Quick Navigation

Report Overview

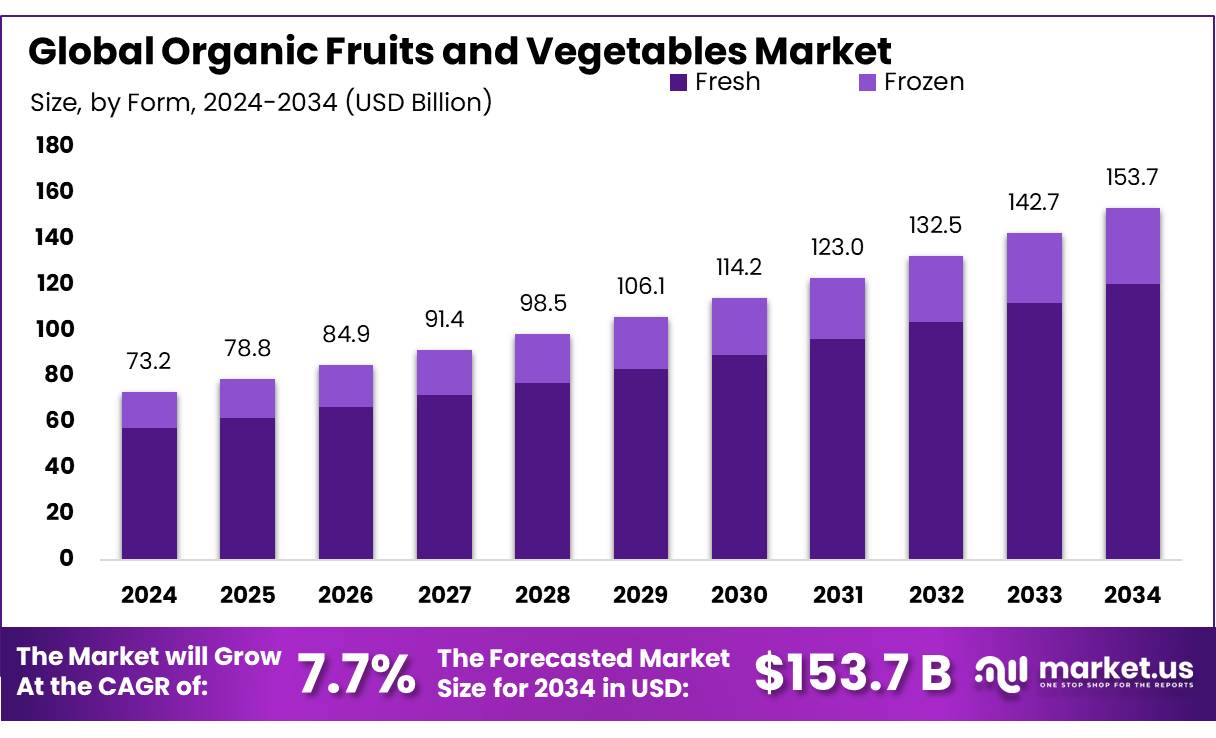

The Global Organic Fruits and Vegetables Market size is expected to be worth around USD 153.7 Billion by 2034, from USD 73.2 Billion in 2024, growing at a CAGR of 7.7% during the forecast period from 2025 to 2034.

The organic fruits and vegetables market concentrates has witnessed significant expansion in recent years, driven by evolving consumer preferences, strengthened regulatory support, and robust government initiatives. This analysis provides an industrial overview covering introduction, current scenario, key drivers, and future growth opportunities, with emphasis on quantitative data from authoritative sources.

The certified organic agricultural land base underpins the concentrate industry. In India, approximately 2.30 million ha of land are managed organically, representing 30% of global organic producers, with 2.76 million farmers involved. India leads globally with 4.43 million organic farmers according to the Economic Survey 2022–2023.

In the United States, organic-certified land grew from 1.8 million acres in 2000 to 4.9 million acres in 2021, supported by USDA’s National Organic Program. The USDA also allocated USD 50 million in organic R&D funding in 2023, a significant increase from USD 3 million in 2002. This growth in certified acreage and funding directly supports concentrate production capacities.

Government Schemes & Subsidies – India’s Mission Organic Value Chain Development in the North-East (MOVCD-NER) has sanctioned 100 FPOs across eight states covering 50,000 ha, enrolling 50,000 farmers since 2015–16; it offers subsidies up to 75% for infrastructure such as grading, cold storage, and transportation. Additionally, the Paramparagat Krishi Vikas Yojana (PKVY) and Operation Greens (allocated ₹500 crore for tomato, onion, and potato value chains) enhance processing and supply chain integration.

Innovative Regional Programs – The Godhan Nyay Yojana in Chhattisgarh supports organic inputs by purchasing cow dung at ₹2/kg, facilitating production of vermicompost and biofertilizers; over ₹5.59 crore has been disbursed to 162,497 farmers since inception. International Trade & Standards – Adoption of the Asia Regional Organic Standard (AROS) by UN agencies facilitates cross-border organic trade.

Key Takeaways

- Organic Fruits and Vegetables Market size is expected to be worth around USD 153.7 Billion by 2034, from USD 73.2 Billion in 2024, growing at a CAGR of 7.7%.

- Fresh held a dominant market position, capturing more than a 78.4% share of the global organic fruits and vegetables market.

- Vegetables held a dominant market position, capturing more than a 67.1% share of the global organic fruits and vegetables market.

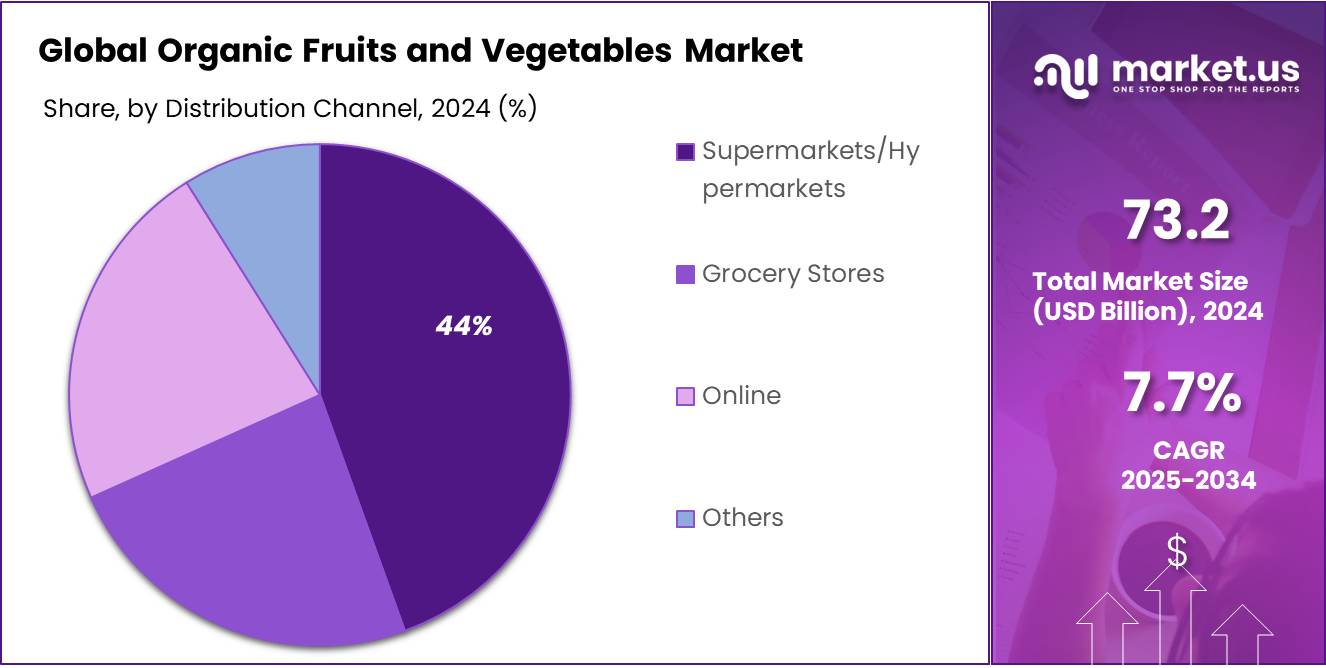

- Supermarkets/Hypermarkets held a dominant market position, capturing more than a 44.9% share of the global organic fruits and vegetables market.

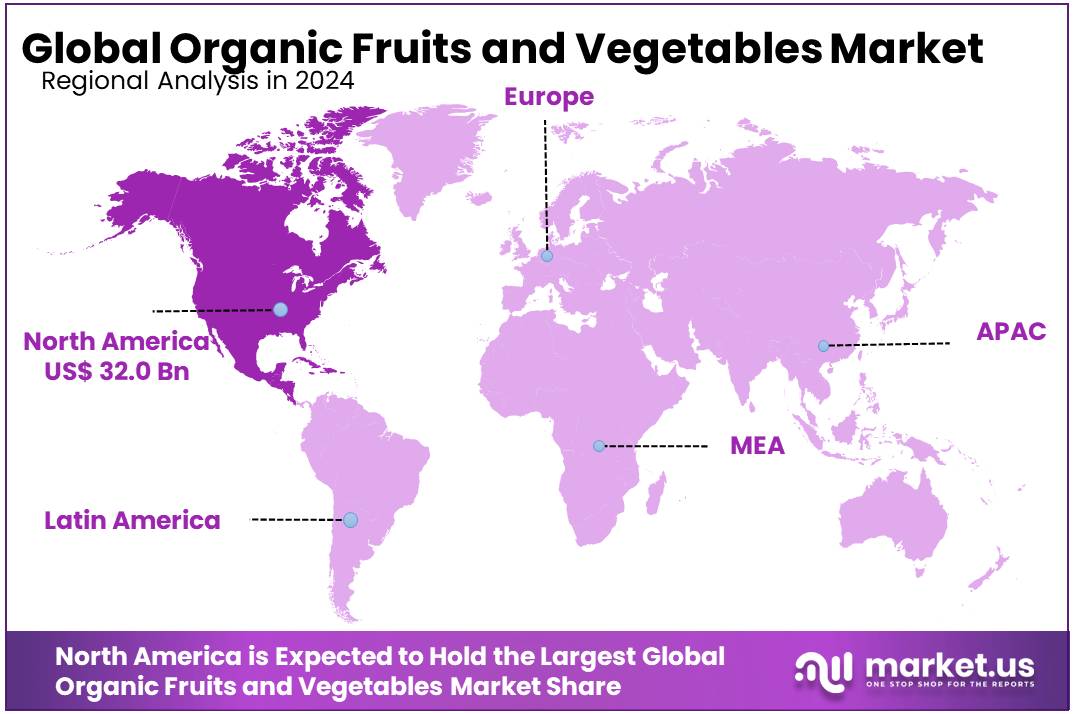

- North America emerged as a dominant region in the organic fruits and vegetables market, accounting for 43.8% of global revenue—equivalent to approximately USD 32 billion.

By Form

Fresh Organic Produce dominates with 78.4% in 2024 driven by consumer demand for minimally processed foods.

In 2024, Fresh held a dominant market position, capturing more than a 78.4% share of the global organic fruits and vegetables market. This strong preference is primarily driven by rising consumer awareness of clean eating, minimal processing, and the nutritional integrity of whole produce. The increasing availability of fresh organic options across supermarkets, farmers’ markets, and direct-to-consumer platforms has played a crucial role in supporting this growth.

As more households and foodservice providers prioritize seasonal, locally sourced organic ingredients, the fresh segment continues to benefit. The market’s shift toward plant-based diets and immunity-boosting foods post-2020 has further solidified the demand for fresh organic fruits and vegetables. In 2025, the segment is expected to maintain its lead, supported by ongoing government efforts to boost organic farming acreage and strengthen farm-to-fork supply chains in both developed and emerging economies.

By Product

Organic Vegetables lead with 67.1% in 2024, fueled by strong household and foodservice demand.

In 2024, Vegetables held a dominant market position, capturing more than a 67.1% share of the global organic fruits and vegetables market. This leadership is largely driven by their essential role in daily meals, both in households and commercial kitchens. Organic vegetables such as spinach, carrots, tomatoes, and bell peppers have seen increased demand due to their perceived health benefits and lower exposure to chemical residues.

Consumers are also showing more willingness to pay premium prices for organically grown greens, especially in urban areas where health trends are more pronounced. The rise of vegetarian and vegan lifestyles, along with clean-label movements, continues to boost the market for organic vegetables. In 2025, the segment is expected to hold its position as public institutions and restaurants expand their use of organic ingredients, encouraged by supportive procurement policies and growing supply chain efficiency.

By Distribution Channel

Supermarkets/Hypermarkets dominate with 44.9% in 2024 as consumers prefer convenience and variety.

In 2024, Supermarkets/Hypermarkets held a dominant market position, capturing more than a 44.9% share of the global organic fruits and vegetables market. This leadership reflects consumers’ growing preference for one-stop shopping experiences where they can find a wide variety of fresh organic produce under one roof. These large-format retail chains offer better visibility, frequent promotions, and reliable quality assurance, which help build consumer trust in organic labels.

Urban shoppers, in particular, rely heavily on supermarkets and hypermarkets for weekly grocery needs, and the increasing shelf space dedicated to organic goods has further fueled this segment. In 2025, the trend is expected to strengthen as retailers expand their organic offerings, invest in better cold chain logistics, and collaborate with local organic farms to maintain freshness and authenticity.

Key Market Segments

By Form

- Fresh

- Frozen

By Product

- Fruits

- Apple

- Bananas

- Watermelon

- Grapes

- Berries

- Mangoes

- Oranges

- Pineapples

- Others

- Vegetables

- Leafy Vegetables

- Carrots

- Potatoes

- Tomato

- Others

By Distribution Channel

- Supermarkets/Hypermarkets

- Grocery Stores

- Online

- Others

Drivers

Government support in expanding organic acreage drives market momentum

One of the most influential forces shaping the organic fruits and vegetables market is extensive government support aimed at scaling organic agriculture. In India, for instance, since 2015–16, a total of 59.74 lakh hectares have been brought under organic farming through key schemes such as the Paramparagat Krishi Vikas Yojana (PKVY) and the Mission Organic Value Chain Development in North Eastern Region (MOVCDNER). These programs offer financial incentives for infrastructure like processing units, grading facilities, and cold storage, along with training farmers in organic methods.

By June 30, 2024, PKVY had supported the formation of 38,043 organic clusters, each spanning approximately 20 hectares, collectively covering 8.41 lakh hectares under organic cultivation. This cluster based model enables group certification, shared infrastructure, and collective marketing, reducing per-farmer costs and improving market access. In parallel, MOVCDNER allocated assistance of ₹46,500 per hectare for three years to promote Farmer Producer Organizations (FPOs) in northeast India. These targeted subsidies have significantly lowered the barrier to entry for smallholders.

Further, the national certification program—NPOP—registered a total of 10.17 million hectares under certification by March 31, 2023, which includes both cultivated and wild harvest areas. This public oversight fosters consumer confidence in organic labeling and legitimizes organic products in domestic and international markets.

Restraints

Lower yields and steep certification costs slow market growth

Organic farming often delivers lower yields than conventional methods, which can restrict the supply of organic fruits and vegetables and increase production costs. Research shows that organic yields are about 18.4% lower on average compared to conventional farming systems . This decline stems from limitations in nutrient management, pest control, and weed suppression—factors that cannot be easily managed without synthetic inputs. As a result, farmers must cultivate larger areas or accept smaller harvests to meet organic supply demands. In some regions, organic yields drop to 80% of conventional outcomes, widening the gap between output and demand .

Beyond yield challenges, annual certification costs impose a financial burden. In North America, inspection and accreditation fees typically range from USD 400 to 2,000 per year, depending on operation size. While programs such as the USDA Organic Certification Cost Share Program can cover up to 75% of these costs—capping at USD 750 per year—many small farmers still face out-of-pocket expenses. These costs can deter producers, especially when combined with lower output and price uncertainties.

Furthermore, on-farm regulatory compliance adds to operational expenses. A case study of organic strawberry production in California indicated regulatory compliance costs of USD 95 per acre for water and nutrient management, plus approximately USD 112 per acre for food safety audits. These necessary investments in quality control and traceability are essential for consumer trust but raise the barrier to entry for smaller operators.

Opportunity

Export-led Opportunities buoy organic fruits and vegetables market

A substantial growth opportunity lies in expanding exports of organic produce, as evidenced by the performance of India’s agro-food sector in 2024–25. In this period, Maharashtra achieved a 15% increase in export value, reaching ₹47,017 crore, with fresh fruits contributing ₹9,500 crore—a 17% rise from the previous year. This surge highlights rising global demand for premium organic fruit backed by preferential government export policies and infrastructure support aimed at reducing transit delays.

Simultaneously, the state’s agricultural focus is being amplified through plantation growth. Fruit plantations across Maharashtra expanded by 68,541 hectares, from 13.32 lakh ha in FY 2023–24 to 14.00 lakh ha in FY 2024–25, driven by export-led incentives and domestic schemes such as the Bhausaheb Fundkar Falbagh Lavgad Scheme. Over 27,000 farmers received ₹9,891 lakh in aid through that program, underpinning longer-term expansion in quality organic output. This push ensures a reliable supply base that can be channelled into processing and export operations.

Furthermore, strategic initiatives to open new foreign markets have borne fruit. Maharashtra exported 14 tonnes of pomegranate to New York via sea freight—following U.S. market access approval in 2023—and similar exports of bananas, grapes, and other fruits to the Gulf and Europe have emerged. These developments reflect a shift away from air freight towards cost-effective sea routes, backed by government subsidies for cold-chain and grading facilities—enabling broader participation by growers.

Trends

Rise in pesticide-awareness driving organic choices

Increasing consumer awareness about pesticide residues is shaping a major trend in the organic fruits and vegetables market. In 2025, the Environmental Working Group (EWG) analyzed over 53,000 samples of produce tested by the USDA and highlighted that 96% of samples from the so called “Dirty Dozen”—including bell peppers, hot peppers, and green beans—contained pesticide residues. This striking data has heightened public concern over food safety, prompting many consumers to carefully choose produce that minimizes exposure. As a result, organic options are increasingly preferred, especially for high-residue items where conventional produce may pose health risks.

Simultaneously, governments are responding to this concern by promoting organic food systems and improving market access. In Haryana, India, officials recently announced plans to set up dedicated organic markets in Gurgaon and Hisar. Farmers will receive ₹20,000 per grower to enhance branding and packaging, and gain access to free quality testing services—designed to ensure that produce meets organic standards and wins consumer trust. These measures not only reassure shoppers about product safety, but also support local farmers in fulfilling rising demand.

Consumers are also being educated on simple steps to reduce conventional pesticide residues. Advice such as washing produce under running water for at least 15 seconds can lessen contamination—although it does not guarantee complete removal. This combination of public education, scientific scrutiny, and supportive policy is creating a strong cultural shift toward safer, cleaner eating habits—benefiting the organic fruits and vegetables market.

Regional Analysis

In 2024, North America emerged as a dominant region in the organic fruits and vegetables market, accounting for 43.8% of global revenue—equivalent to approximately USD 32 billion. This strong foothold reflects well-established organic farming infrastructure, growing consumer awareness, and increasing retail penetration across the region.

Across North America, advanced supply chains and robust retail networks—including supermarkets, hypermarkets, and fast-growing online channels—enabled premium pricing and consistent product availability. The online channel, in particular, is gaining momentum with projected annual growth of 11.3% through 2030.

Domestically, the region benefits from supportive government policies, such as subsidies for organic certification and infrastructure, as well as public campaigns promoting healthy diets. Strategic alignment between public initiatives and private retail investment is expected to sustain growth in organic fruits and vegetables.

Looking ahead, North America is set to further consolidate its leadership. Continued consumer demand for traceable, sustainably produced fresh produce—backed by strong institutional frameworks—positions the region as the global hub for organic fruits and vegetables in 2025 and beyond.

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

Conagra’s Refrigerated & Frozen segment, which includes organic vegetable offerings, reported flat organic net sales of USD 1.3 billion in its latest quarter. Within its international business, organic net sales rose by 4.3%, counterbalanced by a –1.2% volume decline. This suggests resilience in premium pricing but highlights the challenge of volume growth. The company continues to invest in brand-building for frozen vegetables, indicating its strategic focus on maintaining and expanding organic offerings.

Danone collaborates with over 50,000 farms worldwide, sourcing organic ingredients—including fruits—for use in its health focused product lines. The company has also prioritized regenerative agriculture in its supply chains, encompassing both dairy and plant based operations. This strong farm-level engagement and sustainability focus enhance its capacity to integrate organic produce into yogurt, beverages, and plant based alternatives, reinforcing Danone’s strategic pivot toward environmentally responsible growth.

Top Key Players in the Market

- Activz

- Amy’s Kitchen

- Conagra Brands

- Danone S.A.

- Del Monte Foods, Inc

- Dole Food Company, Inc.

- Driscoll’s, Inc.

- General Mills Inc.

- Green Organic Vegetable Inc

- J. Heinz Company

- Organic Valley Family of Farms

- SunOpta, Inc.

- The Hain Celestial Group

- Z Natural Foods LLC

Recent Developments

In 2024 Danone S.A. strengthened its position in the organic fruits and vegetables sector in Danone by focusing on regenerative and traceable sourcing practices. That year, the company achieved a 4.3% like-for-like sales growth, backed by a 3.0% increase in volume and mix—demonstrating consumer demand for its health-focused products.

In fiscal 2024, Conagra Brands—best known for consumer staples like frozen vegetables—saw organic net sales decline by 2.1%, totaling part of its overall USD 12.05 billion in annual net sales. Despite this drop, the Refrigerated & Frozen segment held steady at USD 4.87 billion, though organic volume slipped 4.1% from the prior year.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2024) | USD 73.2 Bn |

| Forecast Revenue (2034) | USD 153.7 Bn |

| CAGR (2025-2034) | 7.7% |

| Base Year for Estimation | 2024 |

| Historic Period | 2020-2023 |

| Forecast Period | 2025-2034 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Form (Fresh, Frozen), By Product (Fruits, Vegetables), By Distribution Channel (Supermarkets /Hypermarkets, Grocery Stores, Online, Others) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – GCC, South Africa, Rest of MEA |

| Competitive Landscape | Activz, Amy’s Kitchen, Conagra Brands, Danone S.A., Del Monte Foods, Inc, Dole Food Company, Inc., Driscoll’s, Inc., General Mills Inc., Green Organic Vegetable Inc, J. Heinz Company, Organic Valley Family of Farms, SunOpta, Inc., The Hain Celestial Group, Z Natural Foods LLC |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |