Global Operating Room Equipment Market By Product Type (Anesthesia devices, Surgical imaging equipment, Endoscopes, Electro surgical devices and Others), By End-User (Hospitals & clinics and Ambulatory surgical centers), Region and Companies – Industry Segment Outlook, Market Assessment, Competition Scenario, Trends and Forecast 2025-2034

- Published date: Feb 2026

- Report ID: 176820

- Number of Pages: 381

- Format:

-

keyboard_arrow_up

Quick Navigation

Report Overview

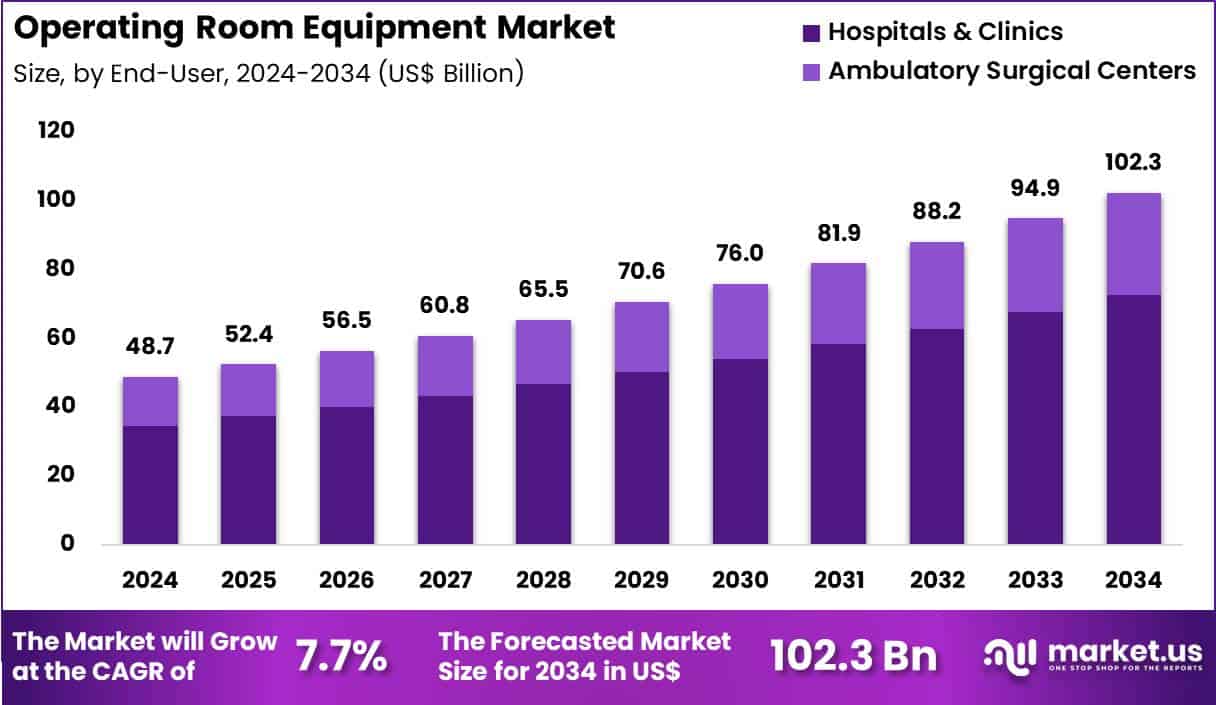

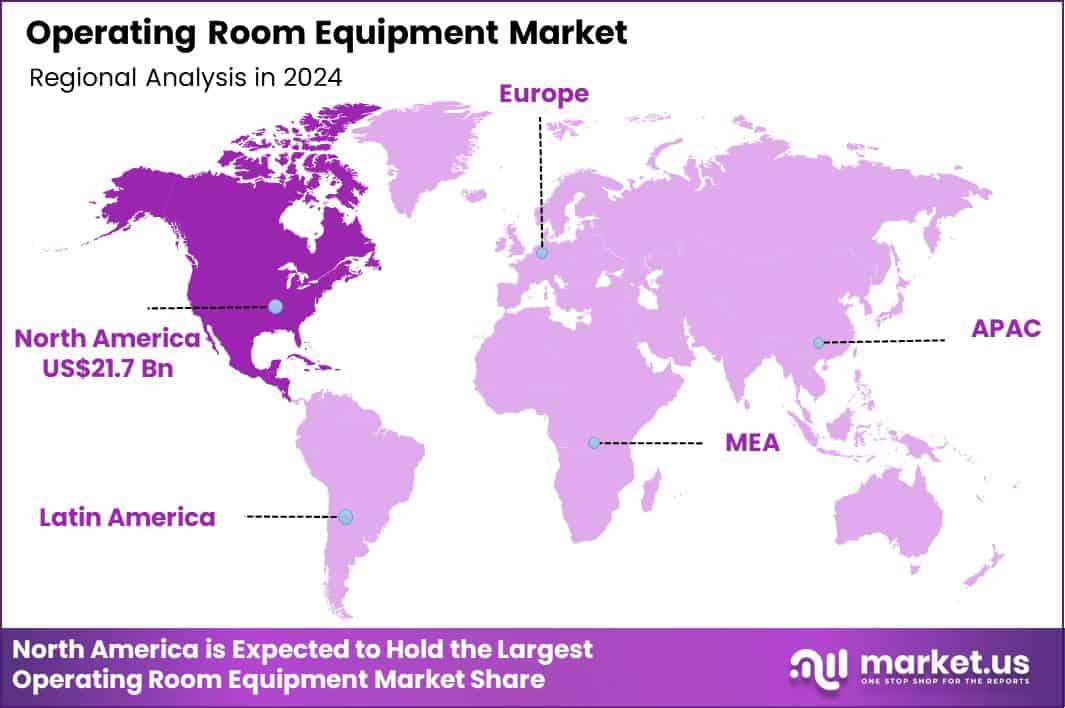

Global Operating Room Equipment Market size is expected to be worth around US$ 102.3 Billion by 2034 from US$ 48.7 Billion in 2024, growing at a CAGR of 7.7% during the forecast period 2025 to 2034. In 2024, North America led the market, achieving over 44.6% share with a revenue of US$ 21.7 Billion.

Increasing demand for advanced surgical precision and patient safety accelerates the operating room equipment market as hospitals upgrade infrastructure to support minimally invasive and complex procedures.

Surgeons increasingly rely on high-definition endoscopic towers and robotic systems during laparoscopic and robotic-assisted surgeries, enabling detailed visualization and precise instrument control in urologic, gynecologic, and colorectal interventions. These setups support integrated operating tables with powered positioning and radiolucent surfaces, facilitating intraoperative imaging and optimal patient access in orthopedic and spinal procedures.

Anesthesiologists utilize advanced anesthesia workstations equipped with integrated monitoring and gas delivery modules to maintain stable hemodynamics during lengthy cardiac and neurosurgical cases. Operating room teams deploy ceiling-mounted surgical booms and lighting systems to organize cables, supply medical gases, and provide shadow-free illumination, streamlining workflows in hybrid rooms combining open and endovascular techniques.

Electrosurgical units and energy platforms deliver controlled cutting and coagulation in general, thoracic, and plastic surgeries, minimizing blood loss and tissue damage. Manufacturers pursue opportunities to develop AI-enhanced imaging and navigation platforms that improve real-time decision-making, expanding applications in brain tumor resections and vascular interventions.

Developers advance modular, modular OR integration systems that allow seamless connectivity between devices, supporting data-driven workflows in high-acuity environments. These innovations facilitate adoption of augmented reality overlays for enhanced anatomical guidance in orthopedic joint replacements and cranial procedures.

Opportunities emerge in sustainable, energy-efficient equipment with antimicrobial surfaces, addressing infection control priorities in cleanroom-like operating suites. Companies invest in robotic and automated positioning technologies that reduce staff fatigue and procedural time in high-volume ambulatory centers.

Recent trends emphasize interoperable ecosystems and remote monitoring capabilities, positioning operating room equipment as critical infrastructure for value-based surgical care focused on efficiency, safety, and superior patient outcomes.

Key Takeaways

- In 2024, the market generated a revenue of US$ 48.07 Billion, with a CAGR of 7.7%, and is expected to reach US$ 102.3 Billion by the year 2034.

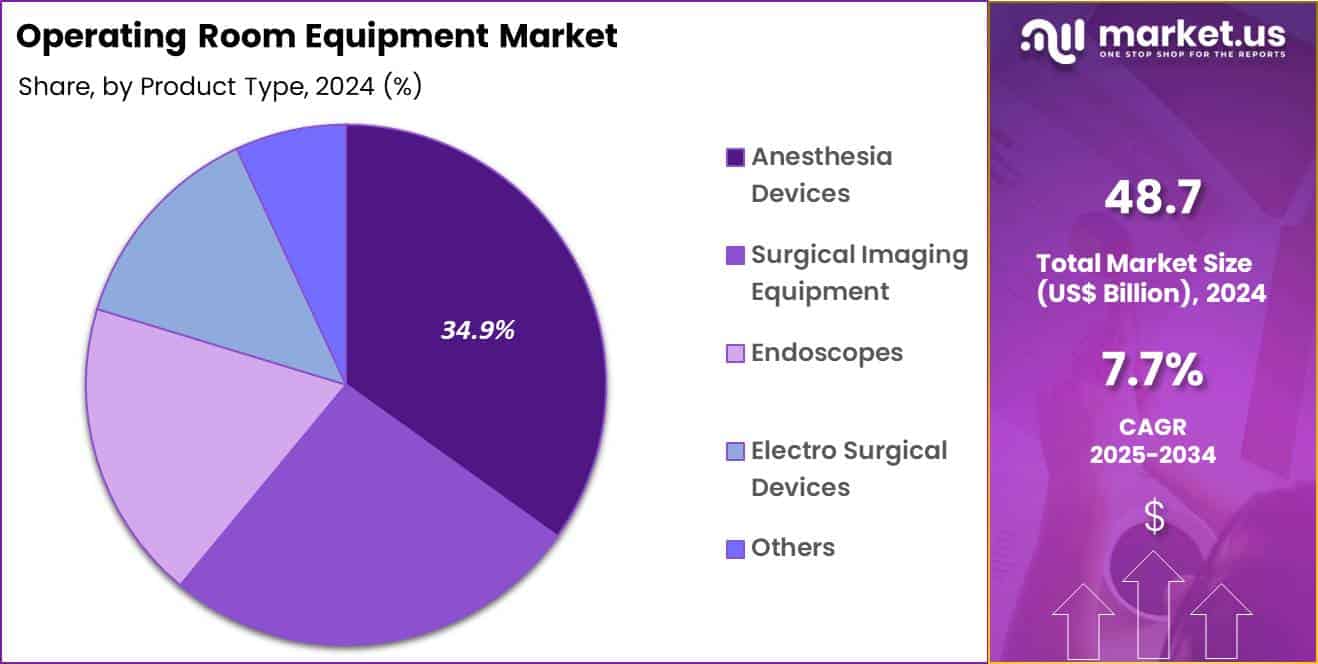

- The product type segment is divided into anesthesia devices, surgical imaging equipment, endoscopes, electro surgical devices and others, with anesthesia devices taking the lead with a market share of 34.9%.

- Considering end-user, the market is divided into hospitals & clinics and ambulatory surgical centers. Among these, hospitals & clinics held a significant share of 71.2%.

- North America led the market by securing a market share of 44.6%.

Product Type Analysis

Anesthesia devices contributed 34.9% of growth within product type and led the operating room equipment market due to their indispensable role in ensuring patient safety and procedural control across surgical specialties. Every operative intervention requires precise anesthesia delivery and monitoring, which keeps utilization consistently high.

Expansion of minimally invasive and complex surgeries increases demand for advanced anesthesia workstations that support ventilation, gas delivery, and real-time physiological monitoring. Clinicians rely on these devices to manage diverse patient profiles, including elderly and high-risk cases. Growth strengthens as hospitals upgrade legacy systems to integrate digital monitoring, decision support, and electronic records.

Enhanced safety features and automation improve workflow efficiency and reduce perioperative risk. Rising surgical volumes across general, orthopedic, and cardiovascular procedures further elevate demand. Training standardization and regulatory emphasis on perioperative safety reinforce procurement. The segment is expected to remain dominant as surgical care continues to prioritize precision anesthesia management and patient outcomes.

End-User Analysis

Hospitals and clinics accounted for 71.2% of growth within end-user and dominated the operating room equipment market due to their high surgical volumes and comprehensive procedural capabilities. These settings manage complex and emergency surgeries that require fully equipped operating rooms and advanced anesthesia, imaging, and electrosurgical systems.

Centralized infrastructure and multidisciplinary teams increase equipment utilization intensity. Hospitals also act as referral hubs, concentrating surgical demand within institutional settings. Growth continues as hospitals expand operating room capacity and modernize surgical suites.

Accreditation standards and infection control protocols encourage regular equipment upgrades. Teaching hospitals drive additional demand through training and research activities. Investment in specialty service lines increases procedural diversity and equipment needs. The segment is anticipated to remain the primary growth driver as hospitals and clinics continue to anchor surgical care delivery.

Key Market Segments

By Product Type

- Anesthesia devices

- Surgical imaging equipment

- Endoscopes

- Electro surgical devices

- Others

By End-User

- Hospitals & clinics

- Ambulatory surgical centers

Drivers

Increasing adoption of robotic systems is driving the market.

The growing utilization of robotic-assisted surgical systems has significantly propelled the demand for advanced operating room equipment to support precise and minimally invasive procedures. Enhanced technological capabilities in robotics enable surgeons to perform complex operations with improved accuracy and reduced recovery times.

Healthcare facilities are increasingly investing in these systems to enhance patient outcomes and operational efficiencies. Stryker’s Mako SmartRobotics platform has facilitated over 1.5 million procedures across 45 countries as of 2024. This milestone reflects the escalating reliance on robotic technologies in orthopedic and other surgical specialties.

The correlation between robotic adoption and the rising volume of elective surgeries further stimulates market expansion. Government initiatives promoting innovative healthcare solutions contribute to the integration of these systems in hospitals.

Key manufacturers are focusing on expanding their robotic portfolios to meet this surging clinical need. This driver aligns with global efforts to modernize surgical infrastructure for better care delivery. Overall, the robotic surge underpins robust advancements in operating room capabilities.

Restraints

High costs and financial strain on hospitals is restraining the market.

The substantial expenses associated with acquiring and maintaining advanced operating room equipment pose a significant barrier to widespread adoption in healthcare institutions. Manufacturing complexities for high-precision devices contribute to elevated pricing structures that strain hospital budgets. Smaller facilities often defer necessary upgrades due to limited financial resources and competing priorities.

Regulatory requirements for equipment safety and compliance add further layers of cost to procurement processes. In 2024, 94% of health care administrators expected to delay equipment upgrades to manage financial strain. This anticipation highlights the pervasive economic pressures impacting investment decisions.

Providers may opt for refurbished alternatives to mitigate expenditures, affecting new equipment sales. This restraint limits market penetration, especially in public health sectors with constrained funding. Collaborative financing options are emerging to address these challenges gradually. Despite technological benefits, fiscal constraints hinder equitable access to modern solutions.

Opportunities

Expansion into emerging markets is creating growth opportunities.

The rapid development of healthcare infrastructure in emerging economies presents avenues for deploying operating room equipment in underserved regions. Governmental investments in medical facilities support the integration of advanced surgical technologies to improve care standards. Increasing awareness of minimally invasive procedures drives demand for specialized equipment in these markets.

Strategic partnerships with local distributors facilitate regulatory navigation and market entry for global manufacturers. The large patient populations in populous nations amplify the potential for equipment utilization in diverse clinical settings.

Stryker reported emerging markets contributing 5.6% of total net sales in 2024. This share indicates growing revenue streams from under-penetrated areas outside developed regions. Educational programs for healthcare professionals enhance proficiency in operating advanced systems. This opportunity allows international firms to diversify beyond saturated markets. Overall, emerging expansions align with initiatives to bridge global healthcare disparities.

Impact of Macroeconomic / Geopolitical Factors

Broader economic conditions influence the operating room equipment market by shaping hospital spending priorities, cash flow discipline, and long term upgrade planning. Inflation and sustained high interest rates increase the cost of capital, which forces providers to defer purchases of advanced surgical tables, lights, and integrated OR systems.

Geopolitical uncertainty disrupts global supply chains for electronics, specialty metals, and precision components, creating delivery delays and sourcing risk. Current US tariffs on imported equipment and parts add to production and procurement costs, which pressures vendor margins and extends budget approvals for buyers.

These challenges weigh heavily on mid sized hospitals and ambulatory centers with tighter financial flexibility. On the positive side, tariff pressure encourages regional manufacturing, simplified system designs, and stronger supplier diversification.

Rising surgical backlogs and demand for safer, technology enabled operating rooms support consistent utilization. With pragmatic investment strategies and operational focus, the market continues to move forward with long term confidence.

Latest Trends

Integration of AI-enabled workflows is a recent trend in the market.

In 2024, the incorporation of artificial intelligence in operating room equipment has advanced workflow efficiencies through automated monitoring and decision support. These systems utilize AI to optimize clinical communication and reduce procedural delays. Manufacturers are focusing on seamless integration with existing hospital infrastructures for enhanced usability.

Acquisitions of AI specialists are accelerating the development of intelligent platforms for surgical environments. Stryker acquired care.ai in 2024 to integrate AI-enabled workflows with its Clinical Communication and Workflow platform. This move enhances virtual care capabilities and streamlines operating room operations.

Clinical applications benefit from real-time data analysis to improve patient safety. The trend emphasizes scalable solutions for high-volume surgical centers. Regulatory adaptations support the commercialization of these hybrid technologies. These innovations aim to minimize errors while maintaining clinical oversight.

Regional Analysis

North America is leading the Operating Room Equipment Market

North America holds a 38% share of the global Operating Room Equipment market, registering strong growth in 2024 through expanded adoption of integrated digital platforms that combine lighting, imaging, and data management to support complex minimally invasive procedures.

Major firms like Stryker and Hillrom have introduced modular surgical tables and ceiling-mounted booms that improve ergonomics and workflow efficiency in high-volume surgical suites. The region’s focus on ambulatory care has led to widespread installation of hybrid operating rooms equipped with real-time navigation systems for orthopedic and cardiovascular interventions.

State-level health departments have funded facility modernizations to accommodate growing surgical caseloads from an aging population and elective procedures. Rising emphasis on infection control has driven demand for antimicrobial surfaces and automated sterilization integration in new equipment deployments.

Partnerships between hospitals and technology developers have facilitated customized solutions for robotic-assisted surgeries, reducing operative times and enhancing precision. Insurance providers have expanded coverage for advanced setups, encouraging providers to invest in scalable infrastructure. The United States had 6,394 Medicare-certified ambulatory surgery centers in 2024, reflecting increased capacity for outpatient procedures requiring modern equipment.

The Asia Pacific region is expected to experience the highest CAGR during the forecast period

Governments across Asia Pacific channel resources into healthcare infrastructure upgrades that equip surgical facilities with integrated visualization and monitoring systems to handle rising procedure volumes. Manufacturers in Japan and South Korea develop energy-efficient lighting arrays and adjustable tables tailored for space-constrained urban hospitals, while providers in India deploy AI-assisted imaging platforms that streamline multidisciplinary team coordination.

Medical facilities in Vietnam expand capacity through procurement of portable endoscopic towers that support rapid setup in regional centers serving rural patients. Investors in Indonesia fund localization of component production for cost-effective anesthesia delivery units, enabling broader distribution to secondary care sites.

Regulators in Thailand approve streamlined certification processes that allow faster rollout of ceiling suspension systems for enhanced surgeon mobility. Clinicians in Malaysia integrate wireless data interfaces that enable seamless recording and review of procedural metrics during high-throughput operations.

Enterprises in Australia customize contamination-control enclosures that address tropical humidity challenges, improving equipment longevity in diverse climates. The Government of India launched a Rs 500 crore scheme in 2024 to boost domestic medical device manufacturing through five targeted sub-schemes.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia

- Netherland

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- New Zealand

- Singapore

- Thailand

- Vietnam

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Key Players Analysis

Key competitors in the operating room equipment market grow by expanding technologically advanced portfolios that include integrated surgical imaging, robotics, and real-time patient monitoring systems that elevate clinical precision and procedural efficiency. They also enhance customer value by offering flexible financing options, comprehensive installation support, and long-term service contracts that reduce total cost of ownership for hospitals and surgical centers.

Strategic partnerships with healthcare providers and specialized surgical training programs help them embed solutions into clinical workflows and strengthen brand preference among care teams. Geographic expansion into Asia Pacific and Latin America complements established positions in North America and Europe, capturing rising capital investment in healthcare infrastructure.

Medtronic exemplifies a diversified medical technology leader with a broad array of surgical instruments, visualization systems, and patient monitoring solutions, supported by extensive global distribution and dedicated clinical support teams.

The company reinforces its strategic agenda through disciplined R&D investment, targeted acquisitions that fill portfolio gaps, and coordinated commercialization that aligns innovation with evolving surgical demands.

Top Key Players

- GE Healthcare

- Siemens Healthineers

- Philips Healthcare

- Stryker

- Medtronic

- Getinge

- B. Braun

- Olympus

- Karl Storz

- Steris

Recent Developments

- In May 2025, Olympus Corporation showcased its latest AI-enabled endoscopy solution, the OLYSENSE Platform, during the Digestive Disease Week annual meeting. The platform incorporates the CADDIE computer-aided detection tool, which applies cloud-based artificial intelligence to support gastroenterologists in identifying suspected polyps during colonoscopy examinations.

- In October 2025, Olympus Corporation announced the receipt of CE approval for three cloud-based artificial intelligence medical devices. This regulatory clearance authorizes commercialization and clinical use of the solutions across the European Economic Area, confirming compliance with European requirements for medical device safety and performance.

Report Scope

Report Features Description Market Value (2024) US$ 48.7 Billion Forecast Revenue (2034) US$ 102.3 Billion CAGR (2025-2034) 7.7% Base Year for Estimation 2024 Historic Period 2020-2023 Forecast Period 2025-2034 Report Coverage Revenue Forecast, Market Dynamics, COVID-19 Impact, Competitive Landscape, Recent Developments Segments Covered By Product Type (Anesthesia devices, Surgical imaging equipment, Endoscopes, Electro surgical devices and Others), By End-User (Hospitals & clinics and Ambulatory surgical centers) Regional Analysis North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, New Zealand, Singapore, Thailand, Vietnam, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA Competitive Landscape GE Healthcare, Siemens Healthineers, Philips Healthcare, Stryker, Medtronic, Getinge, B. Braun, Olympus, Karl Storz, Steris Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF)  Operating Room Equipment MarketPublished date: Feb 2026add_shopping_cartBuy Now get_appDownload Sample

Operating Room Equipment MarketPublished date: Feb 2026add_shopping_cartBuy Now get_appDownload Sample -

-

- GE Healthcare

- Siemens Healthineers

- Philips Healthcare

- Stryker

- Medtronic

- Getinge

- B. Braun

- Olympus

- Karl Storz

- Steris

Our Clients

- 176820

- Feb 2026