Global IVD Antibodies Market By Product Type (Cardiac Markers, Kidney Injury Markers, Tumor Markers and Infection & Inflammation Antibodies), By Application (Cancer, Immunology and Cardiovascular Diseases), By End User (Hospitals, Homecare Settings, Diagnostic Laboratories and Others), Region and Companies – Industry Segment Outlook, Market Assessment, Competition Scenario, Trends and Forecast 2026-2035

- Published date: Feb 2026

- Report ID: 179355

- Number of Pages: 305

- Format:

-

keyboard_arrow_up

Quick Navigation

Report Overview

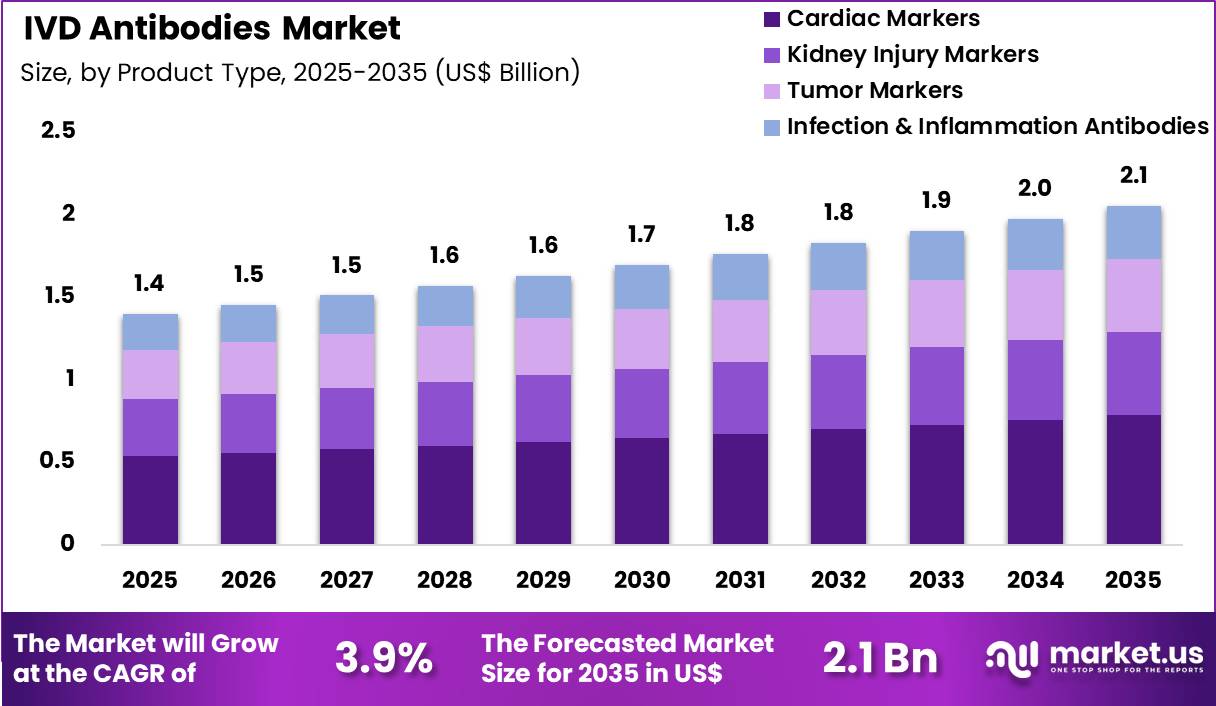

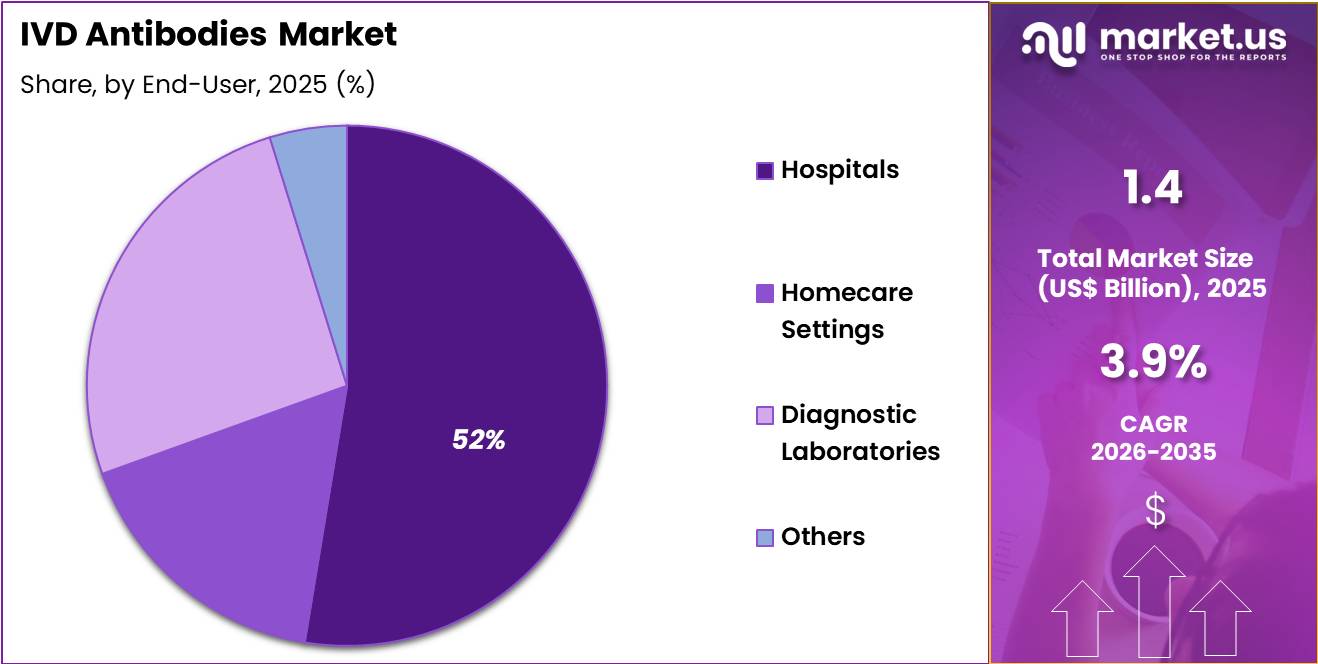

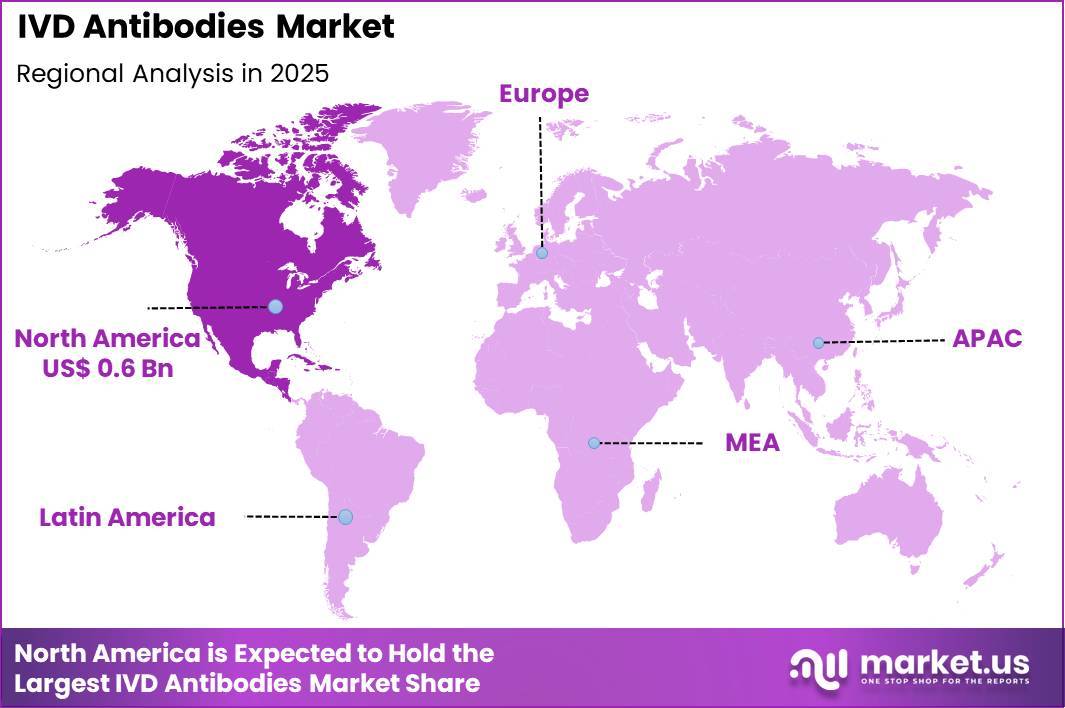

The Global IVD Antibodies Market size is expected to be worth around US$ 2.1 Billion by 2035 from US$ 1.4 Billion in 2025, growing at a CAGR of 3.9% during the forecast period 2026-2035. In 2025, North America led the market, achieving over 42.2% share with a revenue of US$ 0.6 Billion.

Increasing demand for accurate, rapid, and specific diagnostic assays propels the IVD antibodies market as laboratories and manufacturers require high-affinity reagents that enable reliable detection of biomarkers across diverse clinical applications.

Diagnostic companies increasingly incorporate monoclonal antibodies into immunoassays for infectious disease testing, where these reagents bind viral antigens or host antibodies to confirm HIV, hepatitis, or respiratory pathogen infections with high sensitivity.

These antibodies support tumor marker detection in oncology diagnostics, quantifying proteins such as PSA, CA-125, and CEA to monitor cancer progression and therapeutic response in prostate, ovarian, and colorectal malignancies. Clinical laboratories utilize IVD antibodies in cardiac biomarker assays, identifying troponin and BNP levels to diagnose acute myocardial infarction and heart failure episodes swiftly.

Autoimmune disorder testing relies on these antibodies to detect antinuclear antibodies and rheumatoid factor, aiding early identification of systemic lupus erythematosus and rheumatoid arthritis. Allergy diagnostics employ allergen-specific antibodies in IgE assays, facilitating precise identification of triggers for anaphylaxis and atopic conditions.

Manufacturers pursue opportunities to develop recombinant and engineered antibodies with improved stability and reduced cross-reactivity, expanding applications in multiplexed point-of-care platforms that simultaneously detect multiple pathogens or biomarkers.

Developers advance chimeric and humanized antibodies for next-generation assays, enhancing performance in low-abundance analyte detection for neurodegenerative disease markers like amyloid-beta and tau in Alzheimer’s diagnostics. These innovations facilitate integration with lateral flow and microfluidic devices, broadening utility in decentralized testing for chronic conditions.

Opportunities emerge in companion diagnostic antibodies that pair with targeted therapies, supporting personalized treatment decisions in oncology and infectious diseases. Companies invest in high-throughput screening and affinity maturation technologies to accelerate novel antibody discovery. Recent trends emphasize sustainable production methods and multi-specific formats, positioning IVD antibodies as critical components in precision diagnostics and value-based healthcare.

Key Takeaways

- In 2025, the market generated a revenue of US$ 1.4 Billion, with a CAGR of 3.9%, and is expected to reach US$ 2.1 Billion by the year 2035.

- The product type segment is divided into cardiac markers, kidney injury markers, tumor markers and infection & inflammation antibodies, with cardiac markers taking the lead with a market share of 38.2%.

- Considering application, the market is divided into cancer, immunology and cardiovascular diseases. Among these, cancer held a significant share of 41.8%.

- Furthermore, concerning the end user segment, the market is segregated into hospitals, homecare settings, diagnostic laboratories and others. The hospitals sector stands out as the dominant player, holding the largest revenue share of 52.6% in the market.

- North America led the market by securing a market share of 42.2%.

Product Type Analysis

Cardiac markers accounted for 38.2% of growth within product type and dominate the IVD antibodies market due to increasing prevalence of cardiovascular diseases globally. Rising incidences of myocardial infarction, heart failure, and related conditions drive demand for rapid and accurate diagnostic antibodies.

Clinicians rely on these markers for early detection, risk stratification, and patient management. Technological advancements enhance assay sensitivity and reduce turnaround time, improving clinical decision-making.

Hospitals and diagnostic centers adopt cardiac marker tests to streamline emergency and outpatient cardiac care. The segment growth is anticipated to continue as awareness of cardiovascular risk assessment expands and healthcare providers integrate point-of-care testing in clinical workflows.

Application Analysis

Cancer accounted for 41.8% of growth within application and is projected to lead due to increasing global cancer incidence and adoption of immunoassays for tumor detection. Early diagnosis and biomarker monitoring play a critical role in personalized treatment planning.

Rising investment in oncology research supports the development of novel antibody-based diagnostics. Hospitals and specialized diagnostic centers increasingly implement cancer-focused IVD antibody panels for screening and monitoring.

Segment growth is expected to strengthen as advancements in targeted therapies drive demand for accurate tumor marker identification. The increasing emphasis on preventive oncology and population screening enhances adoption across healthcare systems.

End-User Analysis

Hospitals contributed 52.6% of growth within end-user and lead the IVD antibodies market as primary sites for clinical diagnostics and patient management. Hospitals integrate comprehensive testing services across cardiology, oncology, and immunology departments.

The presence of skilled personnel, advanced laboratory infrastructure, and regulatory compliance enables high-volume testing. Rising hospital admissions for chronic and acute conditions drive consistent utilization of IVD antibody assays.

Segment growth is anticipated to continue as hospitals expand laboratory capacities, adopt automated immunoassay platforms, and implement rapid diagnostics to improve patient outcomes. Increasing collaborations with research institutes further enhance antibody testing capabilities.

Key Market Segments

By Product Type

- Cardiac Markers

- Kidney Injury Markers

- Tumor Markers

- Infection & Inflammation Antibodies

By Application

- Cancer

- Immunology

- Cardiovascular Diseases

By End User

- Hospitals

- Homecare Settings

- Diagnostic Laboratories

- Others

Drivers

Rising demand for early and accurate disease diagnosis is driving the market.

The growing emphasis on timely detection of infectious and chronic diseases has substantially increased the utilization of IVD antibodies in immunoassay-based testing platforms. Diagnostic laboratories are expanding their test menus to include antibody-based assays for a wider range of pathogens and biomarkers.

Healthcare systems are prioritizing rapid diagnostic solutions to improve patient management and reduce hospital stays. The correlation between disease prevalence and the need for specific antibody reagents drives consistent procurement by reference labs.

Government screening programs for infectious diseases rely heavily on validated IVD antibodies for reliable results. IVD antibodies enable high sensitivity and specificity in ELISA and lateral flow formats. National diagnostic guidelines recommend antibody-based tests for confirmatory testing in clinical workflows. Key suppliers are scaling production of monoclonal and polyclonal antibodies to meet laboratory requirements. This driver encourages continuous improvement in antibody affinity and stability.

Restraints

Stringent regulatory approval processes are restraining the market.

The complex and time-consuming regulatory pathways for IVD antibodies require extensive analytical and clinical validation data before market entry. Manufacturers must comply with evolving quality standards from health authorities, increasing development timelines and costs. Smaller biotechnology firms often lack the resources to navigate these requirements effectively.

The correlation between regulatory scrutiny and delayed product launches constrains market innovation. Government agencies enforce rigorous post-market surveillance for antibody performance. IVD antibodies intended for high-risk applications face additional clinical evidence demands.

National regulatory frameworks vary by region, complicating global commercialization strategies. Key players allocate significant resources to compliance teams and documentation. This restraint limits the pace at which new antibody reagents reach diagnostic laboratories. Stringent regulatory requirements for IVD antibodies remain a major market restraint.

Opportunities

Expansion of diagnostic testing in emerging economies is creating growth opportunities.

The rapid development of laboratory infrastructure in Asia-Pacific and Latin America offers significant potential for IVD antibodies in routine and specialized testing. Governmental investments in public health laboratories support the introduction of antibody-based assays for infectious disease surveillance.

Increasing private sector participation in diagnostics amplifies demand for high-quality reagents. Partnerships with local distributors enable efficient supply and technical support in these regions. The large population base in emerging markets magnifies prospects for volume-driven growth.

Educational initiatives for laboratory technicians promote standardized use of IVD antibodies. This opportunity allows established suppliers to establish regional manufacturing or distribution hubs. Key companies are tailoring antibody portfolios to address prevalent local diseases.

Overall, emerging economy expansion aligns with global efforts to strengthen diagnostic capacity. Expansion of diagnostic testing in emerging economies is a key growth opportunity.

Impact of Macroeconomic / Geopolitical Factors

Macroeconomic conditions affect the IVD antibodies market by shaping laboratory budgets, research funding, and hospital procurement strategies. Rising inflation increases costs for reagents, high-purity antibodies, and consumables, which raises prices for diagnostic tests and slows purchase cycles. Higher interest rates reduce investment in new laboratory equipment and expansion of diagnostic services.

Geopolitical tensions disrupt global supply chains for critical antibodies and assay components, causing delays and increased shipping costs. Current US tariffs on imported raw materials and laboratory instruments elevate operational expenses for manufacturers and diagnostic labs. These pressures can limit small lab expansions and slow adoption of advanced testing platforms.

At the same time, companies focus on domestic sourcing and process optimization to maintain efficiency. Growing demand for personalized medicine and early disease detection continues to drive long-term market growth.

Latest Trends

Launch of recombinant monoclonal IVD antibodies is a recent trend in the market.

In 2024, several manufacturers introduced recombinant monoclonal antibodies for IVD applications to improve lot-to-lot consistency and reduce animal-derived variability. These antibodies are engineered for enhanced specificity in immunoassay formats used for cancer and infectious disease testing. Suppliers have prioritized scalability in production to meet growing laboratory demand.

Clinical validation studies in 2024 confirmed superior performance in automated platforms. The launch of recombinant monoclonal IVD antibodies represents a major trend toward improved reagent quality and supply reliability. This development addresses longstanding challenges with polyclonal antibody variability.

The trend focuses on integration with high-throughput analyzers for efficient workflow. Regulatory pathways have adapted to facilitate faster approval of recombinant products. Industry collaborations optimize expression systems for higher yields. These advancements aim to elevate diagnostic accuracy while ensuring sustainable supply in the IVD sector.

Regional Analysis

North America is leading the IVD Antibodies Market

North America demonstrated strong growth in 2024 in the IVD antibodies market, driven by extensive adoption of advanced diagnostic technologies and high clinical demand. The region accounted for 42.2 % of the global market, reflecting its leading position in antibody‑based testing. Hospitals and laboratories increasingly implemented immunoassays and molecular diagnostics, improving both speed and accuracy of disease detection.

Major diagnostic firms invested heavily in reagent innovation, enhancing assay sensitivity and specificity for oncology and autoimmune applications. Government health programs promoting widespread screening for infectious diseases further stimulated test volumes. Reimbursement frameworks incentivised providers to integrate high-performance antibody assays into standard care pathways.

Collaborative research between academic institutions and industry accelerated clinical validation of novel antibody targets, increasing product availability. The United States performed over 685 million antibody‑based tests in 2023, underlining the scale of regional utilisation.

The Asia Pacific region is expected to experience the highest CAGR during the forecast period

Asia Pacific is expected to experience robust growth during the forecast period, supported by expanding healthcare infrastructure and rising demand for reliable diagnostics. Rapid urbanisation and increasing prevalence of chronic and infectious diseases in countries such as China and India have led hospitals and laboratories to prioritise accurate serological and immunodiagnostic testing.

National health initiatives are incorporating antibody‑based diagnostics into preventive screening programs to enhance early detection rates. Expanding laboratory networks and new diagnostic facilities in underserved regions improve access to quality testing services.

Local production of critical reagents reduces reliance on imports and lowers costs for healthcare providers. Partnerships between global diagnostic firms and regional distributors promote technology transfer and product adaptation for local clinical needs.

Clinician awareness about the utility of targeted diagnostics is strengthening, encouraging routine use of advanced assays. China conducted over 1 billion antibody‑related diagnostic tests in 2024, highlighting significant adoption across the region.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia

- Netherland

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- New Zealand

- Singapore

- Thailand

- Vietnam

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Key Players Analysis

Key competitors in the IVD antibodies market expand growth by broadening assay coverage with highly specific, well‑validated antibody reagents that address a wider range of clinical biomarkers and diagnostic panels. They also strengthen their market presence by investing in quality control systems and validation services that support reproducibility and compliance with stringent regulatory and laboratory accreditation standards.

Companies pursue co‑development agreements with diagnostic kit manufacturers and instrument OEMs to ensure reagent compatibility with automated analyzers and streamline lab integration. They reinforce commercial traction by launching training programs, application support resources, and data‑driven marketing that help laboratories optimize test performance and improve clinician confidence.

Abcam plc operates as a global life sciences company focused on research and diagnostic antibodies, offering an extensive portfolio of primary and secondary reagents supported by technical documentation and global distribution networks that serve clinical and research laboratories.

The company advances its competitive position through disciplined investment in product innovation, strategic partnerships that extend its application reach, and a customer‑centric commercialization approach that aligns reagent quality with evolving diagnostic needs.

Top Key Players

- Thermo Fisher Scientific

- Abcam

- Bio-Rad Laboratories

- Agilent Technologies

- Merck KGaA

- Sigma-Aldrich

- Cell Signaling Technology

- BD Biosciences

- R&D Systems

- PerkinElmer

Recent Developments

- Abbott Laboratories reported significant growth in its core diagnostics segment, with total diagnostics sales reaching US$8.9 billion in 2025. This performance was driven by the continued rollout of high-throughput immunoassay and molecular platforms that utilize specialized antibodies for precision testing.

- Thermo Fisher Scientific saw its Specialty Diagnostics revenue reach US$4.676 billion in 2025. The company continues to expand its portfolio of monoclonal and polyclonal antibodies used in clinical settings, focusing on integrated diagnostic workflows for chronic and infectious diseases.

Report Scope

Report Features Description Market Value (2025) US$ 1.4 Billion Forecast Revenue (2035) US$ 2.1 Billion CAGR (2026-2035) 3.9% Base Year for Estimation 2025 Historic Period 2020-2024 Forecast Period 2026-2035 Report Coverage Revenue Forecast, Market Dynamics, COVID-19 Impact, Competitive Landscape, Recent Developments Segments Covered By Product Type (Cardiac Markers, Kidney Injury Markers, Tumor Markers and Infection & Inflammation Antibodies), By Application (Cancer, Immunology and Cardiovascular Diseases), By End User (Hospitals, Homecare Settings, Diagnostic Laboratories and Others) Regional Analysis North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, New Zealand, Singapore, Thailand, Vietnam, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA Competitive Landscape Thermo Fisher Scientific, Abcam, Bio-Rad Laboratories, Agilent Technologies, Merck KGaA, Sigma-Aldrich, Cell Signaling Technology, BD Biosciences, R&D Systems, PerkinElmer Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF)

-

-

- Thermo Fisher Scientific

- Abcam

- Bio-Rad Laboratories

- Agilent Technologies

- Merck KGaA

- Sigma-Aldrich

- Cell Signaling Technology

- BD Biosciences

- R&D Systems

- PerkinElmer

Our Clients

- 179355

- Feb 2026