Quick Navigation

Report Scope

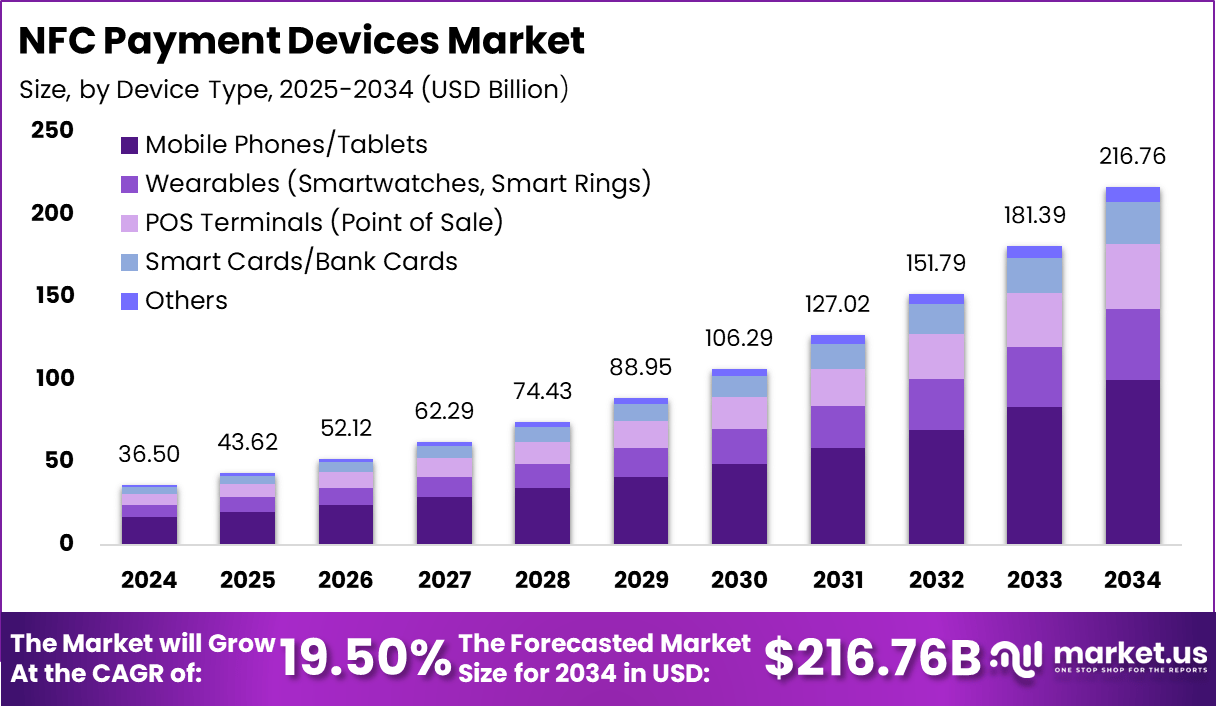

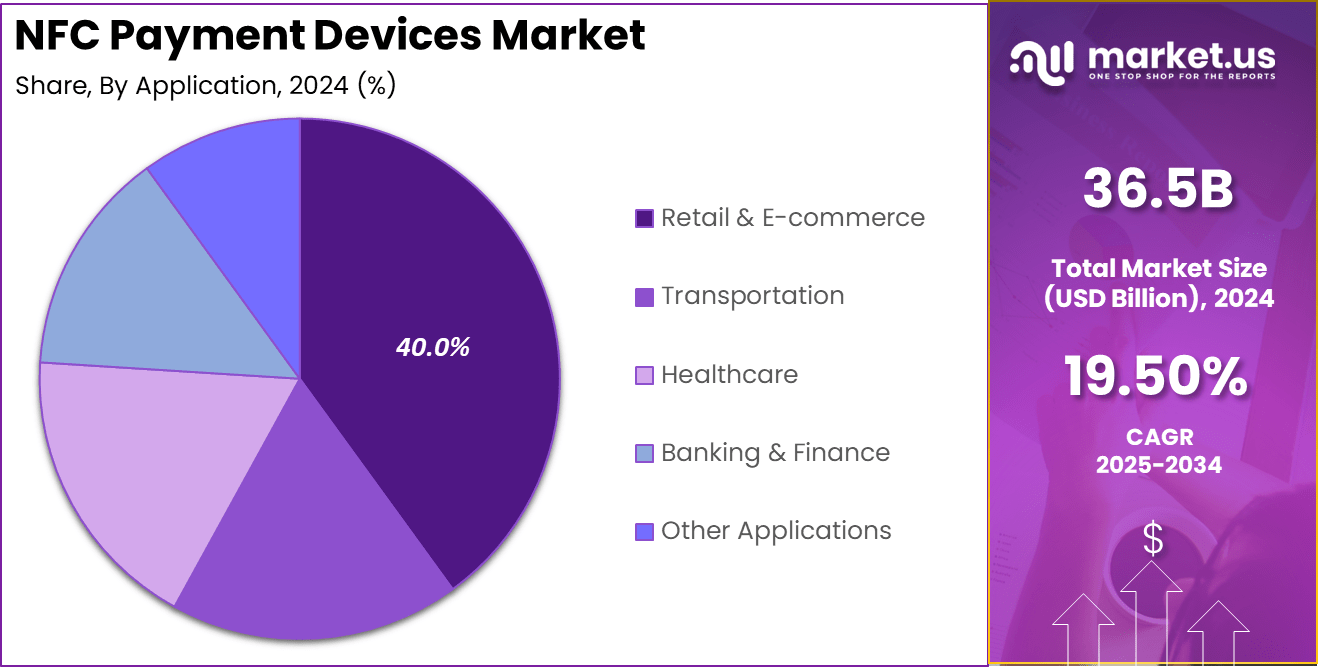

The Global NFC Payment Devices Market is expected to be worth around USD 216.76 Billion by 2034, up from USD 36.5 Billion in 2024. It is expected to grow at a CAGR of 19.50% from 2025 to 2034.

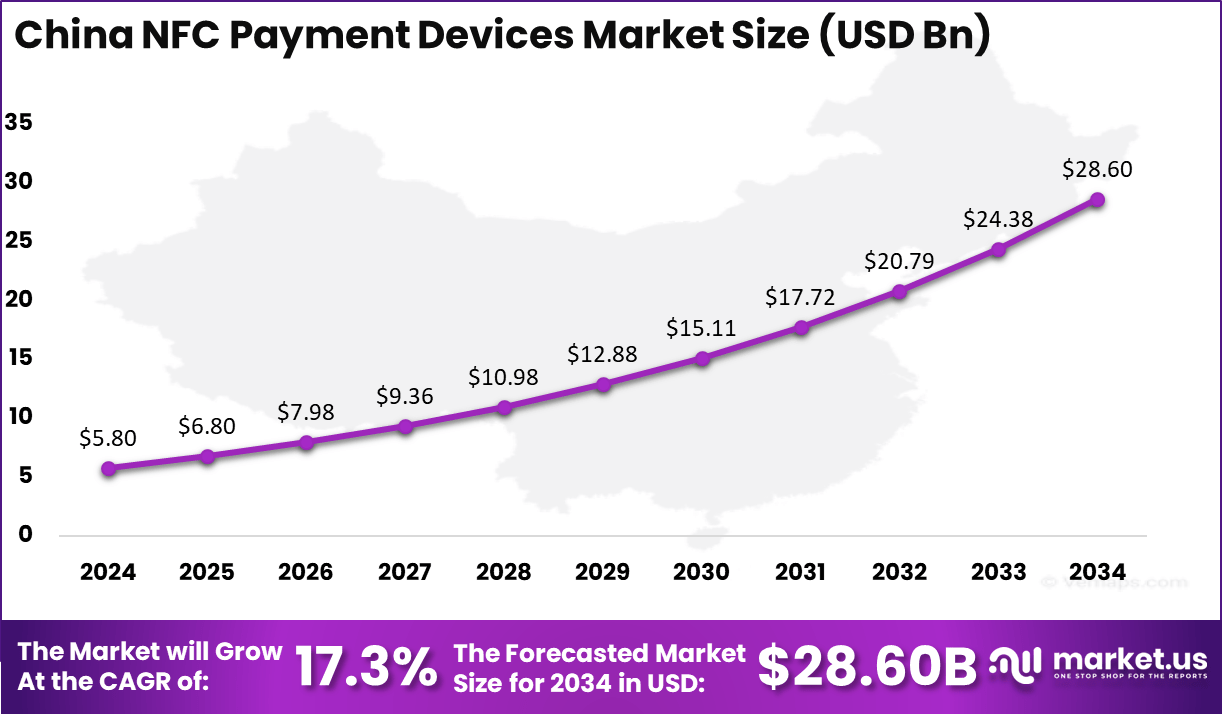

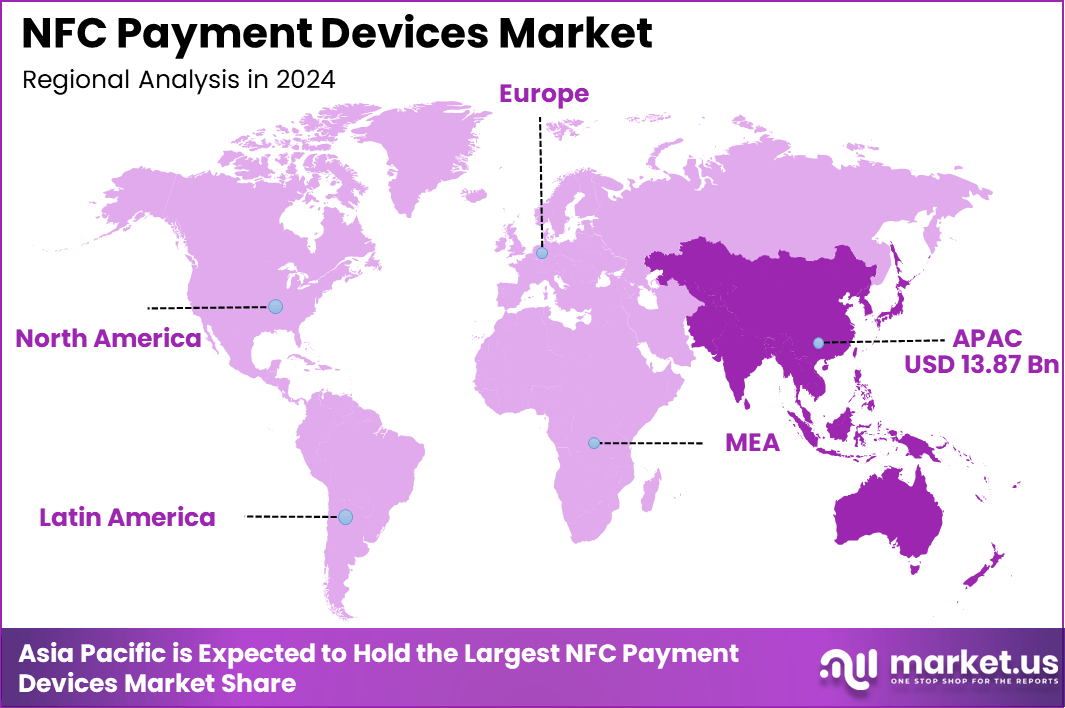

In 2024, Asia-Pacific held a dominant market position, capturing over a 38% share and earning USD 13.87 Billion in revenue. Further, China dominates the market by USD 5.8 Billion, steadily holding a strong position with a CAGR of 17.3%.

The NFC (Near Field Communication) payment devices market has witnessed significant growth in recent years, driven by the increasing adoption of contactless payment solutions. NFC technology enables secure and swift transactions by allowing devices to communicate when nearby, typically within a few centimeters.

This technology has been integrated into various devices, including smartphones, smartwatches, payment wristbands, and smart rings, facilitating seamless payment experiences for consumers.

Several factors are propelling the growth of the NFC payment devices market. The global shift from traditional payment systems to digital platforms has played a crucial role. Consumers increasingly favor contactless payments due to their convenience, speed, and enhanced security features.

The COVID-19 pandemic further accelerated this trend, as contactless transactions minimize physical contact, aligning with health and safety concerns. Additionally, the widespread adoption of smartphones equipped with NFC capabilities has made it easier for consumers to embrace this technology.

Key Takeaways

- Market Growth: The NFC payment devices market is projected to grow from USD 36.5 billion in 2024 to USD 216.76 billion by 2034, reflecting a CAGR of 19.50%.

- Dominant Device Type: Mobile phones and tablets account for the largest share of NFC payment devices, contributing 46% of the market.

- Leading Application: Retail & e-commerce is the primary sector driving demand, holding a 40% market share.

- Regional Growth: The Asia-Pacific region leads global adoption, contributing 38% of the market share.

- China’s Contribution: China alone is expected to generate USD 5.8 billion in NFC payment transactions, with a CAGR of 17.3%.

- Strong Adoption Trends: Growing smartphone penetration, rising preference for contactless transactions, and advancements in security technologies are driving market expansion.

Analysts’ Viewpoint

The demand for NFC payment devices is on the rise across various sectors. Retailers, restaurants, and service providers increasingly adopt contactless payment systems to enhance customer experience and streamline operations.

The integration of NFC technology into wearable devices like smartwatches and fitness trackers has also contributed to market demand, offering consumers more flexibility in how they make payments. Furthermore, the push towards cashless economies in several countries has encouraged businesses to adopt NFC-enabled payment solutions.

The NFC payment devices market presents numerous opportunities for innovation and expansion. The integration of NFC technology with the Internet of Things (IoT) opens up possibilities for smart appliances and connected devices to facilitate payments, creating a more interconnected ecosystem.

Emerging markets, where smartphone penetration is rapidly increasing, offer substantial growth potential for NFC payment solutions. Additionally, collaborations between financial institutions and tech companies can lead to the development of new applications and services, further driving market growth.

Technological advancements continue to shape the NFC payment devices landscape. Enhanced security protocols, such as tokenization and biometric authentication, have made NFC transactions more secure, addressing previous concerns about data breaches and fraud.

The development of NFC-enabled wearables has expanded the usability of contactless payments beyond traditional cards and smartphones, providing consumers with more options. Moreover, improvements in battery life and device durability have made NFC payment devices more reliable and user-friendly, encouraging broader adoption.

Key Statistics

User Base and Adoption

- Smartphone Penetration: About 94% of all smartphones globally are NFC-enabled.

- Contactless Cards: By 2026, 81% of all cards are expected to be contactless.

- NFC Users: Approximately 1.3 billion users worldwide use NFC payments.

- Mobile Payment Users: Projected to reach 1.7 billion by 2027.

Usage Statistics

- Contactless Transactions: In 2020, contactless card payments surged to 3.7 billion transactions in North America, amounting to USD 110 billion.

- NFC Mobile Payments in the USA: Expected to rise to 3 billion by 2027 from 4.4 billion in 2022.

- Average Transaction Value: Approximately USD 15 per transaction.

Quantity and Production

- NFC-enabled Devices Produced: Over 1.5 billion devices are produced annually.

- Smartphones Produced: Approximately 1.4 billion smartphones are produced each year, with most being NFC-enabled.

Device Types

- Smartphones: Dominated the NFC payments market in 2022, accounting for about 80% of all NFC transactions.

- Smartwatches and Fitness Trackers: Part of the growing wearable payment segment, with over 100 million units sold annually.

Regional Analysis

China Region Market Size

In Asia-Pacific, China dominates the market, reaching a market size of USD 5.8 billion. The country continues to hold a strong position, with a CAGR of 17.3%, driven by government initiatives promoting a cashless economy, increasing smartphone penetration, and the widespread use of digital wallets. As a result, China remains at the forefront of NFC payment adoption, shaping the future of contactless transactions.

The market is rapidly expanding as consumers and businesses shift towards seamless digital transactions. The growing reliance on mobile phones and tablets, which account for 46% of NFC payment devices, underscores the convenience and efficiency of this technology.

Retail & e-commerce remains the dominant application segment, holding a 40% market share. The surge in online shopping and in-store contactless payments is fueling demand for NFC-enabled devices. Businesses are increasingly integrating NFC payment solutions to enhance customer experience and streamline transactions.

Asia-Pacific is leading the global NFC payment devices market, capturing 38% of the total market share. The region’s rapid digital transformation and the widespread adoption of smartphones contribute to this dominance.

Asia Pacific Market Size

In 2024, the Asia-Pacific (APAC) region held a dominant position in the NFC payment devices market, capturing more than a 38% share and generating approximately USD 13.87 billion in revenue. This leadership is primarily attributed to the region’s rapid technological adoption and the widespread integration of NFC technology in consumer electronics.

Several factors contribute to APAC’s prominence in this market. The increasing demand for advanced manufacturing hubs for consumer electronics and automobiles in countries such as China and India has created significant opportunities for the near-field communication market in the region. Higher adoption of NFC in electronic gadgets such as smartphones and credit cards has fueled market growth.

Moreover, the region’s dense population and the proliferation of smartphones have accelerated the shift towards digital payments. Governments in countries like India have implemented initiatives to promote cashless transactions, further boosting the adoption of NFC-enabled payment methods. Additionally, the rise of e-commerce platforms and the integration of NFC technology into public transportation systems have expanded the use cases for NFC payments, making them an integral part of daily life in APAC.

The competitive landscape in APAC is also a driving force behind its market dominance. Local companies are investing heavily in NFC technology, leading to innovative payment solutions tailored to the region’s unique needs. This localized approach, combined with strategic partnerships between technology providers and financial institutions, has created a robust ecosystem that supports the widespread adoption of NFC payment devices across various sectors.

By Device Type

In 2024, the Mobile Phones/Tablets segment held a dominant position in the NFC payment devices market, capturing more than a 46% share. This leadership is primarily due to the widespread adoption of smartphones and tablets equipped with NFC capabilities, facilitating contactless payments.

The convenience of using mobile devices for transactions has led to a significant shift towards digital wallets and mobile banking applications. Consumers appreciate the ease and speed of tapping their devices to make payments, reducing reliance on cash and physical cards.

Additionally, the integration of NFC technology into a vast array of mobile applications has expanded its utility beyond payments, including functionalities like access control and information sharing, further solidifying the prominence of mobile phones and tablets in the NFC payment ecosystem.

By Application

In 2024, the Retail & E-commerce segment held a dominant position in the NFC payment devices market, capturing more than a 40% share. This leadership is primarily due to the widespread integration of NFC technology in retail environments, enabling swift and secure contactless transactions.

Consumers increasingly favor the convenience of tapping their NFC-enabled devices for payments, reducing reliance on cash and enhancing the shopping experience. The surge in e-commerce has further propelled this trend, with online retailers adopting NFC for seamless payment processes.

Additionally, the COVID-19 pandemic accelerated the shift towards contactless payments, as both consumers and retailers sought safer transaction methods. Loyalty programs and personalized marketing initiatives have also benefited from NFC technology, allowing retailers to engage customers more effectively.

Overall, the convergence of consumer preferences, technological advancements, and health considerations has solidified the Retail & E-commerce segment’s leading position in the NFC payment devices market.

Key Market Segments

By Device Type

- Mobile Phones/Tablets

- Wearables (Smartwatches, Smart Rings)

- POS Terminals (Point of Sale)

- Smart Cards/Bank Cards

- Others

By Application

- Retail & E-commerce

- Transportation

- Healthcare

- Banking & Finance

- Other Applications

Driving Factors

Shift Towards Digital Payment Systems

The global transition from traditional payment methods to digital platforms has been a significant driving force behind the growth of NFC payment devices. Consumers are increasingly seeking faster, more convenient, and secure ways to conduct transactions, leading to the widespread adoption of contactless payment solutions.

NFC technology facilitates quick transactions by allowing devices to communicate wirelessly over short distances, enhancing the overall user experience. This shift is not limited to developed nations; emerging markets are also embracing digital payments, propelled by the proliferation of smartphones and improved internet connectivity.

The COVID-19 pandemic further accelerated this trend, as contactless payments minimize physical contact, aligning with health and safety concerns. Businesses across various sectors, including retail, hospitality, and transportation, have integrated NFC-enabled payment systems to meet evolving consumer preferences. Governments and financial institutions worldwide are supporting this transition by implementing policies and infrastructures that promote digital transactions.

Restraining Factors

Security Concerns Among Consumers

Despite the advantages of NFC payment devices, security concerns remain a significant barrier to their widespread adoption. Many consumers are apprehensive about the potential risks associated with contactless payments, such as unauthorized transactions and data breaches. The absence of PIN authorization during NFC transactions can lead to vulnerabilities, especially if a device is lost or stolen.

A 2023 survey highlighted this concern, revealing that approximately 35% of respondents who chose not to use mobile wallets cited security concerns as their primary reason. This apprehension is further exacerbated by reports of cyberattacks targeting digital payment systems. To address these issues, industry stakeholders are investing in advanced security measures, such as biometric authentication and tokenization, to protect user data.

However, building consumer trust requires not only technological solutions but also comprehensive education on the safety and reliability of NFC payments. Overcoming these security concerns is crucial for the sustained growth of the NFC payment devices market.

Growth Opportunities

Integration with Wearable Technology

The convergence of NFC technology with wearable devices presents a significant growth opportunity in the payment industry. Wearables such as smartwatches, fitness trackers, and smart rings equipped with NFC capabilities offer users the convenience of making swift transactions without the need for smartphones or physical cards.

This integration aligns with the increasing consumer demand for multifunctional devices that support a seamless lifestyle. Major technology companies are investing in this space, developing innovative products that cater to the growing preference for contactless payments.

Challenging Factors

Regulatory and Standardization Issues

The NFC payment devices market faces challenges related to regulatory compliance and the lack of standardized protocols across different regions. Varying regulations concerning data protection, transaction authentication, and financial reporting create complexities for companies operating in multiple markets.

For instance, the European Union’s General Data Protection Regulation (GDPR) imposes stringent requirements on handling user data, affecting how NFC payment services are implemented. Additionally, the absence of universal standards for NFC technology leads to compatibility issues between devices and payment terminals, hindering seamless user experiences.

These discrepancies can slow down the adoption rate of NFC payments, as businesses may be reluctant to invest in technologies that lack interoperability. Addressing these challenges requires collaborative efforts among industry stakeholders, policymakers, and standardization bodies to develop harmonized regulations and technical standards.

Growth Factors

Rising Adoption of Contactless Payments

The global shift towards contactless payments is a significant growth driver for the NFC payment devices market. Consumers increasingly prefer quick and secure transaction methods, leading to a surge in NFC-enabled payment solutions.

This remarkable growth underscores the escalating demand for seamless payment experiences. Additionally, the COVID-19 pandemic has accelerated the adoption of contactless payments, as consumers and businesses seek safer transaction methods to minimize physical contact. This trend is expected to continue, further propelling the NFC payment devices market.

Emerging Trends

Integration with Wearable Technology

A notable emerging trend in the NFC payment devices market is the integration of NFC technology into wearable devices. Smartwatches, fitness trackers, and even smart rings equipped with NFC capabilities allow users to make payments effortlessly.

This convergence of technology enhances user convenience and aligns with the growing demand for multifunctional devices. The integration of NFC into wearables is a significant contributor to this growth, offering users a seamless and efficient payment experience.

Business Benefits

Enhanced Customer Experience and Operational Efficiency

Implementing NFC payment solutions offers businesses substantial benefits, including improved customer experience and operational efficiency. Contactless payments streamline the transaction process, reducing checkout times and enhancing customer satisfaction.

For example, in 2018, the Westpac Banking Corporation in Australia revealed that contactless payments approached saturation point by being used in over 90% of purchases. This high adoption rate indicates that customers value the speed and convenience of NFC payments.

Additionally, businesses benefit from faster transaction processing, leading to increased throughput and reduced operational bottlenecks. The integration of NFC technology also supports loyalty programs and personalized marketing strategies, further enhancing customer engagement and driving sales growth.

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia

- Netherlands

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Singapore

- Thailand

- Vietnam

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Key Player Analysis

Apple has consistently led the wearable technology market with its innovative product launches, particularly the Apple Watch series. In 2019 alone, Apple sold approximately 31 million Apple Watches, surpassing the entire Swiss watch industry in sales.

The company’s focus on integrating advanced health monitoring features, such as ECG and blood oxygen sensors, has set it apart from competitors. Apple continues to enhance its wearable offerings, maintaining a strong market presence through continuous innovation.

Fitbit, once a pioneer in the fitness tracker market, faced challenges as competitors like Apple entered the wearable space. In November 2019, Google announced plans to acquire Fitbit for $2.1 billion, aiming to bolster its position in the wearable technology sector. The acquisition, finalized in January 2021, marked a significant shift for Fitbit, integrating its health and fitness expertise into Google’s ecosystem.

Garmin has carved a niche in the wearable market by focusing on high-quality fitness trackers and smartwatches tailored for outdoor and fitness enthusiasts. In October 2024, Garmin reported robust financial performance, raising its full-year revenue forecast to approximately $6.12 billion, driven by strong demand for its wearable products.

Top Key Players in the Market

- Apple, Inc.

- Fitbit, Inc.

- Gramin Ltd

- Huawei Technologies Co., Ltd.

- Jakcom Technology Co. Inc.

- McLear Ltd.

- Nymi, Inc.

- Samsung Electronics Co. Ltd.

- Sony Corporation

- Xiaomi Corporation

- Ingenico Group

- Verifone Systems, Inc.

- Other Key Players

Recent Developments

- In 2024, Apple announced that it would allow third-party developers to access its NFC chip, enabling in-store tap payments and potentially using wallets other than Apple Pay.

- In 2024, Vipps, a Norwegian payment app, became the first service to utilize iOS’s more open ecosystem, allowing users in Norway to make tap-to-pay transactions and set it as the default payment option on their iPhones.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2024) | USD 36.5 Billion |

| Forecast Revenue (2034) | USD 216.76 Billion |

| CAGR (2025-2034) | 19.50% |

| Largest Market | North America |

| Base Year for Estimation | 2024 |

| Historic Period | 2020-2023 |

| Forecast Period | 2025-2034 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Device Type (Mobile Phones/Tablets, Wearables (Smartwatches, Smart Rings), POS Terminals (Point of Sale), Smart Cards/Bank Cards, Others), By Application (Retail & E-commerce, Transportation, Healthcare, Banking & Finance, Other Applications), By Revenue Model (Subscription-Based, Ad-Supported, Pay-Per-View, Others) |

| Regional Analysis | North America (US, Canada), Europe (Germany, UK, Spain, Austria, Rest of Europe), Asia-Pacific (China, Japan, South Korea, India, Australia, Thailand, Rest of Asia-Pacific), Latin America (Brazil), Middle East & Africa(South Africa, Saudi Arabia, United Arab Emirates) |

| Competitive Landscape | Apple, Inc., Fitbit, Inc., Gramin Ltd, Huawei Technologies Co., Ltd., Jakcom Technology Co. Inc., McLear Ltd., Nymi, Inc., Samsung Electronics Co. Ltd., Sony Corporation, Xiaomi Corporation, Ingenico Group, Verifone Systems, Inc., Other Key Players |

| Customization Scope | We will provide customization for segments and at the region/country level. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |