Quick Navigation

Report Overview

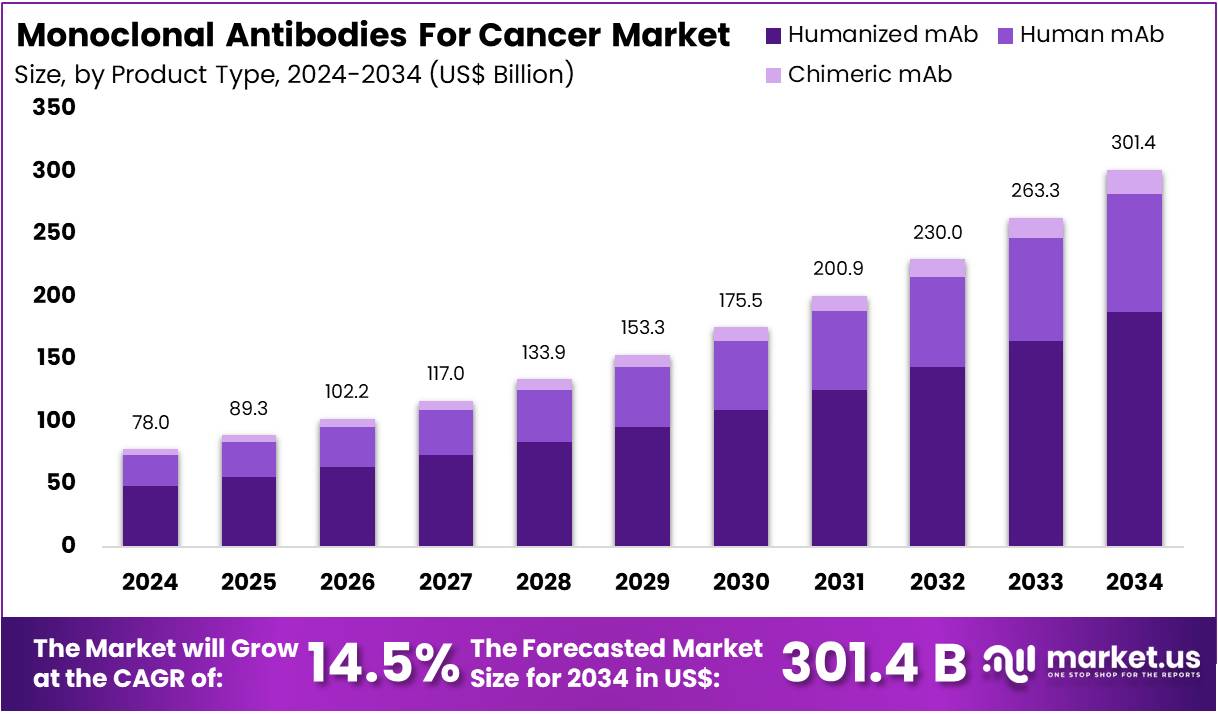

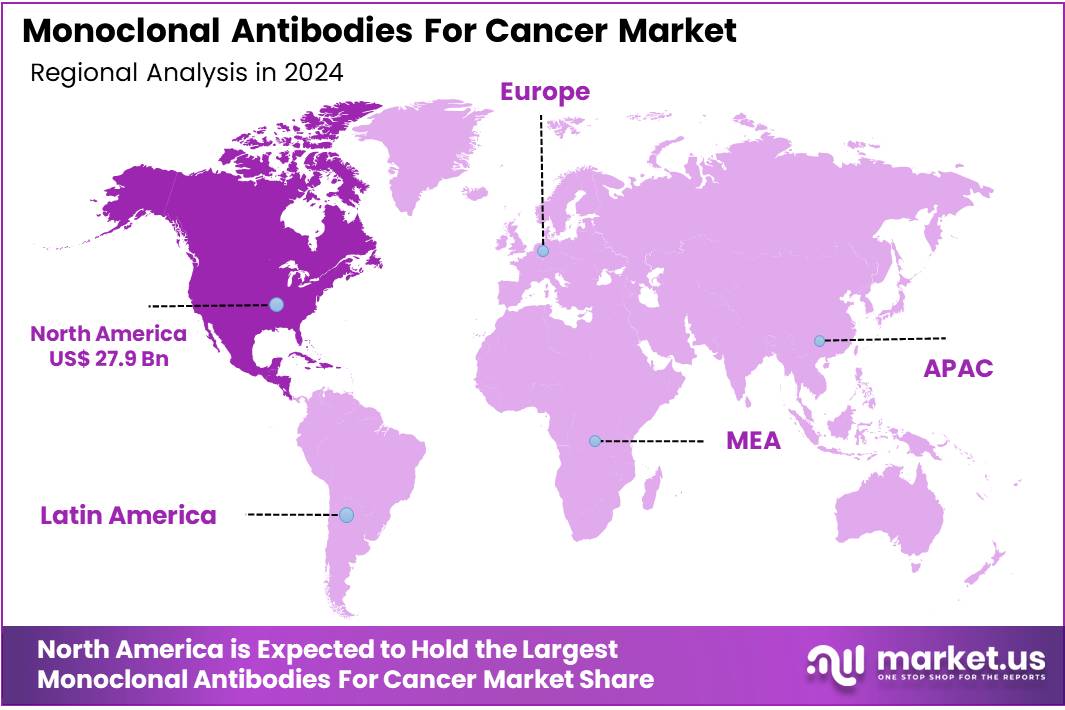

The Global Monoclonal Antibodies for Cancer Market size is expected to be worth around US$ 301.4 Billion by 2034, from US$ 78 Billion in 2024, growing at a CAGR of 14.5% during the forecast period from 2025 to 2034. North America dominated the market, securing a 35.7% share. The market value for the region reached US$ 27.9 billion that year.

The global monoclonal antibodies (mAbs) for cancer market is experiencing rapid growth, driven by rising cancer prevalence, advancements in biotechnology, and increasing adoption of immunotherapy. Monoclonal antibodies are engineered proteins designed to specifically target cancer cells, offering high efficacy with fewer side effects compared to traditional treatments.

- The GLOBOCAN indicates that in 2022, there were 9.7 million cancer-related deaths, compared to 9.96 million in 2020, along with 20 million new cancer cases, up from 19.6 million in 2020.

The introduction of novel mAbs, regulatory approvals, and the rising demand for targeted therapies further support market expansion. Key segments include fully human, humanized, chimeric, and murine monoclonal antibodies, categorized by their mechanism of action, such as immune checkpoint inhibitors (PD-1, PD-L1 inhibitors), antibody-drug conjugates (ADCs), and naked monoclonal antibodies. These therapies are widely used in the treatment of lung, breast, colorectal, leukemia, lymphoma, and other cancers.

Geographically, North America dominates the market due to strong R&D investments, a high incidence of cancer, and favorable reimbursement policies. Europe follows closely, benefiting from government funding and innovation in biosimilars, while Asia-Pacific is the fastest-growing region due to improving healthcare infrastructure and increasing demand for novel therapies.

Leading pharmaceutical players such as Roche, Bristol-Myers Squibb, Merck, Amgen, AbbVie, and AstraZeneca are investing in next-generation monoclonal antibodies, bispecific antibodies, and combination therapies to enhance treatment outcomes. Despite the market’s strong growth prospects, high costs, stringent regulatory approvals, and biosimilar competition pose challenges. However, opportunities lie in breakthroughs such as AI-driven drug discovery, next-generation antibody development, and expansion in emerging markets, which are expected to drive continued innovation and market expansion in the coming years.

Key Takeaways

- The Monoclonal Antibodies for Cancer market generated a revenue of US$ 78.0 Billion and is predicted to reach US$ 301.4 Billion, with a CAGR of 14.5%.

- Based on the Product Type, the Pembrolizumab products segment generated the most revenue for the market with a market share of 38.2%.

- Based on the Cancer Type, the Breast Cancer segment generated the most revenue for the market with a market share of 24.2%.

- Based on the Source, the Humanized mAb segment generated the most revenue for the market with a market share of 62.4%.

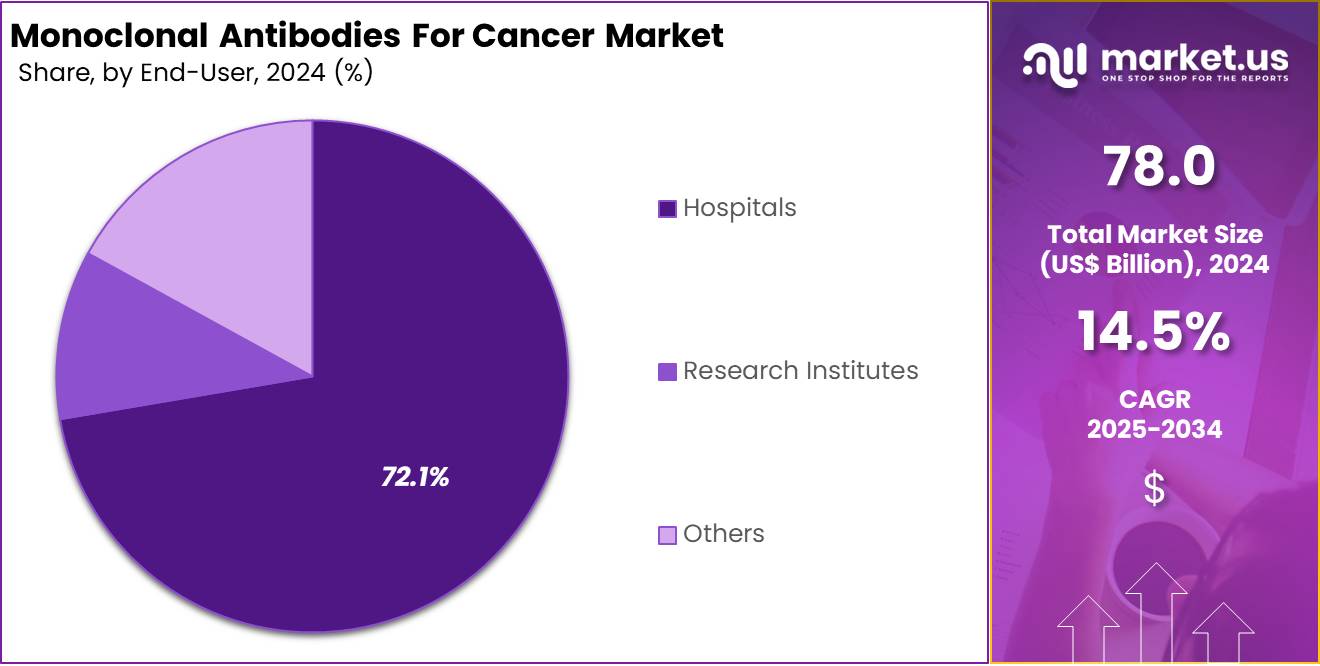

- Based on the End-User, the Hospitals segment generated the most revenue for the market with a market share of 72.1%.

- Based on the Region, the North America generated the most revenue for the market with a market share of 35.7%.

Product Type Analysis

The market is segmented by product type into Bevacizumab, Cetuximab, Ipilimumab, Nivolumab, Pembrolizumab, Pertuzumab, Rituximab, Trastuzumab, and Trastuzumab Emtansine. Pembrolizumab held the largest market share in the product type segment due to its widespread adoption in oncology treatments.

As a PD-1 checkpoint inhibitor, Pembrolizumab is extensively used for multiple cancer types, including non-small cell lung cancer (NSCLC), melanoma, and head and neck squamous cell carcinoma. Its broad FDA approvals and strong clinical efficacy have positioned it as a leading immunotherapy drug.

The growing preference for immuno-oncology therapies, coupled with increasing cancer prevalence, has fueled its market dominance. In 2023, Pembrolizumab generated over $25 billion in global sales, reflecting its strong demand. Additionally, ongoing clinical trials exploring expanded indications are expected to further strengthen its market position.

The drug’s competitive advantage over conventional chemotherapies, along with favorable reimbursement policies and strategic collaborations by Merck & Co., has driven its sustained market growth. As research advances, Pembrolizumab is likely to maintain its leadership in the product type segment.

Cancer Type

Breast cancer held the largest market share in the cancer type segment due to its high global prevalence and increasing adoption of targeted therapies. According to the World Health Organization (WHO), breast cancer tops the list as the most frequently diagnosed cancer worldwide. In 2023 alone, there were over 2.3 million new cases reported. This increasing incidence, along with continuous improvements in treatment methodologies, has substantially propelled market growth.

Targeted therapies, including Trastuzumab, Pertuzumab, and Trastuzumab Emtansine, have revolutionized treatment, particularly for HER2-positive cases. Immunotherapies like Pembrolizumab and hormonal therapies further contribute to market expansion. Additionally, early detection programs and improved screening methods have increased diagnosis rates, boosting demand for effective treatments.

Pharmaceutical companies continue investing in clinical trials and combination therapies, further enhancing treatment efficacy. Favorable reimbursement policies and government initiatives promoting breast cancer awareness and research have also supported market dominance. With ongoing innovations, breast cancer is expected to maintain its leading position in the cancer type segment.

Source Analysis

Monoclonal antibodies for cancer are sourced from Humanized mAb, Human mAb, and Chimeric mAb.In 2024, Humanized mAb held the dominant market share of 62.4%, driven by their superior efficacy, reduced immunogenicity, and expanding therapeutic applications in cancer treatment. Humanized monoclonal antibodies (mAbs) are genetically engineered to closely resemble human antibodies, minimizing immune system rejection while enhancing targeting precision.

Leading therapies such as Trastuzumab, Pembrolizumab, and Bevacizumab have significantly contributed to market dominance, especially in treating breast cancer, lung cancer, and colorectal cancer. The growing adoption of immune checkpoint inhibitors and targeted biologics has further propelled demand.

Favorable regulatory approvals, ongoing clinical trials for new indications, and pharmaceutical investments in R&D continue to expand the market. Additionally, advancements in antibody-drug conjugates (ADCs) using humanized mAbs have enhanced their therapeutic potential. With rising cancer prevalence and increasing acceptance of precision medicine, the Humanized mAb segment is expected to sustain its leadership in the monoclonal antibody market for cancer treatment.

End-User Analysis

In 2024, hospitals held a dominant 72.1% market share in the end-user segment, driven by the increasing demand for advanced cancer treatments, specialized care facilities, and rising hospital admissions for oncology therapies. Hospitals serve as primary centers for monoclonal antibody (mAb) administration, including immune checkpoint inhibitors, targeted therapies, and antibody-drug conjugates (ADCs), making them the preferred choice for patients requiring comprehensive treatment.

The availability of state-of-the-art infrastructure, skilled oncologists, and advanced diagnostic capabilities has further strengthened hospitals’ market position. Additionally, government funding, insurance coverage, and reimbursement policies support the high adoption of costly biologics and immunotherapies in hospital settings.

With the increasing prevalence of cancer, hospitals continue expanding their oncology departments, integrating precision medicine, and adopting personalized treatment approaches. As a result, the hospital segment is expected to maintain its leading position, supported by technological advancements and a growing focus on multidisciplinary cancer care.

Key Market Segments

By Product Type

- Bevacizumab

- Cetumaximab

- Ipilimumab

- Nivolumab

- Pembrolizumab

- Pertuzumab

- Rituximab

- Trastuzumab

- Trastuzumab Emtansine

By Cancer Type

- Breast Cancer

- Colorectal Cancer

- Lung Cancer

- Ovarian Cancer

- Blood Cancer

- Melanoma

- Liver Cancer

- Others

By Source

- Humanized mAb

- Human mAb

- Chimeric mAb

By End-User

- Hospitals

- Research Institutes

- Others

Drivers

Rising Cancer Prevalence

The rising global prevalence of cancer is a significant driver for the monoclonal antibodies (mAb) market, as the increasing number of cases fuels demand for targeted therapies. According to the World Health Organization (WHO), cancer was the second leading cause of death globally in 2023, with around 10 million fatalities.

Additionally, projections from the Global Cancer Observatory (GLOBOCAN) indicate that by 2040, annual new cancer cases are expected to increase to 30 million. This data underscores the ongoing challenge and growing burden of cancer worldwide.

Monoclonal antibodies such as Pembrolizumab, Nivolumab, Trastuzumab, and Rituximab are increasingly used due to their precision in targeting cancer cells while minimizing damage to healthy tissues. Lung, breast, and colorectal cancers account for the highest usage of mAb therapies.

With the growing elderly population and increasing exposure to risk factors such as smoking, pollution, and lifestyle changes, the need for effective, personalized cancer treatments is surging, positioning monoclonal antibodies as a key therapeutic approach.

Restrains

High Treatment Costs

The high cost of monoclonal antibody (mAb) therapies is a major barrier to accessibility, limiting their adoption despite their effectiveness in cancer treatment. Monoclonal antibodies are expensive due to complex biomanufacturing processes, extensive R&D investments, and lengthy clinical trials. The average cost of mAb therapy ranges from $50,000 to $150,000 per patient annually, making it unaffordable for many, especially in low- and middle-income countries.

For instance, Pembrolizumab (Keytruda) costs around $150,000 per year, while Trastuzumab (Herceptin) for breast cancer treatment can exceed $70,000 annually. Additionally, the U.S. healthcare system spent over $100 billion on oncology drugs in 2023, with mAbs accounting for a significant share.

Although biosimilars offer cost-effective alternatives, their market penetration remains slow due to regulatory hurdles and patent protections. High pricing continues to challenge universal access, emphasizing the need for cost-control policies, insurance coverage expansion, and biosimilar adoption to enhance affordability.

Opportunities

Expansion of Biosimilars

The expansion of biosimilar monoclonal antibodies (mAbs) is transforming cancer treatment by providing cost-effective alternatives to expensive biologics. Biosimilars are nearly identical to original monoclonal antibodies, offering comparable efficacy, safety, and quality at a significantly reduced price.

Notably, biosimilars of leading mAbs like Trastuzumab (Herceptin), Bevacizumab (Avastin), and Rituximab (Rituxan) have reduced treatment costs by 30% to 50%, making cancer therapies more accessible. In Europe, where biosimilars have been widely adopted, healthcare systems have saved over $15 billion in recent years. Similarly, in the United States, biosimilar uptake has increased, with projected savings of $100 billion by 2025 across multiple disease areas, including oncology.

Governments and regulatory agencies, such as the FDA, EMA, and WHO, are actively supporting biosimilar adoption through streamlined approval pathways and policy incentives. Emerging markets, particularly in Asia-Pacific and Latin America, are also experiencing rapid growth in biosimilar availability, further increasing competition and enhancing patient access. As biosimilars continue to expand, they are expected to drive market affordability, healthcare savings, and broader treatment accessibility.

Impact of Macroeconomic / Geopolitical Factors

Macroeconomic and geopolitical factors significantly impact the Global Monoclonal Antibodies (mAbs) for Cancer Market, influencing drug pricing, supply chains, and healthcare accessibility. Rising inflation and economic slowdowns have increased production costs for biopharmaceutical companies, making mAb therapies more expensive and straining healthcare budgets, especially in developing nations.

Geopolitical tensions, such as the Russia-Ukraine conflict and U.S.-China trade restrictions, have disrupted the global supply chain for biologics, raw materials, and active pharmaceutical ingredients (APIs). These disruptions delay drug manufacturing and distribution, leading to shortages and price fluctuations.

Additionally, government policies and healthcare spending play a crucial role in market dynamics. Nations with strong regulatory frameworks and public healthcare investments, like the U.S. and Europe, drive market growth, while regions with weaker economies struggle with mAb affordability. Despite challenges, increased biotech investments, biosimilar adoption, and international collaborations are mitigating risks, ensuring the continued expansion of monoclonal antibody-based cancer therapies worldwide.

Latest Trends

The Global Monoclonal Antibodies (mAbs) for Cancer Market is witnessing transformative trends driven by technological advancements and evolving treatment approaches. One key trend is the increasing use of combination therapies, where monoclonal antibodies are integrated with chemotherapy, targeted therapies, or immune checkpoint inhibitors to enhance treatment efficacy. For example, Pembrolizumab (Keytruda) and Nivolumab (Opdivo) are commonly used alongside chemotherapy for lung and melanoma cancers, improving patient outcomes and survival rates.

Another major trend is the integration of AI and Big Data in oncology, accelerating mAb drug discovery and clinical research. AI-driven analytics help identify novel cancer biomarkers, optimize clinical trial designs, and predict patient responses, thereby reducing R&D costs and drug development timelines. Companies like Bristol-Myers Squibb and Roche are leveraging AI to enhance precision medicine strategies.

Furthermore, hospitals and specialty clinics continue to dominate as primary end-users of monoclonal antibodies, accounting for the largest market share. Their advanced infrastructure, availability of skilled oncologists, and access to cutting-edge biologic therapies make them preferred treatment centers.

Governments and healthcare systems are also expanding oncology departments and increasing insurance coverage, further driving hospital-based mAb adoption. These trends collectively shape the future of the monoclonal antibody market, fostering innovation and improving cancer care worldwide.

Regional Analysis

North America Leads the Global Monoclonal Antibodies for Cancer Market

In 2024, North America held a dominant market position, capturing more than a 35.7% share and holds US$ 27.9 Billion market value for the year. North America leads the Global Monoclonal Antibodies (mAbs) for Cancer Market, driven by strong healthcare infrastructure, high cancer prevalence, and advanced biopharmaceutical research.

The region accounts for the largest market share, with the U.S. dominating due to high adoption rates of targeted therapies, extensive R&D investments, and government initiatives supporting biologics development. According to the American Cancer Society, the U.S. recorded approximately 2 million new cancer cases in 2023, increasing the demand for monoclonal antibody-based immunotherapies like Pembrolizumab (Keytruda) and Nivolumab (Opdivo).

The North American biopharmaceutical industry is a global leader, with companies like Bristol-Myers Squibb, Roche, and Amgen pioneering innovative mAb treatments. The U.S. FDA approved over 20 monoclonal antibodies for oncology applications in the past five years, reflecting the region’s focus on precision medicine and personalized cancer treatments.

Additionally, favorable reimbursement policies and widespread insurance coverage make these therapies more accessible to patients. Government initiatives, such as the Cancer Moonshot program, further boost research funding and innovation in biologic therapies. With a well-established regulatory framework, robust clinical trial activity, and growing biosimilar penetration, North America is expected to maintain its leadership in the global monoclonal antibodies for cancer market, driving continued growth and innovation.

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia

- Netherland

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- New Zealand

- Singapore

- Thailand

- Vietnam

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Key Players Analysis

The Global Monoclonal Antibodies (mAbs) for Cancer Market is highly competitive, with key players driving innovation, market expansion, and strategic collaborations. North America holds the largest market share, followed by Europe and Asia-Pacific, due to strong R&D investments, regulatory approvals, and high cancer prevalence.

Leading companies include Roche, Bristol-Myers Squibb, Merck & Co., Amgen, and Eli Lilly, which dominate the market with blockbuster mAbs like Trastuzumab (Herceptin), Pembrolizumab (Keytruda), and Nivolumab (Opdivo). Roche leads with a strong oncology pipeline, while Merck’s Keytruda alone generated over $24 billion in revenue in 2023.

The market is also witnessing biosimilar competition, with companies like Celltrion, Biocon, and Pfizer launching cost-effective alternatives to branded mAbs. Additionally, partnerships and acquisitions, such as Bristol-Myers Squibb’s acquisition of Celgene, are reshaping the competitive landscape. With ongoing clinical trials and expanding applications, the market is projected to grow steadily, fueled by advancements in targeted therapies and increasing global cancer cases.

Top Key Players in the Monoclonal Antibodies for Cancer Market

- Hoffmann-La Roche Ltd.

- Bristol-Myers Squibb Company

- Merck & Co.

- GSK plc.

- Johnson & Johnson

- Novartis AG

- AstraZeneca plc

- Eli Lilly and Company

- AbbVie Inc.

- Amgen, Inc.

Recent Developments

- In March 2022: Sanofi teamed up with Seagen Inc. in an exclusive collaboration. They aim to design, develop, and market antibody-drug conjugates (ADCs). These ADCs target up to three different cancer types, expanding treatment options and potentially enhancing patient outcomes in oncology.

- In July 2022: The FDA accepted the resubmission of Toripalimab, a monoclonal antibody developed by Junshi Biosciences and Coherus, for treating nasopharyngeal cancer. This anti-PD-1 therapy works by preventing PD-1 from binding to its ligands, thereby strengthening the immune system’s response against cancer cells.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2024) | US$ 78.0 Billion |

| Forecast Revenue (2034) | US$ 301.4 Billion |

| CAGR (2025-2034) | 14.5% |

| Base Year for Estimation | 2024 |

| Historic Period | 2020-2023 |

| Forecast Period | 2025-2034 |

| Report Coverage | Revenue Forecast, Market Dynamics, COVID-19 Impact, Competitive Landscape, Recent Developments |

| Segments Covered | Product Type- Bevacizumab, Cetumaximab, Ipilimumab, Nivolumab, Pembrolizumab, Pertuzumab, Rituximab, Trastuzumab Trastuzumab and Emtansine, Cancer Type-Breast Cancer, Colorectal Cancer, Lung Cancer, Ovarian Cancer, Blood Cancer, Melanoma, Liver Cancer and Others, Source- Humanized mAb, Human mAb and Chimeric mAb, End-User- Hospitals, Research Institutes and Others. |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, New Zealand, Singapore, Thailand, Vietnam, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA |

| Competitive Landscape | F. Hoffmann-La Roche Ltd., Bristol-Myers Squibb Company , Merck & Co., GSK plc. , Johnson & Johnson, Novartis AG, AstraZeneca plc, Eli Lilly and Company, AbbVie Inc. and Amgen, Inc. |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |