Quick Navigation

Report Scope

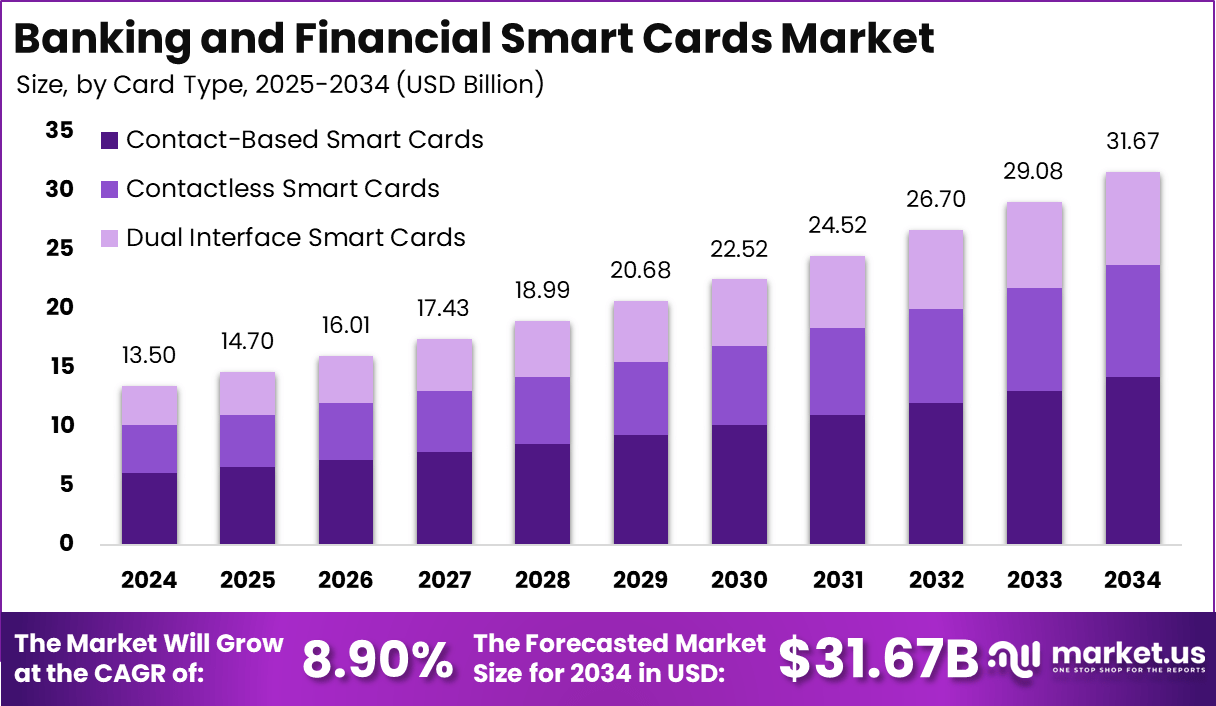

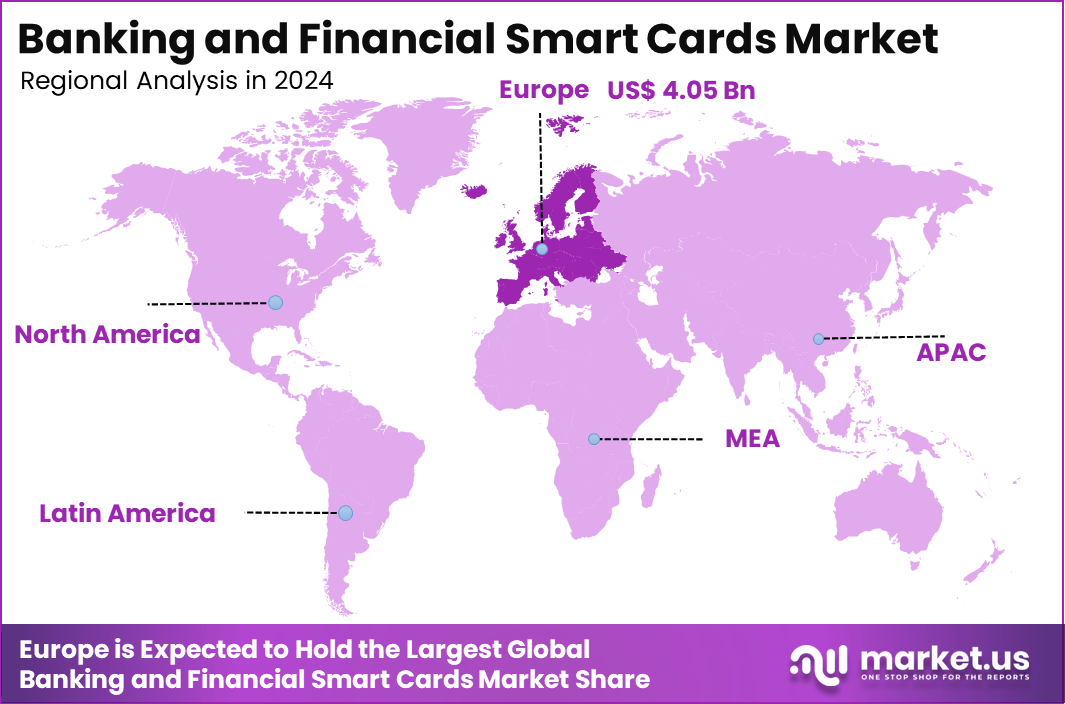

The Global Banking and Financial Smart Cards Market is expected to be worth around USD 31.67 Billion By 2034, up from USD 13.5 Billion in 2024. It is expected to grow at a CAGR of 8.90% from 2025 to 2034. In 2024, Europe held a dominant market position, capturing over a 30% share and earning USD 4.05 Billion in revenue.

The Banking and Financial Smart Cards Market has been rapidly evolving due to the growing adoption of advanced digital payment solutions. These smart cards, which include chip-enabled credit cards, debit cards, and prepaid cards, are designed to provide secure, convenient, and efficient payment methods for consumers and businesses alike. Smart cards store encrypted data and enable secure transactions through technologies like EMV chips and contactless payments, making them an essential component in modern financial systems.

The market’s growth is fueled by the increasing reliance on cashless transactions, the expansion of e-commerce, and the rise in demand for mobile banking solutions. As consumers and businesses alike seek enhanced security and faster transaction methods, smart cards are becoming a key tool in facilitating these needs, especially in regions like North America, Europe, and Asia-Pacific.

Several factors are driving the growth of the Banking and Financial Smart Cards Market. One of the most significant drivers is the growing demand for secure payment methods. With rising concerns about data breaches, fraud, and cybercrime, consumers and businesses are increasingly seeking more secure payment alternatives.

Smart cards, particularly those embedded with EMV chips and contactless payment technology, provide a higher level of security than traditional magnetic stripe cards. According to the EMV Migration Forum, over 90% of global card payments were processed using EMV-enabled cards in 2023, reflecting the increasing adoption of chip-enabled technology.

Additionally, the growing trend toward cashless payments is contributing to the market’s expansion. According to a 2023 report by the World Bank, almost 70% of global payments were cashless, especially in developed regions. The ongoing shift towards digital payment systems, driven by mobile banking apps, e-wallets, and online shopping, is making banking and financial smart cards more popular. With more consumers opting for contactless payments, smart cards are playing a central role in this transformation.

Key Takeaways

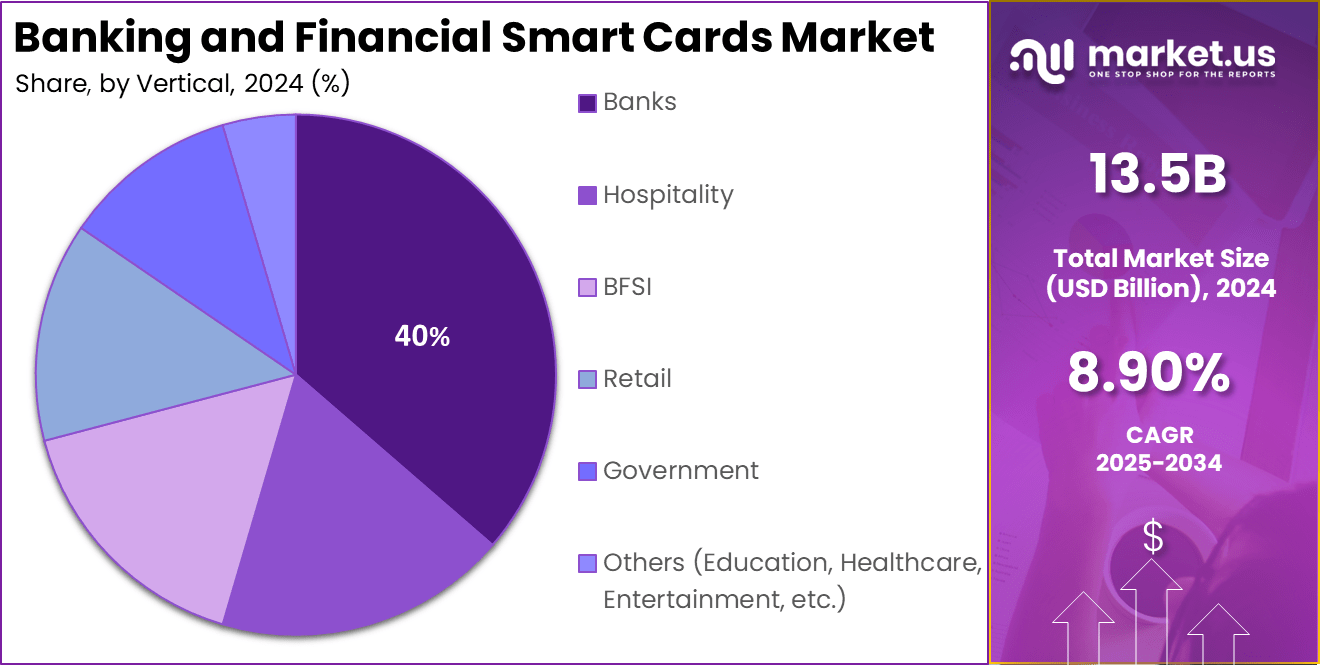

- 2024 Market Value: The market is valued at USD 13.5 Billion in 2024.

- 2034 Market Value: The market is projected to grow to USD 31.67 Billion by 2034, reflecting significant growth potential.

- CAGR: The market is expected to grow at a CAGR of 8.90% from 2024 to 2034.

- By Card Type: Contact-Based Smart Cards hold a dominant share, accounting for 45% of the market.

- By Vertical: Banks are the leading sector, contributing to 40% of the market demand.

- By Region: Europe is the largest market region, capturing 30% of the global market share.

Analyst’s Review

The demand for banking and financial smart cards is increasing as financial institutions and consumers continue to seek more efficient and secure payment solutions. The market is seeing strong demand in both developed and emerging economies, though the drivers of demand differ in each.

In developed economies, high-income consumers prefer contactless cards for fast and secure transactions, especially in retail and public transportation. For example, contactless payment transactions in Europe grew by 30% in 2023, and this growth is expected to continue as more retailers and financial institutions adopt the technology.

The Banking and Financial Smart Cards Market is witnessing several growth opportunities, particularly in emerging economies and through advancements in contactless payment technologies. One of the most promising opportunities is the expansion of financial inclusion.

As smartphone penetration increases in countries like India, China, and Brazil, more consumers are being introduced to digital banking solutions. Financial institutions are capitalizing on this trend by offering smart cards, particularly prepaid cards, to those who do not have access to traditional banking services.

Technological advancements are playing a crucial role in shaping the future of the Banking and Financial Smart card market. One of the most notable innovations is the integration of contactless payment technology, which allows consumers to make payments by simply tapping their cards near a point-of-sale terminal. This NFC (Near Field Communication) technology has revolutionized the payment experience, providing faster, safer, and more convenient transactions.

Key Statistics

Usage and Circulation

- There are between 30 to 50 billion smart cards in circulation globally, including credit cards and SIM cards.

- Asia has about 82.71% of smart card users as of 2021.

Types of Smart Cards

- 40% of smart cards are contact-based, 35% are contactless, and 25% are dual interface.

- Contact cards accounted for the highest share in 2022 due to their wide availability.

Transaction Volume

- The volume of cashless transactions in the Asia-Pacific region was USD 494 billion in 2020 and is projected to increase to USD 1,818 billion by 2030.

- In Europe, the transaction volume was USD 229 billion in 2020 and is expected to grow to USD 522 billion by 2030.

User Base

- By mid-2021, Visa had 93 million contactless smart cards in circulation.

- The user base for smart cards is expanding rapidly due to the increased adoption of contactless payment methods.

Regional Analysis

In 2024, Europe held a dominant market position, capturing more than a 30% share, holding USD 4.05 Billion in revenue, driven by the region’s advanced financial infrastructure and strong adoption of digital payment technologies. Europe’s leading position in the Banking and Financial Smart Cards Market can be attributed to the widespread use of contactless payment technology and the rapid transition to chip-based cards.

The European Union has been a major proponent of EMV card standards (chip and PIN), which have contributed to enhanced security and fraud reduction, leading to high consumer confidence in smart card solutions. As of 2023, over 80% of card payments in Europe were processed through EMV-enabled cards, which bolstered demand for these secure payment methods.

Furthermore, the region benefits from regulatory initiatives that promote digital payment solutions. For instance, the Revised Payment Services Directive (PSD2), which mandates strong customer authentication (SCA), has pushed for the adoption of more secure and innovative payment methods. This has resulted in higher adoption of smart cards across both individual and business users, especially as financial institutions and banks work to comply with stringent security standards.

Another key factor driving Europe’s dominance is the strong presence of global financial institutions and banks, which are major stakeholders in the market. Banks across the region are increasingly investing in advanced payment technologies to offer their customers secure, seamless, and innovative transaction methods. As of 2024, over 40% of the market in Europe is driven by banks, highlighting their critical role in shaping the adoption and growth of smart cards in the region.

Lastly, high smartphone penetration and digital banking are also contributing to the growth of the banking and financial smart cards market in Europe. With more consumers using smartphones for mobile banking, many are transitioning to digital wallets linked to their smart cards, further driving demand for integrated, contactless payment solutions. The shift toward cashless payments in both urban and rural areas of Europe will continue to propel the market forward.

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia

- Netherlands

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Singapore

- Thailand

- Vietnam

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

By Card Type

In 2024, the Contact-Based Smart Cards segment held a dominant market position, capturing more than a 45% share, due to their established use and widespread adoption in various sectors. Contact-based smart cards, which require physical contact with a card reader to initiate a transaction, have long been the standard for secure payment solutions.

Their popularity can be attributed to their proven security features, such as EMV chip technology, which offers enhanced protection against fraud and unauthorized access. As of 2023, over 80% of card payments in Europe and North America were made using contact-based smart cards, cementing their position as the go-to solution for financial transactions.

Additionally, the adoption of contact-based smart cards has been driven by the established infrastructure in banks and financial institutions, which continue to roll out these cards as part of their security and payment systems.

While contactless cards are gaining traction, contact-based smart cards remain essential in business transactions, especially in industries that prioritize security, such as government services, corporate environments, and high-value transactions. Despite the growing popularity of newer card types, the reliability and security of contact-based smart cards ensure they maintain a leading market share.

By Vertical

In 2024, the Banks segment held a dominant market position, capturing more than a 40% share of the Banking and Financial Smart Cards market, driven by the essential role that banks play in issuing payment cards and managing financial transactions.

Banks have been the primary adopters of smart card technologies, including EMV chip cards and contactless payment solutions, to enhance security, reduce fraud, and improve customer experience. With an increasing global shift towards cashless payments, banks are expanding their portfolio of payment solutions, offering a mix of credit, debit, and prepaid smart cards to meet diverse customer needs.

Banks are also key players in driving digital banking transformations by integrating mobile wallets and smart card solutions, aligning with customer demands for faster and safer transactions. Additionally, regulatory frameworks like PSD2 in Europe and GDPR have further pushed banks to invest in secure payment methods, strengthening the adoption of smart cards.

As of 2024, banks continue to dominate the market, leveraging their customer base, infrastructure, and financial expertise to lead in the development and distribution of smart cards across various demographics, from individual consumers to businesses.

Key Market Segments

By Card Type

- Contact-Based Smart Cards

- Contactless Smart Cards

- Dual Interface Smart Cards

By Vertical

- Banks

- Hospitality

- BFSI

- Retail

- Government

- Others (Education, Healthcare, Entertainment, etc.)

Driving Factors

Increasing Demand for Secure Payment Solutions

One of the primary driving factors for the Banking and Financial Smart Cards Market is the rising demand for secure payment solutions. With an increase in digital payment methods and the growing prevalence of online transactions, consumers and financial institutions are becoming more aware of the vulnerabilities that exist in traditional payment systems.

Fraud prevention and data security have thus become top priorities for both individuals and banks. Smart cards, particularly those with EMV chip technology and contactless payment capabilities, provide a secure way to process transactions. These cards use encrypted data and two-factor authentication to ensure that personal information is protected, making them less susceptible to data breaches compared to traditional magnetic stripe cards.

As cybercrime and card fraud continue to rise globally, more countries are implementing regulations that push for security-enhanced payment systems, such as the EMV standard for chip cards. For instance, the EU’s PSD2 directive and GDPR emphasize secure authentication methods, driving banks and financial institutions to adopt smart cards for both consumer and business use. Furthermore, the widespread use of contactless technology in smart cards, which allows for fast and secure payments, is fueling consumer adoption across markets, especially in developed regions like Europe and North America.

Restraining Factors

High Initial Setup Costs for Banks and Financial Institutions

Despite the growing adoption of banking and financial smart cards, one of the key restraining factors is the high initial setup costs for banks and financial institutions. While the long-term benefits of adopting smart card technology, such as reduced fraud and operational efficiency, are clear, the upfront investment required to switch from traditional magnetic stripe cards to EMV chip-enabled or contactless smart cards can be significant. Financial institutions need to invest in upgrading their infrastructure, including card personalization systems, POS terminals, and transaction processing systems, which can be a substantial financial commitment.

Additionally, the need for extensive training programs for employees and merchants who need to understand the new technology adds to the cost burden. Smaller or regional banks, in particular, may find it challenging to make such a significant investment, especially when their customer base is smaller or less tech-savvy.

Moreover, in countries with lower economic development, the costs associated with deploying smart card solutions may be prohibitive, limiting the rate of adoption. As a result, while the technology continues to grow, these financial constraints might slow down widespread global adoption, particularly in emerging markets.

Growth Opportunities

Expansion of Financial Inclusion in Emerging Markets

The expansion of financial inclusion presents a significant growth opportunity for the Banking and Financial Smart Cards Market. In many emerging economies, a large portion of the population remains unbanked or underbanked, lacking access to traditional financial services.

However, the advent of smart cards, particularly prepaid cards, offers a feasible solution for financial institutions to reach these underserved populations. By providing prepaid and debit smart cards linked to mobile wallets, these institutions can bring financial services to people who have limited or no access to physical bank branches.

As smartphone penetration continues to rise in regions like Asia-Pacific, Africa, and Latin America, there is a unique opportunity to offer mobile banking solutions paired with smart card technology. Prepaid cards allow users to store digital currency, make payments, and even access credit without needing a traditional bank account.

According to the World Bank, over 1.7 billion people worldwide remain unbanked, and financial institutions are increasingly focused on using smart card solutions to bridge this gap. The growth of mobile payments and mobile banking in these regions, combined with government-led initiatives to promote financial inclusion, will accelerate the adoption of smart cards in these markets.

Challenging Factor

Security Concerns Around Contactless Payment Technology

While the rise of contactless payment technology has greatly contributed to the growth of the Banking and Financial Smart Cards Market, it also brings about significant security concerns. Contactless cards, which allow users to tap their cards for quick payments, are often perceived as vulnerable to unauthorized transactions.

The possibility of skimming attacks, where criminals use unauthorized scanners to steal card information from consumers’ contactless cards, is a growing concern. Although contactless cards use encrypted technology, there is still some hesitancy among consumers regarding the security of these transactions.

Moreover, the relatively low transaction limit for contactless payments—often ranging from USD 20 to USD 100—can make it easier for fraudsters to make small, unauthorized purchases without being detected. While the cards are designed to require a PIN for transactions beyond a certain amount, many consumers remain unaware of the security risks.

Additionally, merchants and payment gateways also face the challenge of ensuring their systems are compliant with security standards, like PCI DSS (Payment Card Industry Data Security Standard), which can be a complex and costly process. These security concerns need to be addressed with continuous advancements in encryption, biometric verification, and consumer education to fully capitalize on the potential of contactless payment systems.

Growth Factors

Increasing Adoption of Contactless Payment Solutions

One of the primary growth factors driving the Banking and Financial Smart Cards Market is the increasing adoption of contactless payment solutions. As of 2023, nearly 70% of global card payments were processed through contactless methods, with regions like Europe and North America leading the charge.

The convenience of tap-and-go payments has led to widespread consumer acceptance, particularly in urban areas where quick and secure transactions are a priority. The global contactless payment market is expected to grow at a CAGR of 19% from 2023 to 2030. As more consumers prefer the ease of contactless transactions, financial institutions are rapidly expanding their offerings to meet this demand, ensuring continued market growth.

Moreover, the rise of mobile wallets and smartphones with embedded NFC technology is further accelerating the transition towards contactless payments. Consumers can now make payments directly from their smartphones, making traditional smart cards even more integrated into daily life. This trend is especially strong in Asia-Pacific, where mobile payments are expected to increase by 25% annually over the next five years, contributing significantly to the growth of smart cards in the region.

Emerging Trends

Integration with Biometric Authentication

Biometric authentication is emerging as a key trend in the Banking and Financial Smart Cards Market. With concerns over fraud and security breaches on the rise, many financial institutions are integrating biometric features such as fingerprint scanning, facial recognition, and iris scanning into their smart cards and payment systems.

As of 2024, the market for biometric smart cards is expected to grow at a CAGR of 23%. By combining biometrics with smart card technology, banks can offer highly secure, frictionless payment experiences to their customers, which is increasingly becoming a priority in both developed and emerging markets.

The integration of biometric authentication allows for enhanced security by ensuring that only the cardholder can authorize transactions. This trend is gaining traction, particularly in high-risk markets, such as online banking and mobile payments, where the risk of fraud is higher.

The EMV 3DS (Three-Domain Secure) protocol also supports biometric authentication, making it easier for cardholders to authenticate transactions securely. The continued integration of biometrics into financial smart cards will likely become a key differentiator for banks looking to enhance their customer trust and satisfaction.

Business Benefits

Enhanced Security and Reduced Fraud

For businesses, the adoption of smart card technologies brings significant security benefits, making it a wise investment. With EMV chip technology and contactless features, financial institutions can significantly reduce fraud risks.

Fraudulent transactions using magnetic stripe cards have seen a steady decline, and the shift to chip-based smart cards has been credited with reducing card-present fraud by over 80% in regions like North America and Europe. In addition to improving security, the integration of smart card technology also enhances customer experience by offering faster and more efficient payment methods.

For merchants, the use of contactless payment systems means quicker transactions, leading to improved transaction speed and higher customer throughput. A study by NFC Forum showed that contactless payments reduced transaction times by up to 60% compared to traditional payment methods.

This improvement in transaction speed not only improves operational efficiency but also enhances customer satisfaction, driving repeat business and long-term loyalty. As businesses continue to focus on improving payment efficiency and security, investing in smart card technology offers a tangible return on investment, enhancing both customer retention and revenue.

Key Player Analysis

Thales Group has been a significant player in the Banking and Financial Smart Cards Market, with a focus on enhancing security through innovation. In recent years, Thales has actively pursued strategic acquisitions to expand its product offerings and capabilities. One notable acquisition was the purchase of Gemalto, a leading digital security company, in 2019.

Giesecke+Devrient (G+D) is another major player in the banking and financial smart card industry, known for its strong presence in the global market. The company has been at the forefront of contactless payment technologies and is actively involved in smart card production and digital security solutions. G+D has expanded its market reach through strategic partnerships and acquisitions.

IDEMIA has solidified its position as a leader in the Banking and Financial Smart Cards Market with a focus on biometric authentication and advanced security solutions. The company has made significant strides through strategic mergers and product innovations. In 2021, IDEMIA acquired Oberthur Technologies, a merger that strengthened its portfolio in digital identity and payment solutions.

Top Key Players in the Market

- Thales Group

- Giesecke+Devrient

- IDEMIA

- Mastercard

- American Express

- Arm Limited

- Rambus

- CardLogix Corporation

- Entrust Corporation

- Watchdata Co.

- Infineon Technologies

- NXP Semiconductors

- Other Key Players

Recent Developments

- In 2024: Thales Group launched a new range of biometric smart cards that combine fingerprint authentication with EMV chip technology, enhancing payment security.

- In 2024: Giesecke+Devrient expanded its presence in the Asia-Pacific region by rolling out advanced dual-interface smart cards for contactless payments in partnership with major regional banks.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2024) | USD 13.5 Billion |

| Forecast Revenue (2034) | USD 31.67 Billion |

| CAGR (2025-2034) | 8.90% |

| Largest Market | North America |

| Base Year for Estimation | 2024 |

| Historic Period | 2020-2023 |

| Forecast Period | 2025-2034 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Card Type (Contact-Based Smart Cards, Contactless Smart Cards, Dual Interface Smart Cards), By Vertical (Banks, Hospitality, BFSI, Retail, Government, Others (Education, Healthcare, Entertainment, etc.)) |

| Regional Analysis | North America (US, Canada), Europe (Germany, UK, Spain, Austria, Rest of Europe), Asia-Pacific (China, Japan, South Korea, India, Australia, Thailand, Rest of Asia-Pacific), Latin America (Brazil), Middle East & Africa(South Africa, Saudi Arabia, United Arab Emirates) |

| Competitive Landscape | Thales Group, Giesecke+Devrient, IDEMIA, Mastercard, American Express, Arm Limited, Rambus, CardLogix Corporation, Entrust Corporation, Watchdata Co., Infineon Technologies, NXP Semiconductors, Other Key Players |

| Customization Scope | We will provide customization for segments and at the region/country level. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |