Quick Navigation

Report Overview

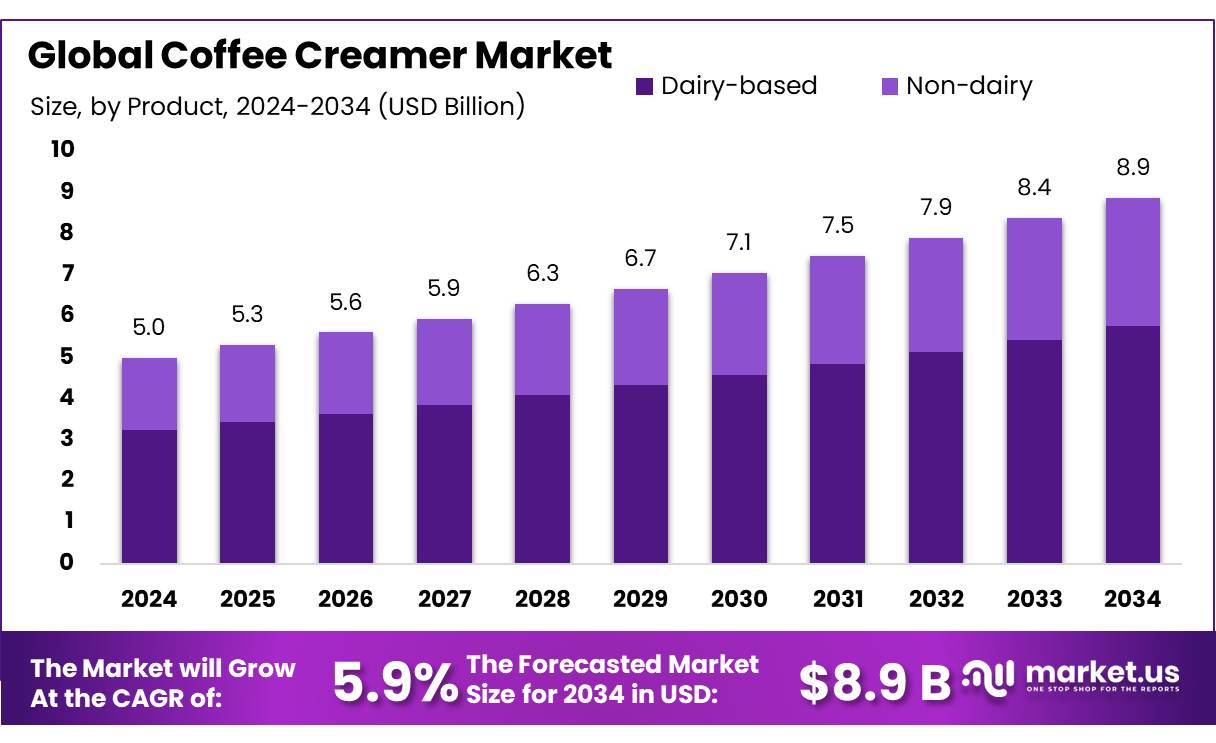

The Global Coffee Creamer Market size is expected to be worth around USD 8.9 Billion by 2034, from USD 5.0 Billion in 2024, growing at a CAGR of 5.9% during the forecast period from 2025 to 2034.

The wet coffee creamer concentrate industry plays a pivotal role in the global coffee and beverage sector, offering a convenient solution for enhancing the flavor and texture of coffee-based drinks. These concentrates are typically produced by blending milk or plant-based alternatives with emulsifiers, stabilizers, and flavoring agents, resulting in a product that is both shelf-stable and easy to use.

The industrial landscape is characterized by significant investments from major players. For instance, Nestlé inaugurated a $675 million coffee creamer manufacturing facility in Glendale, Arizona, in January 2025, aimed at producing popular brands like Coffee mate and Starbucks Coffee At Home. Similarly, Danone North America announced a $65 million investment to establish a new bottle production line in Jacksonville, Florida, enhancing its creamer production capabilities.

Several factors are propelling the growth of wet coffee creamer concentrates. The increasing demand for plant-based and non-dairy options is significant, with non-dairy creamers accounting for over 53.8% of the market share in 2022. Health-conscious consumers are gravitating towards low-fat and fat-free creamers, which are growing at CAGRs of 6.4% and 6.9%, respectively. Additionally, the rise in coffee consumption, with 66% of Americans drinking coffee daily, underscores the expanding market for creamers.

Government initiatives have played a supportive role in this industry’s development. For instance, the U.S. Food and Drug Administration (FDA) has implemented regulations to ensure the safety and quality of food products, including coffee creamers. In March 2025, the FDA extended its recall notice to include certain flavors of coffee creamers, advising consumers in 31 states to return or discard the impacted products. Such measures underscore the government’s commitment to consumer safety and product quality.

Key Takeaways

- Coffee Creamer Market size is expected to be worth around USD 8.9 Billion by 2034, from USD 5.0 Billion in 2024, growing at a CAGR of 5.9%.

- Dairy-based creamers held a dominant position in the global coffee creamer market, capturing more than a 67.9% share.

- Low-fat coffee creamers held a dominant position in the global market, capturing more than a 49.4% share.

- Liquid coffee creamers held a dominant position in the global market, capturing more than a 63.7% share.

- Conventional coffee creamers held a dominant position in the global market, capturing more than a 78.3% share.

- Regular or unflavored coffee creamers held a dominant market position, capturing more than a 54.2% share.

- PET bottles held a dominant market position in the global coffee creamer market, capturing more than a 39.2% share.

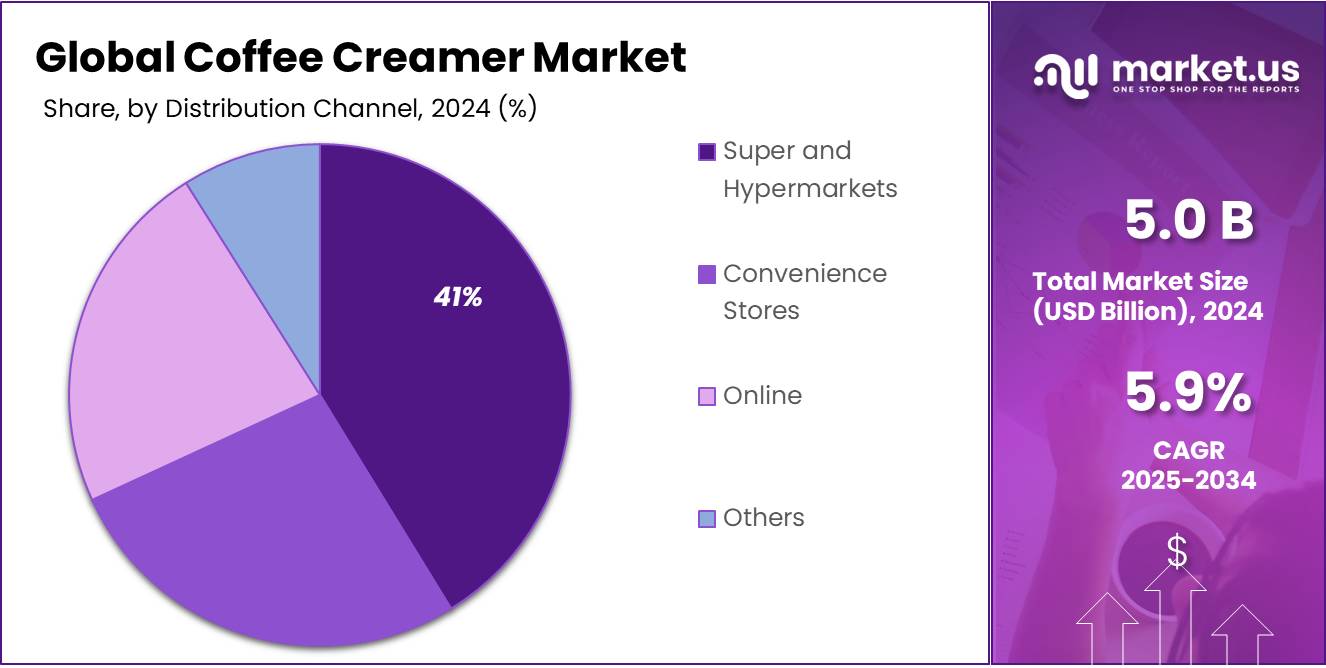

- Super and hypermarkets held a dominant position in the global coffee creamer market, capturing more than a 41.2% share.

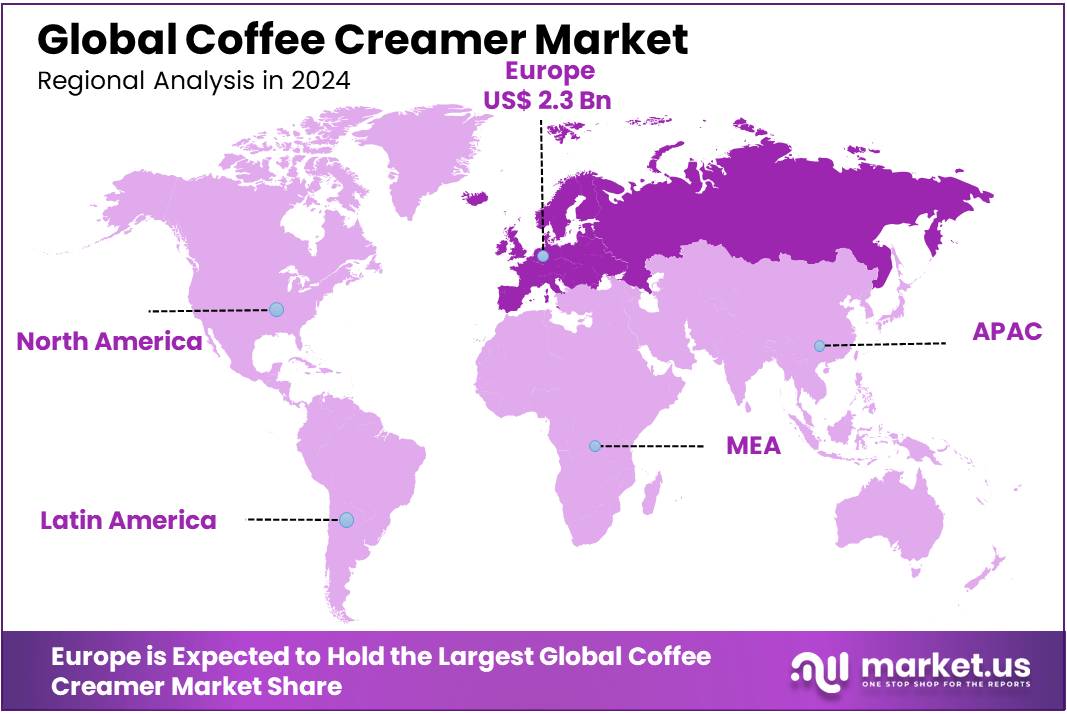

- Europe stands as the dominant region in the global coffee creamer market, commanding a significant share of approximately 45.2%, valued at USD 2.3 billion.

Analyst Viewpoint

From an investment perspective, the coffee creamer market presents a compelling opportunity driven by evolving consumer preferences and technological advancements. This growth is fueled by the rising demand for plant-based and health-conscious products, with non-dairy creamers accounting for 56.7% of the U.S. market revenue in 2024.

Technological innovations are playing a pivotal role in shaping the market. Companies are leveraging advancements to develop creamers with functional benefits, such as added proteins or cognitive enhancers, catering to health-conscious consumers. Additionally, the adoption of sustainable packaging solutions aligns with environmental concerns, appealing to eco-aware customers. However, investors should be mindful of regulatory challenges, as agencies like the FDA scrutinize product safety and labeling, particularly for functional ingredients .

Consumer insights reveal a shift towards personalized nutrition and at-home coffee experiences, especially post-pandemic. The preference for low-sugar, lactose-free, and plant-based options is growing, with 29% of U.S. coffee drinkers favoring low-sugar creamers . This trend underscores the importance of product diversification and innovation. While the market offers substantial growth potential, investors should consider risks such as fluctuating raw material costs and the need for compliance with evolving health regulations.

By Product

Dairy-Based Creamers Lead with 67.9% Market Share in 2024, Driven by Traditional Taste and Texture

In 2024, dairy-based creamers held a dominant position in the global coffee creamer market, capturing more than a 67.9% share. This strong preference is largely due to their rich, creamy texture and the familiar taste that resonates with traditional coffee drinkers. Consumers who value the classic coffee experience often choose dairy-based options for their indulgent mouthfeel and authentic flavor profile.

Despite the growing popularity of plant-based alternatives, dairy-based creamers continue to maintain a significant market presence. This enduring appeal is supported by the introduction of lactose-free and low-fat variants, catering to health-conscious consumers without compromising on taste. Brands like Nestlé and Land O’Lakes have expanded their product lines to include these options, ensuring they meet the evolving needs of their customer base.

By Type

Low-Fat Creamers Capture 49.4% Market Share in 2024, Reflecting Health-Conscious Consumer Preferences

In 2024, low-fat coffee creamers held a dominant position in the global market, capturing more than a 49.4% share. This significant market presence underscores a growing consumer shift towards healthier dietary choices, particularly in reducing fat intake without compromising on taste.

The preference for low-fat options is evident across various regions. In North America, for instance, the demand for low-fat non-dairy creamers has surged, driven by an increasing awareness of health and wellness. Consumers are seeking alternatives that align with their dietary goals, leading to a rise in the consumption of low-fat creamers made from plant-based ingredients like almond, soy, and oat milk.

By Form

Liquid Creamers Dominate with 63.7% Market Share in 2024, Favored for Convenience and Versatility

In 2024, liquid coffee creamers held a dominant position in the global market, capturing more than a 63.7% share. This preference is largely attributed to their convenience and ease of use, allowing consumers to quickly enhance the flavor and texture of their coffee without the need for additional preparation. The growing trend of at-home coffee brewing has further fueled demand for liquid creamers, as they enable consumers to replicate café-style beverages with minimal effort.

The versatility of liquid creamers, available in both dairy and non-dairy options, caters to a wide range of dietary preferences and restrictions. Manufacturers have responded to this demand by offering an array of flavors and formulations, including lactose-free and plant-based alternatives, to appeal to health-conscious consumers. This diversification has not only expanded the consumer base but also reinforced the position of liquid creamers as a staple in modern coffee consumption.

By Nature

Conventional Creamers Dominate with 78.3% Market Share in 2024, Reflecting Consumer Preference for Familiar Taste and Affordability

In 2024, conventional coffee creamers held a dominant position in the global market, capturing more than a 78.3% share. This significant market presence underscores consumers’ enduring preference for traditional taste profiles and the widespread availability of these products. Conventional creamers, often characterized by their consistent flavor and texture, continue to be the go-to choice for many coffee drinkers seeking a familiar and comforting addition to their beverages.

The affordability of conventional creamers further contributes to their market dominance. Priced lower than organic or specialty alternatives, these products are accessible to a broad consumer base, making them a staple in households and foodservice establishments alike. Brands like Nestlé’s Coffee Mate and Land O’Lakes have maintained strong market positions by offering a variety of flavors and formats that cater to diverse consumer preferences.

By Flavor

Regular/Unflavored Creamers Lead with 54.2% Market Share in 2024, Trusted for Their Versatility and Familiar Taste

In 2024, regular or unflavored coffee creamers held a dominant market position, capturing more than a 54.2% share of the global coffee creamer market. This strong preference highlights how many consumers still prioritize simplicity and a classic coffee taste over experimental or sweetened flavor profiles. For everyday coffee drinkers, especially those who enjoy the natural aroma and taste of coffee itself, unflavored creamers are a go-to option for a smooth, neutral texture without altering the coffee’s core flavor.

A major reason for this dominance is versatility. Regular creamers blend seamlessly with various coffee roasts and types—hot, iced, espresso-based—making them suitable for both home and commercial use. Coffee shops and offices also favor regular creamers, as they cater to the widest range of customer preferences without the need for stocking multiple flavored options.

By Packaging Type

PET Bottles Dominate with 39.2% Market Share in 2024, Thanks to Their Durability and Consumer Convenience

In 2024, PET bottles held a dominant market position in the global coffee creamer market, capturing more than a 39.2% share. This popularity is largely due to the convenience and practicality PET bottles offer for both manufacturers and consumers. Their lightweight, durable, and non-breakable nature makes them ideal for everyday handling, storage, and transportation, especially in busy households and retail environments.

Consumers also prefer PET packaging for its resealable feature, which keeps the product fresh for a longer period. The transparency of PET bottles adds another layer of consumer confidence, as people can easily see the product and gauge how much remains. This makes it a popular choice not just for individual households, but also for offices and cafes that use creamers in bulk.

By Distribution Channel

Super and Hypermarkets Lead Coffee Creamer Sales with 41.2% Market Share in 2024, Offering Convenience and Variety

In 2024, super and hypermarkets held a dominant position in the global coffee creamer market, capturing more than a 41.2% share. This prominence is largely due to the convenience and extensive product variety these retail formats offer. Consumers appreciate the ability to compare different brands and flavors in one location, making informed choices based on preferences and dietary needs.

The strategic placement of coffee creamers in these stores, often near coffee and tea sections, enhances visibility and encourages impulse purchases. Promotional activities, such as discounts and bundled offers, further drive sales in this channel. Additionally, the availability of both dairy and non-dairy options caters to a broad consumer base, including those seeking plant-based alternatives.

Key Market Segments

By Product

- Dairy-based

- Non-dairy

By Type

- High-fat

- Low-fat

- Fat-free

By Form

- Liquid

- Powder

By Nature

- Organic

- Conventional

By Flavor

- Regular/Unflavored

- Flavored

By Packaging Type

- Plastic Jars

- Tetrapacks

- PET Bottles

- Others

By Distribution Channel

- Super and Hypermarkets

- Convenience Stores

- Online

- Others

Drivers

Growing Demand for Convenience and Ready-to-Use Products

One of the major driving factors for the coffee creamer market is the increasing consumer preference for convenience and ready-to-use products. As more people adopt fast-paced lifestyles, the demand for products that simplify daily routines has surged. Coffee creamers provide an easy way to enhance the taste and texture of coffee without the hassle of using fresh milk or cream, making them a popular choice especially among working professionals and younger consumers.

According to the U.S. Dairy Export Council, the consumption of flavored creamers has been steadily rising, with retail sales growing by approximately 5% annually over the past few years. This trend reflects a shift in consumer habits toward products that combine taste, convenience, and versatility. The ability of creamers to be stored for longer periods without refrigeration further supports their appeal, particularly in urban areas where time and refrigeration space may be limited.

Government initiatives promoting dairy farming efficiency and sustainability also indirectly support the coffee creamer market. For instance, the U.S. Department of Agriculture (USDA) has programs encouraging dairy innovation, such as the Dairy Business Innovation Initiatives, which aim to increase the production of value-added dairy products, including creamers. These efforts help ensure steady supply and quality, which is crucial as demand grows.

In addition, health-conscious consumers are driving the introduction of new varieties, including plant-based and low-fat creamers, widening the market’s appeal. The Food and Drug Administration (FDA) supports these innovations by updating regulations to accommodate plant-based alternatives, helping companies bring such products to market more efficiently.

Restraints

Health Concerns Over High Sugar and Additive Content

A significant restraining factor for the coffee creamer market is the growing consumer awareness and concern regarding the high sugar and additive content present in many creamer products. As health consciousness rises globally, more people are carefully scrutinizing the ingredients in their food and beverages. Coffee creamers, especially flavored and powdered varieties, often contain added sugars, artificial flavors, and preservatives, which can deter health-focused consumers from regular use.

According to the World Health Organization (WHO), excessive sugar intake is linked to a range of health issues such as obesity, diabetes, and cardiovascular diseases. WHO recommends that free sugar intake should be less than 10% of total daily calories, ideally below 5%. Many popular coffee creamers exceed this guideline in just one serving, raising red flags for nutritionists and consumers alike.

Data from the Centers for Disease Control and Prevention (CDC) also highlight that nearly 42% of American adults have obesity, a condition often connected to dietary sugar consumption. This has led to increasing demand for cleaner-label products with no added sugar, fewer additives, or natural ingredients — categories where many traditional creamers fall short.

In response, government agencies such as the U.S. Food and Drug Administration (FDA) are tightening regulations and encouraging manufacturers to improve labeling transparency and reduce harmful ingredients in processed foods. The FDA’s guidance on added sugars and nutrient content claims pushes companies to reformulate their products, but this transition can be costly and time-consuming, limiting rapid innovation in the creamer segment.

Opportunity

Expanding Demand for Plant-Based and Lactose-Free Creamers

The coffee creamer market is experiencing significant growth opportunities, particularly driven by the increasing consumer preference for plant-based and lactose-free alternatives. This shift is influenced by rising health consciousness, dietary restrictions, and environmental considerations.

According to the National Coffee Association’s Spring 2025 report, nearly one-third of coffee drinkers use creamer daily, highlighting the widespread adoption of coffee creamers. Within this segment, non-dairy creamers, including plant-based options, have gained substantial traction.

This growth is further supported by government initiatives promoting plant-based diets. For instance, the U.S. Department of Agriculture (USDA) has been encouraging the adoption of plant-based foods through various programs and guidelines, recognizing their benefits for health and sustainability. Such support not only fosters innovation in the sector but also enhances consumer confidence in plant-based products.

The increasing availability of plant-based creamers in both retail and foodservice channels reflects this demand. Major brands are expanding their product lines to include oat, almond, and soy-based creamers, catering to diverse consumer preferences. This trend is expected to continue as more consumers seek dairy-free options that align with their dietary choices and lifestyle.

Trends

Plant-Based Creamers: The Rising Trend in Coffee Culture

In recent years, the coffee creamer market has experienced a significant shift towards plant-based alternatives, reflecting broader dietary trends and growing health consciousness among consumers. This movement is not just a passing fad but a substantial change in how people approach their daily coffee rituals.

Plant-based creamers, made from ingredients like almond, oat, and coconut milk, have gained popularity due to their appeal to vegan and lactose-intolerant consumers. These alternatives offer a creamy texture and flavor profile that closely mimic traditional dairy creamers, making them a viable option for those seeking non-dairy choices. The rise of oat milk, for instance, has been particularly notable, with sales increasing by 151% over a one-year period, as reported by USA Today.

This trend is further supported by consumer preferences for healthier and more sustainable products. A survey by the National Coffee Association found that 29% of U.S. coffee drinkers prefer creamers that are low in sugar, indicating a shift towards more health-conscious choices.

The growing demand for plant-based coffee creamers is not only reshaping consumer habits but also influencing product innovation and market dynamics. As consumers continue to prioritize health and sustainability, the coffee creamer market is expected to see continued growth and diversification in the coming years.

Regional Analysis

Europe stands as the dominant region in the global coffee creamer market, commanding a significant share of approximately 45.2%, valued at USD 2.3 billion. This prominence is attributed to the region’s deep-rooted coffee culture, diverse consumer preferences, and a growing inclination towards health-conscious and plant-based dietary choices.

The European coffee creamer market is experiencing robust growth, driven by several key factors. The increasing demand for non-dairy and lactose-free alternatives is notable, with consumers seeking options that align with vegan and lactose-intolerant lifestyles.

Product innovation plays a crucial role in this expansion. Companies are introducing a variety of flavors and formulations to cater to diverse consumer tastes. The rise of online retail platforms has further facilitated access to these products, allowing consumers to explore and purchase coffee creamers more conveniently.

Moreover, the region’s regulatory environment supports the growth of the coffee creamer market. Policies promoting plant-based diets and sustainability are encouraging manufacturers to develop products that meet these standards, thereby enhancing market appeal.

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

Nestlé is a global leader in the coffee creamer market, leveraging its extensive product portfolio and strong brand presence. The company offers a wide range of dairy and non-dairy creamers catering to diverse consumer preferences. Nestlé invests heavily in innovation, focusing on plant-based and health-conscious options to meet evolving market demands. Its robust distribution network and strategic partnerships enable wide market penetration across regions, maintaining its competitive edge and driving consistent growth in the coffee creamer sector.

Danone is a key player known for its emphasis on health-oriented and plant-based dairy products. In the coffee creamer segment, Danone focuses on innovative non-dairy alternatives, appealing to vegan and lactose-intolerant consumers. The company integrates sustainability initiatives into its production, responding to growing consumer demand for eco-friendly products. With strong regional presence in Europe and North America, Danone continues to expand its coffee creamer offerings through research-driven product development and effective marketing strategies.

Chobani, originally renowned for its yogurt products, has expanded into the coffee creamer market by introducing natural and clean-label creamers. The company emphasizes using simple, wholesome ingredients with no artificial additives. Chobani’s innovation in plant-based creamers aligns with the rising consumer interest in healthy and sustainable choices. Its strong brand loyalty and focus on quality have helped it capture significant market share in the U.S., where it is steadily growing its coffee creamer portfolio.

Top Key Players in the Market

- Nestlé S.A.

- Danone

- Chobani LLC

- DreamPak LLC

- Viceroy Holland B.V.

- PT Santos Premium Krimer

- Kerry Group

- FrieslandCampina

- Land O’Lakes, Inc.

- Fujian Jumbo Grand Food Co., Ltd.

- Heartland Food Products Group

- Leaner Creamer LLC

- Califia Farms, LLC

- Laird Superfood

Recent Developments

In 2024 Nestlé S.A. is a prominent player in the global coffee creamer market, with its flagship brand, Coffee Mate, leading the charge. In 2024, Nestlé’s coffee creamer segment achieved a sales milestone of CHF 2.5 billion, contributing approximately 11% to the company’s total revenue of CHF 22.6 billion.

In 2024 Kerry Group, the company reported a revenue of €8.0 billion, with €6.9 billion from continuing operations, reflecting a 3.3% volume growth compared to the previous year. The Taste & Nutrition division, which encompasses Kerry’s coffee creamer offerings, achieved an EBITDA margin of 17.1%, up from 14.5% in 2023, indicating improved operational efficiency.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2024) | USD 5.0 Billion |

| Forecast Revenue (2034) | USD 8.9 Billion |

| CAGR (2025-2034) | 5.9% |

| Base Year for Estimation | 2024 |

| Historic Period | 2020-2023 |

| Forecast Period | 2025-2034 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Product (Dairy-based, Non-dairy), By Type (High-fat, Low-fat, Fat-free, By Form, Liquid, Powder), By Nature (Organic, Conventional), By Flavor (Regular/Unflavored, Flavored), By Packaging Type (Plastic Jars, Tetrapacks, PET Bottles, Others), By Distribution Channel (Super and Hypermarkets, Convenience Stores, Online, Others) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – GCC, South Africa, Rest of MEA |

| Competitive Landscape | Nestlé S.A., Danone, Chobani LLC, DreamPak LLC, Viceroy Holland B.V., PT Santos Premium Krimer, Kerry Group, FrieslandCampina, Land O’Lakes, Inc., Fujian Jumbo Grand Food Co., Ltd., Heartland Food Products Group, Leaner Creamer LLC, Califia Farms, LLC, Laird Superfood |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |