Quick Navigation

Report Overview

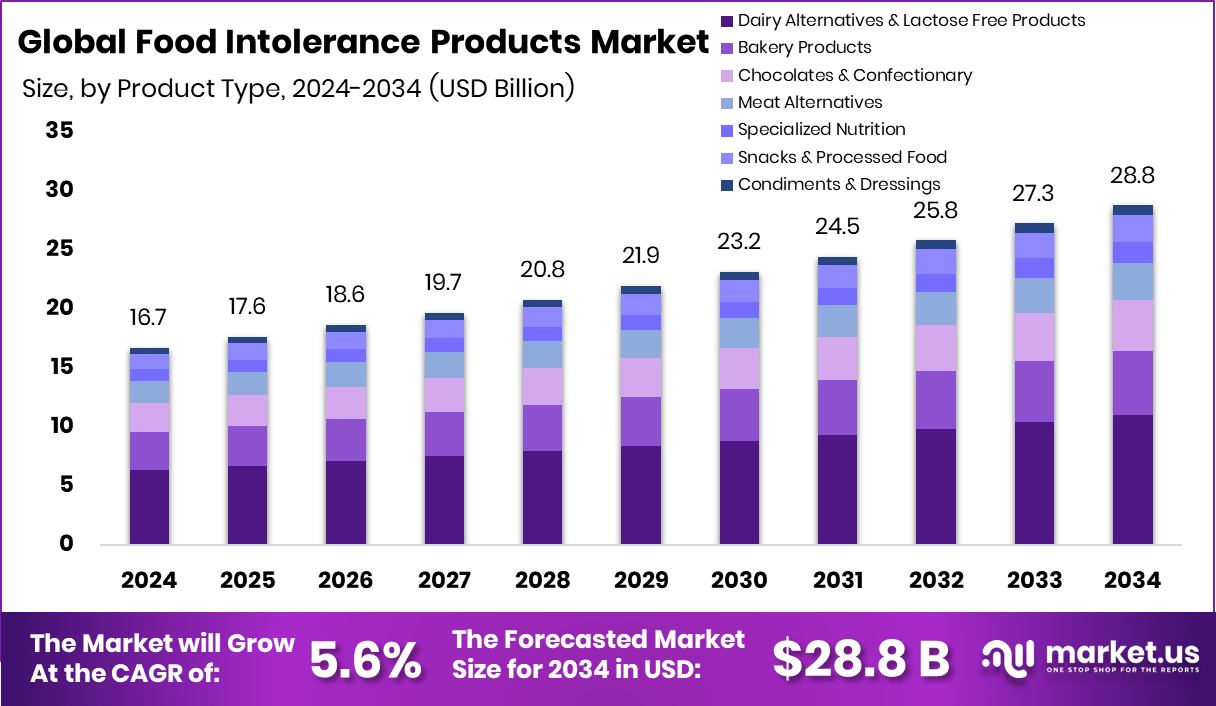

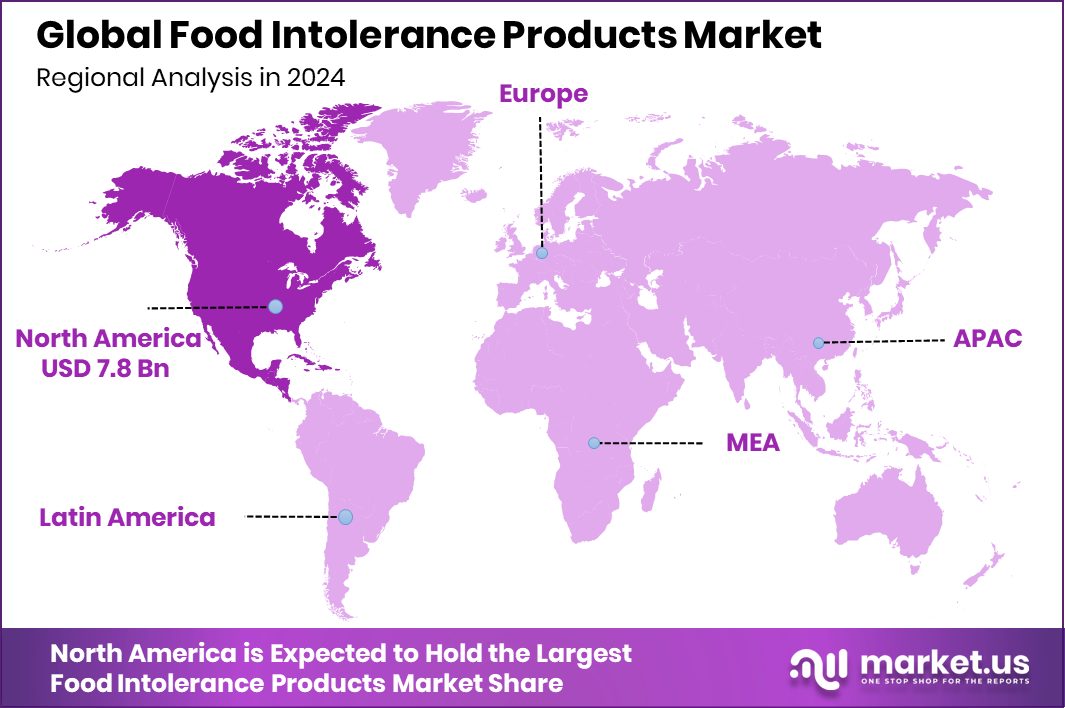

Global Food Intolerance Products Market is expected to be worth around USD 28.8 billion by 2034, up from USD 16.7 billion in 2024, and grow at a CAGR of 5.6% from 2025 to 2034. With a 47.3% share, North America dominates at a USD 7.8 Bn market size.

Food intolerance products are specially formulated food items designed for individuals who experience adverse reactions to certain ingredients, such as lactose, gluten, or specific food additives. Unlike food allergies, which involve the immune system, intolerances usually result from the digestive system’s inability to process specific compounds.

Common food intolerance products include lactose-free dairy, gluten-free grains, and additive-free packaged foods. These products help prevent discomfort such as bloating, indigestion, and stomach pain, enabling consumers to maintain a balanced diet without triggering symptoms.

The food intolerance products market caters to a rapidly growing segment of health-conscious consumers who either have diagnosed food intolerances or prefer free-from diets. This market has seen considerable momentum due to rising public awareness, improved diagnostic testing, and an overall increase in digestive health concerns. Consumers are now actively reading ingredient labels and seeking safe alternatives, prompting food producers to reformulate products and introduce new ranges suited to specific intolerance needs.

The global market for food intolerance products is experiencing significant growth, driven by increasing awareness of food-related health issues and a rising prevalence of food allergies and intolerances. According to the Food and Agriculture Organization (FAO), approximately 220 million people worldwide suffer from food allergies, highlighting the substantial demand for specialized food products that cater to this demographic.

In India, the prevalence of celiac disease, a condition necessitating a strict gluten-free diet, is estimated at 0.67%, affecting approximately 4 to 6 million individuals. Notably, the incidence is higher in northern regions of the country. This underscores the need for increased availability and accurate labeling of gluten-free products to prevent inadvertent consumption and associated health risks.

Key Takeaways

- Global Food Intolerance Products Market is expected to be worth around USD 28.8 billion by 2034, up from USD 16.7 billion in 2024, and grow at a CAGR of 5.6% from 2025 to 2034.

- In 2024, Dairy Alternatives and Lactose Free Products held a 38.1% share by product type category.

- Dairy and Lactose Intolerance led the market by intolerance type with 36.7% of total segment share.

- Conventional products dominated the market by category in 2024, capturing a 67.3% market share.

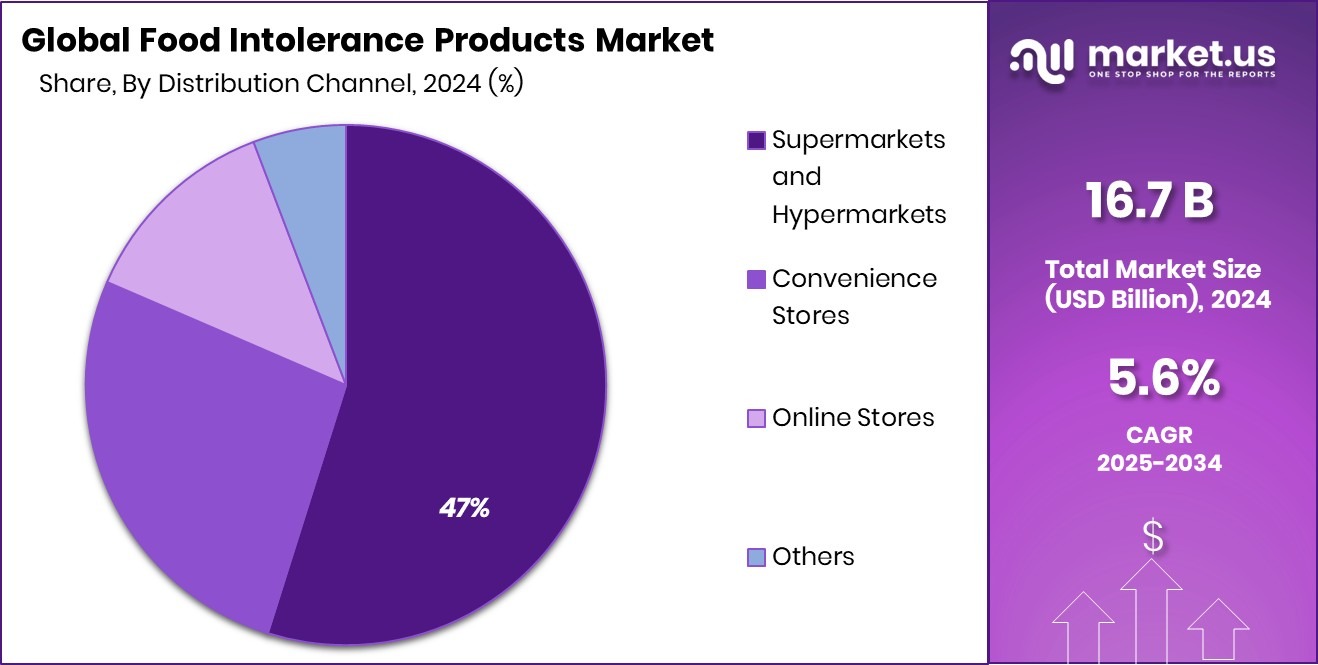

- Supermarkets and Hypermarkets were the leading distribution channel with a 47.4% share in global sales.

- North America leads the Food Intolerance Products Market with 47.3%, reaching USD 7.8 billion.

By Product Type Analysis

Dairy alternatives dominate the food intolerance products market with a 38.1% share in 2024.

In 2024, Dairy Alternatives and Lactose Free Products secured a significant foothold in the Food Intolerance Products Market, boasting a commanding 38.1% market share within the By Product Type segment.

This notable dominance underscores a growing consumer shift towards dietary products that cater to lactose intolerance and other milk-related allergies. The segment’s strength is indicative of a broader trend where health-conscious consumers increasingly opt for alternatives that align with their dietary restrictions and lifestyle choices.

The robust performance of dairy alternatives and lactose-free products is not only a reflection of heightened awareness and diagnosis of food intolerances but also of the improvements in the range and quality of alternatives available. Manufacturers have been keen to innovate in this space, offering a variety of flavorful and nutritionally comparable options to traditional dairy, which has helped in expanding the consumer base.

This segment’s growth is further supported by a well-established distribution network spanning supermarkets, health food stores, and online platforms, ensuring accessibility and convenience for consumers seeking these products.

By Intolerance Type Analysis

The dairy and lactose intolerance category holds a 36.7% share in intolerance-type food products.

In 2024, Dairy and Lactose Intolerance dominated the By Intolerance Type segment of the Food Intolerance Products Market, capturing a substantial 36.7% share. This prominent position reflects the significant prevalence of lactose intolerance among the global population, driving demand for specialized dietary products. As awareness and diagnosis of lactose intolerance have improved, so too has the availability and variety of products designed to meet the needs of this demographic.

The market’s growth is fueled by the increasing number of consumers who are actively seeking out food products that cater to their specific dietary restrictions without sacrificing taste or nutritional value.

This has encouraged food manufacturers to expand their portfolios to include a wide range of lactose-free milk, cheeses, yogurts, and ice cream, among other dairy alternatives. The rise in consumer health consciousness and the trend towards plant-based diets have also played crucial roles in boosting the market segment.

By Category Analysis

Conventional food intolerance products dominate the market, capturing 67.3% share in 2024.

In 2024, the Conventional category held a dominant market position in the By Category segment of the Food Intolerance Products Market, commanding a 67.3% share. This substantial market share underscores the ongoing preference for conventional food intolerance products over their organic counterparts among a majority of consumers. Despite the rising trend towards organic and natural products, conventional offerings remain popular due to their widespread availability and often more affordable pricing.

The dominance of conventional products is further bolstered by established supply chains and extensive distribution networks that ensure easy accessibility for consumers across various retail platforms, including supermarkets, hypermarkets, and online stores. These products cater to a broad audience, offering a variety of options that address specific dietary needs without the premium price tag associated with organic products.

As the market for food intolerance continues to grow, driven by increasing awareness and diagnosis of dietary sensitivities, conventional products are likely to maintain their appeal. They serve as a vital component of the industry, providing cost-effective solutions for consumers seeking relief from food intolerance symptoms while adhering to their budget constraints.

By Distribution Channel Analysis

Supermarkets and hypermarkets lead the distribution channel with a 47.4% share of total sales.

In 2024, Supermarkets and Hypermarkets held a dominant market position in the By Distribution Channel segment of the Food Intolerance Products Market, capturing a significant 47.4% share. This leading position highlights the critical role these retail giants play in the accessibility and distribution of food intolerance products.

The convenience of finding a wide array of specialized food items under one roof, coupled with the advantage of physical product verification and immediate availability, makes supermarkets and hypermarkets a preferred choice for consumers managing food intolerances.

The strategic placement of these products in high-traffic areas and the use of targeted marketing strategies within these outlets have enhanced product visibility and consumer awareness. Additionally, the ability of these retail formats to offer competitive pricing through economies of scale further attracts a large customer base seeking both variety and value.

As consumer demand for specialized dietary products continues to rise, driven by increased awareness of food intolerances and health-conscious lifestyle choices, supermarkets and hypermarkets are expected to remain pivotal in shaping purchasing habits.

Key Market Segments

By Product Type

- Dairy Alternatives and Lactose Free Products

- Bakery Products

- Chocolates and Confectionery

- Meat Alternatives

- Specialized Nutrition

- Snacks and Processed Food

- Condiments and Dressings

By Intolerance Type

- Dairy and Lactose Intolerance

- Sugar Intolerance

- Gluten Intolerance

- Meat Intolerance

- Others

By Category

- Organic

- Conventional

By Distribution Channel

- Supermarkets and Hypermarkets

- Convenience Stores

- Online Stores

- Others

Driving Factors

Rising Awareness Boosts Demand for Intolerance Products

One of the main reasons driving the Food Intolerance Products Market is that more people are becoming aware of food sensitivities and their health impact. With better education, social media awareness, and frequent health check-ups, people now understand the link between diet and digestive issues.

This awareness pushes them to look for safer and suitable alternatives like lactose-free milk, gluten-free bread, and additive-free snacks. Many governments and health organizations also support labeling rules and allergen disclosures, which help consumers make better choices.

As a result, supermarkets and online stores are offering a wider range of such products. This growing consciousness is turning occasional buyers into loyal customers, which fuels long-term growth in the food intolerance sector.

Restraining Factors

High Product Costs Limit Everyday Consumer Access

One big challenge holding back the Food Intolerance Products Market is the high price of these specialized foods. Items like gluten-free flour, lactose-free milk, or nut-free snacks often cost much more than regular products. This price gap makes it hard for middle-income and low-income families to buy them regularly.

While people want to eat healthy, their budgets don’t always allow it. Even in supermarkets, intolerance-friendly products usually sit in premium sections, making them feel like luxury items.

Until production costs go down or more affordable options become available, many consumers might continue to choose cheaper alternatives, even if they don’t suit their health needs. This cost barrier slows down the market’s full growth potential.

Growth Opportunity

Plant-Based Innovations Expand Food Intolerance Choices

A big growth opportunity in the Food Intolerance Products Market is the rise of plant-based innovations. Brands are now using ingredients like oats, rice, almonds, soy, and coconut to create dairy-free, gluten-free, and allergen-free alternatives.

These plant-based products are not only healthier for people with food sensitivities but also appeal to vegans and eco-conscious buyers. For example, oat milk and almond cheese are becoming popular in cafes and grocery stores.

Since plant-based foods are easier to digest and often packed with nutrients, more people are adding them to their diet, even if they don’t have an intolerance. This shift opens new doors for companies to create tasty, affordable, and inclusive products that meet diverse dietary needs.

Latest Trends

Digital Platforms Drive Growth in Intolerance Products

A major trend shaping the Food Intolerance Products Market is the significant expansion of digital platforms. Online shopping has become a preferred method for consumers seeking gluten-free, lactose-free, and allergen-free products, offering convenience and access to a broader range of options.

E-commerce platforms and specialized health food websites provide detailed product information, customer reviews, and personalized recommendations, aiding consumers in making informed choices.

Additionally, social media and online communities have become valuable resources for individuals with food intolerances, facilitating the exchange of recipes, product reviews, and support. This digital shift not only enhances consumer awareness but also enables companies to reach a wider audience, gather feedback, and tailor their offerings to meet specific dietary needs.

Regional Analysis

In North America, Food Intolerance Products captured 47.3%, worth USD 7.8 Bn.

In 2024, North America held a dominant position in the global Food Intolerance Products Market, accounting for 47.3% of the total market share, with a market value of approximately USD 7.8 billion. This dominance is supported by the region’s heightened consumer awareness about food allergies, lactose intolerance, and gluten sensitivities.

Additionally, the availability of a wide range of specialty products in mainstream retail channels like supermarkets and hypermarkets has driven substantial consumer adoption. In Europe, the market is steadily expanding due to growing health consciousness and regulatory support for clean labeling and allergen-free food disclosures.

The Asia Pacific region is witnessing increased traction, primarily driven by rising urbanization, evolving dietary habits, and a growing middle-class population becoming more health-aware. Meanwhile, the Middle East & Africa and Latin America are emerging markets, with gradual growth supported by improving distribution networks and increased product availability.

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

In 2024, Amy’s Kitchen Inc. continued to demonstrate strong brand positioning in the global food intolerance products market by expanding its gluten-free and dairy-free ready meals segment. With a longstanding focus on organic and allergen-free formulations, the company has strengthened its appeal among consumers seeking plant-based and intolerance-friendly options.

In early 2024, Amy’s launched new vegan frozen entrees that excluded major allergens, aligning with the growing demand for simple-label, intolerance-safe foods across North America and Europe. This focus on non-GMO and clean-label manufacturing gives Amy’s a clear edge in consumer trust.

Arla Foods Amba, a dairy cooperative, maintained its momentum by expanding lactose-free dairy offerings in 2024, particularly across Western Europe and parts of Asia. Arla’s innovation strategy included introducing lactose-free protein-enriched yogurts and milk, responding to rising consumer demand for functional yet intolerance-friendly options. In 2024, the company also invested in low-lactose processing technologies to enhance product quality while retaining natural taste, gaining traction in both retail and health-oriented segments.

Chobani LLC made significant strides in 2024 by growing its plant-based and lactose-free yogurt lines. The company’s oat-based and coconut-based alternatives gained strong shelf presence in the U.S. market, targeting dairy-intolerant and vegan consumers alike. Chobani’s emphasis on protein-rich, lactose-free Greek-style yogurts contributed to category growth.

Top Key Players in the Market

- Amys Kitchen Inc.

- Arla Foods Amba

- Chobani LLC

- Dr. Schar

- Ecotone (Mrs. Crimbles Ltd)

- General Mills Inc.

- Hain Celestial Group Inc.

- Oatly Group AB

- Reckitt Benckiser Group Plc

- The Kellogg Company

Recent Developments

- In April 2024, Amy’s Kitchen voluntarily recalled specific batches of its Enchilada Verde Whole Meal due to potential Listeria contamination. The recall was a precautionary measure to ensure consumer safety.

- In April 2025, Arla Foods and Germany’s DMK Group announced their intention to merge, creating Europe’s largest farmer-owned dairy cooperative. The merger will bring together over 12,000 farmers and is expected to generate a combined revenue of €19 billion.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2024) | USD 16.7 Billion |

| Forecast Revenue (2034) | USD 28.8 Billion |

| CAGR (2025-2034) | 5.6% |

| Base Year for Estimation | 2024 |

| Historic Period | 2020-2023 |

| Forecast Period | 2025-2034 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Product Type (Dairy Alternatives and Lactose Free Products, Bakery Products, Chocolates and Confectionary, Meat Alternatives, Specialized Nutrition, Snacks and Processed Food, Condiments and Dressings), By Intolerance Type (Dairy and Lactose Intolerance, Sugar Intolerance, Gluten Intolerance, Meat Intolerance, Others), By Category (Organic, Conventional), By Distribution Channel (Supermarkets and Hypermarkets, Convenience Stores, Online Stores, Others) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – GCC, South Africa, Rest of MEA |

| Competitive Landscape | Amys Kitchen Inc., Arla Foods Amba, Chobani LLC, Dr. Schar, Ecotone (Mrs. Crimbles Ltd), General Mills Inc., Hain Celestial Group Inc., Oatly Group AB, Reckitt Benckiser Group Plc, The Kellogg Company |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |