Quick Navigation

Report Overview

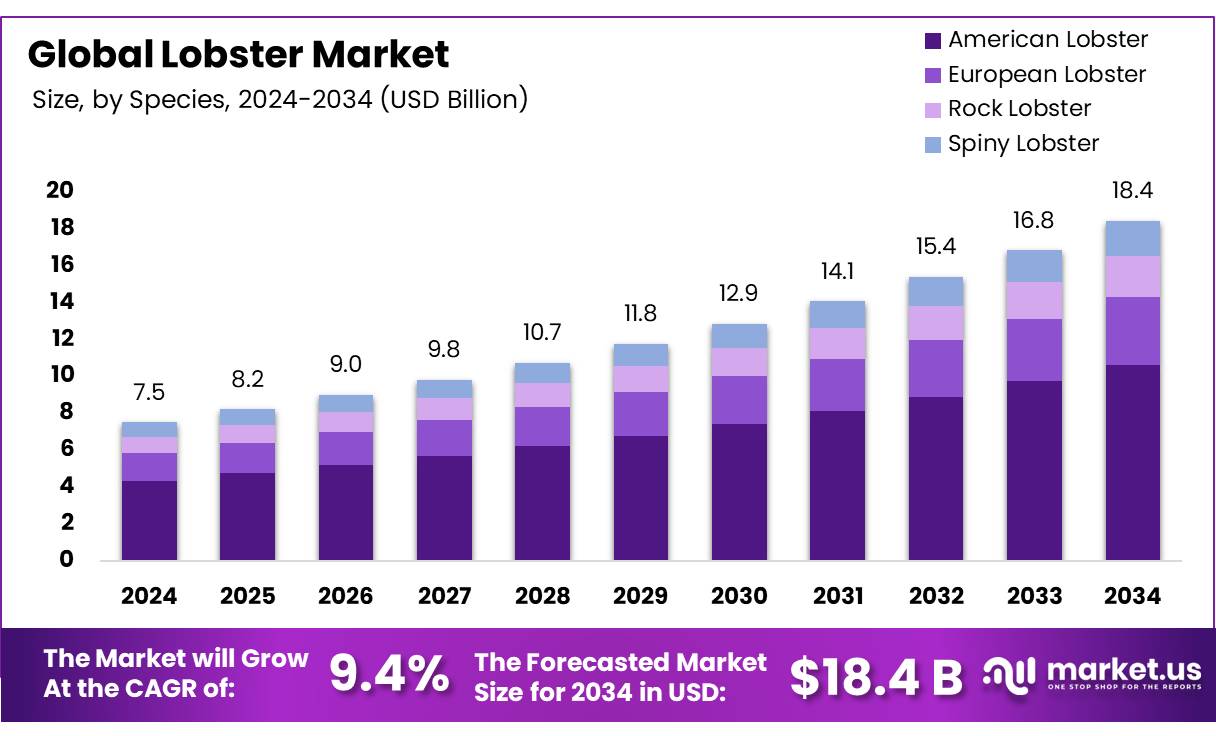

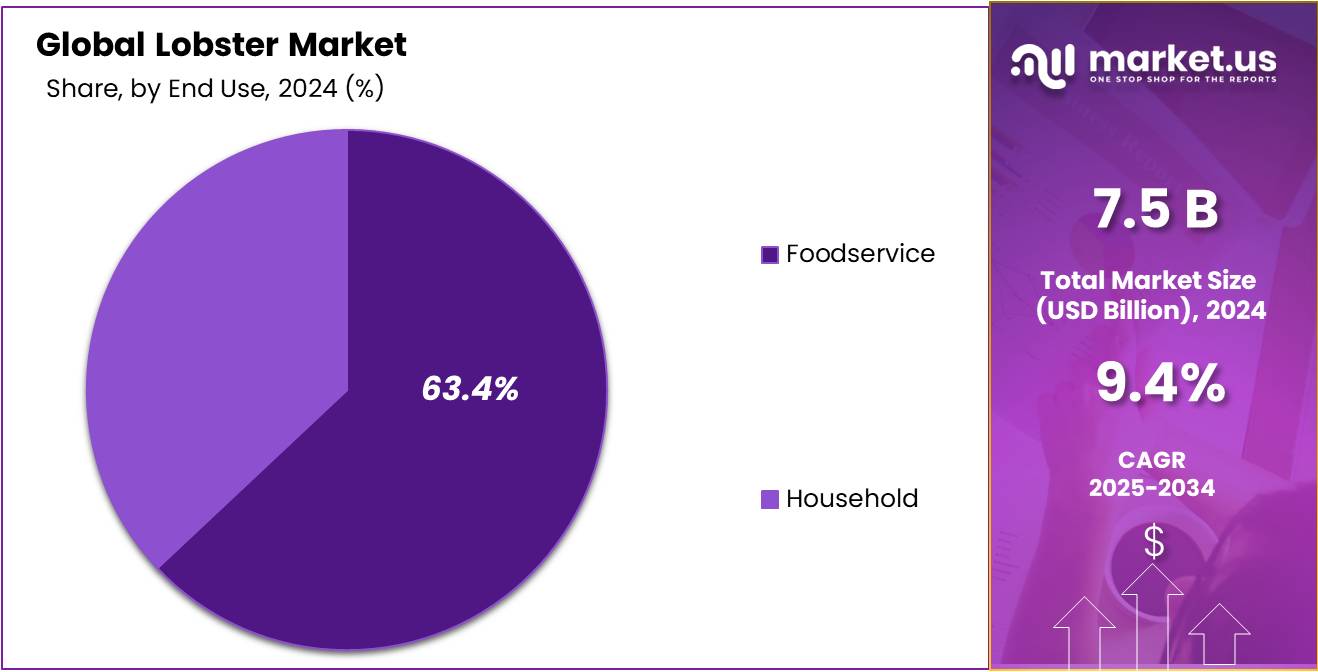

The Global Lobster Market size is expected to be worth around USD 18.4 billion by 2034, from USD 7.5 billion in 2024, growing at a CAGR of 9.4% during the forecast period from 2025 to 2034.

The Lobster Market is a vital segment of the seafood industry, driven by increasing consumer demand for premium, high-quality seafood. Lobsters, marine crustaceans prized for their tender, flavorful meat, are considered a luxury food item, often associated with fine dining and special occasions. The market encompasses fishing, aquaculture, processing, and distribution, with significant activity in North America, Europe, and Asia-Pacific.

This is characterized by robust supply chains, primarily led by North America, which accounted for over 48% of the market share in 2024, driven by fisheries in Maine and Atlantic Canada. Food service dominates distribution channels, holding the largest share due to the proliferation of gourmet restaurants and quick-service chains. However, retail is gaining traction with the rise of e-commerce and direct-to-consumer sales, offering frozen and canned lobster products.

Key driving factors include rising health consciousness, as lobsters are rich in protein, omega-3 fatty acids, and essential nutrients like selenium, boosting demand among fitness enthusiasts. Increasing disposable incomes, particularly in Asia-Pacific, where China’s lobster imports surged in 2024, further propel market growth. The expansion of the hospitality sector and premium dining trends also contribute significantly.

Future growth opportunities lie in innovative aquaculture practices, such as closed-loop systems, and product diversification, including value-added items like lobster rolls and bisque. Emerging markets in Latin America and Europe, coupled with advancements in online retailing, offer untapped potential. However, challenges like price volatility and environmental regulations necessitate sustainable practices to ensure long-term viability.

Key Takeaways

- The Lobster Market is projected to grow from USD 7.5 billion in 2024 to USD 18.4 billion by 2034, at a CAGR of 9.4%.

- American Lobster leads with a 57.8% share, prized for its flavor and sourced mainly from North Atlantic waters.

- Frozen lobster dominates with a 68.7% share, favored for shelf stability and global trade efficiency.

- Hard-shell lobsters hold a 76.3% share due to superior meat yield and transport durability.

- Supermarkets and Hypermarkets capture 41.9% share, offering convenience and reliable cold storage.

- Foodservice drives 63.4% demand, with lobster as a premium menu staple in restaurants and hotels.

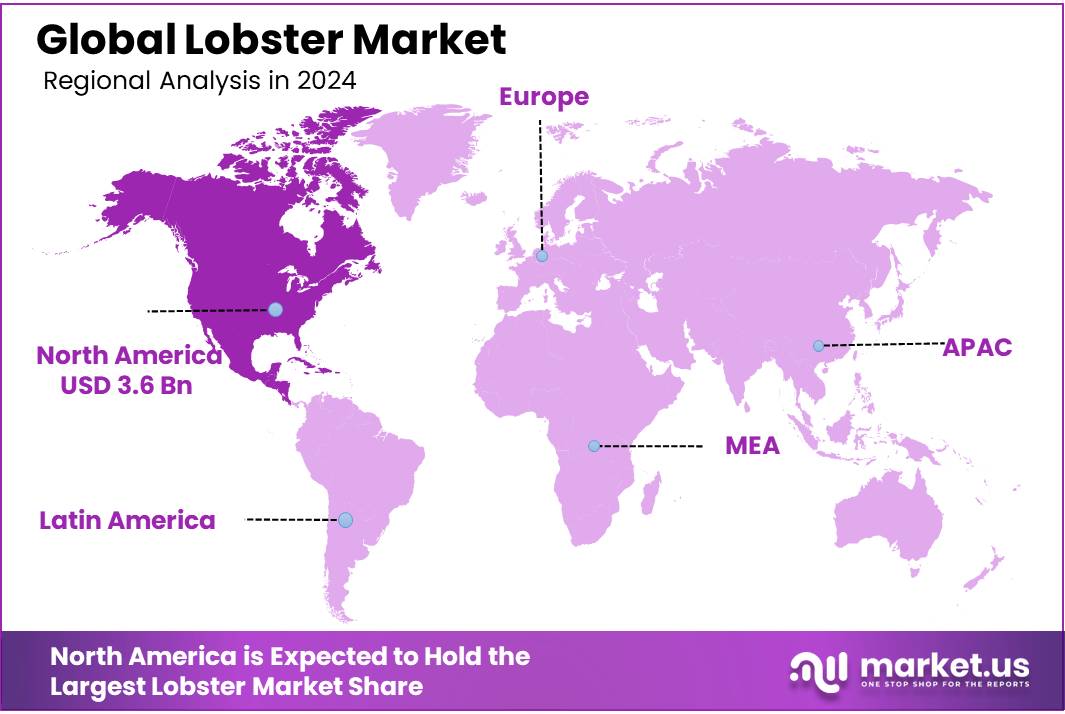

- North America holds a 48.4% share, valued at USD 3.6 billion, supported by strong consumption and logistics.

Analyst Viewpoint

The Lobster Industry presents compelling investment opportunities driven by strong global demand and technological advancements, but it’s not without risks. With North America dominating the market at 48.4% share, valued at USD 3.6 billion in 2024, the sector thrives on premium seafood consumption, particularly in the U.S. and Canada.

The market is not without risks. Environmental factors such as climate change are impacting lobster populations, leading to regulatory challenges. For instance, rising ocean temperatures and acidification are altering lobster habitats, prompting stricter fishing regulations. Price volatility due to seasonal supply fluctuations and geopolitical issues can affect profit margins.

Investors must weigh these factors. Opportunities in aquaculture and global markets are exciting, but environmental and regulatory challenges demand careful strategy. The lobster industry’s future hinges on balancing innovation with resilience, offering a dynamic yet cautious investment landscape.

By Species

In 2024, American Lobster held a dominant market position, capturing more than a 57.8% share in the global lobster market. This species continues to be the most widely harvested and consumed type, especially across North America and parts of Europe. Its popularity is rooted in its rich flavor, tender texture, and adaptability to various cuisines, from fine dining to casual seafood offerings.

The American Lobster fishery occurs from Maine to Cape Hatteras, North Carolina. There are seven Lobster Conservation Management Areas (Areas), which are labeled as Area 1, Area 2, Area 3, Area 4, Area 5, Area 6, and Outer Cape Cod Area. The American lobster resource and fishery are cooperatively managed by the states and the NOAA Fisheries under the framework of the Atlantic States Marine Fisheries Commission.

The lobster fishery predominantly uses pots and traps, but other gear may include gillnets, trawls, and by hand by divers. The market for lobster is for human consumption and is primarily sold live or frozen. U.S. wild-caught American lobster is a smart seafood choice because it is sustainably managed and responsibly harvested under U.S. regulations.

By Product Type

In 2024, Frozen held a dominant market position, capturing more than a 68.7% share in the global lobster market. The frozen segment has gained strong preference due to its extended shelf life, ease of transportation, and year-round availability. It allows suppliers to overcome the limitations of seasonality and perishability that come with live or fresh lobster, making it a practical choice for global trade.

Frozen lobster is widely favored by restaurants, hotels, and retail chains as it reduces the risk of spoilage and lowers logistics costs. In 2025, this segment is expected to see continued growth as consumer demand rises in regions like Asia-Pacific and the Middle East, where importers rely heavily on frozen products due to geographic distance from lobster-producing countries.

Additionally, advancements in freezing technologies have improved the quality of frozen lobster, preserving taste and texture close to that of fresh variants. This has helped in building consumer trust and expanding sales in online grocery platforms and supermarkets. With shifting lifestyles and rising interest in premium frozen seafood, the frozen product type is likely to stay at the forefront of the lobster market’s growth in the coming years.

By Type

In 2024, Hard-shell held a dominant market position, capturing more than a 76.3% share in the global lobster market. Known for their firm texture and higher meat content, hard-shell lobsters are preferred by both consumers and suppliers for their quality and better yield. These lobsters are more durable during transport, making them ideal for exports and long-distance shipments without compromising freshness or structure.

Hard-shell lobsters are especially popular in North America and Europe, where culinary standards demand meatier and more resilient lobsters for both fine dining and bulk food processing. In 2025, demand for hard-shell lobsters is expected to remain strong, supported by rising purchases from foodservice outlets and frozen product manufacturers that prioritize consistent meat quality.

The higher resistance to handling and cooking processes also makes hard-shell types more desirable in commercial kitchens and packaged seafood products. With increasing global interest in premium shellfish and better storage options, hard-shell lobsters are expected to retain their lead, serving as a reliable option for large-scale buyers and quality-conscious consumers alike.

By Distribution Channel

In 2024, Supermarkets and Hypermarkets held a dominant market position, capturing more than a 41.9% share in the global lobster market. These retail formats continue to be the most preferred choice for consumers looking for convenience, product variety, and reliable quality. Their wide reach and established cold storage facilities allow them to stock frozen and fresh lobsters consistently, attracting both household shoppers and bulk buyers.

Supermarkets and hypermarkets often offer attractive packaging, ready-to-cook options, and promotional deals, which contribute to increasing lobster purchases across urban regions. In 2025, their share is likely to grow further, driven by expanding seafood sections, better supply chain systems, and rising middle-class spending on premium food.

These retail outlets also benefit from partnerships with certified suppliers and seafood brands, ensuring sustainable sourcing practices that appeal to environmentally conscious consumers. With a focus on food safety, traceability, and convenient buying experiences, supermarkets and hypermarkets will continue to lead the distribution channel landscape of the lobster market.

By End-Use

In 2024, Foodservice held a dominant market position, capturing more than a 63.4% share in the global lobster market. High demand from hotels, restaurants, cruise lines, and catering services continues to drive this segment’s strong performance. Lobster is widely seen as a premium offering on menus, and its presence boosts the appeal of fine dining and special occasion meals.

Chefs across the globe prefer lobster for its flavor, texture, and versatility in gourmet recipes. In 2025, the foodservice sector is expected to maintain its lead, supported by rising tourism, increasing consumer dining-out habits, and the return of large-scale events. Seasonal lobster dishes, seafood festivals, and luxury hospitality experiences are also boosting year-round demand in this segment.

Many foodservice businesses are now sourcing frozen or pre-cooked lobster to manage costs, reduce prep time, and ensure consistent quality. This operational flexibility has further fueled market share growth. As urban populations grow and culinary cultures evolve, the foodservice industry will remain the primary driver of lobster consumption worldwide.

Key Market Segments

By Species

- American Lobster

- European Lobster

- Rock Lobster

- Spiny Lobster

By Product Type

- Frozen

- Tails

- Meat

- In Shell

- Others

- Live

By Type

- Hard-shell

- Soft-shell

By Distribution Channel

- Supermarkets and Hypermarkets

- Convenience Stores

- Online Retail

- Others

By End-Use

- Foodservice

- Household

Drivers

Sustainability Initiatives Shaping the Lobster Industry

One major driving factor for the lobster industry is the growing emphasis on sustainability initiatives, fueled by consumer demand for ethically sourced seafood and the need to protect lobster populations from overfishing and environmental challenges. As people become more aware of their food choices on the planet, the industry is adapting to ensure long-term viability, balancing economic growth with ecological responsibility.

The National Oceanic and Atmospheric Administration (NOAA) reported that 28 lobster fisheries in North America were certified by the Marine Stewardship Council (MSC), covering a significant portion of the market. This certification ensures that fishing practices meet strict environmental standards, such as maintaining healthy lobster populations and minimizing habitat damage.

The MSC’s influence is huge; 97% of Canada’s lobster fisheries are MSC-certified, showcasing a commitment to sustainable harvesting. These efforts resonate with consumers, who increasingly seek out the MSC blue label in stores and restaurants, driving demand for responsibly sourced lobster.

Restraints

Environmental Challenges Threatening the Lobster Industry

One major restraint for the lobster industry is the growing impact of environmental challenges, particularly climate change, which disrupts lobster habitats and threatens the delicate balance of marine ecosystems. Rising ocean temperatures, acidification, and shifting currents are making it harder for lobsters to thrive.

According to the National Oceanic and Atmospheric Administration (NOAA), ocean temperatures in the Gulf of Maine, a key lobster fishing region. NOAA reported a 20% decline in juvenile lobster abundance in some areas, signaling potential future shortages.

Warmer waters also drive lobsters northward, shifting prime fishing grounds and straining traditional fishing communities in southern New England. Meanwhile, ocean acidification, caused by absorbing excess carbon dioxide, weakens lobster shells, making them more vulnerable to disease and predators.

Opportunity

Rising Global Demand Fueling Lobster Industry Growth

A major growth factor for the lobster industry is the surging global demand for this premium seafood, driven by its reputation as a delicacy and its appeal in both traditional and emerging markets. People around the world are craving lobster’s rich flavor, whether it’s steamed with butter in a coastal Maine shack or served in upscale restaurants in Asia.

This growing appetite is opening new opportunities for fishermen, exporters, and communities, creating jobs and boosting local economies while celebrating a cherished natural resource. Lobster’s high nutritional value, packed with omega-3s and low in calories, makes it a favorite for health-conscious diners, further driving demand.

Government initiatives are helping fuel this growth. NOAA’s Seafood Inspection Program ensures U.S. lobster meets international quality standards, building trust with foreign buyers. Trade agreements, like the U.S.-China Phase One deal, have eased tariffs, boosting exports. Meanwhile, fishermen and cooperatives are investing in cold-chain logistics to deliver fresh lobster worldwide.

Trends

Aquaculture Innovation Boosting Lobster Production

An emerging factor for the lobster industry is the rise of aquaculture innovation, particularly advancements in land-based and sustainable lobster farming. This approach is gaining traction as a way to meet growing demand while easing pressure on wild lobster populations. It’s not just about science, it’s about people finding new ways to bring this beloved seafood to tables worldwide, supporting communities, and preserving the ocean’s delicate balance.

The National Oceanic and Atmospheric Administration (NOAA)—aquaculture is emerging as a game-changer. In Norway, companies have developed land-based systems that raise lobsters from egg to harvest in controlled environments, reducing environmental risks like disease and overfishing.

Government initiatives are key to this progress. NOAA’s Sea Grant program supports pilot projects, helping small-scale farmers test lobster aquaculture. Canada’s Department of Fisheries and Oceans also funds research into sustainable hatchery systems. These efforts show a human touch, communities embracing new ideas to protect their heritage while feeding a hungry world.

Regional Analysis

North America Leads Global Lobster Market with 48.4% Share

In 2024, North America held a dominant position in the global lobster market, capturing a substantial 48.4% share, valued at approximately USD 3.6 billion. The region’s leadership is primarily driven by robust domestic consumption, well-established cold chain logistics, and strong seafood culture across the United States and Canada.

The United States remains the largest contributor within North America, supported by high demand from foodservice channels, luxury restaurants, and retail-ready seafood offerings. Additionally, Maine is recognized as a global hotspot for sustainably harvested American lobster, which adds significant value and authenticity to the regional supply.

Growth is further supported by government-backed sustainability initiatives, including Canada’s Marine Stewardship Council (MSC)-certified fisheries and the U.S. Fishery Management Plans. North America’s consumer trend is shifting toward traceable, eco-labeled seafood, which has boosted premium lobster sales in both fresh and frozen formats.

North America is expected to maintain its leadership, supported by steady production and expanding trade agreements. Emerging markets in Asia and the Middle East present new opportunities for Canadian exports to these regions. With robust infrastructure, high-quality supply, and strong export networks.

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

- Clearwater Seafoods is one of the largest vertically integrated seafood companies in North America. It specializes in wild-caught lobster sourced from the cold Atlantic waters of Canada. The company operates its own fleet and processing plants, ensuring traceability and high product quality. In 2024, Clearwater continued expanding its distribution in Asia and Europe, capitalizing on demand for sustainably harvested lobster.

- East Coast Seafood Group operates as a global supplier of live and frozen lobster products. Headquartered in Massachusetts, the company has a strong presence across the U.S., Canada, Europe, and Asia. In 2024, East Coast expanded its value-added product line, including lobster meat and ready-to-cook offerings.

- Geraldton Fishermen’s Co-operative is a key player in the rock lobster segment. It manages a network of over 150 fishing vessels and emphasizes sustainable harvesting practices. In 2024, the cooperative expanded exports to China, Japan, and the U.S., backed by high demand for Western Rock Lobster.

Top Key Players in the Market

- Clearwater Seafoods

- Douty Bros

- East Coast Seafood Group

- Geraldton Fishermen’s Co-operative

- Supreme Lobster

- Tangier Lobster Company Limited

- Boston Lobster Company

- The Fresh Lobster Company

- Graffam Bros Seafood

- Wild Legend

- Royal Greenland A and S

- Boston Lobster

Recent Developments

- In 2025, Clearwater Seafoods, a leading North American shellfish producer, announced significant changes to its lobster operations. The company laid off workers at its Arichat, Nova Scotia, processing facility and ceased its seasonal lobster processing line at the Lockeport, Nova Scotia, plant, which will now focus solely on scallops.

- In 2024, East Coast Seafood Group (ECSG) remains a global leader in lobster and scallop processing, operating state-of-the-art facilities in Massachusetts. ECSG expanded its product line to include value-added fish species with marinades and dry rubs, complementing its signature North American lobster offerings.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2024) | USD 7.5 Billion |

| Forecast Revenue (2034) | USD 18.4 Billion |

| CAGR (2025-2034) | 9.4% |

| Base Year for Estimation | 2024 |

| Historic Period | 2020-2023 |

| Forecast Period | 2025-2034 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Species (American Lobster, European Lobster, Rock Lobster, Spiny Lobster), By Product Type (Frozen, Tails, Meat, In Shell, Others, Live), By Type (Hard-shell, Soft-shell), By Distribution Channel (Supermarkets and Hypermarkets, Convenience Stores, Online Retail, Others), By End-Use (Foodservice, Household) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – GCC, South Africa, Rest of MEA |

| Competitive Landscape | Clearwater Seafoods, Douty Bros, East Coast Seafood Group, Geraldton Fishermen’s Co-operative, Supreme Lobster, Tangier Lobster Company Limited, Boston Lobster Company, The Fresh Lobster Company, Graffam Bros Seafood, Wild Legend, Royal Greenland A and S, Boston Lobster |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited Users and Printable PDF) |