Quick Navigation

Report Overview

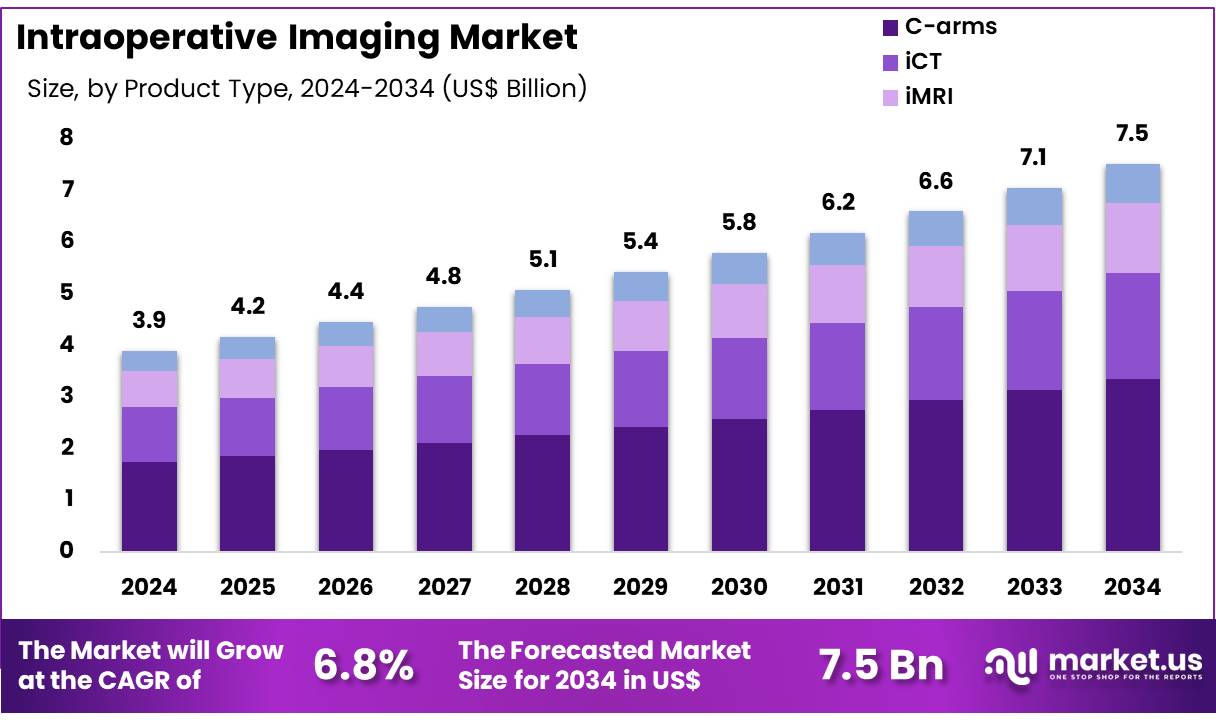

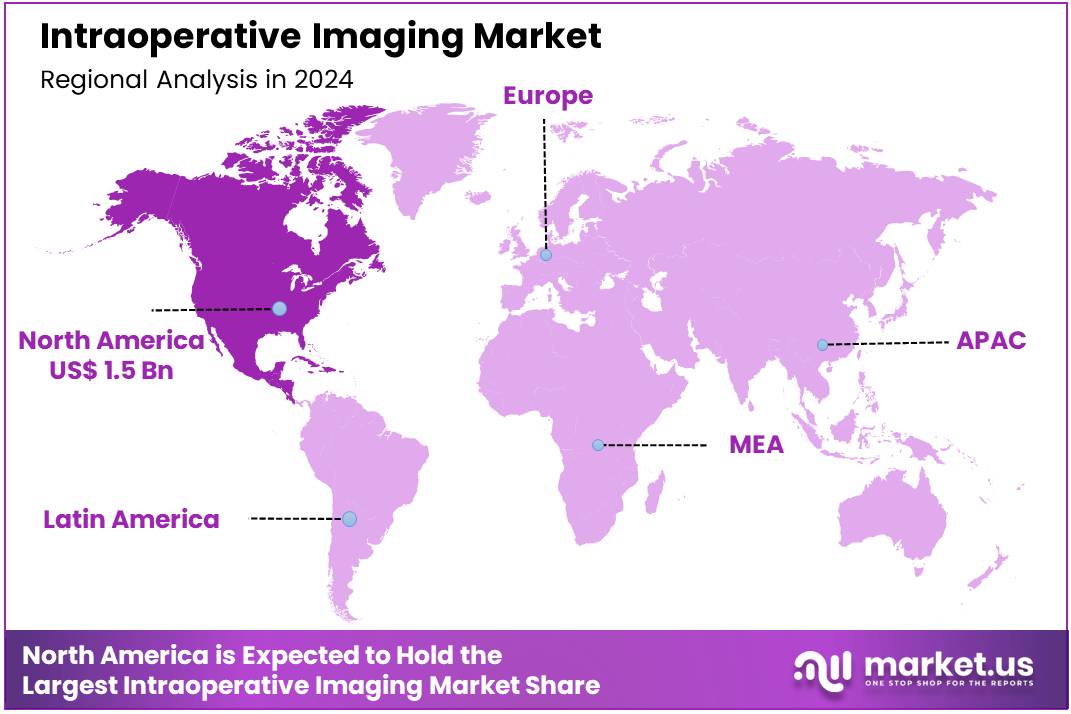

The Global Intraoperative Imaging Market size is expected to be worth around US$ 7.5 Billion by 2034 from US$ 3.9 Billion in 2024, growing at a CAGR of 6.8% during the forecast period 2025 to 2034. In 2024, North America led the market, achieving over 37.6% share with a revenue of US$ 1.5 Billion.

Rising demand for precision surgery and the need for enhanced patient outcomes are driving the growth of the intraoperative imaging market. Intraoperative imaging technologies, such as 3D imaging, fluoroscopy, and ultrasound, provide real-time visual guidance during surgical procedures, improving the accuracy of complex surgeries and reducing the risk of complications. These technologies are crucial in a variety of specialties, including neurosurgery, orthopedics, and cardiovascular surgery, where precise visualization of internal structures is essential.

The increasing adoption of minimally invasive surgery, which requires advanced imaging to guide small incisions, is further fueling market expansion. In February 2024, GE Healthcare announced a strategic partnership with Biofourmis to enhance continuity of care by enabling safe, effective, and accessible healthcare at home. This collaboration combines both companies’ expertise to develop scalable solutions, offering potential applications for intraoperative imaging in home care settings.

The integration of artificial intelligence (AI) and machine learning with intraoperative imaging systems is another growing trend, helping surgeons make more informed decisions during procedures by providing advanced analytics and enhanced image clarity.

Additionally, the ongoing development of portable imaging devices offers increased flexibility in surgical environments, allowing for imaging in smaller and more remote settings. As technology continues to advance, the intraoperative imaging market presents significant opportunities for improving surgical precision, reducing recovery times, and advancing patient care.

Key Takeaways

- In 2024, the market for intraoperative imaging generated a revenue of US$ 3.9 billion, with a CAGR of 6.8%, and is expected to reach US$ 7.5 billion by the year 2033.

- The product type segment is divided into C-arms, iCT, iMRI, and intraoperative ultrasound, with C-arm taking the lead in 2024 with a market share of 44.5%.

- Considering application, the market is divided into neurosurgery, trauma /emergency room surgery, orthopedic surgery, oncology surgery, ENT surgery, cardiovascular surgery, and others. Among these, neurosurgery held a significant share of 42.4%.

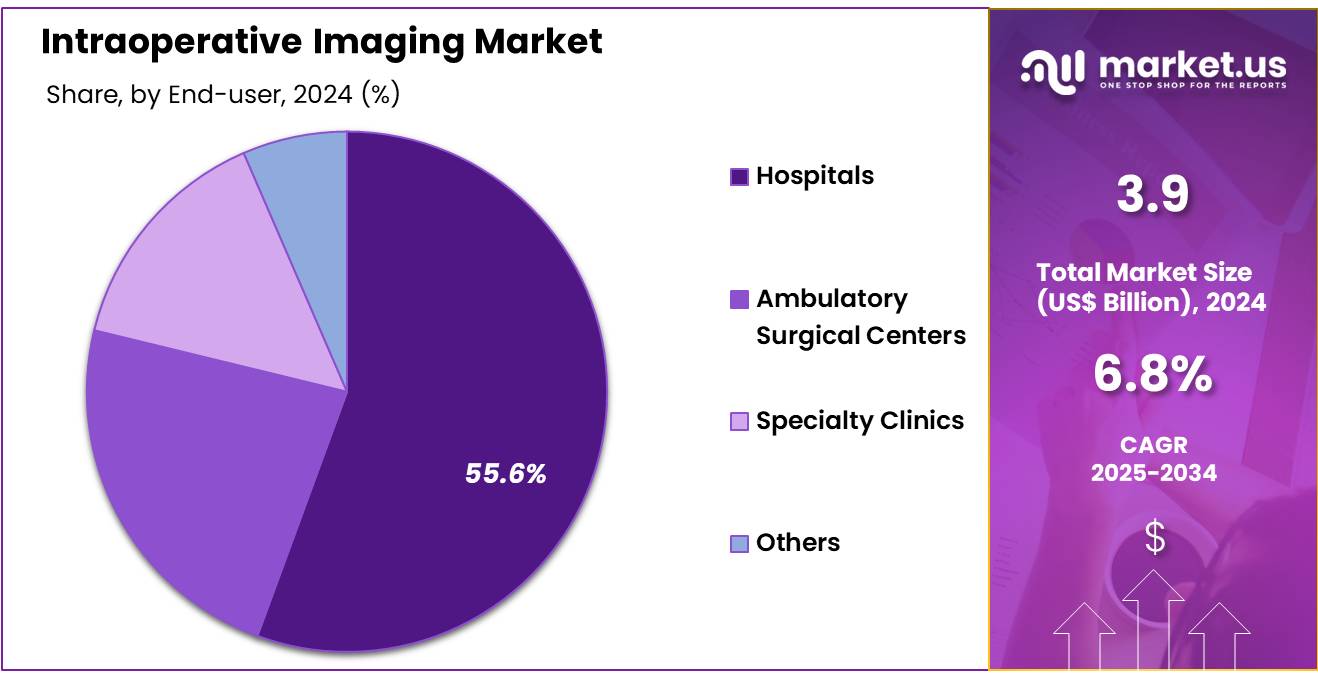

- Furthermore, concerning the end-user segment, the market is segregated into hospitals, ambulatory surgical centers, specialty clinics, and others. The hospital sector stands out as the dominant player, holding the largest revenue share of 55.6% in the intraoperative imaging market.

- North America led the market by securing a market share of 37.6% in 2024.

Product Type Analysis

The C-arm segment claimed a market share of 44.5% owing to the increasing demand for real-time imaging during complex surgical procedures. C-arms offer high-resolution imaging and are widely used in orthopedic, trauma, and cardiovascular surgeries, where precise visual guidance is crucial for improving patient outcomes.

The growing adoption of minimally invasive surgeries, which require real-time imaging for accurate navigation, is anticipated to drive demand for C-arms. Additionally, advancements in C-arm technologies, such as portable and mobile C-arms with enhanced imaging capabilities, are likely to make them more accessible and efficient in diverse surgical environments. As the need for precision in surgical procedures increases, the C-arm segment is projected to expand rapidly.

Application Analysis

The neurosurgery held a significant share of 42.4% due to as the demand for accurate and real-time imaging during brain and spine surgeries increases. Neurosurgeons rely heavily on advanced imaging technologies to visualize critical structures, minimize risks, and improve surgical outcomes. The growing complexity of neurosurgical procedures, particularly with the rise in brain tumor surgeries, spinal surgeries, and deep brain stimulation procedures, is expected to drive the need for intraoperative imaging solutions.

Moreover, the growing focus on minimally invasive techniques in neurosurgery is likely to further boost the demand for imaging systems that offer detailed guidance with minimal disruption to surrounding tissues. As the importance of precise imaging continues to be recognized in neurosurgery, this segment is anticipated to see continued growth.

End-user Analysis

The hospital segment had a tremendous growth rate, with a revenue share of 55.6% owing to the increasing number of surgeries performed in hospital settings, as well as the demand for enhanced surgical precision and patient safety. Hospitals are likely to invest in intraoperative imaging technologies to support complex and high-risk surgeries, including neurosurgery, orthopedic surgery, and cardiovascular procedures. The need for real-time imaging to guide surgeons and reduce the risk of complications is projected to drive this segment’s growth.

Additionally, hospitals are increasingly adopting advanced imaging technologies to improve patient outcomes, reduce recovery times, and optimize operating room efficiency. As the healthcare industry focuses on improving surgical quality and reducing costs, the hospital segment is expected to see significant expansion in the intraoperative imaging market.

Key Market Segments

By Product Type

- C-arms

- iCT

- iMRI

- Intraoperative Ultrasound

By Application

- Neurosurgery

- Trauma /Emergency Room Surgery

- Orthopedic Surgery

- Oncology Surgery

- ENT Surgery

- Cardiovascular Surgery

- Others

By End-user

- Hospitals

- Ambulatory Surgical Centers

- Specialty Clinics

- Others

Drivers

Increasing number of surgical procedures is driving the market

The increasing number of surgical procedures in the US is driving the demand for intraoperative imaging. As medical capabilities expand and the population requires more interventions, the volume of operations performed grows across many medical specialties. Modern surgical techniques, including minimally invasive approaches, frequently rely on real-time visualization during the procedure to enhance accuracy and improve patient outcomes.

This heightened need for precise guidance in the operating room directly fuels the demand for advanced imaging systems. The data on hospital utilization provides insight into the volume of surgical activity. For example, US community hospitals recorded over 32.3 million admissions in 2023, according to the American Hospital Association (AHA), reflecting the significant number of inpatient procedures performed, many of which utilize or could benefit from intraoperative imaging.

Restraints

Rising operational costs for hospitals are restraining the market

Rising operational costs for hospitals are restraining investment in new intraoperative imaging equipment. While the benefits of advanced imaging in surgery are clear, the significant financial pressures faced by healthcare providers can limit their ability to make large capital investments in new technology. Hospitals contend with increasing expenses related to labor, supplies, and other operational needs, impacting their bottom line and the funds available for equipment procurement.

These financial constraints can lead to delayed purchases or prioritization of other critical needs over expensive imaging systems. For instance, the median operating margin for US hospitals was a loss of 3.8% in 2022, based on data from the Medicare Cost Report analysis, illustrating the financial challenges many institutions faced during this period when considering significant capital expenditures like intraoperative imaging systems.

Opportunities

Technological advancements are creating growth opportunities

Technological advancements are creating growth opportunities in the intraoperative imaging market. Innovations are consistently improving the capabilities of imaging systems used during surgery, leading to enhanced image quality, reduced radiation exposure, and better integration with other surgical tools and navigation systems. The development of more sophisticated software for image processing and 3D reconstruction also increases the utility and precision of intraoperative imaging.

These technological leaps make the systems more valuable to surgeons and can improve patient care, encouraging adoption. The US Food and Drug Administration (FDA) continues to clear new and improved intraoperative imaging devices, demonstrating the successful translation of technological innovation into commercially available products.

Impact of Macroeconomic / Geopolitical Factors

Macroeconomic and geopolitical factors significantly influence the market for imaging technology used during surgery. Economic conditions directly impact the capital budgets of hospitals and healthcare systems, which are the primary purchasers of this expensive equipment; periods of economic strength generally correlate with increased investment in new technology, while downturns can lead institutions to defer major purchases, affecting market demand.

Geopolitical instability can disrupt global supply chains for complex medical devices and their components, potentially causing manufacturing delays, increasing costs, and creating uncertainty in equipment availability for healthcare providers.

According to a report in May 2025, geopolitical risks were contributing to supply chain disruptions in the broader medical device sector, which includes imaging equipment. Despite these potential negative impacts from economic volatility and geopolitical tensions, the critical role of accurate visualization in improving patient safety and surgical outcomes provides a fundamental demand that helps stabilize the market for these essential tools.

Current US tariff policies can influence the market for surgical imaging equipment by increasing the cost of imported medical devices and their components. Many sophisticated imaging systems and their specialized parts are manufactured internationally, and tariffs imposed on these goods increase the cost for US hospitals and surgical centers acquiring them.

Reports in early 2025 highlighted that US tariffs on various medical devices and components were expected to raise healthcare costs and impact the medical technology supply chain. While these tariffs present a financial challenge for healthcare providers investing in imaging technology, the essential nature of this equipment for modern surgical practice and patient care ensures continued demand, and tariffs could potentially encourage some degree of domestic manufacturing of certain components or systems over time, contributing to a more resilient supply chain in the future.

Latest Trends

Increased focus on workflow integration is a recent trend

A recent trend in the market is the increased focus on workflow integration for intraoperative imaging systems. Manufacturers are designing systems that seamlessly fit into the existing operating room environment and surgical workflow, minimizing disruption and improving efficiency. This includes features like intuitive user interfaces, faster image processing, and improved maneuverability of mobile units.

The goal is to make obtaining and utilizing real-time imaging during surgery as quick and easy as possible, allowing surgical teams to focus on the patient. The design features highlighted in FDA 510(k) submissions and product literature for devices cleared in 2022-2024 often emphasize improved workflow and ease of use, reflecting this key development trend in the market.

Regional Analysis

North America is leading the Intraoperative Imaging Market

North America dominated the market with the highest revenue share of 37.6% owing to the increasing adoption of advanced surgical procedures. The FDA has been instrumental in clearing new intraoperative imaging devices, which facilitates their use in hospitals across the US. For instance, the FDA has cleared several advanced intraoperative imaging systems between 2022 and 2024, enhancing the availability of these technologies for surgical guidance.

Furthermore, the National Institutes of Health (NIH) supports research that advances intraoperative imaging techniques. Through grants and funding initiatives, the NIH contributes to the development of more precise and effective imaging tools used during surgery.

This support is evident in the NIH’s funding of projects focused on improving surgical outcomes through enhanced visualization technologies. The combination of FDA approvals and NIH-backed research has fueled the expansion of intraoperative imaging in North American medical centers.

The Asia Pacific region is expected to experience the highest CAGR during the forecast period

Asia Pacific is expected to grow with the fastest CAGR owing to the increasing investment in healthcare infrastructure and the rising demand for minimally invasive surgical procedures. Governments across the Asia Pacific region are modernizing their healthcare facilities, which is projected to increase the adoption of advanced medical technologies like intraoperative imaging.

For example, countries like Japan and China are actively promoting the use of advanced medical devices to improve surgical precision and patient outcomes. Additionally, the growing awareness of the benefits of minimally invasive surgery among both surgeons and patients is likely to drive the demand for intraoperative imaging systems that enhance surgical accuracy.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia

- Netherland

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- New Zealand

- Singapore

- Thailand

- Vietnam

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Key Players Analysis

Key players in the global intraoperative imaging market pursue growth through technological innovation, strategic partnerships, and geographic expansion. They focus on developing advanced imaging systems that enhance surgical precision and reduce patient recovery times. Collaborations with hospitals and research institutions facilitate the integration of cutting-edge technologies into clinical practice. Expanding into emerging markets allows companies to tap into new customer bases and address the increasing demand for surgical procedures.

Additionally, investments in training and support services ensure the effective utilization of imaging systems, leading to improved patient outcomes. Brainlab AG is a leading player in the intraoperative imaging sector, specializing in digital surgery and medical technology. The company offers a range of products, including the Loop-X mobile imaging robot and the Cirq robotic alignment module, designed to support spine procedures. Brainlab’s innovations aim to enhance surgical precision and efficiency, contributing to better patient outcomes.

Through strategic acquisitions, such as MedPhoton and Dr. Langer Medical GmbH, Brainlab has expanded its capabilities in robotic surgery and intraoperative imaging. With a strong focus on research and development, Brainlab continues to be at the forefront of advancements in surgical technology.

Top Key Players

- Ziehm Imaging GmbH

- Siemens Healthcare GmbH

- Medtronic plc

- Koninklijke Philips

- IMRIS

- GE HealthCare

- Canon Medical Systems Corporation

- Brainlab AG

Recent Developments

- In January 2024, Siemens Healthineers AG expanded its collaboration with City Cancer Challenge (C/Can), focusing on global initiatives. The partnership aims to support C/Can’s cancer-related projects in low- and middle-income regions, contributing to better access to care.

- In October 2023, GE Healthcare reached a major achievement by leading the US Food and Drug Administration (FDA) list for artificial intelligence (AI) powered medical devices. With 58 510(k) clearances or authorizations in the US, this milestone underscores GE Healthcare’s commitment to advancing healthcare through cutting-edge AI technology.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2024) | US$ 3.9 billion |

| Forecast Revenue (2034) | US$ 7.5 billion |

| CAGR (2025-2034) | 6.8% |

| Base Year for Estimation | 2024 |

| Historic Period | 2020-2023 |

| Forecast Period | 2025-2034 |

| Report Coverage | Revenue Forecast, Market Dynamics, COVID-19 Impact, Competitive Landscape, Recent Developments |

| Segments Covered | By Product Type (C-arms, iCT, iMRI, and Intraoperative Ultrasound), By Application (Neurosurgery, Trauma /Emergency Room Surgery, Orthopedic Surgery, Oncology Surgery, ENT Surgery, Cardiovascular Surgery, and Others), By End-user (Hospitals, Ambulatory Surgical Centers, Specialty Clinics, and Others) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, New Zealand, Singapore, Thailand, Vietnam, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA |

| Competitive Landscape | Ziehm Imaging GmbH, Siemens Healthcare GmbH, Medtronic plc, Koninklijke Philips, IMRIS, GE HealthCare, Canon Medical Systems Corporation, Brainlab AG |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |