Quick Navigation

Report Overview

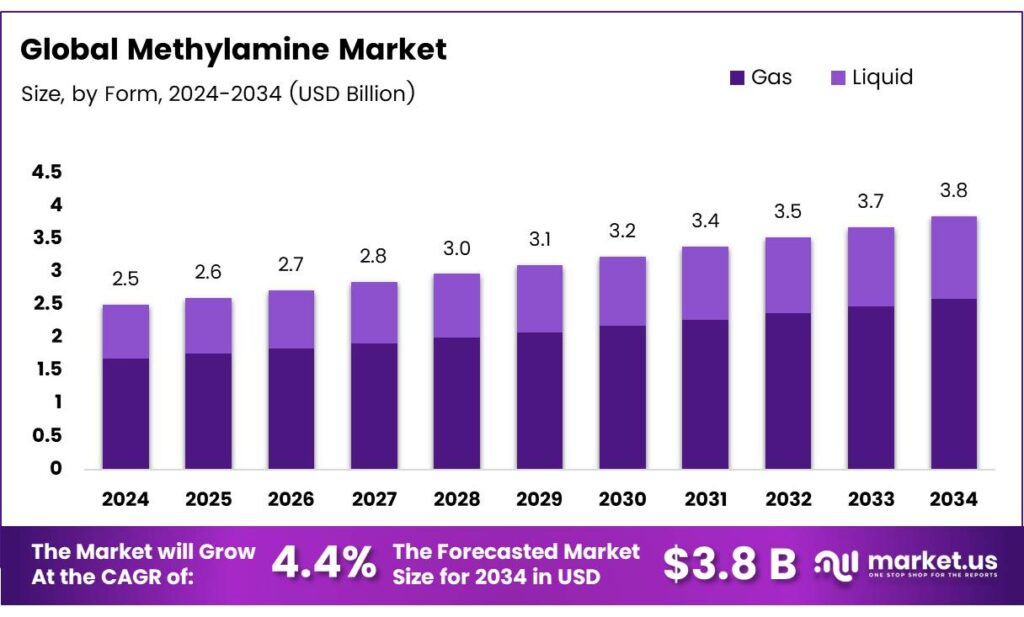

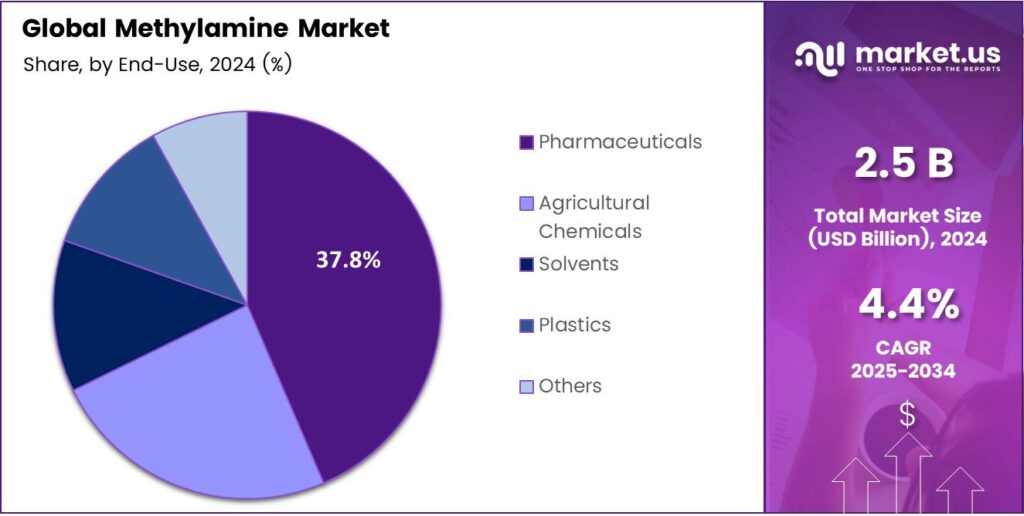

The Global Methylamine Market size is expected to be worth around USD 3.8 billion by 2034, from USD 2.5 billion in 2024, growing at a CAGR of 4.4% during the forecast period from 2025 to 2034.

Methylamine in its anhydrous form appears as a colorless gas or liquid with a pungent, fishy odor similar to ammonia. It boils at low temperatures, causing rapid vaporization when unconfined. The vapors are heavier than air and tend to accumulate in low-lying areas. This substance is easily ignited under most conditions, and prolonged exposure to intense heat can cause containers to rupture violently and rocket.

Anhydrous methylamine is widely used in the production of pharmaceuticals, insecticides, paint removers, surfactants, and rubber chemicals. The aqueous solution of methylamine presents as a colorless to yellow liquid containing dissolved gas, with an odor ranging from fishlike to ammonia-like as vapor concentration increases. A 30% solution has a flash point of 34 °F and is corrosive to skin and eyes.

It is less dense than water, though its vapors remain heavier than air. Combustion of the solution produces toxic oxides of nitrogen. Chemically, methylamine is the simplest member of the methylamines, consisting of ammonia with a single methyl group substituent. It functions as a mouse metabolite and is classified as a primary aliphatic amine, a one-carbon compound, and a member of the methylamines. It also serves as the conjugate base of methylammonium.

- Chronic toxicity, animal studies show that repeated inhalation exposure in rats causes mild nasal irritation at 75 ppm, damage to the respiratory mucosa of the nasal turbinates at 250 ppm, and bodyweight loss, liver damage, and nasal degenerative effects at 750 ppm. No adverse reproductive effects or fetal abnormalities were observed in CD-1 mice treated daily with 0.25, 1, 2.5, or 5 mmol methylamine per kg via intraperitoneal injection during gestation days 1–17.

Key Takeaways

- The Global Methylamine Market is projected to grow from USD 2.5 billion in 2024 to USD 3.8 billion by 2034 at a CAGR of 4.4%.

- Gas form dominated the By Form segment in 2024 with a 67.3% share due to efficient storage and rapid vaporization.

- Pharmaceuticals led the By End-Use segment in 2024 with 37.8% share, driven by its role in synthesizing antidepressants and antibiotics.

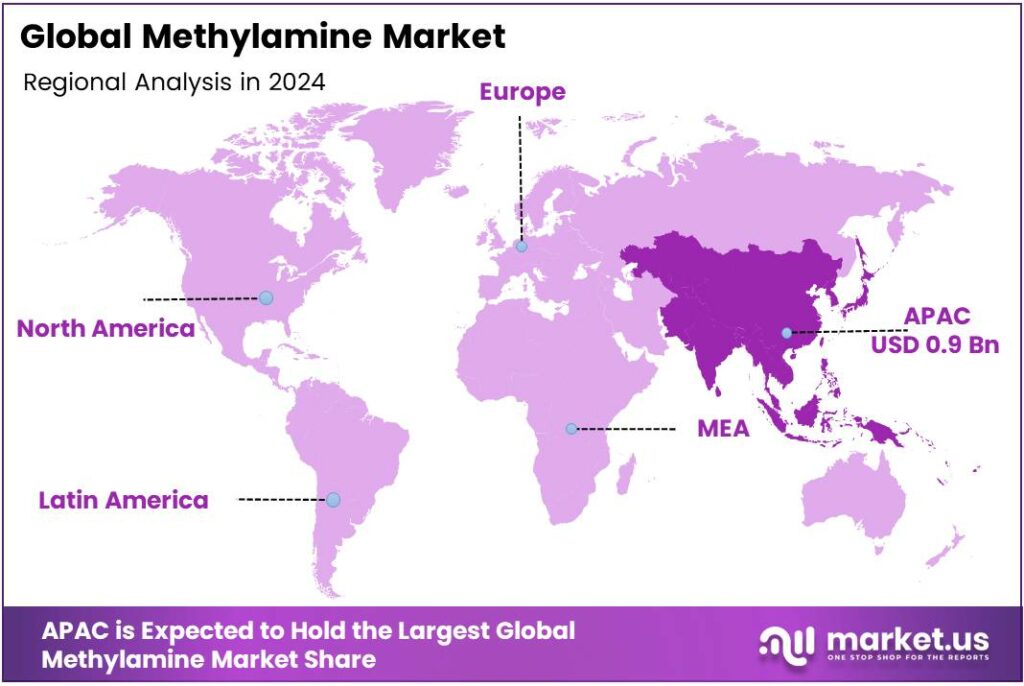

- Asia-Pacific held the largest regional share in 2024 at 39.4%, USD 0.9 billion, fueled by chemical manufacturing in China, India, South Korea, and Japan.

By Nature

By Form Analysis, Gas dominates with 67.3% due to its ease of handling and transportation in industrial applications.

In 2024, Gas held a dominant market position in the By Form Analysis segment of the Methylamine Market, with a 67.3% share. This form leads because it allows efficient storage and quick dispersion, suiting large-scale chemical processes. Industries prefer it for its low boiling point, enabling rapid vaporization.

The Liquid form captures the remaining share in the methylamine market. It offers advantages in precise dosing and stability for certain reactions. Liquid methylamine suits applications needing controlled volumes, like in labs. Additionally, it minimizes vapor hazards in confined spaces. Overall, while secondary, it supports diverse industrial needs effectively.

By End-Use Analysis

Pharmaceuticals dominate with 37.8% due to rising demand for active ingredients in drug manufacturing.

In 2024, Pharmaceuticals held a dominant market position in the By End-Use Analysis segment of the Methylamine Market, with a 37.8% share. This sector thrives as methylamine serves as a key intermediate for synthesizing medications. Growing healthcare needs boost its usage of antidepressants and antibiotics. Furthermore, innovations in pharma formulations enhance their role.

Agricultural Chemicals represent a vital sub-segment in the methylamine end-use. Methylamine aids in producing pesticides and herbicides, enhancing crop protection. Farmers increasingly adopt these chemicals to boost yields amid population growth. This drives steady demand. Also, eco-friendly formulations using methylamine gain traction. Hence, it contributes substantially to market expansion.

Solvents form another important area in the methylamine market by end-use. They utilize methylamine in paint removers and cleaning agents, offering strong dissolving power. Industries value its efficiency in removing residues without damaging surfaces. Moreover, regulatory approvals for safer solvents spur growth. Thus, this sub-segment sustains consistent market participation.

Key Market Segments

By Form

- Gas

- Liquid

By End-Use

- Pharmaceuticals

- Agricultural Chemicals

- Solvents

- Plastics

- Others

Emerging Trends

Shift to low-carbon, green-methanol feedstocks

A clear trend in methylamine is decarbonising the feedstock. Methylamines are made by reacting ammonia with methanol, so cutting methanol’s footprint directly lowers the product carbon footprint of methylamine. That focus has sharpened because methanol is one of the chemical sector’s biggest emitters: after ammonia, methanol accounts for about 28% of primary chemical production emissions.

- Governments are now steering billions into cleaner carbon sources that can ultimately flow into green and bio-methanol. In Europe, the REPowerEU push aims to scale biomethane to 35 billion m³ per year, with an estimated €37 billion investment need; that biomethane underpins multiple renewable carbon routes and hydrogen supply chains used to produce low-carbon methanol, which then feeds methylamines.

In the U.S., the Department of Energy is funding work that upgrades bio-methanol into advanced fuels, reflecting a broader federal interest in scaling renewable methanol platforms that chemical makers can tap. Methylamine’s next competitiveness frontier is feedstock decarbonisation, and the policy and technology pieces for green-methanol supply are moving into place.

Drivers

Growing demand from the pharmaceutical industry

- The demand for methylamine is the rapidly expanding global pharmaceutical sector. The European Federation of Pharmaceutical Industries & Associations (EFPIA), the worldwide pharmaceutical market, saw North America alone accounting for 53.3% of global sales. In India, the domestic pharmaceutical market for FY 2023-24 was valued at USD 50 billion, with domestic consumption at USD 23.5 billion and exports at USD 26.5 billion.

Methylamine serves as a key chemical building block in the synthesis of active pharmaceutical ingredients (APIs) and intermediates used in a variety of medications. As pharmaceutical production rises, so does the need for its upstream inputs. With the pharma market globally edging over USD 1.6 trillion and showing steady growth, the ripple effect into intermediates such as methylamine becomes clear.

In addition, many governments are actively supporting pharmaceutical manufacturing via initiatives and policies, which further drive chemical demand. In India, for instance, the Make in India programme and dedicated API-manufacturing incentives encourage domestic chemical supply chains and reduce dependency on imports. This means intermediates like methylamine have greater local demand as more pharma production is established.

Restraints

Strict health and safety regulations

One major restraint for the methylamine industry is the stringent exposure limits and safety regulations that producers must meet. Meanwhile, the National Institute for Occupational Safety and Health (NIOSH) has set the same 10 ppm (12 mg/m³) exposure level and lists the Immediately Dangerous to Life or Health (IDLH) value at 100 ppm.

The EU’s Seveso III Directive (for managing major-accident hazards), substances that are highly hazardous trigger lower-tier or upper-tier threshold quantities, which in turn forces chemical plants into stricter permit regimes, risk-management plans, and emergency-response obligations. The fact that it is a reactive, flammable gas with toxicity means many jurisdictions will treat it more conservatively.

For methylamine manufacturers, this means higher capital costs for safety infrastructure, longer lead times to permit plants, greater liability and insurance costs, and more frequent regulatory audits. All of those act as a restraint because they increase the hurdle to expand capacity or shift quickly to new geographies or feedstocks.

Opportunity

Rising Use of the Dimethylamine Salt of 2,4-D Enhances Demand for Methylamine

The methylamine market is experiencing an increasing demand for the dimethylamine (DMA) salt form of the herbicide 2,4‑Dichlorophenoxyacetic acid (commonly called 2,4-D), which uses methylamine (in the form of dimethylamine) as a feedstock. The dimethylamine salt and the 2-ethylhexyl ester forms account for approximately 90-95% of the total global use of 2,4-D formulations.

This means that a large majority of global 2,4-D demand relies on methylamine-derived salt forms rather than the acid alone. Because 2,4-D remains one of the most widely used herbicides worldwide, registered and used across numerous crops, non-crop areas, and applications, with a long commercial history. As agricultural expansion, weed resistance management.

Regional Analysis

Asia-Pacific leads with a 39.4% share and a USD 0.9 Billion market value.

In 2024, Asia-Pacific held a dominant share of 39.4%, valued at around USD 0.9 billion, positioning it as the leading regional market for methylamine. The region’s growth is largely supported by the expanding chemical manufacturing ecosystem across China, India, South Korea, and Japan.

These countries are major producers of agrochemicals, pharmaceuticals, and solvents, all of which rely on methylamine as a critical intermediate. Rising agricultural productivity demands and the growing use of methylamine-based herbicides such as 2,4-D have also strengthened its consumption base.

China remains the primary growth engine, driven by increasing domestic consumption of methylamine in pesticide and pharmaceutical applications. India, meanwhile, is witnessing strong investment inflows in specialty chemicals and intermediates, supported by government initiatives like the Production Linked Incentive (PLI) scheme and the Make in India policy that aim to boost local manufacturing of essential chemicals.

Increasing environmental regulations in North America and Europe have indirectly benefited the Asia-Pacific region, as global manufacturers shift production bases to cost-competitive and less-regulated environments. With these combined factors, Asia-Pacific is expected to maintain its leadership in the methylamine market, supported by sustained chemical output growth.

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

Alkyl Amines Chemicals Limited (AACL) is recognized for its extensive production capacity and integrated manufacturing approach. The company benefits from strong backward integration and a diverse product portfolio that extends beyond methylamines to various derivatives. Its significant market share in India and strategic expansion initiatives position it as a low-cost, high-volume producer, making it a pivotal and resilient player in the global supply chain for this essential chemical.

Balaji Amines Ltd. is a key competitor in the methylamine space, known for its robust production capabilities and focus on amines and their derivatives. The company leverages its strong domestic presence in India and cost-effective manufacturing processes to serve a wide range of industries, including pharmaceuticals and agrochemicals. Its consistent capacity expansions and vertical integration strategy make it a significant and growing contributor to the global methylamine market.

Balchem Corporation distinguishes itself in the methylamine market through its focused application in specialty segments, particularly human nutrition and animal feed. Unlike volume-driven producers, Balchem adds significant value by manufacturing choline chloride, which uses methylamines as a key raw material. This downstream integration into high-value, performance-based end products provides a stable demand stream and insulates it from commodity price fluctuations.

Top Key Players in the Market

- Alkyl Amines Chemicals Limited

- Balaji Amines Ltd.

- Balchem Corporation

- BASF SE

- Celanese Corporation

- Eastman Chemical Company

- Johnson Matthey Plc

- Luxi Chemical Group Co., Ltd.

- MITSUBISHI GAS CHEMICAL COMPANY, INC.

- The Chemours Company

Recent Developments

- In 2025, Alkyl Amines Chemicals Limited, a key player in aliphatic amines, including methylamines, reported strong financial performance. This reflects robust demand in the amines sector, particularly for methylamine derivatives used in pharmaceuticals and agrochemicals.

- In 2025, Balaji Amines Ltd., a major producer of methylamines and ethylamines, is advancing multiple capacity expansions tied to the methylamine sector. The company commissioned its upgraded Dimethyl Carbonate (DMC) plant, integrated for electronic-grade production.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2024) | USD 2.5 Billion |

| Forecast Revenue (2034) | USD 3.8 Billion |

| CAGR (2025-2034) | 4.4% |

| Base Year for Estimation | 2024 |

| Historic Period | 2020-2023 |

| Forecast Period | 2025-2034 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Form (Gas, Liquid), By End-Use (Pharmaceuticals, Agricultural Chemicals, Solvents, Plastics, Others) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – GCC, South Africa, Rest of MEA |

| Competitive Landscape | Alkyl Amines Chemicals Limited, Balaji Amines Ltd., Balchem Corporation, BASF SE, Celanese Corporation, Eastman Chemical Company, Johnson Matthey Plc, Luxi Chemical Group Co., Ltd., MITSUBISHI GAS CHEMICAL COMPANY, INC., The Chemours Company |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited Users and Printable PDF) |