Quick Navigation

Report Overview

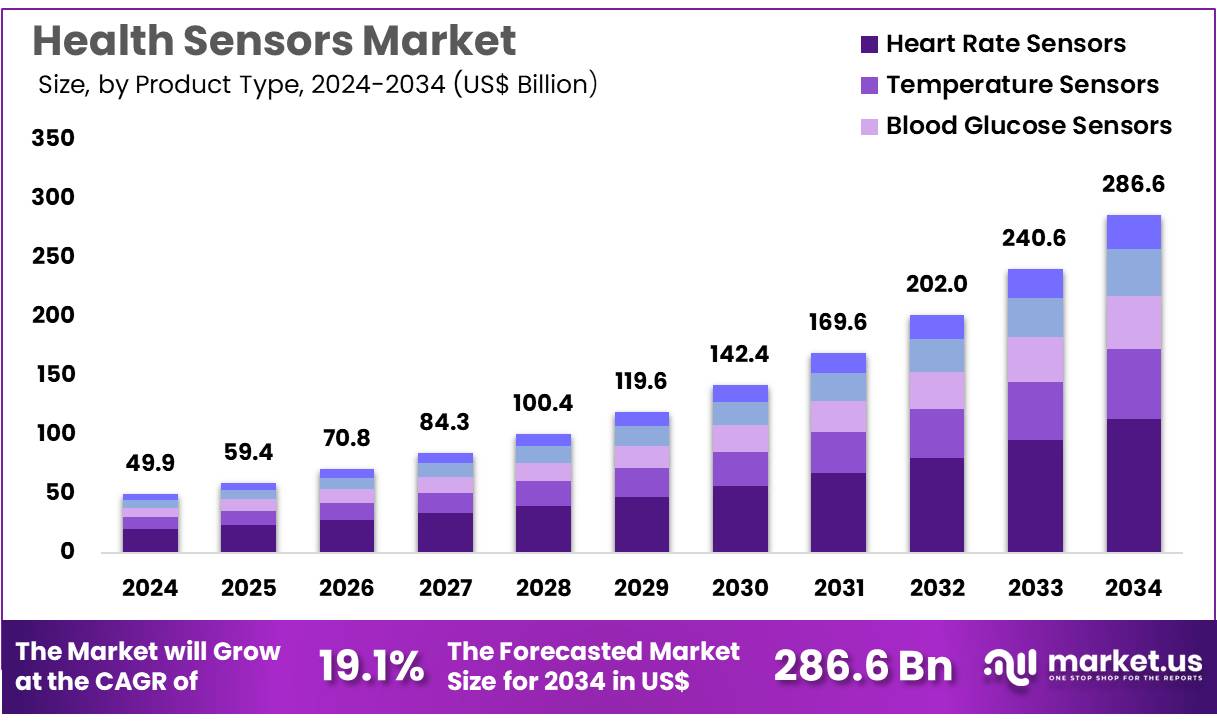

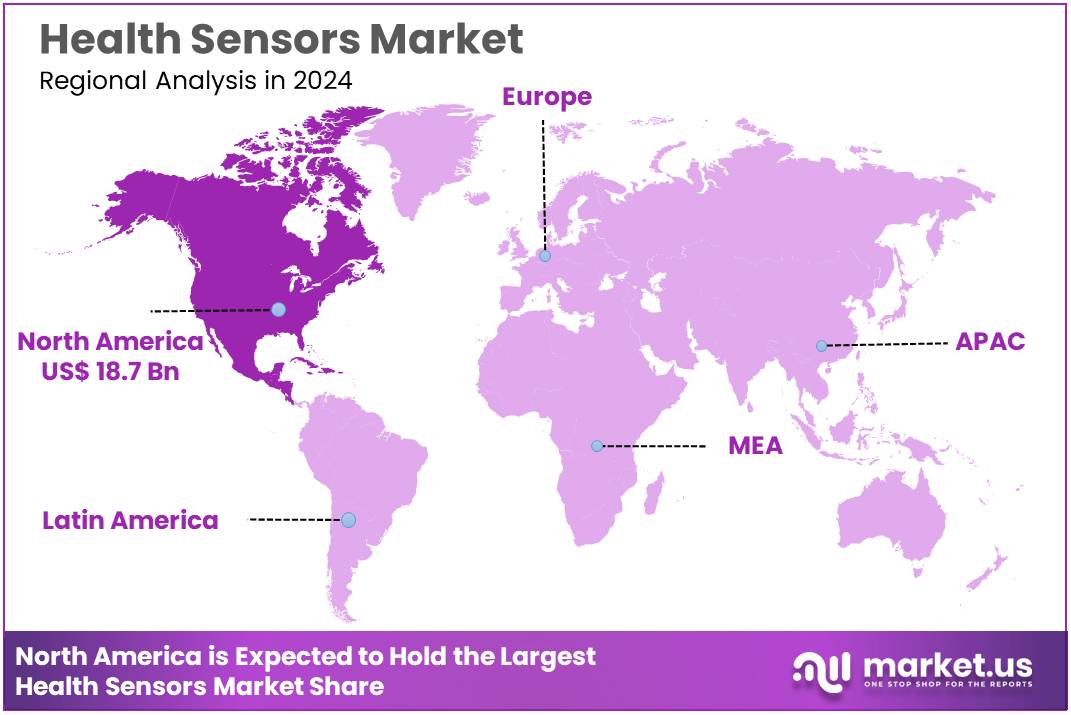

Global Health Sensors Market size is expected to be worth around US$ 286.6 billion by 2034 from US$ 49.9 billion in 2024, growing at a CAGR of 19.1% during the forecast period 2025 to 2034. In 2024, North America led the market, achieving over 37.4% share with a revenue of US$ 18.7 Billion.

Increasing demand for real-time health monitoring and preventive care drives rapid growth in the health sensors market. Health sensors find applications in continuous glucose monitoring, cardiac activity tracking, respiratory function assessment, and wearable fitness devices. These sensors empower healthcare providers and individuals to gather accurate physiological data, enabling early diagnosis and personalized treatment plans.

In December 2023, Neuranics introduced a development kit featuring a high-precision magnetic sensor that captures subtle magnetic signals from cardiac activity, advancing biomagnetic monitoring capabilities. The integration of sensors with telemedicine platforms and mobile health applications further expands their usability, supporting remote patient monitoring and chronic disease management. Advances in miniaturization, wireless connectivity, and artificial intelligence facilitate the creation of sophisticated yet user-friendly health sensor devices.

Growing awareness around lifestyle-related health conditions fuels demand for sensors that track vital signs, physical activity, and sleep quality. Health sensors also enhance hospital workflows by providing continuous monitoring, reducing the need for manual checks, and improving patient safety. Opportunities abound in emerging areas such as implantable sensors and smart textiles, which promise to further revolutionize patient care.

Industry collaborations between technology firms, medical device manufacturers, and healthcare providers accelerate innovation and drive market expansion. Overall, health sensors remain pivotal in transforming healthcare delivery through proactive, data-driven approaches.

Key Takeaways

- In 2024, the market for health sensors generated a revenue of US$ 49.9 billion, with a CAGR of 19.1%, and is expected to reach US$ 286.6 billion by the year 2033.

- The product type segment is divided into heart rate sensors, temperature sensors, blood glucose sensors, blood oxygen sensors and others, with heart rate sensors taking the lead in 2024 with a market share of 39.7%.

- Considering technology, the market is divided into handheld diagnostic sensors, wearable sensors and implantable/ingestible sensors. Among these, wearable sensors held a significant share of 57.3%.

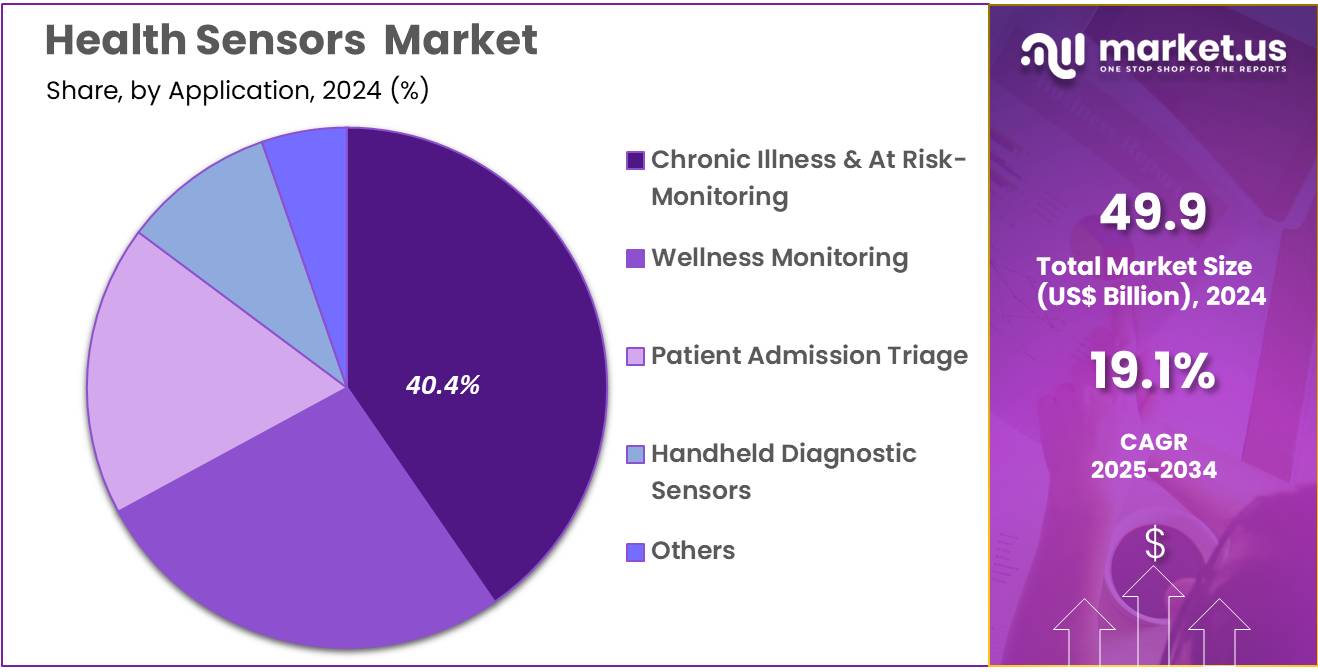

- Furthermore, concerning the application segment, the market is segregated into handheld diagnostic sensors, chronic illness & at risk-monitoring, wellness monitoring, patient admission triage and others. The chronic illness & at risk-monitoring sector stands out as the dominant player, holding the largest revenue share of 40.4% in the health sensors market.

- The end-user segment is segregated into hospitals & clinics, long-term care centers & nursing homes, home care settings and others, with the hospitals & clinics segment leading the market, holding a revenue share of 44.6%.

- North America led the market by securing a market share of 37.4% in 2024.

Product Type Analysis

The heart rate sensors segment claimed a market share of 39.7% owing to rising consumer awareness about cardiovascular health and increasing adoption of wearable fitness devices. The growing prevalence of cardiovascular diseases globally fuels demand for continuous heart rate monitoring solutions. Manufacturers focus on enhancing sensor accuracy and miniaturization, which appeals to both healthcare providers and individual users.

Integration of heart rate sensors into smartwatches, fitness bands, and mobile health applications is anticipated to boost market expansion. Technological advancements, such as optical and electrical heart rate monitoring, improve user experience and reliability. Increasing health-conscious lifestyles and preventive care trends also support the segment’s growth.

Additionally, partnerships between device manufacturers and healthcare companies encourage broader usage. The surge in telehealth and remote patient monitoring further emphasizes the importance of these sensors. Growing government initiatives promoting digital health technologies add momentum. Rising investments in R&D for advanced sensor technologies are expected to accelerate innovation. The segment’s ability to deliver real-time, non-invasive monitoring positions it for continued market leadership.

Technology Analysis

The wearable sensors held a significant share of 57.3% due to increasing demand for real-time health monitoring and fitness tracking. The convenience and portability of wearable devices attract consumers focused on proactive health management and chronic disease monitoring. Innovations in sensor miniaturization, battery efficiency, and wireless connectivity enhance device functionality and user adoption. Integration with smartphones and cloud-based platforms supports continuous data collection and analysis, improving personalized healthcare delivery.

Rising awareness about lifestyle diseases and fitness trends pushes demand for wearable technologies across all age groups. Healthcare providers increasingly recommend wearables for remote monitoring, reducing hospital visits and healthcare costs. Expansion of telemedicine services is projected to further fuel adoption.

Additionally, growing investments in wearable technology startups contribute to market dynamism. Consumer preference for multifunctional devices combining heart rate, activity, and sleep tracking supports growth. Regulatory support for medical-grade wearables enhances credibility. Collaborations between tech companies and healthcare firms accelerate innovation. Overall, the segment is poised for robust expansion driven by technological advances and shifting consumer behavior.

Application Analysis

The chronic illness & at risk-monitoring segment had a tremendous growth rate, with a revenue share of 40.4% owing to the increasing global burden of chronic diseases such as diabetes, cardiovascular conditions, and respiratory disorders. Healthcare systems prioritize early detection and continuous monitoring to prevent complications and reduce hospitalization rates. Advances in sensor accuracy and integration with telehealth platforms enable more effective remote patient monitoring.

The rising geriatric population and increasing awareness of personalized healthcare foster demand for monitoring solutions tailored to chronic illness management. Insurance companies and healthcare providers are likely to encourage sensor use to optimize patient outcomes and control costs. Continuous glucose monitors, blood pressure monitors, and respiratory sensors are integral to this growth.

The adoption of AI and machine learning enhances predictive analytics for at-risk patients, improving clinical decision-making. Government initiatives promoting chronic disease management programs further support market growth. Increased funding for digital health technologies and patient education also play a key role. Growing patient preference for home-based monitoring fuels adoption. Consequently, this segment is set to dominate application-driven demand.

End-User Analysis

The hospitals & clinics segment grew at a substantial rate, generating a revenue portion of 44.6% due to the increasing integration of health sensors into clinical workflows for improved patient care and operational efficiency. Healthcare facilities invest heavily in advanced monitoring technologies to support critical care, early diagnosis, and postoperative monitoring. Rising patient volumes and the prevalence of chronic and acute diseases create steady demand for accurate and continuous vital sign monitoring devices.

The segment benefits from growing adoption of telemedicine and remote monitoring platforms that enable hospitals to extend care beyond physical boundaries. Regulatory emphasis on patient safety and quality outcomes incentivizes sensor deployment in clinical settings. Hospitals increasingly leverage sensor data to enable predictive analytics and personalized treatment plans. The trend toward value-based care models encourages technology adoption to reduce readmissions and adverse events. Collaborations with sensor manufacturers drive customization and integration solutions.

Expansion of healthcare infrastructure in emerging markets supports segment growth. Training and awareness programs boost healthcare provider acceptance. Overall, the segment is poised to maintain dominance through sustained technological and clinical advancements.

Key Market Segments

By Product Type

- Heart Rate Sensors

- Temperature Sensors

- Blood Glucose Sensors

- Blood Oxygen Sensors

- Others

By Technology

- Handheld Diagnostic Sensors

- Chronic illness & at risk-monitoring

- Patient admission triage

- Logistical tracking

- In hospital clinical monitoring

- Post-acute care monitoring

- Wearable Sensors

- Disposable wearable sensors

- Non-disposable wearable sensors

-

- Implantable/Ingestible Sensors

By Application

- Handheld Diagnostic Sensors

- Chronic Illness & At Risk-Monitoring

- Wellness Monitoring

- Patient Admission Triage

- Others

By End-user

- Hospitals & Clinics

- Long-term care centers & Nursing homes

- Home Care Settings

- Others

Drivers

The rising prevalence of chronic diseases is driving the market

The rising prevalence of chronic diseases such as diabetes, cardiovascular conditions, and respiratory disorders is a significant driver for the health sensors market. These conditions often require continuous or regular monitoring of physiological parameters like blood glucose, heart rate, blood pressure, and oxygen saturation to effectively manage the disease and prevent complications.

Health sensors integrated into wearable devices, remote monitoring systems, or point-of-care diagnostics provide individuals and healthcare providers with valuable data for personalized care and early intervention. The increasing number of people living with chronic illnesses globally fuels the demand for technologies that enable convenient and continuous health tracking. According to the CDC, in 2023, 76.4% of US adults reported having one or more chronic conditions, representing a substantial population that could benefit from health sensor technologies for monitoring and management.

Restraints

Data privacy and security concerns are restraining the market

Data privacy and security concerns are restraining the market. Health sensors collect sensitive personal health information, and ensuring the secure transmission, storage, and use of this data is paramount. Patients and healthcare providers are increasingly aware of the risks associated with data breaches and unauthorized access to health information.

Establishing robust cybersecurity measures and complying with evolving data protection regulations globally add complexity and cost for manufacturers and service providers in the market. Addressing these concerns and building trust regarding data handling practices is crucial for broader adoption, but the inherent risks associated with digital health data pose a significant challenge.

Opportunities

The growing adoption of remote patient monitoring is creating growth opportunities

The growing adoption of remote patient monitoring (RPM) programs is creating significant growth opportunities in the market. Healthcare providers are increasingly utilizing health sensors as part of RPM initiatives to remotely track patients’ health data, particularly for managing chronic conditions or monitoring post-discharge recovery. RPM allows for timely intervention, reduces the need for frequent in-person visits, and can improve patient engagement in their own care.

The expansion of telehealth infrastructure and favorable reimbursement policies in many regions are facilitating the implementation of RPM programs, directly increasing the demand for connected health sensors. Data indicates a significant increase in the use of remote monitoring; between January 2019 and November 2022, remote patient monitoring claim volume in the US surged by 1,294%, reflecting a substantial increase in the utilization of sensor-based monitoring in clinical practice.

Impact of Macroeconomic / Geopolitical Factors

Macroeconomic and geopolitical factors influence the health sensors market. Economic conditions impact consumer spending on health and fitness wearables, as these can be considered discretionary purchases, and also affect healthcare providers’ budgets for investing in remote patient monitoring infrastructure; during economic downturns, consumer demand for non-essential health tech might decrease, while stable economies can support increased adoption of both consumer and medical-grade sensors.

Geopolitical tensions and trade policies can disrupt the global supply chains for electronic components, semiconductors, and specialized materials used in manufacturing health sensors, potentially leading to increased production costs or delays in product availability. Reports in early 2025 indicated that geopolitical risks were contributing to volatility across various global supply chains, impacting sectors including electronics and medical devices.

Despite potential negative impacts from economic uncertainties and supply chain disruptions, the increasing focus on preventive healthcare, remote monitoring, and personalized wellness maintains a strong underlying demand, encouraging manufacturers and healthcare providers to navigate these challenges and ensure continued access to valuable health sensing technologies.

Current US tariff policies can indirectly impact the market by affecting the cost of imported electronic components, microcontrollers, and specialized sensors used in the manufacturing of health sensor devices. The production of sophisticated health sensors often relies on complex global supply chains for these critical parts, and tariffs imposed on imported components can increase manufacturing costs for companies operating in or importing into the US.

For instance, according to the US International Trade Commission DataWeb, US imports for consumption of instruments and appliances used in medical, surgical, dental or veterinary sciences (under HTS 9018), a broad category that includes various medical sensors and diagnostic apparatus, had a Customs Value of approximately US$29.36 billion in 2023, indicating the substantial volume and associated tariff costs within this sector. These increased input costs present a financial challenge for device manufacturers, potentially leading to higher prices for health sensor products, which could impact affordability and accessibility for consumers and healthcare systems.

However, the growing recognition of the value of health sensors in improving health outcomes and empowering individuals provides a strong incentive for continued market growth, driving stakeholders to optimize supply chains and mitigate cost pressures to ensure widespread availability of these beneficial technologies.

Latest Trends

Miniaturization and integration of sensors into wearables is a recent trend

Miniaturization and the seamless integration of health sensors into wearable devices are a significant recent trend in the market. Sensors are becoming smaller, more power-efficient, and capable of being integrated into a wider range of form factors, including smartwatches, fitness trackers, patches, and even clothing. This trend enhances user comfort and convenience, enabling continuous and unobtrusive health monitoring throughout the day and night.

The increasing sophistication of these integrated sensors allows for the capture of a broader range of physiological data points with greater accuracy. Companies in the wearables sector are heavily investing in this trend; Garmin, a major player in connected wearables with health monitoring features, reported record revenue of US$6.30 billion in fiscal year 2024, an increase of 20% compared to the prior year, with growth across all segments including fitness, highlighting the strong consumer adoption of sensor-equipped wearable devices.

Regional Analysis

North America is leading the Health Sensors Market

North America dominated the market with the highest revenue share of 37.4% owing to a heightened focus on personal health monitoring and the increasing incidence of chronic conditions. The US Centers for Disease Control and Prevention (CDC) highlights that approximately 6 in 10 Americans live with at least one chronic disease, underscoring the need for continuous health monitoring solutions.

Wearable devices, equipped with sensors tracking metrics like heart rate and activity, have seen widespread adoption. For instance, a report indicated that North America held the largest share of the global wearable medical devices market in 2024. The FDA’s initiatives in digital health are also fostering the integration of these sensing technologies into mainstream healthcare.

The Asia Pacific region is expected to experience the highest CAGR during the forecast period

Asia Pacific is expected to grow with the fastest CAGR owing to the region’s growing geriatric population and the rising prevalence of chronic diseases. In 2022, Asia accounted for a significant proportion of global cardiovascular disease cases, increasing the demand for monitoring devices. Governments across the Asia Pacific are also investing more in digital health infrastructure.

For example, India introduced a digital health ecosystem under the Ayushman Bharat Digital Health Mission (ABDM) in 2022. The increasing penetration of smartphones and internet access is also expected to facilitate the broader adoption of these monitoring technologies in the region.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia

- Netherland

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- New Zealand

- Singapore

- Thailand

- Vietnam

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Key Players Analysis

Key players in the health sensors market drive growth by developing innovative, miniaturized, and wireless devices that enable continuous monitoring of vital signs and health parameters. They invest in integrating AI and machine learning to enhance data accuracy and provide personalized health insights. Companies form strategic partnerships with healthcare providers and technology firms to expand their product reach and improve user experience.

Many focus on entering emerging markets to tap into the rising demand for remote patient monitoring and preventive care solutions. Continuous research and development fuel the creation of versatile, cost-effective sensors suited for diverse healthcare applications.

Apple Inc. stands out as a major player in this market, leveraging its expertise in consumer electronics to deliver advanced wearable health monitoring devices like the Apple Watch. The company integrates multiple sensors that track heart rate, blood oxygen, and ECG, providing users with real-time health data and alerts. Apple’s strong ecosystem, combining hardware, software, and health services, creates a seamless experience for consumers and healthcare professionals alike. The company’s focus on innovation and user-friendly design has positioned it as a leader in personal health technology worldwide.

Top Key Players

- Stryker Corporation

- Smith’s Medical Inc

- Sibel Health

- Sensirion AG

- Koninklijke Philips

- GE Healthcare

- DuPont Liveo Healthcare Solutions

- Danaher Corporation

Recent Developments

- In October 2023, Sibel Health launched Discovery, a next-generation physiological monitoring platform crafted specifically for use in clinical trials. The platform combines FDA-cleared wearable sensors with real-time vital sign tracking and integrates novel digital endpoints to enhance clinical data collection and analysis.

- In November 2023, DuPont Liveo Healthcare Solutions entered into a collaboration with STMicroelectronics, a key player in semiconductor innovation, to jointly conceptualize a smart wearable device aimed at enabling remote monitoring of biological signals, blending materials science with cutting-edge electronics.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2024) | US$ 49.9 billion |

| Forecast Revenue (2034) | US$ 286.6 billion |

| CAGR (2025-2034) | 19.1% |

| Base Year for Estimation | 2024 |

| Historic Period | 2020-2023 |

| Forecast Period | 2025-2034 |

| Report Coverage | Revenue Forecast, Market Dynamics, COVID-19 Impact, Competitive Landscape, Recent Developments |

| Segments Covered | By Product Type (Heart Rate Sensors, Temperature Sensors, Blood Glucose Sensors, Blood Oxygen Sensors, and Others), By Technology (Handheld Diagnostic Sensors (Chronic Illness & At Risk-Monitoring, Patient Admission Triage, Logistical Tracking, In Hospital Clinical Monitoring, and Post-Acute Care Monitoring) and Wearable Sensors (Disposable Wearable Sensors, Non-Disposable Wearable Sensors, and Implantable/Ingestible Sensors)), By Application (Handheld Diagnostic Sensors, Chronic Illness & At Risk-Monitoring, Wellness Monitoring, Patient Admission Triage, and Others), By End-user (Hospitals & Clinics, Long-Term Care Centers & Nursing Homes, Home Care Settings, and Others) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, New Zealand, Singapore, Thailand, Vietnam, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA |

| Competitive Landscape | Stryker Corporation, Smith’s Medical Inc, Sibel Health, Sensirion AG, Koninklijke Philips, GE Healthcare, DuPont Liveo Healthcare Solutions, Danaher Corporation. |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |