Quick Navigation

Report Overview

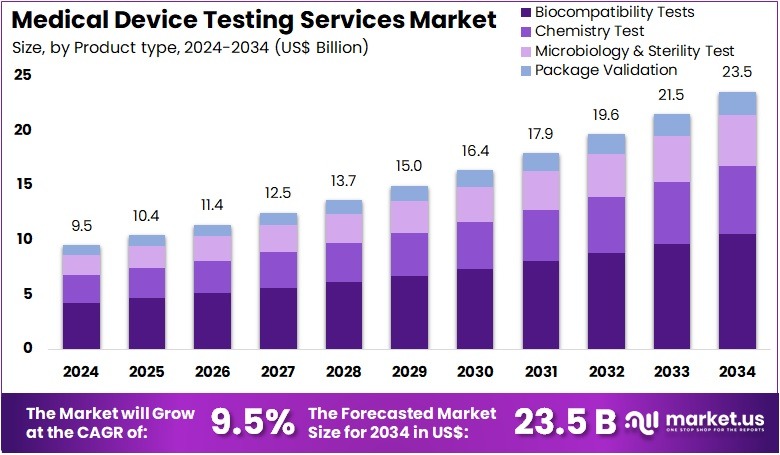

The Medical Device Testing Services Market Size is expected to be worth around US$ 23.5 billion by 2034 from US$ 9.5 billion in 2024, growing at a CAGR of 9.5% during the forecast period 2025 to 2034.

Growing emphasis on patient safety and regulatory compliance drives the expansion of the medical device testing services market, which encompasses a broad range of evaluations including biological, chemical, mechanical, and electrical testing. These services play a critical role in verifying device safety, efficacy, and performance across various applications such as implantable devices, diagnostic equipment, and surgical instruments.

In June 2023, TUV SUD inaugurated a new laboratory in Minnesota, accredited to ISO 17025 standards, to specialize in biological and chemical testing for medical devices, highlighting the industry’s focus on precision and reliability. This market benefits from stringent global regulatory frameworks requiring comprehensive pre-market and post-market testing to ensure compliance. Opportunities arise from the introduction of advanced testing methodologies, including in vitro diagnostics and biocompatibility assessments, which enhance risk management and accelerate product approvals.

Recent trends reveal increasing adoption of automation and digital technologies to improve testing accuracy and turnaround times. Additionally, the integration of sustainability principles in testing protocols offers competitive advantages by reducing environmental impacts. Medical device manufacturers increasingly rely on third-party testing providers to navigate complex regulations and reduce time-to-market. The rise of innovative device categories such as wearable and connected health devices further fuels demand for specialized testing services.

Growing investments in healthcare infrastructure and expanding healthcare access also stimulate market growth. With continuous technological advancements and evolving regulatory landscapes, the medical device testing services market is positioned for sustained expansion, supporting safer and more effective healthcare solutions worldwide.

Key Takeaways

- In 2024, the market for medical device testing services generated a revenue of US$ 9.5 billion, with a CAGR of 9.5%, and is expected to reach US$ 23.5 billion by the year 2034.

- The product type segment is divided into biocompatibility tests, chemistry test, microbiology & sterility test, and package validation, with biocompatibility tests taking the lead in 2023 with a market share of 44.7%.

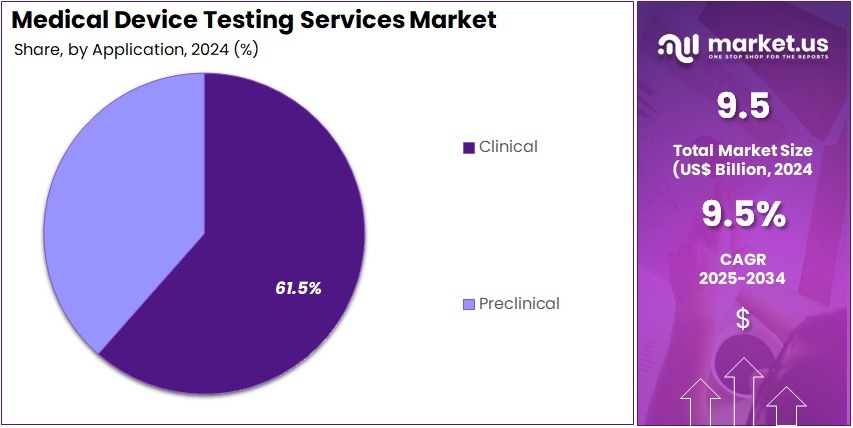

- Considering application, the market is divided into preclinical and clinical. Among these, clinical held a significant share of 61.5%.

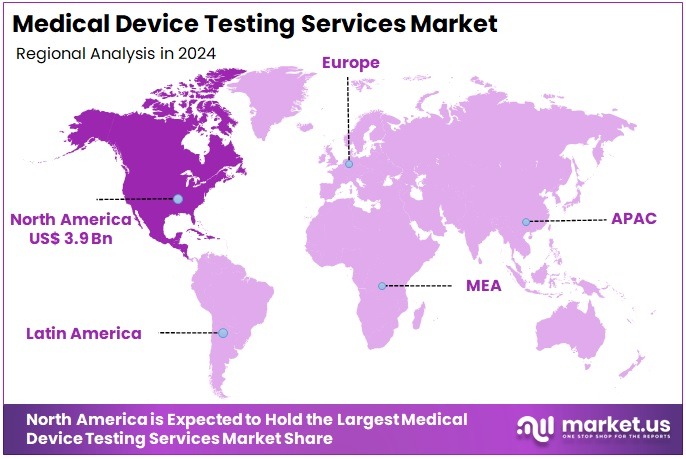

- North America led the market by securing a market share of 41.2% in 2023.

Product Type Analysis

The biocompatibility tests segment claimed a market share of 44.7%. Increasing regulatory requirements for safety and efficacy drive this expansion as manufacturers prioritize ensuring their devices do not cause adverse biological reactions. Growing adoption of implantable and wearable medical devices further fuels demand for thorough biocompatibility assessments.

Advances in testing methodologies and materials science improve accuracy and reduce testing time, encouraging more companies to invest in these services. Moreover, stringent guidelines from authorities such as the FDA and ISO necessitate comprehensive biocompatibility evaluations, positioning this segment for sustained growth.

Application Analysis

The clinical held a significant share of 61.5% due tothe increasing importance of human trials in device validation. Rising awareness about patient safety and effectiveness of medical devices mandates extensive clinical evaluations before market approval. Advances in clinical trial designs and digital health technologies facilitate more efficient and comprehensive data collection, enhancing the appeal of clinical testing services.

Additionally, the expanding pipeline of innovative medical devices, particularly in areas such as cardiology and orthopedics, drives demand for clinical testing. Regulatory bodies increasingly emphasize clinical evidence, further propelling this segment’s growth.

Key Market Segments

By Product Type

- Biocompatibility Tests

- Orthopedic Device’s Biocompatibility Tests

- Ophthalmic Implantation Device’s Biocompatibility Tests

- Neurosurgical Implantation Devices Biocompatibility Tests

- General Surgery Implantation Devices Biocompatibility Tests

- Dermal Filler’s Biocompatibility Tests

- Dental Implant Devices’ Biocompatibility Tests

- Cardiovascular Device’s Biocompatibility Tests

- Others

- Chemistry Test

- Toxicological Risk Assessment and consulting

- Chemical characterization (E&L)

- Analytical method development and validation

- Microbiology & Sterility Test

- Sterility Test & Validation

- Pyrogen & Endotoxin Testing

- Bioburden Determination

- Antimicrobial Testing

- Others

- Package Validation

By Application

- Preclinical

- Large animal research

- Microbiology & Sterility Test

- Chemistry Test

- Biocompatibility Tests

- Small animal research

- Microbiology & Sterility Test

- Chemistry Test

- Biocompatibility Tests

- Large animal research

- Clinical

Drivers

Stringent Regulatory Requirements are driving the market

The increasingly stringent regulatory requirements for medical devices worldwide are a significant driver for the medical device testing services market. Regulatory bodies like the US Food and Drug Administration (FDA) mandate thorough evaluation before devices can be marketed. In 2023, the FDA authorized 36 PMA (Premarket Approval) applications for high-risk medical devices, along with 2,180 PMA supplements, indicating the volume of rigorous pre-market scrutiny that necessitates extensive testing data to demonstrate safety and effectiveness.

Similarly, the Medical Device Regulation (MDR) in the European Union, which fully came into effect in 2021, has heightened the requirements for clinical evaluation and post-market surveillance, requiring more comprehensive testing. These demanding regulatory landscapes compel medical device manufacturers to utilize independent testing services to ensure compliance and gain market access, thereby fueling the growth of this market.

Restraints

Complexity of Medical Devices is restraining the market

The growing complexity of modern medical devices is becoming a restraint on the medical device testing services market. As devices evolve with advanced software, sensors, and connectivity features, the testing process becomes more specialized. Standard testing procedures are no longer sufficient. Instead, a tailored and highly technical approach is often required. This shift in testing demand puts pressure on service providers to update their capabilities. Not all facilities can quickly adapt, which limits their ability to test these high-tech devices effectively and consistently.

In September 2023, the FDA issued final guidance on “Cybersecurity in Medical Devices: Quality System Considerations and Content of Premarket Submissions.” This document highlights the growing need for cybersecurity assessments in device testing.

As digital integration expands, so does the need for specialized knowledge and tools. Testing labs must invest in new technologies and cybersecurity expertise. However, acquiring such capabilities takes time and resources. This can create short-term gaps in capacity, potentially delaying market entry for some complex medical devices.

Opportunities

Globalization of Medical Device Manufacturing creates growth opportunities

The globalization of medical device manufacturing is driving strong growth in the medical device testing services market. As production expands across multiple countries, companies must comply with the unique regulatory standards of each region. This creates a growing need for specialized testing services. These services help manufacturers ensure compliance with varying safety and quality regulations. Global firms increasingly rely on testing providers with multi-regional expertise. This shift is boosting the demand for testing partners familiar with international medical device regulations.

According to MedTech Europe, over 15,900 patent applications were filed with the European Patent Office (EPO) in 2023 under the medical technology category. This figure highlights the rapid pace of innovation within the industry.

New product development across borders requires thorough regulatory testing before market entry. As companies launch advanced devices globally, the need for standardized and region-specific testing is rising. This trend supports continued expansion of the testing services sector, especially those offering cross-border regulatory compliance solutions.

Impact of Macroeconomic / Geopolitical Factors

Macroeconomic conditions and geopolitical factors can influence the medical device testing services market. Economic uncertainty might cause manufacturers to optimize spending, potentially affecting the volume or type of testing they pursue. Conversely, government initiatives promoting the medical device industry or emphasizing product safety can bolster the demand for thorough evaluation.

Geopolitical tensions could disrupt global supply chains, indirectly affecting the production and subsequent testing of devices. However, the fundamental need for regulatory compliance, as highlighted by the FDA’s ongoing premarket review processes with thousands of submissions annually, tends to provide a baseline demand for these services. The continuous advancement in medical technology and the consistent need to meet stringent global standards suggest a resilient market for these services, adapting to broader economic and political landscapes.

Current US tariffs could have a nuanced impact on the medical device testing services market. If tariffs increase the cost of imported medical devices or testing equipment, this might indirectly affect the overall expenditure on bringing devices to market, potentially influencing the budget allocated for testing. However, the mandatory nature of much of the testing required for regulatory approval, such as the FDA’s PMA process for high-risk devices, means that manufacturers will likely still need to invest in these services.

Tariffs could also incentivize domestic testing capabilities, potentially shifting some demand towards US-based testing providers. While tariffs might introduce some cost considerations for manufacturers, the essential requirement for rigorous testing to ensure safety and gain market access remains a primary driver, suggesting the market for these services will likely adapt to these economic policies.

Latest Trends

Focus on Cybersecurity Testing is a recent trend in the market

A key trend in the medical device testing services market is the rising demand for cybersecurity testing. With more medical devices becoming connected to networks, the risk of cyberattacks has grown. Protecting patient data and device functionality is now a top priority. This shift is driving manufacturers to seek testing services that focus on identifying and fixing security flaws. Cybersecurity has become a vital part of device development, as healthcare systems demand safer and more reliable technologies.

The U.S. FDA updated its cybersecurity guidance in March 2024. It now requires manufacturers to submit postmarket cybersecurity plans and a Software Bill of Materials (SBOM) with their applications for cyber devices. This regulatory move is expanding the scope of device testing services. Specialized testing providers are now helping firms meet compliance requirements. As regulations tighten, the need for in-depth cybersecurity evaluations is expected to grow. This change is shaping a new standard in the medical device testing market.

Regional Analysis

North America is leading the Medical Device Testing Services Market

North America dominated the market with the highest revenue share of 41.2% owing to stringent regulatory requirements enforced by the FDA and the increasing complexity of medical devices. The FDA’s ongoing emphasis on pre-market approval and the need for comprehensive testing to ensure safety and efficacy drive the demand for these services.

Furthermore, the high volume of medical device manufacturing in the US necessitates robust testing procedures. As of April 2024, clinicaltrials.gov listed a significant number of active clinical trials related to medical devices, indicating substantial ongoing development requiring testing services

The Asia Pacific region is expected to experience the highest CAGR during the forecast period

Asia Pacific is expected to grow with the fastest CAGR owing to the expanding medical device manufacturing sector in the region, particularly in countries like China and India. Additionally, the increasing adoption of stringent quality standards and regulatory requirements in several Asia Pacific countries is expected to boost the demand for these services.

For instance, in March 2024, Stryker established a new testing facility in India to enhance their research and development operations, indicating a growing focus on rigorous testing within the region. This trend, coupled with a large and diverse patient pool, suggests a strong upward trajectory for the market.

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia

- Netherland

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- New Zealand

- Singapore

- Thailand

- Vietnam

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Key Players Analysis

Key players in the medical device testing services market drive growth by expanding service portfolios, enhancing technological capabilities, and increasing global reach. They focus on offering comprehensive testing solutions that encompass biocompatibility, electrical safety, and performance evaluations to meet stringent regulatory requirements.

Strategic acquisitions and partnerships enable these companies to integrate advanced technologies and broaden their service offerings. Emphasizing quality assurance and compliance with international standards ensures the delivery of reliable and safe medical devices. Additionally, investments in research and development foster innovation and adaptability to emerging industry trends.

Eurofins Scientific, a prominent player in this sector, provides a wide range of testing services, including analytical testing, clinical diagnostics, and laboratory services across various industries. Established in 1987 and headquartered in Luxembourg, Eurofins operates over 900 laboratories in 62 countries, employing approximately 63,000 people globally. The company has expanded its capabilities through strategic acquisitions, such as acquiring EAG Laboratories in 2017, to enhance its service offerings in the life sciences sector. Eurofins’ commitment to innovation and quality has positioned it as a leader in the medical device testing services market.

Top Key Players in the Medical Device Testing Services Market

- TUV SUD

- SGS SA

- Pace Analytical Services LLC

- Nelson Laboratories, LLC

- Laboratory Corporation of America Holdings

- Eurofins Scientific

- Element Minnetonka

- Charles River Laboratories

Recent Developments

- In January 2025: IMQ Group entered the Indian market through the launch of Elettra Tech Labs, a joint venture aimed at delivering specialized testing and inspection services. The facility is focused on medical devices as well as electrical and electronic products, marking a strategic move to broaden the company’s service portfolio and establish a stronger foothold in a rapidly expanding sector.

- In March 2024: Stryker expanded its research and development capabilities in India by significantly enlarging its prototype and testing facility. The upgraded 55,600-square-foot site features advanced infrastructure and microbiology capabilities, reflecting the company’s continued investment in operational and technological growth within the region.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2024) | US$ 9.5 billion |

| Forecast Revenue (2034) | US$ 23.5 billion |

| CAGR (2025-2034) | 9.5% |

| Base Year for Estimation | 2024 |

| Historic Period | 2020-2023 |

| Forecast Period | 2025-2034 |

| Report Coverage | Revenue Forecast, Market Dynamics, COVID-19 Impact, Competitive Landscape, Recent Developments |

| Segments Covered | By Product Type (Biocompatibility Tests (Orthopedic Device’s Biocompatibility Tests, Ophthalmic Implantation Device’s Biocompatibility Tests, Neurosurgical Implantation Devices Biocompatibility Tests, General Surgery Implantation Devices Biocompatibility Tests, Dermal Filler’s Biocompatibility Tests, Dental Implant Devices’ Biocompatibility Tests, Cardiovascular Device’s Biocompatibility Tests, and Others), Chemistry Test (Toxicological Risk Assessment and Consulting, Chemical Characterization (E&L), and Analytical Method Development and Validation), Microbiology & Sterility Test (Sterility Test & Validation, Pyrogen & Endotoxin Testing, Bioburden Determination, Antimicrobial Testing, and Others), and Package Validation), By Application (Preclinical (Large Animal Research (Microbiology & Sterility Test, Chemistry Test, and Biocompatibility Tests) and Small Animal Research (Microbiology & Sterility Test, Chemistry Test, and Biocompatibility Tests)) and Clinical) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, New Zealand, Singapore, Thailand, Vietnam, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA |

| Competitive Landscape | TUV SUD, SGS SA, Pace Analytical Services LLC, Nelson Laboratories, LLC, Laboratory Corporation of America Holdings, Eurofins Scientific, Element Minnetonka, and Charles River Laboratories. |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |