% earn above USD 100,000 annually, a demographic already normalized to wearables monetization.

Female participation in outdoor recreation reached 51.9% in 2023, the first time women accounted for more than half of all outdoor participants in the United States. This demographic shift signals a structural opportunity for women-specific hydration backpack designs with anatomically optimized fit systems. Brands that develop dedicated women’s fit lines capture a majority-participant demographic that current product ranges still underserve at scale.

APAC emerging markets including India, Vietnam, Indonesia, and Australia present a +2.2% CAGR upside opportunity per the market opportunity table, with the execution window within one to four years. Urban fitness culture and a rapidly expanding trail event calendar in these markets are building the same infrastructure that drove North American hydration backpack adoption one decade earlier. Brands entering these markets through digital-first DTC channels avoid the distribution cost structures that slowed physical retail penetration in earlier emerging market expansions.

| Opportunity | (~) % Potential CAGR Upside | Geographic Relevance | Execution Window |

|---|---|---|---|

| Smart/IoT-Enabled Packs: Embedded Sensor and App Ecosystem | +2.8% | North America core, EU, APAC emerging markets | Medium term (2 to 4 years) |

| APAC Emerging Market Penetration (India, SEA, ANZ) | +2.2% | India, Vietnam, Indonesia, Australia/NZ | Short to Medium term (1 to 4 years) |

| B2B Corporate Wellness and Branded Gifting Channel | +1.6% | North America, EU, GCC, India | Short term (≤ 2 years) |

| Tactical and Paramilitary Segment Expansion (Defense + First Responders) | +1.9% | North America, Indo-Pacific, EU NATO states | Medium term (2 to 4 years) |

| Sustainable Material and Circular Economy Positioning | +1.4% | EU regulatory core, North America, ANZ | Short to Medium term (1 to 4 years) |

| Festival, Rave and Urban Lifestyle Segment Monetization | +1.2% | North America, EU, Southeast Asia | Short term (≤ 2 years) |

Regional Analysis

North America Dominates the Hydration Backpack Market with a Market Share of 39.80%, Valued at USD 184.11 Million

North America holds the leading regional position driven by the largest documented outdoor recreation participation base globally, with the National Park Service recording more than 325 million recreation visits in 2023 across U.S. national parks. This volume of active outdoor visits translates directly into hydration gear purchase cycles and product upgrade demand across running, hiking, and cycling categories.

Europe represents the second-largest regional market, supported by a dense trail running and gravel cycling culture across Germany, France, and the Nordic countries. EU Regulation 2024/3190, in force since January 2025, is accelerating reformulation of reservoir materials across European OEMs. Brands with pre-certified TPU supply chains hold a compliance advantage that restricts market entry for non-certified competitors across the EU-5.

Asia Pacific is the fastest-expanding regional opportunity, driven by urban fitness culture in China, South Korea, and Japan alongside an expanding trail running event calendar in India and Southeast Asia. U.S. Forest Service data shows national forests support approximately 148 million recreation visits annually in the U.S. alone, signaling the infrastructure scale that APAC outdoor markets are still building toward, creating early-mover opportunity for brands entering now.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East and Africa

- GCC

- South Africa

- Rest of MEA

Apple, Inc. commands premium positioning through its Apple Watch ecosystem, which integrates fitness tracking, health monitoring, and third-party app connectivity at scale. Outdoor recreation value added increased by 9.0% in 2023 to reach USD 639.5 billion in the U.S. economy, a macro tailwind that directly expands Apple’s addressable market for health and activity wearables. However, Apple’s closed hardware ecosystem limits interoperability with standalone hydration monitoring accessories, leaving a white space for open-platform competitors.

Google (Fitbit, Inc.) pursues a data-first strategy through its Fitbit platform, prioritizing health metrics aggregation and cross-device data continuity over hardware premiumization. In June 2025, HydraPak expanded its Re_Pak recycling program nationwide with 300 collection boxes across more than 100 retail and event locations, signaling a sustainability-led supply chain shift that aligns with Google’s reported ESG positioning for Fitbit products. Google’s Android integration advantage gives Fitbit access to the largest global smartphone user base, but brand recall among premium outdoor buyers remains weaker than dedicated sports wearable competitors.

Key Players

- Apple, Inc.

- Google (Fitbit, Inc.)

- Garmin Ltd.

- HYPE

- SAMSUNG

- Fossil Group

- Huawei Technologies Co., Ltd.

Recent Developments

- April 2025 – CamelBak launched the redesigned H.A.W.G. 20, the first mountain-bike hydration backpack to integrate RECCO search-and-rescue technology, enhancing rider safety and emergency searchability during trail events.

- May 2025 – Canyon and Millet introduced the SHARP Hydration Vest, a performance hydration backpack system for gravel racing, marathon MTB, and endurance cycling, featuring a 2-liter HydraPak reservoir for sustained fluid delivery.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 462.6 Million |

| Forecast Revenue (2035) | USD 1,265.20 Million |

| CAGR (2026-2035) | 10.60% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Market Opportunity Analysis, Technology and Innovation Landscape, Competitive Landscape, Recent Developments |

| Segments Covered | By Type (Smart Watches, Smart Bands, Smart Clothing, Others), By Wearing Type (Hand Wear, Leg Wear, Head Wear, Others), By Application (Heart Rate Tracking, Sleep Monitoring, Glucose Monitoring, Sports [Running Tracking, Cycling Tracking], Others), By Distribution Channel (Online, Offline) |

| Regional Analysis | North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East and Africa (GCC, South Africa, and Rest of MEA) |

| Competitive Landscape | Apple, Inc., Google (Fitbit, Inc.), Garmin Ltd., HYPE, SAMSUNG, Fossil Group, Huawei Technologies Co., Ltd. |

| Customization Scope | Customization for segments, region/country-level will be provided. Additional customization can be done based on requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |