Quick Navigation

Report Overview

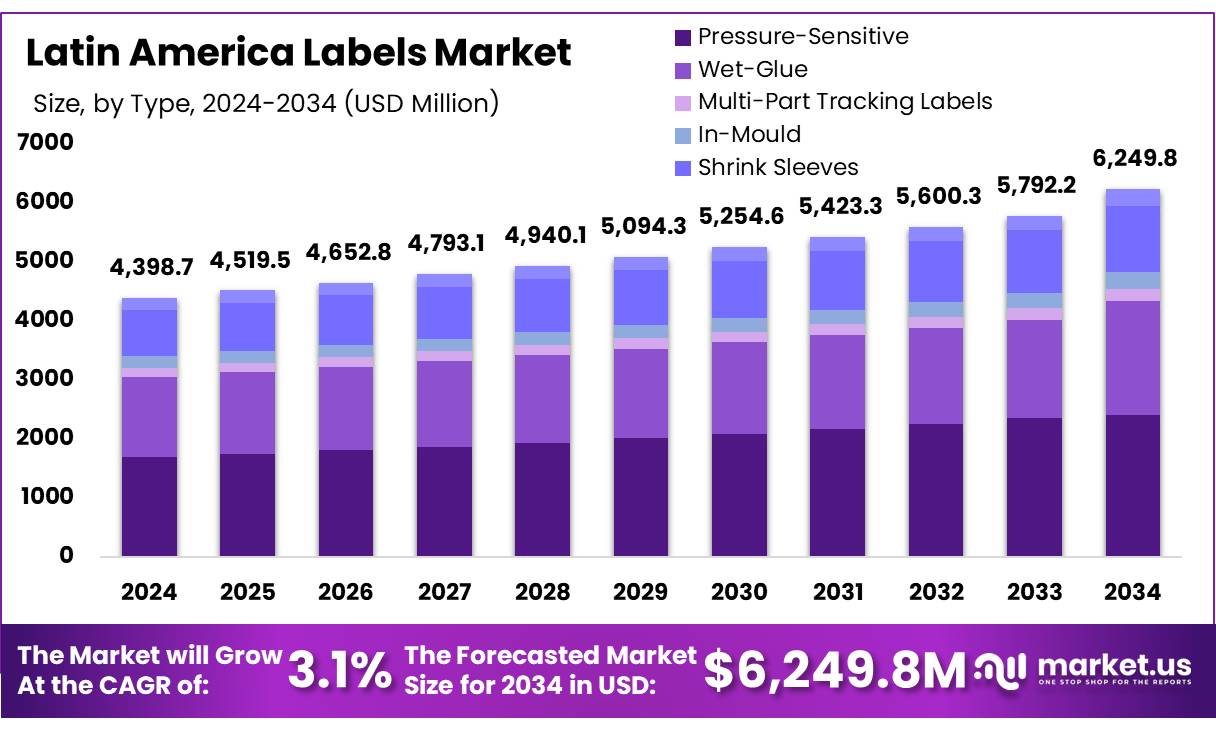

The Latin America Labels Market size is expected to be worth around USD 6249.8 Mn by 2034, from USD 4,398.7 Mn in 2024, growing at a CAGR of 3.1% during the forecast period from 2025 to 2034.

Labels serve as a critical component in the packaging and branding ecosystem by providing essential information about a product, including its name, brand, ingredients, manufacturing details, price, and safety warnings.

Several factors are fueling the growth of the Latin America labels market, including the increasing demand for personalized and visually attractive packaging, coupled with the rise of the packaged food industry. The surge in e-commerce has also driven the need for transit and return labels, further stimulating market expansion. Additionally, regulatory pressures have intensified the focus on providing comprehensive product information, contributing to the adoption of advanced label technologies in various sectors.

Key Takeaways

- Latin America labels market is valued at USD 4,398.7 million in 2024 and is estimated to register a CAGR of 3.1%.

- Latin America labels market is projected to reach USD 5,792.2 million by 2034.

- In Latin America labels market, Pressure-Sensitive type labels held the majority of revenue share in 2024 of 38.5%.

- Among the materials, Paper accounted for the majority of the market share, with 34.4%.

- Between printing technologies, Flexographic Printing accounted for the largest market share in 2024, with 32.9%.

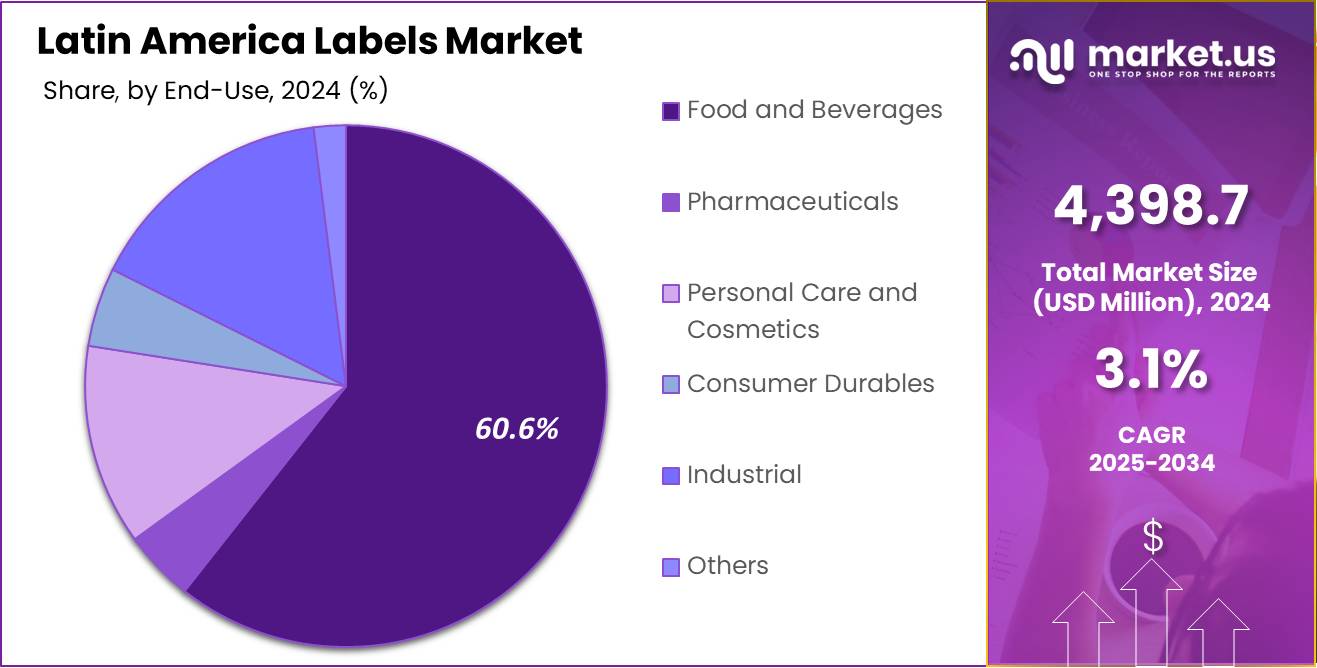

- Among end-uses, Food and Beverages accounted for the majority of the market share, with 60.6%.

- In Latin America, Brazil accounted for the largest market share with 43.9% among other countries.

Type Analysis

Pressure-Sensitive Accounted for The Largest Market Share

Latin America labels market is segmented based on type into pressure-sensitive, wet-glue, multi-part tracking labels, in-mold, shrink sleeves, others. Among these, pressure-sensitive type labels held the majority of the market share, with 38.5% due to their versatility, ease of End-Use, and cost-effectiveness. These labels are self-adhesive, requiring no heat, water, or solvent for End-Use, making them highly convenient for manufacturers and consumers alike. Their widespread use in various industries, such as food and beverages, consumer goods, pharmaceuticals, and logistics, further contributes to their dominance in the market.

Additionally, pressure-sensitive labels offer excellent design flexibility, durability, and high-quality printing, which makes them an ideal choice for branding and product information. The growing demand for customizable packaging solutions, coupled with the increasing need for efficient labeling, has driven the preference for pressure-sensitive labels in the region. Moreover, the rising trend of e-commerce and retail packaging also bolstered the demand for this label type, cementing its leadership in the market.

Latin America Labels Market, By Type, 2020-2024 (USD Mn)

| Type | 2020 | 2021 | 2022 | 2023 | 2024 |

|---|---|---|---|---|---|

| Pressure-Sensitive | 1,530.8 | 1,560.2 | 1,593.8 | 1,640.2 | 1,691.4 |

| Wet-Glue | 1,270.5 | 1,288.3 | 1,308.8 | 1,333.9 | 1,360.1 |

| Multi-Part Tracking Labels | 138.7 | 140.8 | 143.3 | 146.4 | 149.8 |

| In-Mould | 183.9 | 186.7 | 190.1 | 194.6 | 199.7 |

| Shrink Sleeves | 724.7 | 737.6 | 752.5 | 772.2 | 794.0 |

| Others | 192.6 | 194.6 | 197.0 | 200.2 | 203.7 |

Material Analysis

Paper Material Dominated Latin America Labels Market

Based on a material, the market is segmented into paper, polypropylene, polyester, polyvinyl chloride, polycarbonate, others. Among these, paper holds the largest share, accounting for 34.4% of the market. This significant share highlights the predominant use of paper in various industries, driven by its versatility, sustainability, and widespread adoption. Paper is used extensively across packaging, printing, and labeling, contributing to its dominant position.

Additionally, the growing demand for eco-friendly and recyclable materials has further boosted the popularity of paper in comparison to synthetic alternatives such as polypropylene and polycarbonate. Paper’s ability to meet both functional and environmental demands makes it a preferred choice in numerous End-Uses, solidifying its leadership in the market. Although other materials like polypropylene and polyester also play substantial roles, the paper segment continues to be the major user, supported by a strong consumer preference for sustainable and biodegradable options.

Latin America Labels Market, By Material, 2020-2024 (USD Mn)

| Material | 2020 | 2021 | 2022 | 2023 | 2024 |

|---|---|---|---|---|---|

| Paper | 1,372.2 | 1,398.7 | 1,428.5 | 1,469.3 | 1,513.9 |

| Polypropylene | 99.0 | 99.7 | 100.7 | 101.7 | 102.7 |

| Polyester | 995.1 | 1,012.8 | 1,033.5 | 1,059.7 | 1,088.3 |

| Polyvinyl Chloride | 1,169.3 | 1,186.5 | 1,206.6 | 1,233.6 | 1,263.6 |

| Polycarbonate | 103.8 | 104.9 | 106.2 | 107.7 | 109.3 |

| Others | 301.7 | 305.6 | 310.1 | 315.4 | 320.9 |

Printing Technology Analysis

Due to Their Versatility and Cost-Effectiveness Flexographic Printing Technologies Dominated the Market.

Based on printing technologies, the market is further divided into flexographic printing, offset printing, digital printing, gravure printing, screen printing, letterpress printing and others. Among these technologies, flexographic printing accounted for the largest market share in 2024, with 32.9% primarily due to its versatility, speed, and cost-effectiveness. This printing technology is widely used for high-volume printing on a variety of substrates, including paper, plastic, and foil, which makes it ideal for packaging End-Uses such as labels, corrugated boxes, and flexible films.

Its ability to print on uneven surfaces and its suitability for long runs with minimal setup times make it highly efficient for industries requiring fast turnaround times, such as food and beverage, retail, and consumer goods. Additionally, advancements in flexographic printing inks and plates have improved print quality, making it an increasingly popular choice among manufacturers. As a result, its broad End-Use across diverse industries and its continuous innovation in terms of sustainability and operational efficiency have driven its dominance in the market.

Latin America Labels Market, By Printing Technology, 2020-2024 (USD Mn)

| Printing Technology | 2020 | 2021 | 2022 | 2023 | 2024 |

|---|---|---|---|---|---|

| Flexographic Printing | 1,308.6 | 1,334.1 | 1,363.4 | 1,402.6 | 1,446.2 |

| Offset Printing | 864.2 | 878.0 | 894.2 | 914.1 | 934.8 |

| Digital Printing | 522.6 | 533.9 | 546.7 | 564.1 | 583.3 |

| Gravure Printing | 422.0 | 428.2 | 435.4 | 445.0 | 455.5 |

| Screen Printing | 182.8 | 184.9 | 187.2 | 190.3 | 193.7 |

| Letterpress Printing | 399.2 | 404.2 | 410.1 | 417.7 | 426.0 |

| Others | 341.7 | 344.9 | 348.6 | 353.7 | 359.2 |

End-Use Analysis

Based on End-Uses, the market is further divided into food and beverages, pharmaceuticals, personal care and cosmetics, consumer durables, industrial, others. Among these End-Uses, food and beverages accounted for the largest market share in 2024, with 60.6% due to the growing demand for packaging solutions that ensure product safety, quality, and appeal. This industry relies heavily on high-quality printing for labels, packaging, and branding, which are crucial for attracting consumers and complying with regulatory standards.

The rapid growth of the food and beverage sector, driven by changing consumer preferences and the increasing demand for packaged goods, has fueled the need for effective printing technologies. Flexographic printing, commonly used in this End-Use, allows for efficient, high-volume production of printed materials on various packaging substrates such as plastic, paper, and foil. Additionally, with a focus on sustainability and eco-friendly packaging, the food and beverage industry is increasingly adopting advanced printing technologies that meet both aesthetic and functional requirements. This combination of factors has solidified food and beverages as the dominant End-Use in the market.

Latin America Labels Market, By End-Use, 2020-2024 (USD Mn)

| End-Use | 2020 | 2021 | 2022 | 2023 | 2024 |

|---|---|---|---|---|---|

| Food and Beverages | 2,425.2 | 2,470.8 | 2,522.8 | 2,591.1 | 2,666.6 |

| Pharmaceuticals | 182.5 | 184.6 | 187.0 | 190.3 | 193.7 |

| Personal Care and Cosmetics | 511.5 | 518.3 | 526.4 | 536.8 | 547.7 |

| Consumer Durables | 205.3 | 207.2 | 209.4 | 212.3 | 215.4 |

| Industrial | 632.5 | 642.7 | 654.6 | 670.6 | 687.8 |

| Others | 84.0 | 84.6 | 85.4 | 86.4 | 87.5 |

Key Market Segments

By Type

- Pressure-Sensitive

- Wet-Glue

- Multi-Part Tracking Labels

- In-Mould

- Shrink Sleeves

- Others

By Material

- Paper

- Polypropylene

- Polyester

- Polyvinyl Chloride

- Polycarbonate

- Others

By Printing Technology

- Flexographic Printing

- Offset Printing

- Digital Printing

- Gravure Printing

- Screen Printing

- Letterpress Printing

- Others

By End-Use

- Food and Beverages

- Pharmaceuticals

- Personal Care and Cosmetics

- Consumer Durables

- Industrial

- Others

Drivers

Increasing Demand from Food & Beverage Industry Market in Latin America

The increasing demand from the food and beverage industry in Latin America is significantly boosting the commercial printing market due to several key factors. As the region experiences rising urbanization and a growing middle class, the demand for packaged food and beverage products is soaring. This shift is largely driven by changing consumer lifestyles, where convenience and quality are highly valued, leading to an increased reliance on packaged goods. With this, the need for high-quality printing on labels, packaging, and promotional materials has surged.

Packaging plays a vital role in not only protecting the product but also enhancing its visual appeal, which is crucial for attracting consumers in a competitive market. In particular, flexible packaging is gaining popularity due to its cost-effectiveness, ability to preserve freshness, and ease of transport, further boosting demand for advanced printing solutions.

Moreover, the rise of e-commerce in Latin America has amplified the need for attractive and durable packaging to meet the expectations of online shoppers. As companies strive to differentiate their products on retail shelves or digital platforms, the demand for innovative printing techniques, such as flexographic printing, has become more pronounced. This trend is driving growth in the printing sector, as manufacturers in the food and beverage industry increasingly invest in modern, efficient printing technologies to meet both consumer preferences and regulatory requirements. Thus, the food and beverage industry’s expansion in Latin America is a major catalyst for the commercial printing market’s growth in the region.

Restraints

Recycling Challenges Associated with Certain Label Types May Hinder the Market’s Growth

Recycling complexities associated with pressure sensitive labels release liners and shrink sleeves labels present a significant restraint for the Latin America labels market, primarily due to the difficulties involved in processing these materials and the environmental implications of their disposal. Release liners, which play a critical role in label application by enabling easy separation of the label from its backing, are predominantly manufactured using virgin raw materials such as supercalendered (SC) paper, glassine, and virgin PET resin. While these materials provide the necessary strength and functionality, they also contribute to resource depletion and environmental strain.

The silicone coating used in release liners often contains impurities, including filmic and adhesive residues and foreign plastics, which create a barrier to efficient recyclability. Despite being technically recyclable, the complexity of their composition results in many release liners being incinerated or ending up in landfills, adding to environmental concerns.

Similarly, traditional shrink sleeves, widely used in the food and beverage, personal care, and pharmaceutical industries, pose considerable challenges in recycling due to their multi-layered structure. These sleeves are often composed of polyester-based film (PETG), which has a density similar to that of PET bottles.

During the standard recycling process, where bottles and labels are separated through a float-sink method, PETG labels tend to remain with the PET bottle material, causing contamination in the recovered material stream. When PETG and PET are mixed during recycling, the lower melting point of PETG causes clumping, resulting in defects in the recycled PET, making it less suitable for manufacturing new PET-based products such as bottles and containers.

Opportunity

Growing Demand for Sustainable and Eco-Friendly Labeling Solutions Is Anticipated to Create More Opportunities

The increasing global emphasis on environmental sustainability has significantly influenced industrial packaging practices across major sectors such as food and beverages, personal care, and healthcare. Consumers in Latin America are demonstrating heightened environmental awareness, demanding greater emphasis on product sustainability credentials such as recyclability and carbon neutrality. As sustainability becomes a central focus of product campaigns, manufacturers, retailers, and regulatory authorities are collaborating to reduce the use of environmentally harmful materials and promote the adoption of recyclable and eco-friendly packaging solutions.

Labeling and packaging industries are responding to these demands by focusing on down gauging substrates and transitioning from multilayer structures to mono-materials, which are easier to recycle. Pressure-sensitive and shrink-sleeve labeling technologies, while widely adopted, face increasing scrutiny due to concerns over waste generation during the label production and application stages.

- Colombia was the first country in the region to introduce EPR regulations in 2005, followed by Mexico in 2006. As a result of its early adoption, Colombia now boasts the most comprehensive waste management regulations in the region, covering diverse categories of waste.

- Brazil’s approach to Extended Producer Responsibility (EPR) stands out among its Latin American counterparts due to its implementation of reverse logistics certificates to ensure effective waste management of packaging and related materials. The Brazilian government formalized this initiative by passing Decree No. 11,413 in April 2023, which established a reverse logistics certificate program mandating that producers develop reverse logistics systems for their packaging operations.

Trends

Role of AI and Automation

Artificial intelligence (AI) and machine learning are transforming the label industry by driving automation, enhancing operational efficiency, and enabling the creation of end-to-end ecosystems that optimize processes from design to production. Digital production, once a niche solution, has become a mainstream approach in label conversion, replacing traditional long lead times and high-volume runs with faster turnaround times and the ability to handle short and medium print runs. Digital printing, now a cornerstone for the industry, offers unmatched precision, flexibility, and speed, enabling businesses to meet evolving market demands effectively.

The integration of AI further enhances these capabilities by enabling real-time decision-making, predictive analytics, and workflow optimization, reducing errors, minimizing waste, and improving print quality. As AI-driven solutions continue to advance, they are redefining industry standards, empowering label manufacturers to improve production efficiency, streamline supply chains, and meet sustainability goals, positioning the Latin America labels market for continued growth.

Geopolitical Impact Analysis

The Geopolitical Tensions Significantly Impacted Latin America Labels Market

Geopolitical conflicts have significantly impacted the label printing industry in Latin America by disrupting global supply chains, increasing raw material costs, and introducing operational uncertainties. Regional conflicts and international trade tensions often lead to trade restrictions and tariffs, complicating the procurement of essential materials such as paper, adhesives, and inks. These supply chain disruptions can result in delays and increased costs, challenging label manufacturers to maintain production schedules and profitability.

Additionally, geopolitical instability can lead to currency fluctuations, affecting the cost of imported materials and potentially squeezing profit margins. Political unrest may also prompt governments to implement stringent regulations or change existing policies, requiring manufacturers to adapt quickly to new compliance standards. Moreover, geopolitical tensions can lead to shifts in consumer demand and market dynamics, influencing the volume and types of labeling required. In summary, geopolitical conflicts introduce a layer of complexity and risk to the label printing industry in Latin America, necessitating strategic planning and adaptability to navigate the evolving challenges.

Key Countries Covered

- Latin America

- Brazil

- Mexico

- Chile

- Argentina

- Rest of Latin America

Latin America Label Market, By Country, 2020-2024 (USD Mn)

| Country | 2020 | 2021 | 2022 | 2023 | 2024 |

|---|---|---|---|---|---|

| Brazil | 1,755.1 | 1,787.7 | 1,824.9 | 1,874.5 | 1,928.8 |

| Mexico | 1,073.8 | 1,091.7 | 1,112.5 | 1,139.6 | 1,169.2 |

| Chile | 133.9 | 135.2 | 136.8 | 138.7 | 140.9 |

| Argentina | 273.7 | 276.8 | 280.4 | 285.1 | 290.1 |

| Rest of Latin America | 804.6 | 816.9 | 831.1 | 849.6 | 869.7 |

Key Players Analysis

To Maintain Their Dominance as Industry Leaders in The Latin America Label Market, Companies are Implementing Several Key Strategies

Leading companies are investing in advanced printing technologies such as digital printing, flexographic printing, and sustainable printing solutions. These innovations help improve print quality, reduce lead times, and offer customized solutions for a range of industries, from food and beverage to pharmaceuticals. Through these strategies, companies in the Latin American label market aim to maintain their leadership positions, stay competitive, and adapt to ever-changing market demands.

Market Key Players

- All4Labels Global Packaging Group

- CCL Industries

- Multi-Color Corporation

- Mondi

- Beontag

- Fuji Seal International, Inc.

- Amcor plc

- Diacel Corporation

- Taghleef Industries

- UPM

- DRG Technologies

- PCM

- Nissha Co Ltd.

- Westrock

- Other Key Players

Recent Development

- In December 2024, Multi-Color Corporation (MCC) has acquired Eximpro, a leading Mexican provider of shrink sleeve label (SSL) solutions, expanding its presence in Mexico and the North American market. These acquisition enhances MCC’s capabilities and market reach, with Eximpro leadership team continuing under the MCC Eximpro brand. The move strengthens MCC’s position in the North American SSL market, focusing on growth, innovation, and sustainable solutions.

- In October 2024, All4Labels Global Packaging Group has expanded its partnership with ACTEGA, extending the exclusive commercialization of Signite® “no-label look” technology to include Central and South America. Under the name STARDIRECT™, the technology will be integrated into All4Labels’ STAR Portfolio, focusing on sustainability and circularity, with production scaling up across Europe and South America.

- In June 2024, CCL Industries has acquired the remaining 50% equity of its Middle East joint venture, Pacman-CCL, for $143 million, gaining full ownership of operations in the UAE, Oman, Egypt, Saudi Arabia, and Pakistan.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2024) | USD 4,398.7 Mn |

| Forecast Revenue (2034) | USD 5,792.2 Mn |

| CAGR (2025-2034) | 3.1% |

| Base Year for Estimation | 2024 |

| Historic Period | 2020-2023 |

| Forecast Period | 2025-2034 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Type (Pressure-Sensitive , Wet-Glue , Multi-Part Tracking Labels, In-Mould, Shrink Sleeves, and Others), By Material (Paper, Polypropylene , Polyester, Polyvinyl Chloride, Polycarbonate, and Others), By Printing Technology (Flexographic Printing, Offset Printing, Digital Printing, Gravure Printing, Screen Printing, Letterpress Printing, and Others) By End-use (Food and Beverages, Pharmaceuticals, Personal Care and Cosmetics, Consumer Durables, Industrial, and Others) |

| Regional Analysis | Latin America – Brazil, Mexico, Chile, Argentina, Rest of Latin America |

| Competitive Landscape | All4Labels Global Packaging Group, CCL Industries, Multi-Color Corporation, Mondi, Beontag, Fuji Seal International, Inc., Amcor plc, Diacel Corporation, Taghleef Industries, UPM, DRG Technologies, PCM, Nissha Co Ltd., Westrock, Others |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |