Quick Navigation

Report Overview

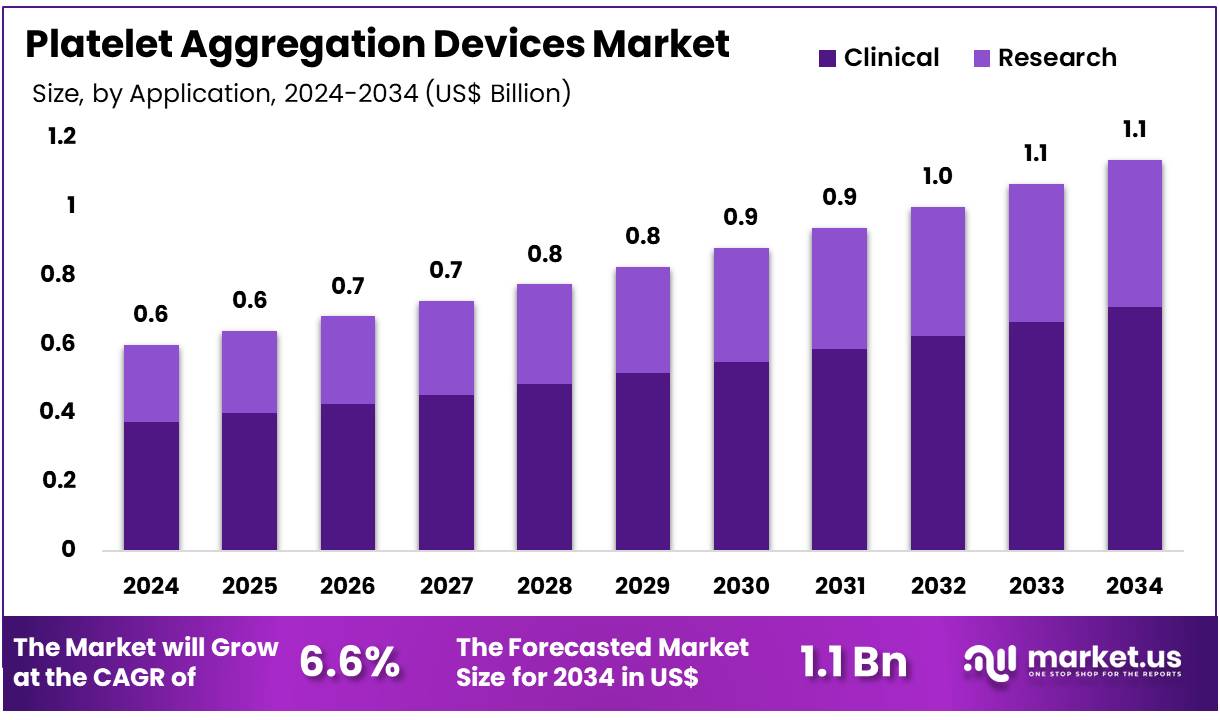

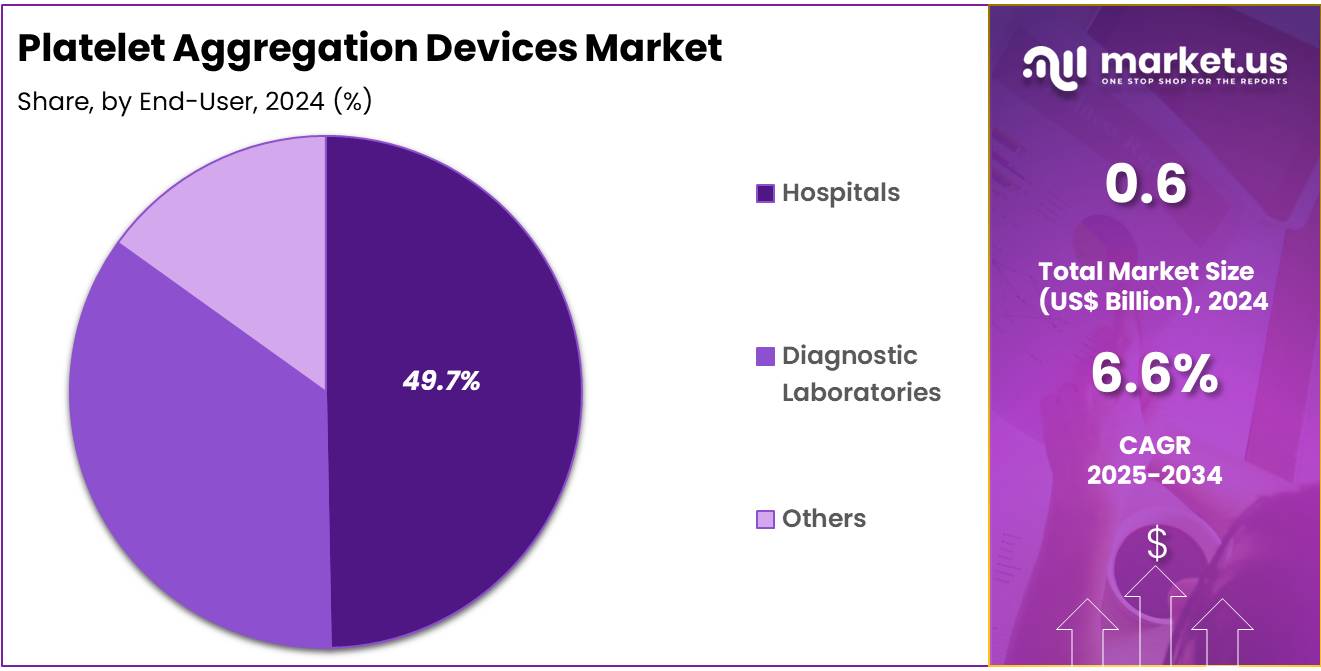

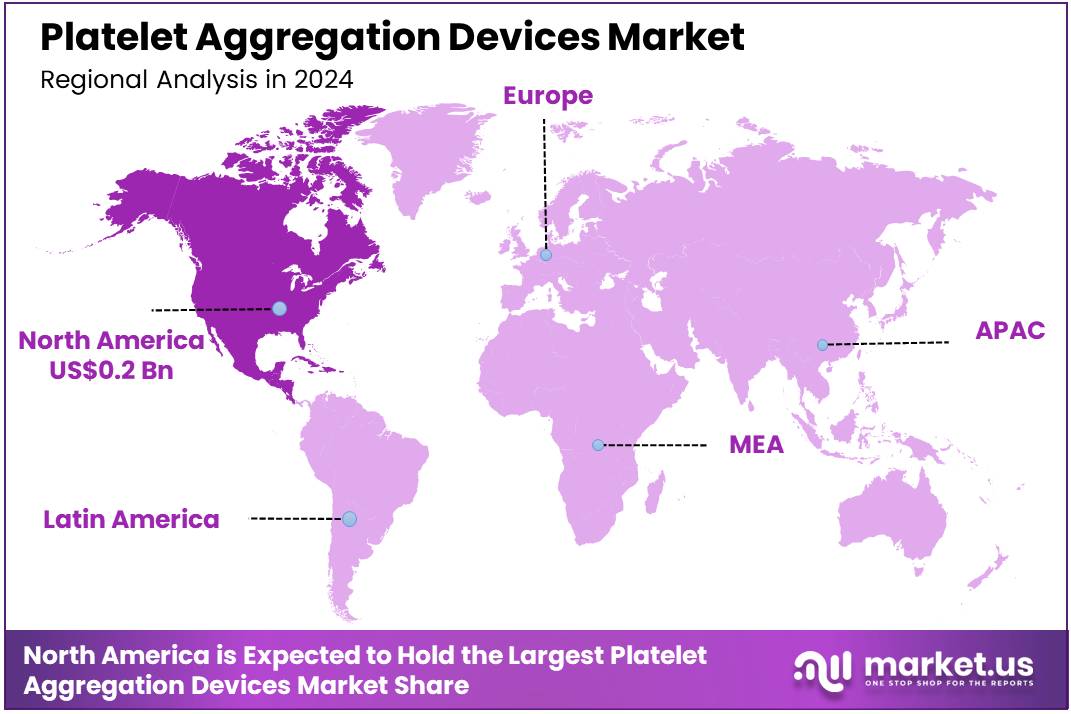

The Global Platelet Aggregation Devices Market size is expected to be worth around US$ 1.1 billion by 2034 from US$ 0.6 billion in 2024, growing at a CAGR of 6.6% during the forecast period 2025 to 2034. In 2023, North America led the market, achieving over 40.1% share with a revenue of US$ 0.2 Billion.

Increasing awareness of the importance of platelet function in cardiovascular health and disease is driving the growth of the platelet aggregation devices market. These devices are crucial for diagnosing and monitoring disorders related to blood clotting, such as thrombosis, bleeding disorders, and cardiovascular diseases. Platelet aggregation tests are essential for assessing platelet function, particularly in patients with risk factors for heart attacks, strokes, and peripheral vascular diseases.

The rising prevalence of chronic conditions, such as hypertension and diabetes, which contribute to clotting disorders, further fuels demand for accurate and efficient platelet aggregation testing. In July 2021, Sysmex Europe GmbH launched the CN-6500 and CN-3500 blood coagulation analyzers, incorporating CLEIA methodology to optimize testing workflows for varied medical requirements. These state-of-the-art analyzers are designed to boost laboratory efficiency while facilitating faster and more accurate diagnosis and treatment in coagulation disorders.

Recent trends in the market show increased adoption of automated platelet aggregation devices, which offer high throughput and enhanced precision, improving patient management and clinical decision-making. Additionally, innovations in point-of-care testing are opening new opportunities for the market, as healthcare providers seek quicker, more accessible diagnostic options. As research into blood disorders and personalized medicine advances, the platelet aggregation devices market is poised for continued growth and innovation.

Key Takeaways

- In 2023, the market for Platelet Aggregation Devices generated a revenue of US$ 6 billion, with a CAGR of 6.6%, and is expected to reach US$ 1.1 billion by the year 2033.

- The product type segment is divided into systems, consumables, reagents, and accessories, with systems taking the lead in 2023 with a market share of 38.6%.

- Considering application, the market is divided into research and clinical. Among these, clinical held a significant share of 62.5%.

- Furthermore, concerning the end-user segment, the market is segregated into diagnostic laboratories, hospitals, and others. The hospitals sector stands out as the dominant player, holding the largest revenue share of 49.7% in the Platelet Aggregation Devices market.

- North America led the market by securing a market share of 40.1% in 2023.

Product Type Analysis

The systems segment led in 2023, claiming a market share of 38.6% owing to the increasing need for accurate and efficient monitoring of platelet function in clinical and research settings. Platelet aggregation systems, which help assess the response of platelets to various stimuli, are projected to see rising demand due to their critical role in diagnosing platelet dysfunction and managing conditions like cardiovascular diseases, bleeding disorders, and thrombosis.

The growing prevalence of these conditions, along with advancements in system technology to enhance accuracy and ease of use, is anticipated to boost the adoption of platelet aggregation systems. Furthermore, as the healthcare industry shifts towards personalized medicine, the demand for sophisticated, reliable systems for platelet testing is likely to increase, driving growth in this segment.

Application Analysis

The clinical held a significant share of 62.5% due to the increasing use of platelet aggregation testing in clinical diagnostics. Healthcare providers are expected to rely more on these devices to monitor patients with thrombotic disorders, cardiovascular diseases, and other conditions that involve platelet dysfunction. As the focus on patient-specific treatment plans and personalized healthcare intensifies, the demand for precise platelet function assessments will likely grow.

The segment’s growth is also supported by the expanding role of platelet aggregation testing in pre-surgical assessments, where it is crucial to assess the risks of bleeding or clotting. The development of more advanced, user-friendly devices is projected to further accelerate the adoption of platelet aggregation devices in clinical environments.

By End-User Analysis

The hospitals segment had a tremendous growth rate, with a revenue share of 49.7% owing to hospitals being major end-users of diagnostic tools for managing patients with cardiovascular diseases, thrombocytopenia, and other platelet-related disorders. Hospitals are expected to continue to be the primary settings for platelet aggregation testing, as these institutions require reliable, high-throughput devices to assist in the diagnosis and treatment of conditions that affect platelet function.

The increasing number of patients with heart diseases, diabetes, and bleeding disorders is anticipated to drive hospitals to adopt more advanced platelet aggregation devices. Additionally, as hospitals prioritize early detection and precise monitoring of platelet activity for better treatment outcomes, the demand for platelet aggregation devices is likely to continue growing, reinforcing the segment’s expansion.

Key Market Segments

Product Type

- Systems

- Consumables

- Reagents

- Accessories

Application

- Research

- Clinical

End-user

- Diagnostic Laboratories

- Hospitals

- Others

Drivers

Increasing Prevalence of Cardiovascular and Circulatory Diseases Driving the Platelet Aggregation Devices Market

Increasing prevalence of cardiovascular and circulatory diseases is anticipated to drive the platelet aggregation devices market significantly. Data from the British Heart Foundation in June 2023 revealed that cardiovascular and circulatory diseases accounted for approximately one-third of global deaths, with 20.5 million fatalities recorded in 2021.

This growing burden highlights the urgent need for advanced diagnostic tools to assess platelet function and manage clotting disorders effectively. Platelet aggregation devices play a critical role in identifying abnormalities that contribute to conditions like heart attacks and strokes. Healthcare providers increasingly adopt these devices to enhance the precision of treatment strategies for patients at risk of thrombotic events. Technological advancements, such as microfluidics and optical-based detection systems, improve diagnostic accuracy and ease of use.

Pharmaceutical companies utilize platelet aggregation testing in drug development to evaluate the efficacy and safety of antiplatelet therapies. Rising awareness about preventive healthcare and early diagnosis fosters the adoption of these devices in clinical settings. Governments and research institutions expand funding for cardiovascular diagnostics, boosting market growth.

Collaborations between device manufacturers and healthcare facilities enhance the accessibility of innovative platelet aggregation solutions. These trends underscore the essential role of platelet testing in addressing the global burden of circulatory diseases.

Restraints

High Costs Are Restraining the Platelet Aggregation Devices Market

High costs associated with platelet aggregation devices are restraining the market. Advanced technologies, such as optical and impedance-based systems, require substantial investment in manufacturing, increasing their overall price. Smaller healthcare facilities often face financial constraints, limiting their ability to adopt these devices. The cost of consumables, including reagents and calibration kits, further adds to operational expenses. Limited insurance coverage for platelet aggregation tests in many regions discourages routine usage.

In low-income countries, inadequate healthcare infrastructure and restricted budgets reduce access to these advanced diagnostic tools. Training requirements for operating complex systems increase expenses for hospitals and diagnostic labs. Addressing these challenges requires cost-efficient innovations and broader insurance coverage to improve the affordability and accessibility of platelet aggregation devices.

Opportunities

Rising R&D Activities as an Opportunity for the Platelet Aggregation Devices Market

Rising R&D activities are anticipated to create significant opportunities for the platelet aggregation devices market. In October 2023, researchers at the University of Birmingham developed innovative nanobodies capable of regulating platelet clumping, marking a major advancement in medical science. These nanobodies pave the way for new diagnostic tools and therapies targeting clotting disorders. Pharmaceutical companies increasingly invest in research to refine platelet aggregation devices for enhanced accuracy and efficiency.

Integration of nanotechnology and bioengineering enables the development of portable and cost-effective diagnostic systems. Collaborative efforts between academic institutions and industry players accelerate the commercialization of novel solutions. Expanding government funding for cardiovascular and hematological research supports the innovation pipeline in platelet testing technologies.

These advancements improve diagnostic precision, addressing the growing demand for effective tools in managing cardiovascular conditions. These trends position rising R&D activities as a key driver for growth in the platelet aggregation devices market.

Impact of Macroeconomic / Geopolitical Factors

Macroeconomic and geopolitical factors significantly affect the platelet aggregation devices market. On the positive side, increasing global investments in healthcare, particularly in cardiovascular diseases and surgical procedures, drive the demand for advanced diagnostic tools and treatment devices, including platelet aggregation devices. Rising awareness of platelet function testing and the need for effective patient management further contribute to market growth.

However, economic recessions or budget cuts in healthcare systems may limit spending on high-cost devices, potentially slowing market adoption. Geopolitical factors, such as trade restrictions and regulatory differences, can disrupt the supply chain and impact the availability of essential components.

Additionally, political instability and fluctuating exchange rates can hinder international market expansion. Despite these challenges, the growing emphasis on early diagnosis, better patient outcomes, and improved treatment methods ensures a continued positive trajectory for the market.

Latest Trends

Launch of Novel Products Driving the Platelet Aggregation Devices Market:

Rising launches of novel products play a crucial role in driving the platelet aggregation devices market. High levels of innovation in medical technology are expected to enhance the accuracy, efficiency, and usability of platelet aggregation testing devices. The growing demand for personalized healthcare and more precise diagnostic tools is likely to increase the adoption of these advanced systems.

In February 2022, Futura Surgicare Pvt Ltd introduced a new product, Hemostax, under the Dolphin Hemostats brand. This absorbable hemostatic solution was developed to help surgeons manage bleeding more effectively during procedures, aiming to improve surgical outcomes and patient care. As the market continues to see such innovations, the availability of more advanced and user-friendly products is anticipated to drive further growth in the platelet aggregation devices sector.

Regional Analysis

North America is leading the Platelet Aggregation Devices Market

North America dominated the market with the highest revenue share of 40.1% owing to an increasing demand for accurate diagnostic tools to monitor blood disorders, including conditions like leukemia, lymphoma, and myeloma. Data from the Leukemia & Lymphoma Society indicated that leukemia, lymphoma, and myeloma were expected to contribute to 9.4% of nearly 1.96 million new cancer diagnoses in the U.S. Non-Hodgkin lymphoma (NHL), a highly prevalent cancer, made up roughly 4% of all cancer cases nationwide, further highlighting the need for advanced diagnostic and therapeutic tools.

Platelet aggregation devices, which play a critical role in assessing platelet function, have become essential in diagnosing and managing hematologic conditions, particularly in patients undergoing chemotherapy or dealing with bleeding disorders. The growing focus on personalized medicine, increasing healthcare awareness, and advancements in device technology have further fueled the demand for platelet aggregation devices.

As the healthcare sector continues to invest in advanced diagnostics, the market for platelet aggregation devices in North America is expected to continue its expansion, contributing to improved patient outcomes in blood-related diseases.

The Asia Pacific region is expected to experience the highest CAGR during the forecast period

Asia Pacific is expected to grow with the fastest CAGR owing to an increasing prevalence of cardiovascular diseases, rising healthcare investments, and advancements in diagnostic technology. Countries like China, India, and Japan are expected to experience higher demand for platelet aggregation devices as the incidence of heart disease, stroke, and other thrombotic disorders continues to rise.

The growing aging population in the region, coupled with the increasing focus on early diagnosis and personalized treatment, is likely to drive the adoption of platelet aggregation testing. Additionally, as healthcare systems in Asia Pacific continue to improve, governments and healthcare providers are expected to invest in more advanced diagnostic technologies.

The increasing prevalence of lifestyle-related diseases, such as hypertension and diabetes, which contribute to cardiovascular conditions, will further stimulate the need for effective platelet function tests. With the rising demand for accurate, reliable, and non-invasive diagnostic tools, the platelet aggregation devices market in Asia Pacific is anticipated to expand significantly in the coming years.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia

- Netherland

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- New Zealand

- Singapore

- Thailand

- Vietnam

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Key Players Analysis

Key players in the platelet aggregation devices market focus on developing advanced analyzers and consumables to improve diagnostic accuracy and efficiency in assessing platelet function. Companies invest in R&D to expand applications in areas like cardiovascular disease management, bleeding disorders, and drug monitoring.

Collaborations with healthcare providers and research institutions enhance innovation and promote technology adoption. Geographic expansion into regions with rising healthcare investments and growing awareness of platelet disorders supports market growth. Many players also emphasize compliance with regulatory standards and affordability to ensure accessibility and reliability.

Haemonetics Corporation is a leading company in this market, offering innovative solutions such as the TEG platelet mapping system. The company focuses on integrating advanced technology with user-friendly designs to provide precise and reliable diagnostics. Haemonetics’ global presence and dedication to improving patient outcomes position it as a key player in platelet function analysis.

Top Key Players

- Werfen

- Sysmex Corporation

- Siemens Healthcare GmbH

- Precision BioLogic

- Haemonetics Corporation

- Futura Surgicare

- Hoffmann-La Roche Ltd

- Chrono-Log Corporation

Recent Developments

- In May 2022, Precision BioLogic Inc. introduced the CRYOcheck Chromogenic Factor IX assay in regions such as Australia, Canada, the UK, the EU, and New Zealand. This innovative assay is designed to improve hemophilia B diagnosis and management by providing accurate results and seamless integration with advanced laboratory equipment.

- In February 2022, Futura Surgicare launched Hemostax, a novel absorbable hemostatic product under its Dolphin Hemostats brand. Made from oxidized regenerated cellulose, Hemostax is engineered to assist surgeons in effectively managing bleeding during surgeries, enhancing procedural efficiency and patient care outcomes.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2024) | US$ 0.6 billion |

| Forecast Revenue (2034) | US$ 1.1 billion |

| CAGR (2024-2033) | 6.6% |

| Base Year for Estimation | 2023 |

| Historic Period | 2020-2023 |

| Forecast Period | 2025-2034 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Product Type (Systems, Consumables, Reagents, and Accessories), By Application (Research and Clinical), By End-user (Diagnostic Laboratories, Hospitals, and Others) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, New Zealand, Singapore, Thailand, Vietnam, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA |

| Competitive Landscape | Werfen, Sysmex Corporation, Siemens Healthcare GmbH, Precision BioLogic, Haemonetics Corporation, Futura Surgicare, F. Hoffmann-La Roche Ltd, and Chrono-Log Corporation. |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |