Quick Navigation

Report Overview

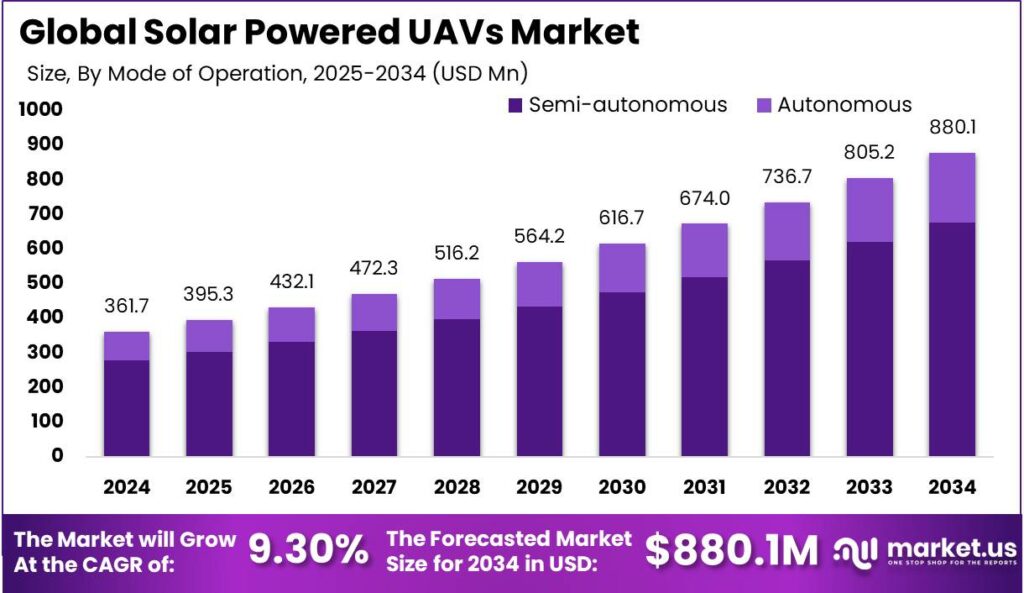

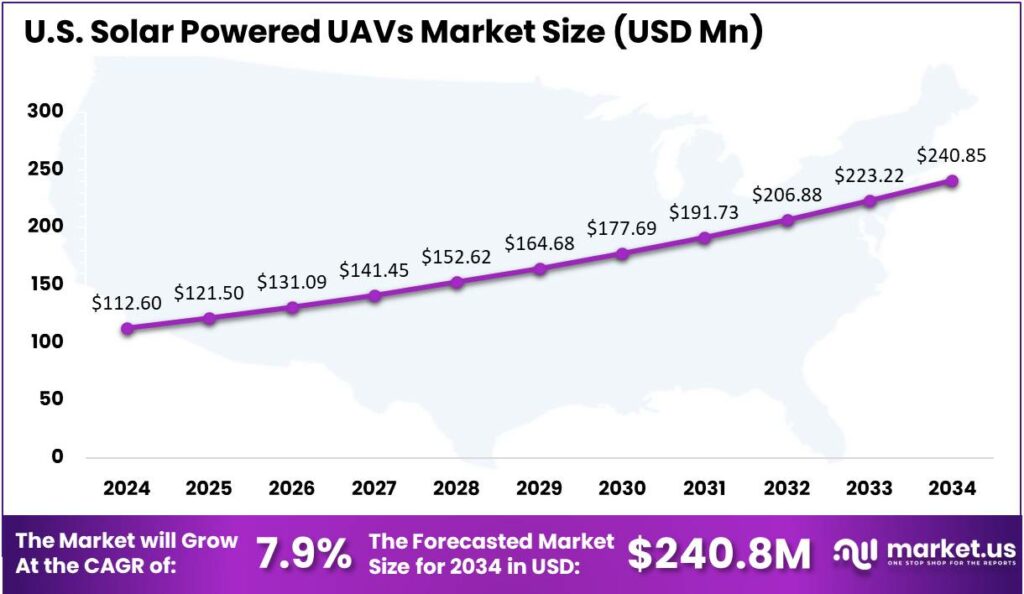

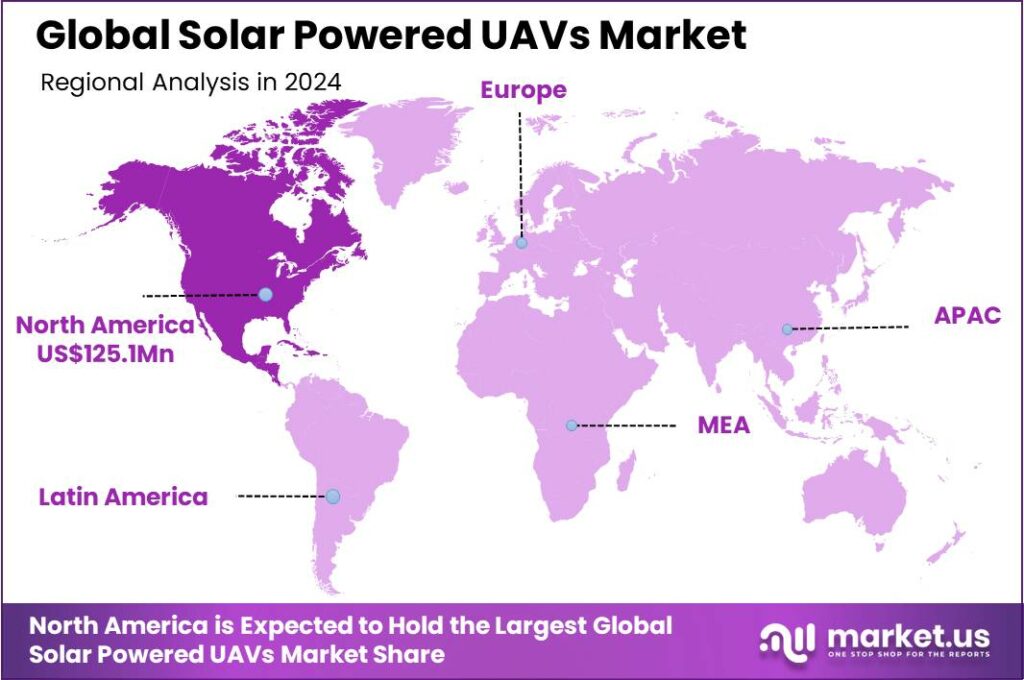

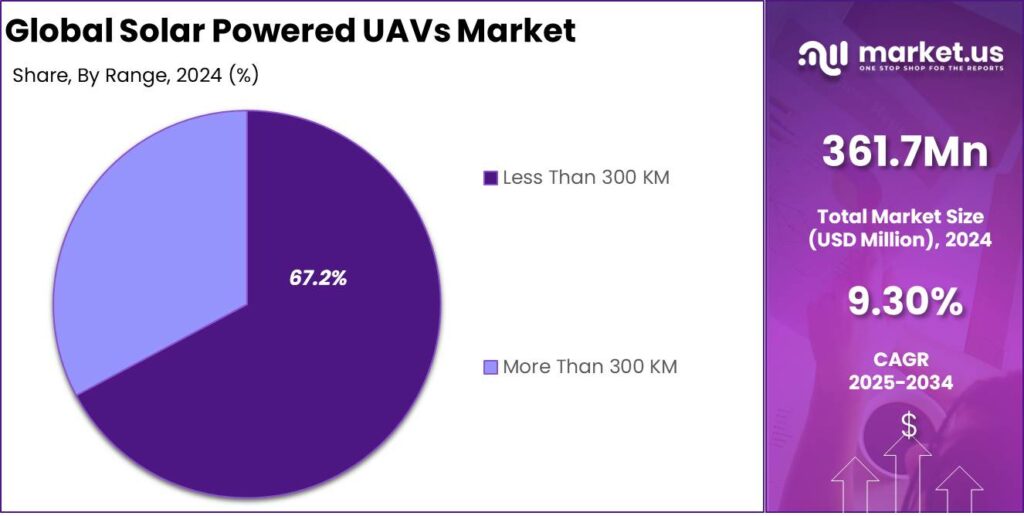

The Global Solar Powered UAVs Market size is expected to be worth around USD 880.1 Million By 2034, from USD 361.7 Million in 2024, growing at a CAGR of 9.30% during the forecast period from 2025 to 2034. In 2024, North America led the global solar-powered UAV market with over 34.6% market share, generating approximately USD 125.1 million in revenue. The U.S. market alone was valued at USD 112.6 million and is projected to grow at a 7.9% CAGR.

Solar-powered UAVs, or solar drones, use photovoltaic cells to harness solar energy for sustained flight without traditional fuel. Equipped with lightweight solar panels, they convert sunlight into electrical power for propulsion and electronics. The solar UAV market includes the aircraft, supporting systems, sensors, energy storage, and software for commercial, civil, and military applications.

The solar-powered UAV market is growing due to technological advancements and the global shift toward clean energy. Key drivers include the demand for long-endurance UAVs in defense, border control, and maritime patrol, where solar UAVs offer a cost-effective, eco-friendly alternative. The demand for real-time data and high-resolution imaging in agriculture, environmental monitoring, and disaster relief is driving adoption in civilian sectors.

Government support for green energy and unmanned aviation, along with advancements in solar cells and battery technologies, is driving the growth of solar-powered UAVs. These UAVs are gaining attention for global connectivity projects, especially in areas lacking internet infrastructure. This convergence of trends positions the solar UAV market for steady growth, fueled by sustainability goals and strategic needs.

Several factors are propelling the adoption of solar-powered UAVs. The need for persistent surveillance capabilities, especially in defense and border security, has led to increased utilization of these drones. In agriculture, they offer efficient monitoring of large tracts of land, aiding in precision farming practices. Additionally, their ability to operate in remote and inaccessible areas makes them valuable for disaster management and environmental studies.

For instance, In October 2024, AeroVironment successfully tested its upgraded solar-powered HALE aircraft, Horus A, developed with SoftBank. As an advanced version of the Sunglider platform, it offers stronger stratospheric payload capacity. This upgrade positions it for key roles in surveillance and telecom services, marking a major step in high-altitude connectivity solutions.

Recent advancements in lightweight materials, efficient solar panels, and energy storage have greatly improved solar-powered UAVs’ flight durations and payload capacities. For example, BAE Systems’ PHASA-35 can remain airborne for up to a year, enhancing surveillance and communication. These innovations are broadening the UAVs’ operational potential across various applications.

Key Takeaways

- The global Solar Powered UAVs Market size is expected to reach USD 880.1 Million by 2034, up from USD 361.7 Million in 2024, reflecting a CAGR of 9.30% during the forecast period from 2025 to 2034.

- In 2024, the Semi-autonomous segment held a dominant market position, accounting for more than 77.1% of the global Solar Powered UAVs market by mode of operation.

- The Multirotor drones segment also captured a significant market share in 2024, holding over 61.8% of the global solar-powered UAVs market.

- The Less Than 300 KM segment maintained a dominant market position in 2024, representing more than 67.2% of the global solar-powered UAVs market.

- In 2024, the Commercial segment led the market with a dominant share of more than 29.4% in the global Solar Powered UAVs market.

- North America held a leading position in the global solar-powered UAVs market in 2024, capturing over 34.6% of the market share, generating approximately USD 125.1 million in revenue.

- Specifically, the U.S. solar-powered UAV market was valued at around USD 112.6 million in 2024, and is expected to grow at a 7.9% CAGR.

U.S. Economic Growth

In 2024, the U.S. solar powered unmanned aerial vehicles (UAVs) market was valued at approximately USD 112.6 million, marking a significant foothold in the global renewable aviation segment. Solar-powered UAVs, using panels on their wings or fuselage, are gaining traction in civilian and defense sectors due to rising demand for long-endurance surveillance, low-emission platforms, and energy-efficient aviation.

The market is projected to grow at a 7.9% CAGR, driven by tech innovation and strong government interest. Agencies like NASA, the DoD, and NOAA are exploring solar UAVs for long-endurance, high-altitude missions where traditional drones fall short, enabling new applications in surveillance, disaster response, and environmental monitoring.

Increased federal investment in clean energy and U.S. decarbonization goals are driving the adoption of solar-powered UAVs in defense and aviation. Technological advances in lightweight materials, efficient solar cells, and energy storage are boosting performance and reliability, supporting long-term market growth despite challenges like payload limits and weather sensitivity.

In 2024, North America held a dominant market position in the global solar powered UAVs market, capturing more than a 34.6% share and generating approximately USD 125.1 million in revenue. This regional dominance can be attributed to a robust defense infrastructure, widespread technological advancement in renewable aviation, and the presence of leading UAV manufacturers and aerospace innovators such as AeroVironment and Boeing.

Government agencies like NASA, the DoD, and the DOE have significantly advanced solar UAV R&D and deployment. The U.S. military uses solar UAVs for extended surveillance missions, reducing the need for refueling. Supportive federal policies targeting net-zero emissions in aviation and defense further drive demand for efficient, sustainable solar-powered drones.

North America’s lead in photovoltaic tech and drone autonomy boosts its dominance in the solar UAV market. Research institutions and private firms are advancing solar efficiency, lightweight materials, and energy storage for low-light operation. Rising commercial use in agriculture, monitoring, and telecom, driven by U.S. startups, adds to growing non-military demand. Together, innovation, government backing, and private investment position North America as a global solar UAV leader.

Mode of Operation Analysis

In 2024, the Semi-autonomous segment held a dominant market position, capturing more than a 77.1% share in the global Solar Powered UAVs market by mode of operation. Industries like defense, agriculture, and infrastructure prefer semi-autonomous UAVs for their blend of automated flight and manual override, offering reliability in dynamic conditions and enabling real-time decision-making.

Semi-autonomous solar UAVs are more cost-effective to deploy and maintain than fully autonomous models, which require expensive AI systems, sensors, and real-time processing. Their affordability and easier integration into existing workflows make them appealing for sectors like precision farming and environmental monitoring, especially in price-sensitive markets.

Another critical reason for the segment’s lead is the existing regulatory environment. In most countries, aviation authorities impose tighter restrictions on fully autonomous UAV operations due to concerns around airspace safety, data privacy, and liability in case of system failures. Semi-autonomous UAVs, which allow human oversight and intervention, face fewer barriers to approval and certification.

The semi-autonomous segment is benefiting from upgrades in flight automation software and solar power management, improving efficiency without full independence. Operators can program flight paths, energy use, and mission schedules while maintaining manual control for critical moments. As technology advances, semi-autonomous solar UAVs are expected to remain the preferred choice for organizations seeking a balance of automation, control, and cost-efficiency.

Type Analysis

In 2024, Multirotor drones segment held a dominant market position, capturing more than a 61.8% share in the global solar-powered UAVs market. This dominance can be attributed to the structural flexibility, maneuverability, and vertical takeoff and landing capabilities of multirotor designs, which make them ideal for a wide variety of civilian and defense applications.

These drones are particularly suitable for operations requiring stable hovering, such as aerial photography, environmental monitoring, and short-range surveillance, where endurance and solar integration play a crucial role. Their ability to stay aloft while conserving battery energy through solar panels makes them highly efficient for medium-duration missions, especially in areas with limited infrastructure.

The rising demand from sectors like agriculture, infrastructure inspection, and public safety has further accelerated the growth of multirotor solar UAVs. Unlike fixed-wing drones, which need runway space, or hybrid drones that are still in early-stage adoption, multirotors offer plug-and-play usability in both rural and urban settings.

Another reason for their market leadership is the recent improvement in lightweight solar cell integration. Multirotor drones now feature flexible solar panels that wrap around rotor arms and upper fuselages, optimizing surface area for solar absorption without compromising mobility. These advancements in energy harvesting have effectively extended flight times and reduced dependency on traditional battery recharging methods.

Range Analysis

In 2024, the Less Than 300 KM segment held a dominant market position in the global solar powered UAVs market, capturing more than a 67.2% share. This segment’s leadership is primarily driven by its suitability for short-range surveillance, environmental monitoring, and agricultural mapping applications.

These drones are particularly favored for their compact design, lower production costs, and operational simplicity, making them ideal for commercial and civilian users who require efficient yet affordable aerial solutions. The lower range also ensures more stability and better control, which is essential in applications like wildlife tracking, crop inspection, and infrastructure monitoring.

One of the key reasons behind the dominance of the Less Than 300 KM segment is the rapid adoption of solar UAVs in precision farming and urban infrastructure surveillance, where long-distance travel is not a requirement. For instance, drones with this range are being deployed to monitor irrigation levels, detect pest infestations, or assess solar panel installations across industrial rooftops and farms.

The segment benefits from fewer regulatory restrictions, as short-range UAVs face less stringent airspace rules, simplifying deployment for commercial operators. Demand from educational and research institutions for localized environmental studies has also driven adoption, due to their cost-efficiency and manageable flight control systems.

End-user Analysis

In 2024, Commercial segment held a dominant market position, capturing more than a 29.4% share in the global Solar Powered UAVs market. This growth was driven by the rising use of solar UAVs in industries such as telecommunications, infrastructure inspection, logistics, and environmental monitoring.

Commercial enterprises are increasingly deploying solar-powered drones for their ability to stay airborne for longer durations without requiring fuel refills or frequent battery swaps. This endurance makes them ideal for tasks like surveying large construction projects, pipeline monitoring, and providing aerial internet connectivity in rural or remote areas.

The commercial sector has also embraced solar UAVs due to their cost-efficiency and low environmental impact. Businesses are under growing pressure to reduce carbon footprints and adopt greener technologies. Solar UAVs provide a sustainable alternative to fossil-fuel-based aerial vehicles, allowing companies to carry out aerial operations while aligning with ESG goals.

The segment’s leadership is driven by the growing use of data-driven decision-making. AI-equipped UAVs with cameras, thermal sensors, and LiDAR systems gather real-time data for tasks like crop monitoring and wind farm inspections. Their ability to perform data-intensive tasks autonomously, without frequent landings, enhances efficiency and safety across industries.

Key Market Segments

By Mode of Operation

- Semi-autonomous

- Autonomous

By Type

- Fixed wing drones

- Multirotor drones

- Hybrid

By Range

- Less Than 300 KM

- More Than 300 KM

By End-user

- Government & Defense

- Commercial

- Agricultural

- Others

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Singapore

- Rest of Asia Pacific

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Driver

Demand for Long-Endurance, Eco-Friendly Surveillance

The growing demand for continuous aerial surveillance has driven the rise of solar-powered UAVs. Unlike traditional battery-powered drones with limited flight time, solar UAVs use solar energy for extended operations, minimizing the need for frequent landings and ground charging.

Solar-powered UAVs align with global sustainability goals by using renewable energy to lower carbon emissions and reduce fuel and maintenance costs. Their eco-friendly design attracts organizations focused on minimizing environmental impact. Advances in solar panel efficiency, energy storage, and lightweight materials have improved their commercial viability, increasing both payload capacity and operational range.

Restraint

Technical Limitations and Environmental Dependencies

Solar-powered UAVs face challenges due to their reliance on sunlight, limiting efficiency in areas with low solar exposure or adverse weather. Cloud cover, rain, and shorter daylight hours can reduce energy harvesting, restricting flight duration and mission effectiveness.

Integrating solar panels into UAVs adds weight and complexity, which can impact aerodynamic efficiency, payload capacity, and maneuverability. Current battery technology limits energy storage, making continuous operation difficult during nighttime or cloudy conditions. Additionally, the high initial cost of developing solar-powered UAVs, due to advanced materials and specialized components, presents a financial challenge, especially for small enterprises.

Opportunity

Expansion into Remote and Infrastructure-Limited Regions

Solar-powered UAVs offer significant potential in remote areas with limited infrastructure, providing services like internet connectivity, environmental monitoring, and disaster response. In rural or isolated communities, they can act as aerial communication relays, bridging the digital divide, especially in developing countries with minimal ground infrastructure. Their independence from ground power sources makes them ideal for rapid deployment in emergencies.

Solar-powered UAVs are valuable in environmental conservation, enabling monitoring of ecosystems, tracking wildlife, and detecting illegal activities like poaching. Their long flight times and low environmental impact allow continuous, non-disruptive observation. Additionally, their scalability supports commercial uses such as agricultural monitoring, pipeline inspection, and mineral exploration, enhancing efficiency and safety in remote or hazardous areas.

Challenge

Regulatory and Airspace Integration Issues

The integration of solar-powered UAVs into existing airspace systems faces regulatory challenges due to aviation rules designed for manned aircraft. A key issue is the absence of standardized regulations for beyond-visual-line-of-sight (BVLOS) operations, which are crucial for long-endurance solar UAVs. Without clear guidelines, operators may encounter legal and logistical hurdles, hindering market growth.

Airspace congestion and potential conflicts with manned aircraft pose challenges for UAV integration, requiring advanced traffic management and collision avoidance systems. The lack of such systems can compromise safety and operational flexibility. Additionally, varying international regulations on UAV classification, flight zones, and operational rules complicate cross-border operations, limiting scalability and efficiency.

Emerging Trends

A key trend is the integration of solar power with high-altitude, long-endurance (HALE) UAVs. Platforms like the BAE Systems PHASA-35 and India’s CATS Infinity project are designed for extended stratospheric flights, offering services like surveillance, communication, and environmental monitoring, showcasing global interest in solar-powered UAVs.

Another emerging development is the combination of solar energy with hydrogen fuel cells. This hybrid approach enhances the endurance and reliability of UAVs, making them suitable for missions requiring continuous operation over vast areas .

Furthermore, the adoption of artificial intelligence (AI) and machine learning in UAV systems is enabling autonomous operations, real-time data analysis, and adaptive mission planning. These capabilities are particularly beneficial for applications like disaster response, agriculture, and infrastructure inspection .

Business Benefits

Solar-powered UAVs can remain airborne for significantly longer periods compared to traditional battery-powered drones. By harnessing solar energy during daylight hours, these UAVs reduce the need for frequent landings and recharging. This capability is particularly beneficial for applications requiring continuous monitoring, such as environmental surveillance and infrastructure inspection.

Solar-powered UAVs produce zero emissions during flight, aligning with global sustainability goals. Their operation reduces the carbon footprint of aerial activities, making them suitable for eco-sensitive missions and companies committed to environmental responsibility.

The unique capabilities of solar-powered UAVs make them suitable for a wide range of applications, including telecommunications, surveillance, and scientific research. Their ability to operate at high altitudes for extended periods allows them to function as pseudo-satellites, providing services traditionally reserved for orbital satellites but at a lower cost.

Key Player Analysis

Advances in solar tech and light materials have led key companies to drive innovation in solar-powered UAVs.

AeroVironment is a pioneer in the solar UAV market. Known for the iconic “Helios” and “Pathfinder” projects, the company has long focused on developing high-altitude, long-endurance UAVs for both commercial and military applications. Their UAVs are designed for ultra-efficient flight using solar panels, offering unmatched endurance and clean energy usage.

Airbus SE, a major name in aerospace, has made a significant impact with its Zephyr solar-powered UAV. This high-altitude pseudo-satellite (HAPS) system can stay aloft for weeks, making it a strong alternative to traditional satellites for surveillance, earth observation, and communication. Airbus’s large-scale production capabilities and global reach give it a strong competitive edge in this niche but growing market.

Atlantik Solar, developed by ETH Zurich, is known for its fully autonomous solar-powered UAV that completed one of the longest-ever continuous solar-powered flights. Its uniqueness lies in combining real-world field tests with advanced power management, making it a notable player in low-power, high-efficiency UAV designs.

Top Key Players in the Market

- AeroVironment Inc.

- Airbus SE

- Atlantik Solar

- Aurora Flight Sciences

- Avy

- BAE Systems

- Chinese Academy of Aerospace Aerodynamics

- DJI

- Elektra

- Eos Technologie

- Kea Aerospace

- Korea Aerospace Research Institute

- QinetiQ

- Silent Falcon UAS Technologies

- Skydweller Aero

- Sunbirds SAS

- Uav-instruments

- Others

Opportunities for Industry Players

- Extended Surveillance and Monitoring: Solar-powered UAVs offer prolonged flight durations, making them ideal for continuous surveillance and monitoring tasks. Their extended operational range without refueling is ideal for border security, disaster assessment, and environmental monitoring, cutting costs and improving data collection efficiency.

- Agricultural Applications: In agriculture, solar UAVs provide farmers with real-time data on crop health, irrigation needs, and pest infestations. Their extended flight times allow for comprehensive coverage of large farming areas, leading to more informed decision-making and optimized resource utilization. This technology supports precision farming practices, contributing to increased yields and sustainability.

- Telecommunications and Connectivity: High-altitude solar UAVs can function as pseudo-satellites, delivering internet connectivity to remote and underserved regions. Companies like Airbus are developing solar-powered drones capable of providing communication services, which is particularly valuable in disaster-stricken areas where traditional infrastructure is compromised.

- Environmental and Climate Research: Solar UAVs are instrumental in conducting environmental and climate research. Their ability to fly at high altitudes for extended periods enables the collection of atmospheric data, monitoring of wildlife, and assessment of ecological changes.

- Military and Defense Operations: The defense sector benefits from solar UAVs’ endurance and stealth capabilities. They are utilized for intelligence gathering, reconnaissance missions, and communication support. Their prolonged flight times and minimal acoustic signatures make them suitable for operations in contested or sensitive areas, enhancing situational awareness and operational effectiveness.

Industry News

- In March 2025, Kea Aerospace partnered with Li-S Energy to integrate advanced lithium-sulfur battery technology into its high-altitude UAVs, aiming to significantly enhance flight endurance and operational efficiency.

- In February 2024, India’s National Aerospace Laboratories tested a solar-powered UAV that flew for over 21 hours, showing how solar drones can support long-term missions without needing frequent landings or battery changes.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2024) | USD 361.7 Mn |

| Forecast Revenue (2034) | USD 880.1 Mn |

| CAGR (2025-2034) | 9.30% |

| Base Year for Estimation | 2024 |

| Historic Period | 2020-2023 |

| Forecast Period | 2025-2034 |

| Report Coverage | Revenue forecast, AI impact on market trends, Share Insights, Company ranking, competitive landscape, Recent Developments, Market Dynamics and Emerging Trends |

| Segments Covered | By Mode of Operation (Semi-autonomous, Autonomous), By Type (Fixed wing drones, Multirotor drones, Hybrid), By Range (Less Than 300 KM, More Than 300 KM), By End-user (Government & Defense, Commercial, Agricultural, Others) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, New Zealand, Singapore, Thailand, Vietnam, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA |

| Competitive Landscape | AeroVironment Inc., Airbus SE, Atlantik Solar, Aurora Flight Sciences, Avy, BAE Systems, Chinese Academy of Aerospace Aerodynamics, DJI, Elektra, Eos Technologie, Kea Aerospace, Korea Aerospace Research Institute, QinetiQ, Silent Falcon UAS Technologies, Skydweller Aero, Sunbirds SAS, Uav-instruments, Others |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three license to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |