Quick Navigation

- Report Overview

- Key Takeaways

- Product Type Analysis

- Route of Administration Analysis

- Application Analysis

- Distribution Channel Analysis

- Key Market Segments

- Drivers

- Restraints

- Opportunities

- Impact of Macroeconomic / Geopolitical Factors

- Latest Trends

- Regional Analysis

- Key Players Analysis

- Recent Developments

- Report Scope

Report Overview

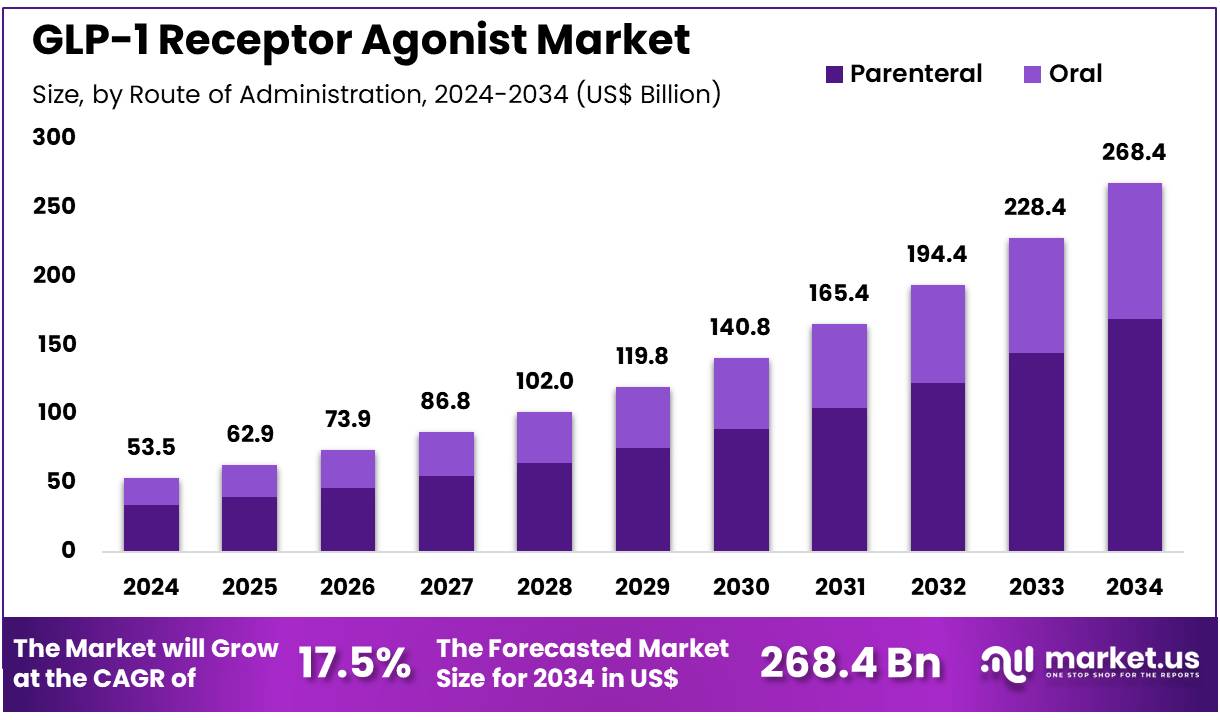

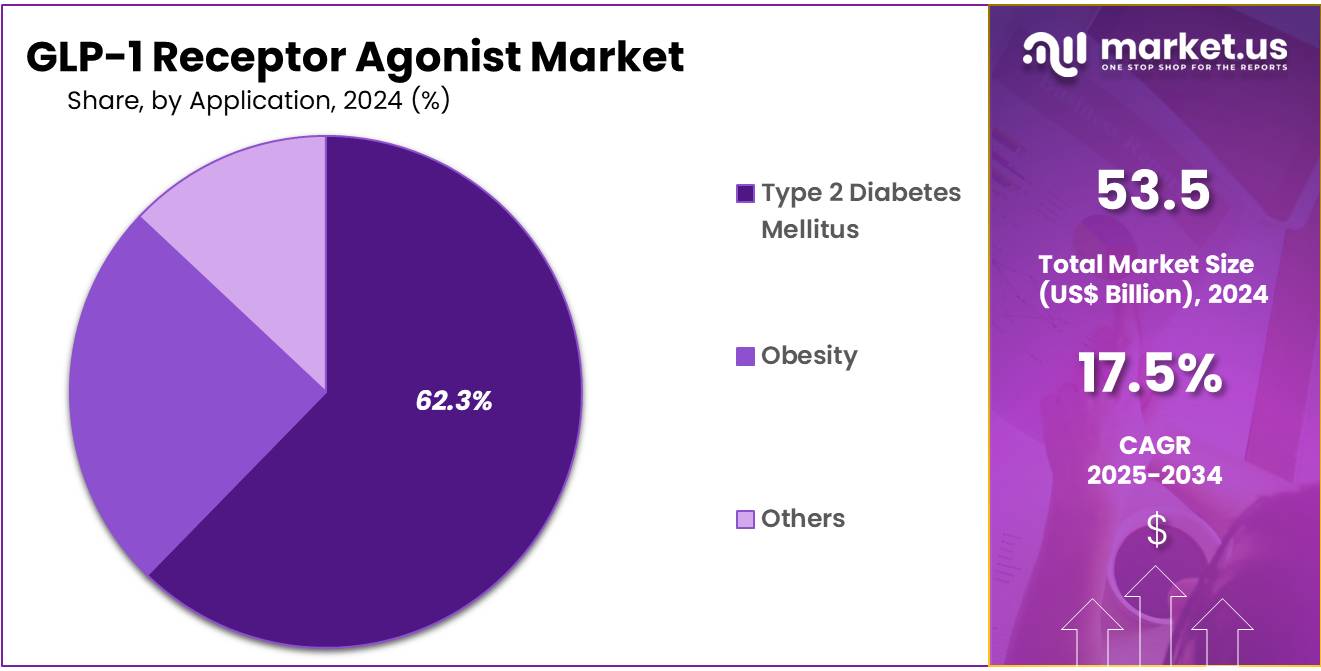

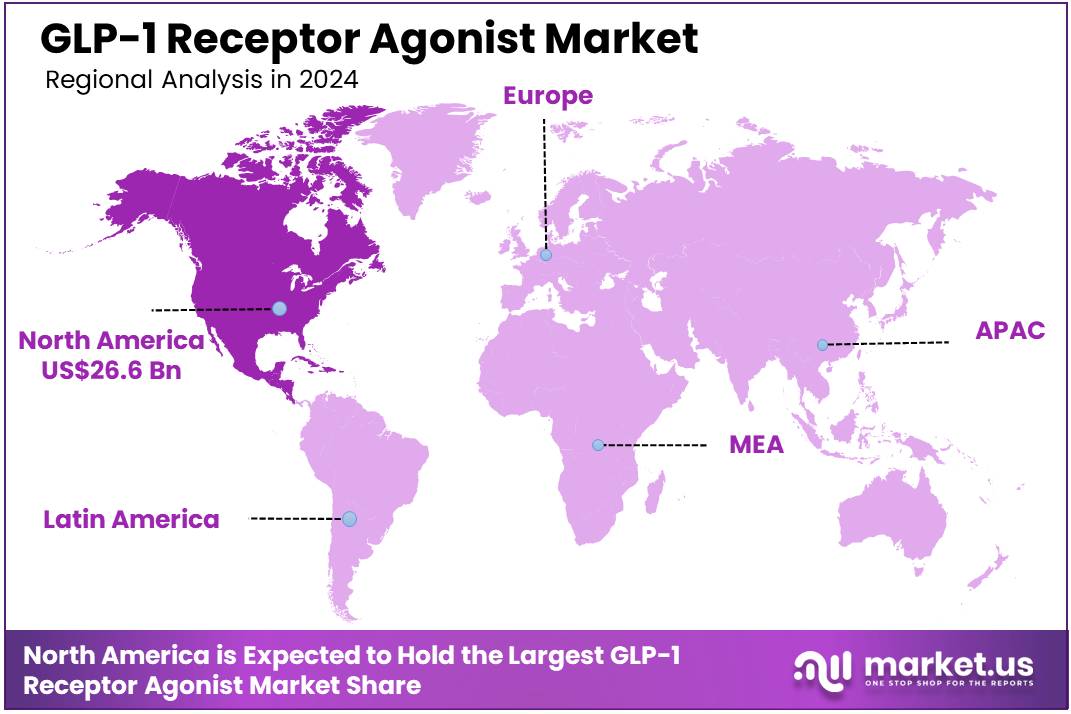

Global GLP-1 Receptor Agonist Market size is expected to be worth around US$ 268.4 billion by 2034 from US$ 53.5 billion in 2024, growing at a CAGR of 17.5% during the forecast period 2025 to 2034. In 2024, North America led the market, achieving over 49.7% share with a revenue of US$ 26.6 Billion.

Increasing prevalence of metabolic disorders, such as obesity and type 2 diabetes, has significantly fueled the growth of the GLP-1 receptor agonist market. These drugs, which stimulate insulin release and reduce appetite, offer promising therapeutic options for managing blood sugar levels and supporting weight loss in individuals with these conditions. The growing demand for more effective, long-term treatments for obesity, diabetes, and cardiovascular health has driven the rapid adoption of GLP-1 receptor agonists.

In August 2024, Eli Lilly & Company announced the positive outcomes of the SURMOUNT-1 trial, indicating that Tirzepatide (marketed as Zepbound and Mounjaro) decreased the risk of developing type 2 diabetes by 94% in individuals with prediabetes, obesity, or overweight. During the 176-week study, participants receiving the 15 mg dose experienced an average weight loss of 22.9%, demonstrating the drug’s efficacy.

The market also sees significant opportunities for expanding the application of GLP-1 receptor agonists beyond diabetes, with emerging research exploring their role in treating heart failure, non-alcoholic steatohepatitis (NASH), and other chronic conditions. Advances in formulation and combination therapies, alongside positive clinical data, continue to fuel innovation and open new avenues for market growth.

Key Takeaways

- In 2024, the market for GLP-1 receptor agonist generated a revenue of US$ 53.5 billion, with a CAGR of 17.5%, and is expected to reach US$ 268.4 billion by the year 2033.

- The product type segment is divided into semaglutide, liraglutide, exenatide, dulaglutide, and others, with semaglutide taking the lead in 2024 with a market share of 58.4%.

- Considering route of administration, the market is divided into parenteral and oral. Among these, parenteral held a significant share of 63.2%.

- Furthermore, concerning the application segment, the market is segregated into type 2 diabetes mellitus, obesity, and others. The type 2 diabetes mellitus sector stands out as the dominant player, holding the largest revenue share of 62.3% in the GLP-1 receptor agonist market.

- The distribution channel segment is segregated into hospital pharmacies, online pharmacies, and retail pharmacies, with the hospital pharmacies segment leading the market, holding a revenue share of 57.8%.

- North America led the market by securing a market share of 49.7% in 2024.

Product Type Analysis

The semaglutide segment led in 2024, claiming a market share of 58.4% owing to the clinical efficacy and widespread adoption of semaglutide-based products for both type 2 diabetes and obesity management. Clinical trial data published since 2021 has consistently demonstrated significant HbA1c reduction and weight loss with semaglutide compared to other GLP-1 receptor agonists.

The availability of both injectable and oral formulations of semaglutide has further enhanced its market penetration and patient preference. The strong clinical profile and versatile administration options have established semaglutide as a leading product type in the GLP-1 receptor agonist market.

Route of Administration Analysis

The parenteral held a significant share of 63.2% due to the established efficacy and bioavailability of injectable GLP-1 receptor agonists in managing blood glucose levels and promoting weight loss. Several well-established and widely prescribed GLP-1 receptor agonists, including various formulations of semaglutide, liraglutide, and dulaglutide, are administered via subcutaneous injection.

While oral GLP-1 receptor agonists are gaining traction, the long-standing clinical experience and proven effectiveness of parenteral formulations continue to hold the largest market share.

Application Analysis

The type 2 diabetes mellitus segment had a tremendous growth rate, with a revenue share of 62.3% owing to the well-established role of GLP-1 receptor agonists in improving glycemic control, promoting weight loss, and offering cardiovascular benefits in patients with type 2 diabetes.

The American Diabetes Association (ADA) guidelines updated in 2023 recommend GLP-1 receptor agonists as a preferred treatment option for many patients with type 2 diabetes, particularly those with or at high risk for cardiovascular disease or kidney disease. The high global prevalence of type 2 diabetes continues to drive the demand for effective glucose-lowering agents like GLP-1 receptor agonists.

Distribution Channel Analysis

The hospital pharmacies segment grew at a substantial rate, generating a revenue portion of 57.8% as hospitals are key centers for the diagnosis and management of type 2 diabetes and obesity, often initiating treatment with GLP-1 receptor agonists.

The established infrastructure and purchasing power of hospital pharmacies, coupled with the direct dispensing to patients within the hospital setting and through outpatient clinics, contribute to this segment’s dominance. Furthermore, hospital pharmacies often manage the dispensing of injectable medications requiring specific storage and handling, which is the case for many GLP-1 receptor agonists.

Key Market Segments

Product Type

- Semaglutide

- Liraglutide

- Exenatide

- Dulaglutide

- Others

Route of Administration

- Parenteral

- Oral

Application

- Type 2 diabetes mellitus

- Obesity

- Others

Distribution Channel

- Hospital pharmacies

- Online pharmacies

- Retail pharmacies

Drivers

Increasing Global Prevalence of Type 2 Diabetes Mellitus and Obesity is Driving the Market

The escalating global prevalence of type 2 diabetes mellitus and obesity is a major driver for the GLP-1 Receptor Agonist Market. The International Diabetes Federation (IDF) estimated that 537 million adults were living with diabetes in 2021, and this number is projected to rise significantly in the coming years. Obesity rates are also climbing globally, with the World Health Organization (WHO) reporting over one billion individuals affected in 2022.

GLP-1 receptor agonists have demonstrated efficacy in managing both conditions by improving glycemic control and promoting weight loss, making them increasingly prescribed therapeutic options. The growing awareness of the health risks associated with diabetes and obesity and the increasing emphasis on effective management strategies are fueling the demand for GLP-1 receptor agonists.

Restraints

High Cost and Potential Gastrointestinal Side Effects May Restrain Market Growth

The relatively high cost of GLP-1 receptor agonists can be a significant restraint on market growth, particularly in regions with limited healthcare access or reimbursement. The monthly cost of some GLP-1 receptor agonists can be substantial, potentially limiting their affordability for a large segment of the patient population.

Additionally, gastrointestinal side effects, such as nausea, vomiting, and diarrhea, are commonly associated with GLP-1 receptor agonists, especially during the initial phase of treatment. These side effects can impact patient tolerability and adherence, potentially limiting the widespread adoption of these drugs in some individuals. Ongoing research into mitigating these side effects and the development of more cost-effective alternatives are crucial for overcoming these restraints.

Opportunities

Growing Clinical Evidence of Cardiovascular and Renal Benefits is Creating Growth Opportunities

Increasing clinical evidence highlighting the cardiovascular and renal benefits of certain GLP-1 receptor agonists is significantly driving their adoption. Landmark clinical trials published since 2021, such as those investigating the effects of semaglutide and dulaglutide, have demonstrated a reduction in major adverse cardiovascular events (MACE) and a slowing of the progression of chronic kidney disease in patients with type 2 diabetes.

These findings have led to the inclusion of GLP-1 receptor agonists in updated treatment guidelines by organizations like the American Heart Association (AHA) and the American Diabetes Association (ADA) for patients with these comorbidities. The proven benefits beyond glucose control are expanding the use of GLP-1 receptor agonists and driving market growth.

Impact of Macroeconomic / Geopolitical Factors

The GLP-1 Receptor Agonist Market in 2025 is influenced by macroeconomic factors affecting healthcare expenditure and access to innovative medicines. Economic growth in developed economies typically supports higher healthcare spending, facilitating the adoption of relatively expensive GLP-1 receptor agonists.

Conversely, economic downturns can lead to budgetary constraints in healthcare systems and potentially limit patient access, especially in countries with less robust reimbursement mechanisms. Government healthcare policies and regulations regarding drug pricing and reimbursement play a critical role in determining the affordability and market penetration of GLP-1 receptor agonists.

Favorable reimbursement policies and government initiatives to improve access to diabetes and obesity treatments can significantly drive market growth. Geopolitical factors, such as trade agreements, intellectual property rights, and the stability of international supply chains for pharmaceutical ingredients, can also impact the manufacturing and distribution of GLP-1 receptor agonists globally.

The recent US tariff policies implemented in April 2025 could have specific implications for the GLP-1 Receptor Agonist Market. The United States relies on international supply chains for the manufacturing of pharmaceutical ingredients and finished drug products. Tariffs on imported active pharmaceutical ingredients (APIs) or components used in the manufacturing of GLP-1 receptor agonists could potentially increase production costs for US-based manufacturers.

This could lead to higher drug prices for patients and healthcare systems. Furthermore, retaliatory tariffs imposed by other countries on US-manufactured pharmaceuticals could impact the export opportunities for US companies in the global GLP-1 receptor agonist market. The long-term effects will depend on the specific details of the tariff policies and the strategic responses of pharmaceutical companies in adjusting their supply chains and pricing strategies.

Latest Trends

Recent Development of Novel Formulations and Delivery Systems is Driving Adoption

The ongoing development of novel formulations and delivery systems for GLP-1 receptor agonists is creating significant growth opportunities. The introduction of oral formulations, such as oral semaglutide approved in 2019, has improved patient convenience and adherence by eliminating the need for injections.

Pharmaceutical companies are also investing in the development of longer-acting injectable formulations, reducing the frequency of administration to once weekly or even less. Additionally, research into novel delivery technologies, such as microneedle patches and implantable devices, holds the potential to further enhance patient convenience and compliance, thereby expanding the market reach and attractiveness of GLP-1 receptor agonists.

Regional Analysis

North America is leading the GLP-1 Receptor Agonist Market

North America dominated the market with the highest revenue share of 49.7% owing to the high prevalence of both type 2 diabetes and obesity, coupled with a well-established healthcare infrastructure and favorable reimbursement policies. According to the Centers for Disease Control and Prevention (CDC) data from 2023, over 37 million adults in the United States have diabetes, and the prevalence of obesity is also significantly high.

The strong presence of key pharmaceutical companies, the high adoption rates of innovative treatments, and the extensive coverage for prescription drugs contribute to North America’s dominant market position. Furthermore, the increasing awareness of the cardiovascular and renal benefits of GLP-1 receptor agonists is further driving their uptake in the region.

The Asia Pacific region is expected to experience the highest CAGR during the forecast period

Asia Pacific is expected to grow with the fastest CAGR owing to the rapidly increasing prevalence of type 2 diabetes and growing investments in healthcare infrastructure. The International Diabetes Federation (IDF) reported in 2021 that the Asia Pacific region has the largest number of adults living with diabetes globally, exceeding 290 million.

As healthcare systems in countries like China and India continue to expand and patient access to advanced medications improves, the demand for effective glucose-lowering and weight management drugs like GLP-1 receptor agonists is expected to surge. Increasing awareness of diabetes and obesity, coupled with rising disposable incomes and government initiatives to improve chronic disease management, are key factors driving the significant growth potential of the GLP-1 receptor agonist market in the Asia Pacific region.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia

- Netherland

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- New Zealand

- Singapore

- Thailand

- Vietnam

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Key Players Analysis

Key players in the GLP-1 Receptor Agonist Market are characterized by their strong research and development capabilities, extensive product portfolios, and global presence. These companies are continuously innovating to develop new GLP-1 receptor agonists with improved efficacy, safety profiles, and convenient administration routes, including oral formulations.

Strategic collaborations, licensing agreements, and acquisitions are also common strategies to expand their market reach and product offerings. Competition in the market is intense, with companies focusing on demonstrating superior clinical outcomes and securing favorable reimbursement status for their products.

Novo Nordisk A/S, headquartered in Bagsvaerd, Denmark, is a dominant player in the GLP-1 receptor agonist market. The company offers a range of GLP-1 receptor agonists, including semaglutide (Ozempic, Rybelsus, Wegovy) and liraglutide (Victoza, Saxenda). Novo Nordisk’s strong clinical data and successful commercialization of its GLP-1 receptor agonist portfolio have established it as a market leader. Their continuous investment in research and development, particularly in oral formulations and novel indications, further strengthens their position.

Top Key Players

- Sun Pharmaceutical Industries Ltd

- Sanofi

- Pfizer.Inc

- Novo-Nordisk A/S

- Eli Lilly and Company

- Boehringer Ingelheim International GmbH

- AstraZeneca

- Amylyx Pharmaceuticals

Recent Developments

- In July 2024, Amylyx Pharmaceuticals strategically acquired Avexitide, a promising GLP-1 receptor agonist, from Eiger Biopharmaceuticals. Avexitide, which has been granted FDA breakthrough therapy designation, has shown significant effectiveness in treating Postbariatric Hypoglycemia (PBH) and congenital hyperinsulinism, and is expected to commence Phase 3 trials for PBH by early 2025.

- In January 2024, Novo Nordisk A/S established new research partnerships with two U.S.-based biotechnology companies, with the goal of developing advanced treatments for cardiometabolic conditions. This strategic move reinforces Novo Nordisk’s dedication to pioneering innovative therapies for conditions such as obesity, diabetes, and cardiovascular diseases.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2024) | US$ 53.5 billion |

| Forecast Revenue (2034) | US$ 268.4 billion |

| CAGR (2025-2034) | 17.5% |

| Base Year for Estimation | 2024 |

| Historic Period | 2020-2023 |

| Forecast Period | 2025-2034 |

| Report Coverage | Revenue Forecast, Market Dynamics, COVID-19 Impact, Competitive Landscape, Recent Developments |

| Segments Covered | By Product Type (Semaglutide, Liraglutide, Exenatide, Dulaglutide, and Others), By Route of Administration (Parenteral and Oral), By Application (Type 2 Diabetes Mellitus, Obesity, and Others), By Distribution Channel (Hospital Pharmacies, Online Pharmacies, and Retail Pharmacies) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, New Zealand, Singapore, Thailand, Vietnam, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA |

| Competitive Landscape | Sun Pharmaceutical Industries Ltd, Sanofi, Pfizer.Inc, Novo-Nordisk A/S, Eli Lilly and Company, Boehringer Ingelheim International GmbH, AstraZeneca, and Amylyx Pharmaceuticals. |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |