Global Latex Agglutination Test Kits Market By Product Type (ELISA, Serum Neutralization, Indirect Fluorescent, and Hemagglutination Inhibition) By Technology (Blood, Cerebrospinal Fluid, Urine, and Others) By Application (Antibody Detection and Antigen Testing) By End-User (Hospital Pharmacies, Online Pharmacies, and Retail Pharmacies), Region and Companies – Industry Segment Outlook, Market Assessment, Competition Scenario, Trends and Forecast 2025-2034

- Published date: Aug 2025

- Report ID: 156633

- Number of Pages: 324

- Format:

-

keyboard_arrow_up

Quick Navigation

Report Overview

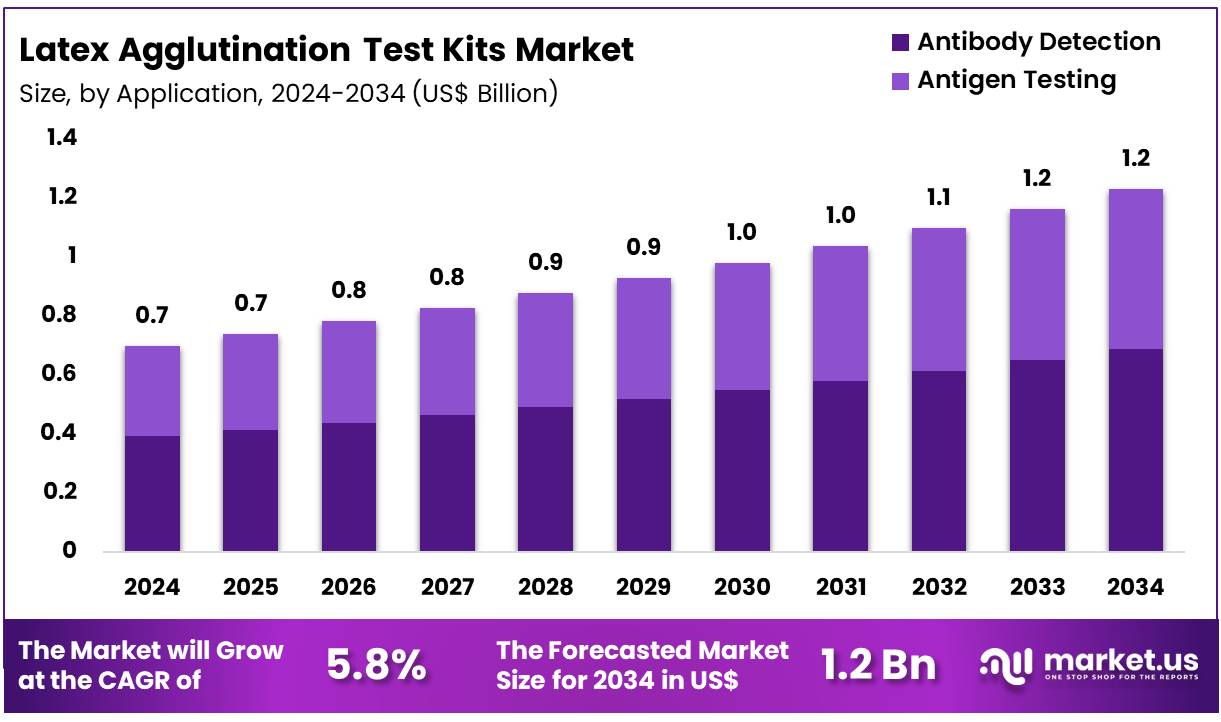

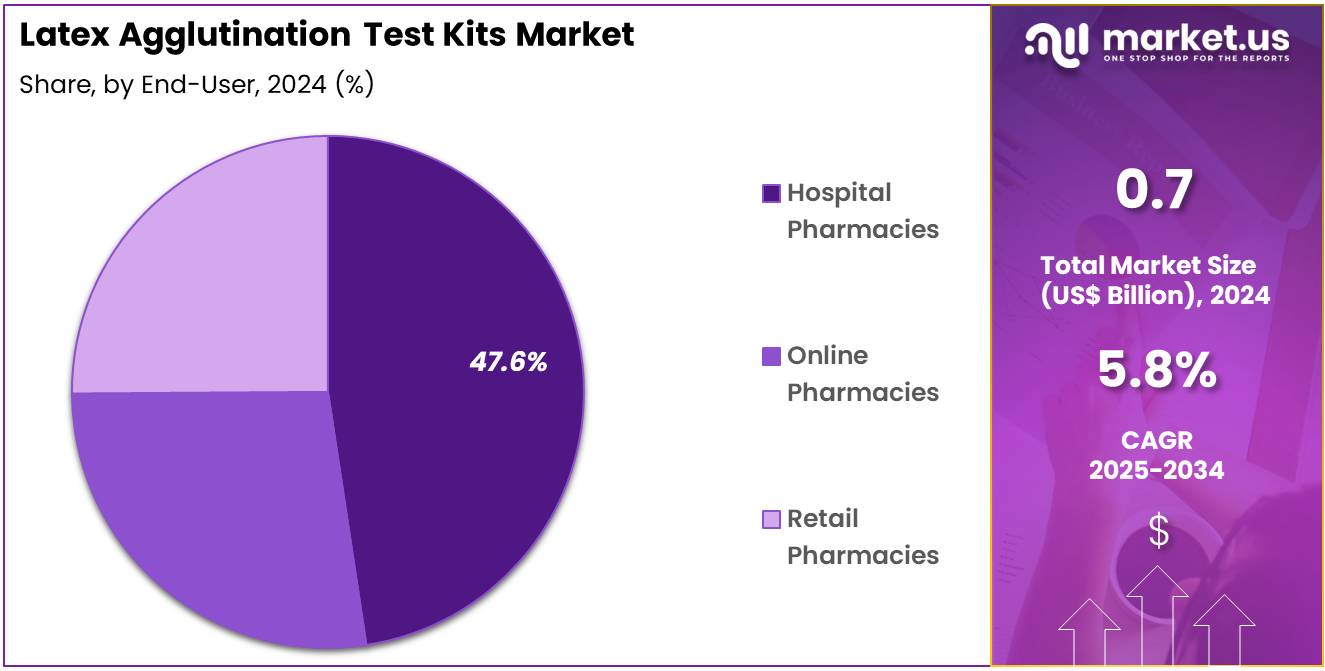

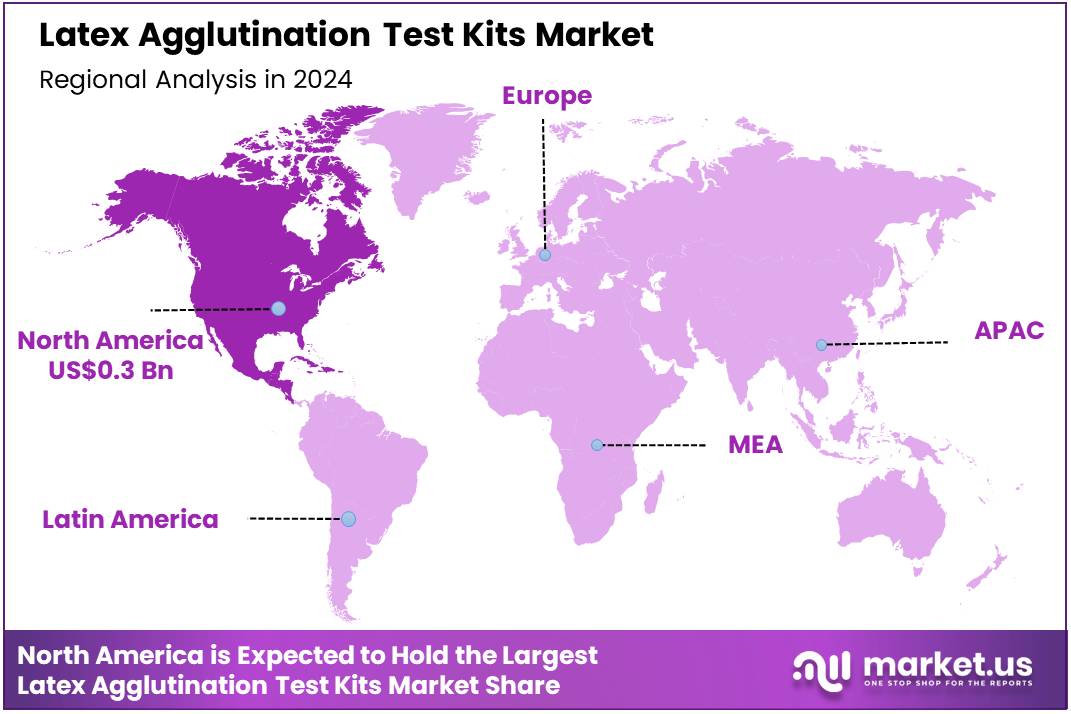

The Global Latex Agglutination Test Kits Market size is expected to be worth around US$ 1.2 Billion by 2034 from US$ 0.7 Billion in 2024, growing at a CAGR of 5.8% during the forecast period 2025 to 2034. In 2024, North America led the market, achieving over 42.4% share with a revenue of US$ 0.3 Billion.

The latex agglutination test kits market is experiencing strong growth, driven by a combination of diverse applications, the rising global incidence of infectious and autoimmune diseases, and the increasing adoption of rapid, decentralized diagnostic solutions. These kits offer a convenient and cost-effective method for diagnosing a wide range of conditions, making them a popular choice in both clinical and research settings. Furthermore, an increasing number of training programs on various laboratory tests, including latex agglutination, are boosting market expansion by enhancing technical expertise.

The rising global burden of infectious diseases is a primary catalyst for this market. The World Health Organization (WHO) reports that infectious diseases remain a leading cause of death worldwide, with an estimated 17.9 million deaths from cardiovascular diseases alone. While not a direct measure of infectious disease, this statistic highlights the massive global health burden that requires continuous and rapid diagnostic interventions.

The CDC’s 2024 annual report on infectious diseases in the US, for instance, documents a sharp increase in cases of meningococcal disease, which exceeded pre-pandemic levels. This surge in infectious disease cases directly correlates with a higher demand for diagnostic tools that can provide rapid and accurate results at the point of care.

Market growth is also being fueled by robust research and development initiatives and a heightened public health focus on disease prevention. The National Institutes of Health (NIH) is a major funder of infectious disease research, with its National Institute of Allergy and Infectious Diseases (NIAID) overseeing a budget of over US$ 6.6 billion to support research on the diagnosis, treatment, and prevention of infectious diseases. This investment is creating new opportunities for the development of advanced diagnostic tools.

The CDC’s continuous efforts to strengthen surveillance and laboratory capacity in high-risk countries like India also plays a significant role in this market. By focusing on diseases like influenza and tuberculosis, the CDC’s initiatives facilitate early detection and response to outbreaks, which in turn drives the demand for diagnostic tools like latex agglutination test kits.

Key Takeaways

- In 2024, the market for latex agglutination test kits generated a revenue of US$ 0.7 Billion, with a CAGR of 5.8%, and is expected to reach US$ 1.2 Billion by the year 2034.

- The product type segment is divided into ELISA, serum neutralization, indirect fluorescent, and hemagglutination inhibition, with ELISA taking the lead in 2023 with a market share of 38.7%.

- Considering technology, the market is divided into blood, cerebrospinal fluid, urine, and others. Among these, blood held a significant share of 41.5%.

- Furthermore, concerning the application segment, the market is segregated into antibody detection and antigen testing. The antibody detection sector stands out as the dominant player, holding the largest revenue share of 55.9% in the latex agglutination test kits market.

- The end-user segment is segregated into hospital pharmacies, online pharmacies, and retail pharmacies, with the hospital pharmacies segment leading the market, holding a revenue share of 47.6%.

- North America led the market by securing a market share of 42.4% in 2023.

Product Type Analysis

ELISA holds 38.7% of the product type segment in the latex agglutination test kits market. This segment’s growth is projected to continue due to its high sensitivity and specificity, making it critical for the accurate detection of infectious and autoimmune diseases. Hospitals, clinics, and diagnostic laboratories are anticipated to adopt ELISA kits for rapid, reliable testing. The rising prevalence of diseases such as hepatitis, HIV, and COVID-19 is likely to increase demand. Technological advancements, including automated and multiplex ELISA platforms, are expected to improve efficiency and throughput, supporting larger-scale testing.

Government and health organization programs aimed at strengthening diagnostic infrastructure are projected to further expand adoption, particularly in emerging markets. Additionally, point-of-care ELISA devices are anticipated to improve accessibility in remote areas. Research in immunology and oncology is likely to boost ELISA usage in both clinical and research settings. The versatility, reliability, and ability to provide quantitative results ensure ELISA remains a key driver of market growth.

Technology Analysis

Blood accounts for 41.5% of the technology segment in the latex agglutination test kits market. Its growth is anticipated as blood samples are fundamental for detecting infections, monitoring immune responses, and evaluating patient health. Hospitals and diagnostic labs are projected to favor blood testing due to the sample’s compatibility with multiple assays, including ELISA, which ensures accurate and reproducible results. Technological innovations like automated blood testing systems are likely to improve throughput and reduce human error, driving adoption.

Government initiatives promoting early detection of infectious diseases and regular health monitoring are projected to strengthen demand. Additionally, the rising prevalence of chronic and infectious diseases worldwide will likely increase the need for blood-based diagnostic tests. Emerging healthcare markets are expected to further contribute to segment growth. Blood remains a dominant sample type due to its reliability, wide applicability, and role in both clinical diagnostics and research.

Application Analysis

Antibody detection holds 55.9% of the application segment in the latex agglutination test kits market. The segment’s growth is projected due to increasing demand for disease surveillance, immunization monitoring, and diagnostic research. Hospitals, clinics, and laboratories are anticipated to expand antibody testing capacities to respond to rising infections and vaccination programs. Advances in immunoassays are likely to improve test speed, sensitivity, and specificity, further encouraging adoption.

Point-of-care antibody kits are expected to become increasingly popular in remote and resource-limited areas. Research applications, particularly in immunology, oncology, and vaccine development, are projected to boost demand. Additionally, government programs for public health monitoring and outbreak management are likely to support the segment. Antibody detection continues to be a critical tool in diagnostics, driving market growth through its essential role in both clinical and research settings.

End-User Analysis

Hospital pharmacies represent 47.6% of the end-user segment in the latex agglutination test kits market. This growth is projected as hospitals serve as primary centers for diagnostics, patient care, and outbreak management. Rapid, on-site testing for infections, autoimmune disorders, and other health conditions is anticipated to drive hospital adoption of latex agglutination kits. Ready-to-use ELISA and other kits are likely preferred for operational efficiency and consistent results.

Automated and high-throughput platforms are expected to optimize hospital workflows, improving patient outcomes. Government and institutional initiatives supporting hospital infrastructure and diagnostic expansion are projected to strengthen segment growth. As healthcare systems emphasize fast, accurate, and cost-effective diagnostics, hospital pharmacies are likely to maintain their dominant position. The combination of high patient volume, clinical complexity, and regulatory support makes hospital pharmacies a critical growth driver in the market.

Key Market Segments

By Product Type

- ELISA

- Serum Neutralization

- Indirect Fluorescent

- Hemagglutination Inhibition

By Technology

- Blood

- Cerebrospinal Fluid

- Urine

- Others

By Application

- Antibody Detection

- Antigen Testing

By End-user

- Hospital Pharmacies

- Online Pharmacies

- Retail Pharmacies

Drivers

The increasing global burden of infectious diseases is driving the market.

The market for latex agglutination test kits is experiencing significant growth driven by the rising global incidence of infectious diseases, which creates a sustained and urgent demand for rapid, on-site diagnostics. Many pathogens, including influenza, Streptococcus pneumoniae, and Neisseria meningitidis, can be quickly and effectively identified using these simple, cost-effective tests. According to the World Health Organization (WHO), seasonal influenza alone causes an estimated one billion cases annually, with 3-5 million of these being severe cases that require immediate medical attention.

The rapid diagnosis provided by these kits allows healthcare professionals to make timely treatment decisions, especially in resource-limited or point-of-care settings where access to central laboratories is impractical. Furthermore, a 2024 WHO report noted that meningitis, a severe infectious disease with a high mortality rate, continues to pose a major public health challenge, with the highest burden of bacterial meningitis occurring in the sub-Saharan African “meningitis belt.” This persistent threat drives ongoing investment and adoption of rapid diagnostic tools to enable quick, effective responses to outbreaks and sporadic cases, thereby ensuring the market’s robust growth.

Restraints

The low sensitivity and specificity of some test kits are restraining the market.

A significant restraint on the market is the inherent limitation in the sensitivity and specificity of some latex agglutination tests when compared to more advanced diagnostic technologies like polymerase chain reaction (PCR). While these tests offer speed and simplicity, their performance can sometimes lead to false-negative or false-positive results, which may delay proper treatment or lead to unnecessary medical interventions.

For instance, a 2023 study published in the journal Clinical Microbiology and Infection compared a rapid test with a molecular assay for bacterial meningitis and found that while the rapid test provided results within minutes, its sensitivity was lower, with some tests missing a significant percentage of cases. This can have serious implications, particularly for high-stakes diagnoses where accuracy is paramount. This concern over diagnostic performance has prompted many laboratories and healthcare providers to shift towards more sensitive molecular and immunoassay-based methods for confirmatory testing. The high-acuity healthcare environment prioritizes precision, and a perceived lack of reliability in agglutination tests, especially in complex clinical scenarios, consequently limits their broader adoption.

Opportunities

The rising demand for point-of-care diagnostics is creating growth opportunities.

The market is presented with significant opportunities due to the rising global demand for point-of-care (POC) diagnostics, which are tests performed near the patient rather than in a central laboratory. These test kits are perfectly suited for such decentralized healthcare settings as they require minimal training, no specialized equipment, and provide rapid results, enabling immediate clinical decisions.

A 2024 analysis of the POC diagnostics sector noted that the market was valued at an estimated US$ 47.8 billion in 2024, reflecting the strong shift toward decentralized testing. This movement away from traditional hospital laboratories is driven by the need for faster diagnosis in emergency rooms, physician offices, and community health clinics.

The American Medical Association’s 2024 Physician Practice Benchmark Survey highlighted the ongoing trend of physicians valuing on-site diagnostic capabilities for greater efficiency and patient convenience. The ease of use, cost-effectiveness, and rapid turnaround time of these test kits make them an ideal solution for a variety of diagnostic applications, thereby positioning them at the forefront of the point-of-care revolution and providing a significant avenue for market expansion.

Impact of Macroeconomic / Geopolitical Factors

The latex agglutination test kits market is facing a challenging operational environment influenced by ongoing macroeconomic and geopolitical factors. Persistent global inflation since 2022 has eroded purchasing power and driven up the cost of essential raw materials, such as latex microspheres and specialized antibodies. While the International Monetary Fund (IMF) projected a decline in global inflation to 5.9% in 2024, its continued presence in key regions has strained supply chains and increased manufacturing costs.

Geopolitical tensions have further complicated matters, causing disruptions in trade routes and export restrictions, resulting in significant price volatility for critical components. A 2024 World Bank report highlighted a more than 300% increase in shipping costs from Asia to Europe due to regional instability, directly impacting the cost of foreign-manufactured products. Despite these challenges, the market has shown resilience by adapting through strategic diversification of supply chains and investments in regional production hubs to mitigate risks and stabilize costs. This shift is positioning the industry to better absorb external shocks and ensure a stable supply to its global customers.

US tariff policies are significantly altering the import and manufacturing strategies within the diagnostic industry. The introduction of duties on a wide range of imported goods, including diagnostic reagents and equipment from key trading partners, has raised the final cost of these products for US hospitals and clinics. According to the American Hospital Association (AHA), tariffs on imported healthcare equipment and supplies were a major factor in increasing operational costs for hospitals in 2024.

Furthermore, these tariffs disrupt the global supply chains of multinational companies that rely on components sourced from various countries for a single product. For example, a 2024 US International Trade Commission report indicated that tariffs had increased the cost of lab supplies from certain regions by up to 25%. However, this environment is also driving domestic manufacturing. Many companies are speeding up plans to build or expand production facilities in the US to bypass these import duties. This shift strengthens the domestic manufacturing sector, ensures a more stable supply for the US market, and fosters innovation by localizing the production process.

Latest Trends

The trend toward digitalization and smart integration is a recent development.

A key trend in 2024 is the increasing digitalization of diagnostic results and the smart integration of traditionally analog test kits with modern digital platforms. While the core technology of these kits remains simple, manufacturers are now enhancing their utility by pairing them with smartphone applications, cloud-based data systems, and portable readers. This allows for automated reading of results, reducing human error and enabling real-time data capture and reporting to electronic health records.

A major diagnostics company, in its 2024 annual report, highlighted the release of a new rapid test with an integrated digital reader that connects to a secure cloud platform, allowing clinicians to manage patient results remotely. This trend extends beyond simple data capture; it facilitates epidemiological surveillance by anonymously aggregating test results, providing health authorities with a real-time overview of disease outbreaks.

For instance, the Centers for Disease Control and Prevention (CDC) has increasingly encouraged the use of digitally-enabled diagnostics to support its flu surveillance efforts. This move toward smart integration elevates the traditional test kit into a powerful tool for modern healthcare management and public health, creating new avenues for innovation.

Regional Analysis

North America is leading the Latex Agglutination Test Kits Market

The North American latex agglutination test kits market accounted for 42.4% of the global share in 2024, a result of multiple factors including the prevalence of infectious diseases, a well-established healthcare system, and the presence of key industry players. The US faces a significant number of infectious disease cases each year, driving a constant demand for fast, affordable diagnostic methods.

For example, during the 2023-2024 flu season, the Centers for Disease Control and Prevention (CDC) estimated 40 million flu-related illnesses, with 470,000 hospitalizations and 28,000 deaths. This high incidence rate emphasizes the need for quick and accurate diagnostic solutions to ensure timely treatments and effective management of public health, areas where latex agglutination test kits excel.

The market is further supported by a well-established network of diagnostic laboratories and hospitals. The availability of numerous CLIA-certified laboratories and the growing adoption of point-of-care diagnostics make latex agglutination test kits a preferred choice for their speed and ease of use. Additionally, the continuous innovation by leading companies, such as Thermo Fisher Scientific and Bio-Rad Laboratories, ensures the availability of new and improved products with enhanced sensitivity and specificity. These advancements, combined with a favorable regulatory environment and a strong focus on infectious disease surveillance, contribute to the sustained growth of the market in North America.

The Asia Pacific region is expected to experience the highest CAGR during the forecast period

The Asia Pacific latex agglutination test kits market is anticipated to experience robust growth during the forecast period. This is largely due to the region’s rapidly growing population, increasing prevalence of infectious diseases, and improving healthcare infrastructure. The World Health Organization (WHO) has consistently highlighted the significant burden of communicable diseases in the region, including tuberculosis, dengue, and malaria, which necessitates widespread and accessible diagnostic tools.

Countries like China and India are making substantial investments in healthcare, which is expected to support the establishment of new diagnostic laboratories and clinics. For example, India’s National Centre for Disease Control (NCDC) has been actively involved in strengthening disease surveillance and control programs, which will likely increase the demand for rapid diagnostic tests.

Furthermore, the rising awareness of early disease detection and the growing adoption of point-of-care testing in remote and resource-limited areas are driving the market. Governments across the region are focusing on improving public health by launching initiatives to combat infectious diseases. These initiatives often involve large-scale testing programs where the low cost and simplicity of latex agglutination test kits make them an ideal solution. The expanding presence of local and international manufacturers in the region, coupled with the rising demand for efficient diagnostic solutions, indicates that the Asia Pacific market is projected to play a pivotal role in the future growth of this industry.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia

- Netherland

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- New Zealand

- Singapore

- Thailand

- Vietnam

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Key Players Analysis

Key players in the rapid diagnostics industry employ a multi-faceted approach to expand their market footprint. They primarily focus on strategic mergers and acquisitions to consolidate their product portfolios and acquire innovative technologies. Companies also invest heavily in research and development, aiming to enhance test sensitivity and specificity while simultaneously developing automated platforms that minimize manual interpretation.

Furthermore, they pursue global expansion by establishing partnerships with local distributors and entering emerging markets, where a growing demand for cost-effective, rapid diagnostic tools exists. This combination of inorganic and organic growth strategies solidifies their competitive position.

Meridian Bioscience, a life science company, develops, manufactures, and distributes a wide range of diagnostic products and critical raw materials. The company provides both molecular and immunological reagents for diagnostic applications, supporting manufacturers with essential components for human, animal, plant, and environmental testing. Its core business focuses on developing solutions that deliver results with speed, accuracy, and simplicity. Meridian Bioscience builds relationships and provides solutions to hospitals, reference laboratories, research centers, and diagnostic manufacturers across more than 70 countries.

Top Key Players

- Thermo Fisher Scientific Inc

- HiMedia Laboratories Microbiology International

- Eurofins Abraxis

- Creative Diagnostics

- Cardinal Health

- Biotium

- Bio-Rad Laboratories, Inc

- bioMérieux S.A.

- Bioloegend Inc

- Atlas Medical GmbH

Recent Developments

- In March 2023, Cardinal Health partnered with Bendcare to co-develop innovative healthcare solutions in the field of rheumatology. This collaboration is expected to drive growth in the latex agglutination test kits market by enhancing product offerings and expanding access to advanced diagnostic solutions.

- In June 2022, Thermo Fisher Scientific formed a strategic partnership with Diagnostic BioSystem (DBS) to provide an extensive portfolio of primary antibodies across the US Through this collaboration, laboratories gain access to high-quality, innovative, and cost-effective products for routine histopathology staining, improving efficiency and reliability in diagnostic workflows.

- In April 2022, Bio-Rad Laboratories participated in the 32nd European Congress of Clinical Microbiology & Infectious Diseases (ECCMID). The company showcased its complete range of infectious disease testing systems, reagents, and quality control solutions, highlighting tools designed to optimize laboratory workflows and enhance the accuracy of clinical diagnostics.

Report Scope

Report Features Description Market Value (2024) US$ 0.7 Billion Forecast Revenue (2034) US$ 1.2 Billion CAGR (2025-2034) 5.8% Base Year for Estimation 2024 Historic Period 2020-2023 Forecast Period 2025-2034 Report Coverage Revenue Forecast, Market Dynamics, COVID-19 Impact, Competitive Landscape, Recent Developments Segments Covered By Product Type (ELISA, Serum Neutralization, Indirect Fluorescent, and Hemagglutination Inhibition) By Technology (Blood, Cerebrospinal Fluid, Urine, and Others) By Application (Antibody Detection and Antigen Testing) By End-User (Hospital Pharmacies, Online Pharmacies, and Retail Pharmacies) Regional Analysis North America-US, Canada, Mexico;Europe-Germany, UK, France, Italy, Russia, Spain, Rest of Europe;APAC-China, Japan, South Korea, India, Rest of Asia-Pacific;South America-Brazil, Argentina, Rest of South America;MEA-GCC, South Africa, Israel, Rest of MEA Competitive Landscape Thermo Fisher Scientific Inc, HiMedia Laboratories Microbiology International, Eurofins Abraxis, Creative Diagnostics, Cardinal Health, Biotium, Bio-Rad Laboratories, Inc, bioMérieux S.A., Bioloegend Inc, Atlas Medical GmbH. Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF)  Latex Agglutination Test Kits MarketPublished date: Aug 2025add_shopping_cartBuy Now get_appDownload Sample

Latex Agglutination Test Kits MarketPublished date: Aug 2025add_shopping_cartBuy Now get_appDownload Sample -

-

- Thermo Fisher Scientific Inc

- HiMedia Laboratories Microbiology International

- Eurofins Abraxis

- Creative Diagnostics

- Cardinal Health

- Biotium

- Bio-Rad Laboratories, Inc

- bioMérieux S.A.

- Bioloegend Inc

- Atlas Medical GmbH

Our Clients

- 156633

- Aug 2025