Quick Navigation

Report Overview

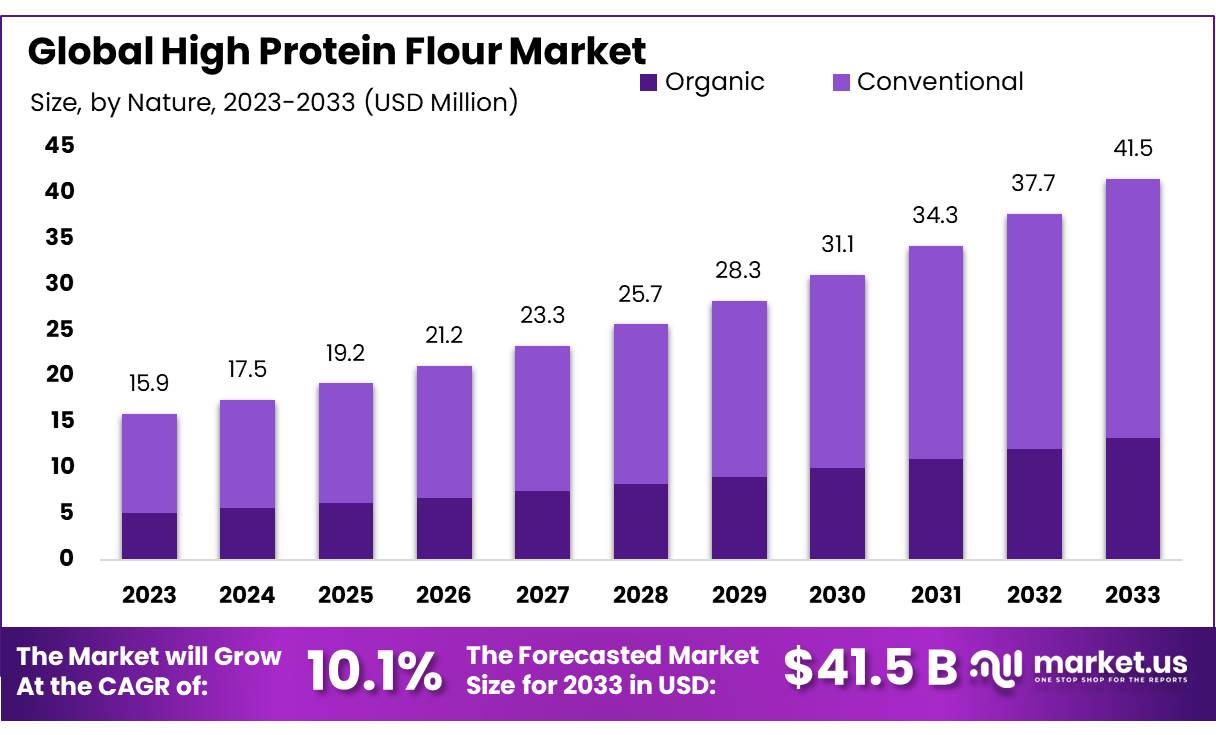

The Global High Protein Flour Market size is expected to be worth around USD 41.5 Bn by 2033, from USD 15.87 Bn in 2023, growing at a CAGR of 10.1% during the forecast period from 2024 to 2033.

High Protein Flour refers to a type of flour that contains a higher amount of protein compared to regular all-purpose flour. Typically made from hard wheat varieties, high-protein flour contains around 12-15% protein, whereas standard all-purpose flour generally contains about 8-11% protein. This increased protein content is essential for products that require more structure, such as bread, pizza dough, and certain baked goods.

End-Use Industries High Protein Flour is particularly prevalent in the bakery and snack industries. According to the U.S. Department of Agriculture (USDA), the bakery products segment in the U.S. alone accounted for over 30% of the total high-protein flour consumption in 2023.

Additionally, the pasta and noodles segment is seeing growth, with high-protein pasta consumption increasing by 6.3% annually. The demand for High Protein Flour in gluten-free products is also surging, especially in regions like North America and Europe, where consumers are increasingly seeking alternative options for dietary preferences.

Government support for the promotion of high-protein, nutrient-dense foods is contributing to the market’s growth. In 2022, the U.S. Food and Drug Administration (FDA) and European Food Safety Authority (EFSA) both issued guidelines encouraging food manufacturers to develop products with higher protein content to address growing concerns around obesity and protein malnutrition. The U.S. Department of Agriculture (USDA) reported an increase of 4.8% in the production of high-protein flour in the last year alone due to these regulatory measures.

The European Union follows closely with a market share of 28%, driven by rising consumer demand for health-focused food products. On the export side, China has expanded its export of high-protein wheat flour by 15% over the last two years, reaching USD 500 million in 2023, catering to growing markets in Asia and the Middle East.

Investments and Innovations Private sector investments are also playing a crucial role in the development of high-protein flour products. In 2023, Archer Daniels Midland (ADM) invested USD 150 million into the expansion of its high-protein flour production facility in the U.S. to meet rising demand.

Moreover, Nestlé has formed a strategic partnership with Pulse Canada to explore plant-based protein alternatives, including High Protein Flour derived from pulses like peas and lentils. The collaboration aims to create more sustainable, high-protein alternatives for the food industry.

Government initiatives are also playing a crucial role in this sector. The Indian Ministry of Food Processing Industries has launched the Production Linked Incentive Scheme for Food Processing Industry (PLISFPI) with an outlay of ₹10,900 crore (approximately USD 1.3 billion) from 2021-22 to 2026-27 to encourage domestic production and exports.

Additionally, the government has permitted 100% Foreign Direct Investment (FDI) in the food processing sector under certain conditions, which is expected to attract significant private investments.

The demand for high protein flour is further supported by innovations and partnerships within the industry. Major companies such as Archer Daniels Midland (ADM), General Mills, and King Arthur Flour Company are actively involved in developing new products that cater to health-conscious consumers.

The B2B distribution channel for high protein flour accounts for 87.8% of the market share and is projected to grow at a CAGR of 10.8%, reflecting the increasing demand from food manufacturers for high-quality protein ingredients.

Key Takeaways

- High Protein Flour Market size is expected to be worth around USD 41.5 Bn by 2033, from USD 15.87 Bn in 2023, growing at a CAGR of 10.1%.

- Conventional high-protein flour held a dominant market position, capturing more than a 68.2% share of the market.

- Powder high-protein flour held a dominant market position, capturing more than a 78.1% share of the market.

- Bleached high-protein flour held a dominant market position, capturing more than a 63.3% share.

- Wheat-Based high-protein flour held a dominant market position, capturing more than an 83.5% share.

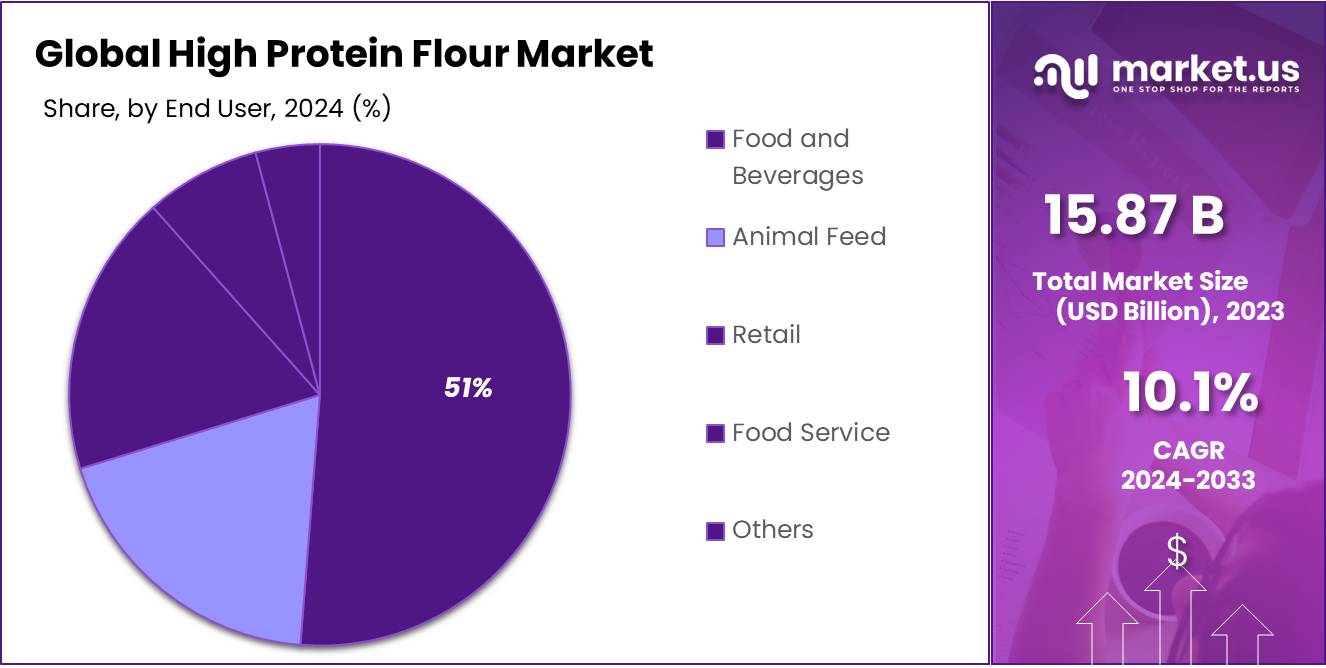

- Food and Beverages held a dominant market position, capturing more than a 56.4% share.

- Hypermarkets & Supermarkets held a dominant market position, capturing more than a 45.6% share.

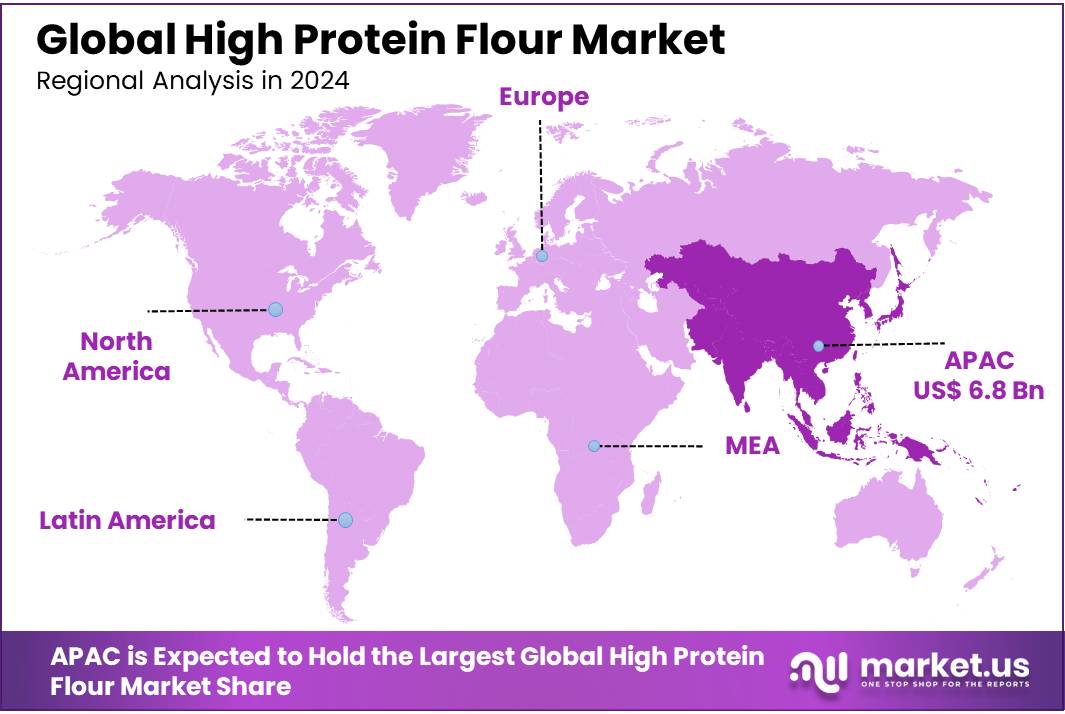

- Asia Pacific (APAC) dominates the global high-protein flour market, accounting for approximately 43.5% of the market share, valued at USD 6.8 billion in 2023.

By Nature

In 2023, Conventional high-protein flour held a dominant market position, capturing more than a 68.2% share of the market. The conventional segment continues to lead due to its widespread availability, cost-effectiveness, and consistent supply. Conventional high-protein flour is commonly sourced from wheat and other grains, which are processed using traditional methods. It remains the preferred choice for large-scale food manufacturers and bakers, especially in the production of bakery products, pasta, and snacks.

The conventional flour market benefits from established infrastructure and lower production costs, which make it more affordable for both producers and consumers. Additionally, conventional High Protein Flour are used in a wide range of applications, making them highly versatile in the food industry. This segment’s growth is supported by its strong presence in global supply chains and the ongoing demand for functional, protein-enriched ingredients in everyday food products.

The Organic high-protein flour segment is growing at a faster rate, driven by the increasing consumer demand for healthier and more sustainable food options. However, organic high-protein flour still holds a smaller market share compared to conventional flour, primarily due to its higher cost and limited availability. As the organic food trend continues to rise, the organic segment is expected to see stronger growth in the coming years.

By Form

In 2023, Powder high-protein flour held a dominant market position, capturing more than a 78.1% share of the market. The powder form is widely preferred due to its versatility, ease of use, and long shelf life. It is commonly used in baking, snack production, and other food applications, as it can be easily incorporated into various recipes. Powdered high-protein flour is also the preferred choice for manufacturers because it can be easily stored, transported, and mixed with other ingredients in large-scale production processes.

The powder form offers significant benefits in terms of flexibility and consistency in production. It can be used in a wide range of food products, including bread, pasta, protein bars, and beverages, where precise protein content is crucial. This widespread use across different food categories is a key factor driving the dominance of the powdered form in the market.

On the other hand, the Liquid form of high-protein flour is gaining traction, particularly in specialized applications like protein drinks, sauces, and nutritional supplements. However, the liquid segment remains smaller compared to powder, mainly due to higher costs and storage challenges. Despite this, as demand for functional beverages and liquid nutritional products grows, the liquid form of high-protein flour is expected to expand in the coming years.

Ву Туре

In 2023, Bleached high-protein flour held a dominant market position, capturing more than a 63.3% share of the market. Bleached flour is widely used in the food industry due to its fine texture, white color, and ability to produce lighter, fluffier baked goods. It is commonly found in products such as cakes, pastries, and bread, where a smooth and consistent texture is desired. The bleaching process also makes the flour more stable and easier to work with, which has contributed to its popularity among both home bakers and large-scale food manufacturers.

The Bleached segment benefits from being more affordable and accessible, as it is produced on a larger scale with well-established processing methods. It is especially favored in commercial baking, where consistent quality and cost-efficiency are key priorities.

In contrast, the Unbleached high-protein flour segment is growing, driven by consumer preference for less processed, more natural food options. Unbleached flour retains its natural color and nutrients, making it a popular choice for health-conscious consumers and artisanal bakers. However, it still holds a smaller market share compared to bleached flour due to its higher cost and slightly coarser texture, which can affect the final product’s appearance and texture. Despite this, the unbleached segment is expected to see steady growth as demand for more natural and organic food products increases.

By Source

In 2023, Wheat-Based high-protein flour held a dominant market position, capturing more than an 83.5% share of the market. Wheat-based flour remains the most widely used source due to its availability, cost-effectiveness, and the high protein content it offers.

It is commonly used in baking, pasta production, and various processed food products, where its gluten content helps provide the structure and texture required for many applications. Wheat-based high-protein flour is the go-to choice for large-scale manufacturers due to its consistent quality, ease of use, and well-established production processes.

The popularity of wheat-based high-protein flour is supported by its versatility across a broad range of food products, from bread and baked goods to snack foods and protein bars. It also benefits from a long-standing presence in the market, with wheat being one of the most widely cultivated grains globally.

By End User

In 2023, Food and Beverages held a dominant market position, capturing more than a 56.4% share of the high-protein flour market. The food and beverage sector continues to be the largest end user, driven by the increasing demand for protein-enriched food products.

High Protein Flour is widely used in the production of baked goods, snacks, protein bars, pasta, and beverages, offering both nutritional value and functional benefits. The growing consumer preference for healthier, high-protein diets has led to a surge in the use of High Protein Flour in this segment.

This sector is seeing strong growth due to rising health-consciousness, with more consumers seeking food products that support muscle growth, weight management, and overall well-being. Major food brands are incorporating High Protein Flour into their product lines to meet the demand for functional foods, further driving the growth of this segment.

The Animal Feed segment is also significant, holding a growing share of the market. High Protein Flour is used in animal feed to enhance the nutritional profile of pet food and livestock feed, especially in the production of protein-rich diets. As the global pet food market continues to expand, so does the demand for High Protein Flour in pet and animal feed.

By Distribution Channel

In 2023, Hypermarkets & Supermarkets held a dominant market position, capturing more than a 45.6% share of the high-protein flour market. These large retail chains continue to be the primary distribution channel due to their wide reach and convenient shopping experience.

Hypermarkets and supermarkets offer High Protein Flour from various brands, catering to the growing demand for health-conscious food options. These stores are preferred by consumers for their variety, ease of access, and competitive pricing. Additionally, the availability of High Protein Flour in larger quantities at these outlets makes them ideal for both individual consumers and businesses looking to purchase in bulk.

The Specialty Stores segment is also growing, as more consumers seek premium or niche products. Specialty stores, which focus on organic, gluten-free, or health-focused foods, are becoming popular destinations for high-protein flour. In 2023, specialty stores accounted for 22.5% of the market, attracting health-conscious buyers looking for unique, high-quality products. These stores offer personalized customer service and specialized knowledge about the benefits of High Protein Flour.

Retail Stores and Online Stores have also seen steady growth. Retail stores cater to local markets, offering High Protein Flour in smaller packages, which are convenient for regular household use. Meanwhile, Online Stores have gained traction due to the convenience of shopping from home, especially for niche or hard-to-find products.

Key Market Segments

By Nature

- Organic

- Conventional

By Form

- Powder

- Liquid

Ву Туре

- Bleached

- Unbleached

By Source

- Wheat Based

- Non-wheat Based

By End User

- Food and Beverages

- Animal Feed

- Retail

- Food Service

- Others

By Distribution Channel

- Hypermarkets & Supermarkets

- Specialty Stores

- Retail Stores

- Online Stores

- Others

Drivers

Increasing Consumer Demand for High-Protein Products

The growing demand for high-protein products is one of the main driving factors behind the rise of high-protein flour. In recent years, there has been a noticeable shift in consumer preferences toward healthier food options, particularly those that provide higher nutritional value.

According to the International Food Information Council (IFIC), 41% of consumers in the U.S. have increased their protein intake over the past five years, with a significant focus on plant-based proteins. This trend is expected to continue as people increasingly seek out alternatives that support better health, muscle maintenance, and weight management.

High Protein Flour, made from ingredients such as peas, lentils, chickpeas, and quinoa, offers an alternative to traditional wheat-based flour. The increased interest in gluten-free and plant-based diets is also contributing to the rise in demand for such alternatives.

A report by the U.S. Department of Agriculture (USDA) shows that the plant-based food market in the U.S. grew by 27% in 2020 alone, totaling a market value of $7 billion. This expansion is expected to continue, with protein-rich alternatives like high-protein flour being a key area of innovation.

As more consumers opt for high-protein diets, food manufacturers are responding by developing products that include higher protein content. A Nielsen survey found that 61% of consumers are actively looking for products with higher protein content, especially in the snack, bakery, and pasta categories. This increased consumer awareness of protein’s benefits has made high-protein flour a sought-after ingredient in the food industry.

Government Initiatives Promoting Health and Nutrition

Governments worldwide are increasingly focused on promoting healthier diets, which is another critical factor driving the high-protein flour market. Various health initiatives and dietary guidelines emphasize the importance of protein in the daily diet.

In the U.S., for example, the 2020-2025 Dietary Guidelines for Americans recommend that protein be a central part of every meal, with a focus on plant-based protein sources. The growing support for plant-based protein is reflected in policy incentives that encourage the development and consumption of protein-rich food alternatives.

The European Union has also implemented various initiatives under the “Farm to Fork” strategy, which aims to make food systems fair, healthy, and environmentally-friendly. The EU’s commitment to promoting plant-based foods aligns with the rise of high-protein flour made from legumes and other plant sources.

According to the European Commission, the plant-based food market in Europe is projected to grow by 12% annually, with significant government backing for sustainable protein sources. These initiatives provide a solid foundation for the high-protein flour market to thrive, as both consumers and manufacturers are encouraged to embrace plant-based protein alternatives.

Additionally, the U.S. government has invested in agricultural programs aimed at enhancing the production of pulse crops, such as chickpeas, lentils, and peas, which are integral to the production of high-protein flour. According to the USDA, the acreage devoted to pulse crops in the U.S. has grown by 5% annually in recent years, contributing to an increase in the availability of plant-based protein sources.

Rising Health Consciousness and Dietary Trends

Health consciousness is another key driver for the growing popularity of high-protein flour. Consumers are increasingly aware of the health benefits of protein, including its role in muscle repair, weight management, and overall wellness. According to a report from the Centers for Disease Control and Prevention (CDC), protein intake is crucial for preventing muscle loss in older adults, which has led to the introduction of high-protein options in various food categories.

The global market for high-protein food is also driven by the growing adoption of specific diets such as keto, paleo, and low-carb, all of which emphasize high protein intake. In the U.S., for example, the keto diet market is valued at over $9 billion.

This market has significantly influenced the demand for high-protein ingredients, including flour, which is used in bread, pasta, and baked goods. High Protein Flour is increasingly seen as a solution for creating products that meet the needs of these health-conscious consumers.

In addition to specific diets, rising concerns about obesity and chronic diseases such as diabetes and heart disease have made consumers more focused on the nutritional content of their food. According to the World Health Organization (WHO), over 2 billion people globally are overweight or obese, a factor contributing to the rising demand for healthier food alternatives, including high-protein flour.

Innovations in High-Protein Flour Production

Innovations in food technology and flour production have made high-protein flour more accessible and affordable, further fueling its market growth. Advances in processing techniques have allowed manufacturers to extract higher protein content from various plant sources, resulting in better-textured, more functional flours.

The Food and Agriculture Organization (FAO) reports that advances in milling technology have increased the protein content of certain grains and legumes by up to 20%, making them viable alternatives to traditional wheat flour.

Moreover, the increasing availability of high-protein flour in bulk is making it a more attractive option for large-scale food manufacturers. With the global protein ingredients market projected to reach $57.5 billion by 2027, innovations in high-protein flour production are set to play a major role in meeting the demand for protein-enriched foods.

As food manufacturers continue to develop new products incorporating high-protein flour, the market for these products is expected to expand, driven by both technological advancements and the increasing consumer demand for protein-rich diets.

Restraints

High Cost of Production and Consumer Pricing Sensitivity

One of the major restraining factors for the growth of the high-protein flour market is the high cost of production associated with these products. High Protein Flours are typically produced using alternative protein sources, such as peas, lentils, quinoa, and chickpeas, which can be more expensive to source and process than traditional wheat flour.

The additional processing required to enhance protein content, coupled with the use of premium ingredients, leads to higher overall costs. This cost burden often translates into higher retail prices, which can be a significant barrier to widespread consumer adoption.

The Food and Agriculture Organization (FAO) has reported that the cost of pulses and legumes (common sources for high-protein flour) increased by 10% globally in the past few years. This price rise impacts the production cost of High Protein Flour, making them less accessible to price-sensitive consumers.

For instance, in the U.S. market, plant-based flour products often retail at 25-50% higher prices compared to traditional wheat flour, which can discourage mass-market acceptance.

According to the U.S. Department of Agriculture (USDA), the price sensitivity in the consumer food market is a significant factor. A 2023 USDA report revealed that 42% of consumers would only purchase plant-based and alternative protein products if they were priced similarly to traditional options.

This sensitivity to pricing highlights a challenge for manufacturers of High Protein Flour in reaching a larger, price-conscious audience. Without achieving cost parity with wheat flour, the high-protein flour market risks being limited to premium consumers, slowing its growth in mainstream markets.

Limited Consumer Awareness and Understanding

Another key restraint facing the high-protein flour market is the limited consumer awareness and understanding of these products. Despite the growing interest in plant-based and high-protein diets, many consumers remain unfamiliar with high-protein flour alternatives.

A study by the International Food Information Council (IFIC) showed that only 25% of consumers were aware of high-protein flour options as a viable ingredient in their diets. This lack of awareness can hinder the growth of the market, as consumers tend to gravitate toward familiar products they understand and trust.

The marketing and promotion of high-protein flour products are still in their early stages, and many consumers may not know how to incorporate these flours into everyday recipes. Moreover, high-protein flour often requires a different method of use compared to regular flour, which can be a barrier to adoption.

For example, baking with high-protein flour may require adjustments in recipes or additional ingredients to maintain desired texture and flavor. The lack of consumer education around these factors can make it difficult for the market to expand, particularly in mainstream grocery stores.

Supply Chain Challenges and Sourcing Limitations

Another major restraint for high-protein flour adoption is the challenge of sourcing sufficient raw materials to meet growing demand. Unlike wheat, which is widely grown and cultivated around the world, ingredients used in High Protein Flour—such as peas, lentils, and quinoa—are less commonly farmed and often have smaller cultivation scales. As demand for these flours increases, there is pressure on the supply chains to scale up production.

The FAO has pointed out that global production of pulses, a key ingredient in High Protein Flour, is constrained by factors such as climate variability and the limited availability of arable land suitable for pulse cultivation.

For instance, the U.S. has seen fluctuating pulse production levels, with the area planted with peas and lentils declining by 5% in 2022, primarily due to climate-induced challenges and market volatility. Such limitations in supply make it difficult to maintain consistent and affordable pricing for high-protein flour, as raw materials become scarcer.

In addition, the infrastructure needed for processing and distribution of alternative protein sources is less developed compared to traditional flour mills. This can lead to delays in production and higher logistical costs, which further contribute to the overall price of high-protein flour.

Opportunity

Expansion of Plant-Based and Gluten-Free Food Markets

A significant growth opportunity for high-protein flour lies in the booming demand for plant-based and gluten-free products. Consumers are increasingly adopting plant-based diets, driven by health concerns, environmental sustainability, and ethical considerations.

In addition, the gluten-free food market, valued at approximately $5.3 billion in 2020 (according to the Gluten Intolerance Group), has been expanding consistently. High Protein Flours made from ingredients like chickpeas, lentils, and quinoa meet the dietary needs of both plant-based and gluten-free consumers, positioning them as attractive options in this growing market.

The rising number of individuals diagnosed with celiac disease or gluten sensitivity—estimated to affect 1 in 100 people worldwide—further supports this demand.

Increasing Awareness of Health Benefits

Rising consumer awareness of the health benefits associated with high-protein diets represents another key growth opportunity for high-protein flour. Studies have shown that increased protein intake can support muscle maintenance, aid in weight management, and help in the recovery of tissue and muscle after exercise.

According to the International Food Information Council (IFIC), 52% of consumers are actively trying to increase their protein intake, with many focusing on plant-based protein sources. This rising awareness aligns well with the trend toward high-protein flour, which is not only rich in protein but also offers other nutritional benefits such as fiber, vitamins, and minerals.

The demand for protein-rich foods is further fueled by the global fitness trend, with more consumers turning to protein-packed snacks and baked goods. As a result, high-protein flour is being incorporated into various food products, such as protein-enriched breads, muffins, cookies, and crackers.

The rising interest in fitness, coupled with the desire to improve overall health and wellness, provides a promising market for high-protein flour manufacturers to tap into. The global protein ingredients market is expected to grow at a CAGR of 8.2% from 2021 to 2028, reaching a market value of $66.5 billion, which will likely drive further demand for high-protein alternatives in baking and food production.

Governments are also encouraging healthier eating habits through public health campaigns and nutritional guidelines. For example, the U.S. Dietary Guidelines recommend that 10-35% of daily calories come from protein. These efforts are likely to further accelerate consumer demand for high-protein products, including High Protein Flour.

Innovation in Product Offerings and Applications

Product innovation presents another significant growth opportunity for high-protein flour. As manufacturers explore new applications for high-protein flour, the range of potential products continues to expand. From protein-enriched breads and pastas to protein bars and smoothies, high-protein flour is being incorporated into a wide variety of consumer goods.

According to the Food and Agriculture Organization (FAO), there has been an increasing focus on developing products that use sustainable and nutrient-dense ingredients, with protein-rich alternatives gaining traction in the food industry.

A report by the U.S. Department of Agriculture (USDA) shows that investment in plant-based food companies has surged, with more than $3 billion raised in 2020 alone. These developments are opening up new pathways for the creation of innovative products using High Protein Flour, which will help expand their reach in both mainstream and niche markets.

Trends

Increased Use of Alternative Protein Sources in Food Products

A key trend shaping the high-protein flour market is the growing use of alternative protein sources to meet the rising consumer demand for plant-based, gluten-free, and sustainable food products. As people seek healthier, more environmentally friendly options, food manufacturers are turning to plant-based protein-rich flours derived from sources like peas, lentils, quinoa, and chickpeas.

According to the Food and Agriculture Organization (FAO), the global production of plant-based proteins is expected to increase by 10% annually through 2025, as consumers prioritize plant proteins for their health benefits and lower environmental impact compared to animal-based proteins.

For instance, pea protein, a popular ingredient in High Protein Flour, has seen a 20% annual growth rate in recent years, reflecting its increasing use in food products like pasta, bread, and snacks.

Governments and organizations are also backing this trend. The USDA’s 2020-2025 Dietary Guidelines encourage the inclusion of plant-based foods to improve health outcomes and reduce environmental footprints.

Growth of High-Protein Flour in Bakery and Snack Products

Another significant trend is the growing application of high-protein flour in the bakery and snack industries. With increasing consumer demand for high-protein, low-carb, and gluten-free products, bakeries and snack manufacturers are incorporating High Protein Flour into a wide range of products.

The global bakery market, valued at $455 billion in 2020 (according to the FAO), is rapidly adopting alternative protein flours to cater to health-conscious consumers.

This trend aligns with government initiatives promoting healthier eating habits. In the U.S., the USDA’s MyPlate initiative emphasizes balanced eating, with a focus on proteins from diverse sources. This has spurred interest in non-traditional, nutrient-dense ingredients like high-protein flour.

Rising Popularity of Sustainable and Eco-Friendly Ingredients

Sustainability is a growing trend in the food industry, and high-protein flour derived from environmentally friendly sources is gaining popularity. Plant-based protein flours generally have a lower environmental footprint compared to animal-based products, particularly in terms of water usage, greenhouse gas emissions, and land usage.

According to the Food and Agriculture Organization (FAO), plant-based protein production typically requires 75% less land and 50% less water compared to producing animal-based proteins.

Regional Analysis

Asia Pacific (APAC) dominates the global high-protein flour market, accounting for approximately 43.5% of the market share, valued at USD 6.8 billion in 2023. The rapid expansion of plant-based and gluten-free diets, coupled with increasing health awareness, has spurred growth in countries like China, India, and Japan.

The rise of urbanization and the adoption of Western diets, combined with a large population base, are key factors propelling the demand for alternative protein sources. In addition, governments in the region are actively promoting healthier food choices, contributing to the market’s growth.

North America is the second-largest market for high-protein flour, with the U.S. and Canada driving the demand for plant-based and gluten-free products. In 2023, the North American market was valued at approximately USD 3.2 billion, growing at a steady rate of 7.5% annually.

The increasing awareness of protein’s role in maintaining health, alongside the popularity of clean-label and sustainable food products, has fueled this demand. Additionally, the region’s robust food processing and manufacturing industries play a crucial role in market development.

Europe also shows strong growth, particularly in the U.K., Germany, and France, where there is rising consumer interest in functional foods. The European market is projected to reach USD 2.5 billion by 2025, driven by health-conscious consumers and regulatory support for alternative proteins.

Latin America and Middle East & Africa represent emerging markets, where high-protein flour adoption is accelerating due to rising awareness of health benefits and increasing gluten-free and plant-based food demand. However, these regions still hold a smaller share compared to APAC, North America, and Europe.

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Key Players Analysis

The high-protein flour market is highly competitive, with several major players establishing a strong presence through product innovation and strategic partnerships. Archer Daniels Midland (ADM) is a leading global player, leveraging its vast distribution network and extensive portfolio of ingredients. The company’s focus on plant-based and alternative protein solutions has made it a significant contributor to the market.

Ardent Mills and Bay State Milling Company are also key players, offering a variety of high-protein flour options derived from alternative sources such as quinoa, chickpeas, and peas. These companies have invested heavily in research and development to cater to the growing demand for healthy, sustainable, and gluten-free products.

Other notable players such as General Mills and King Arthur Baking Company, Inc. are expanding their product lines to include High Protein Flour to meet consumer demand. Giusto’s, known for its organic flour offerings, is increasingly incorporating high-protein varieties into its portfolio to attract health-conscious customers.

Miller Milling Company, Siemer Milling Company, and The White Lily Foods Company also play important roles in the market, providing high-quality protein-rich flours for both the retail and industrial segments.

Smaller players like Janie’s Mill, Weatherbury Farm, and Khandesh Roller Flour Mills Pvt. Ltd. are also emerging as competitive forces in regional markets, focusing on organic and locally sourced ingredients to cater to niche markets.

Top Key Players

- Archer Daniels Midland (ADM)

- Ardent Mills

- Bay State Milling Company

- Central Milling

- Doves Farm Foods

- General Mills

- Giusto’s

- Great River Organic Milling

- Janie’s Mill

- Kaizen Food Company

- Khandesh Roller Flour Mills Pvt. Ltd.

- King Arthur Baking Company, Inc.

- Miller Milling Company

- New Hope Mills

- Siemer Milling Company

- The White Lily Foods Company

- Weatherbury Farm

Recent Developments

In 2024, ADM aims to increase its revenue from plant-based food ingredients to approximately USD 3.5 billion, growing at a compound annual growth rate (CAGR) of 8%.

In 2024, Ardent Mills plans to increase its revenue from alternative protein flours by 15%, aiming to reach USD 1 billion by expanding its presence in key markets like North America and Europe.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2023) | USD 15.9 Bn |

| Forecast Revenue (2033) | USD 41.5 Bn |

| CAGR (2024-2033) | 10.1% |

| Base Year for Estimation | 2023 |

| Historic Period | 2020-2022 |

| Forecast Period | 2024-2033 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Nature (Organic, Conventional), By Form (Powder, Liquid), Ву Туре (Bleached, Unbleached), By Source (Wheat Based, Non-wheat Based), By End User (Food and Beverages, Animal Feed, Retail, Food Service, Others), By Distribution Channel (Hypermarkets and Supermarkets, Specialty Stores, Retail Stores, Online Stores, Others) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA |

| Competitive Landscape | Archer Daniels Midland (ADM), Ardent Mills, Bay State Milling Company, Central Milling, Doves Farm Foods, General Mills, Giusto’s, Great River Organic Milling, Janie’s Mill, Kaizen Food Company, Khandesh Roller Flour Mills Pvt. Ltd., King Arthur Baking Company, Inc., Miller Milling Company, New Hope Mills, Siemer Milling Company, The White Lily Foods Company, Weatherbury Farm |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |