Quick Navigation

Report Overview

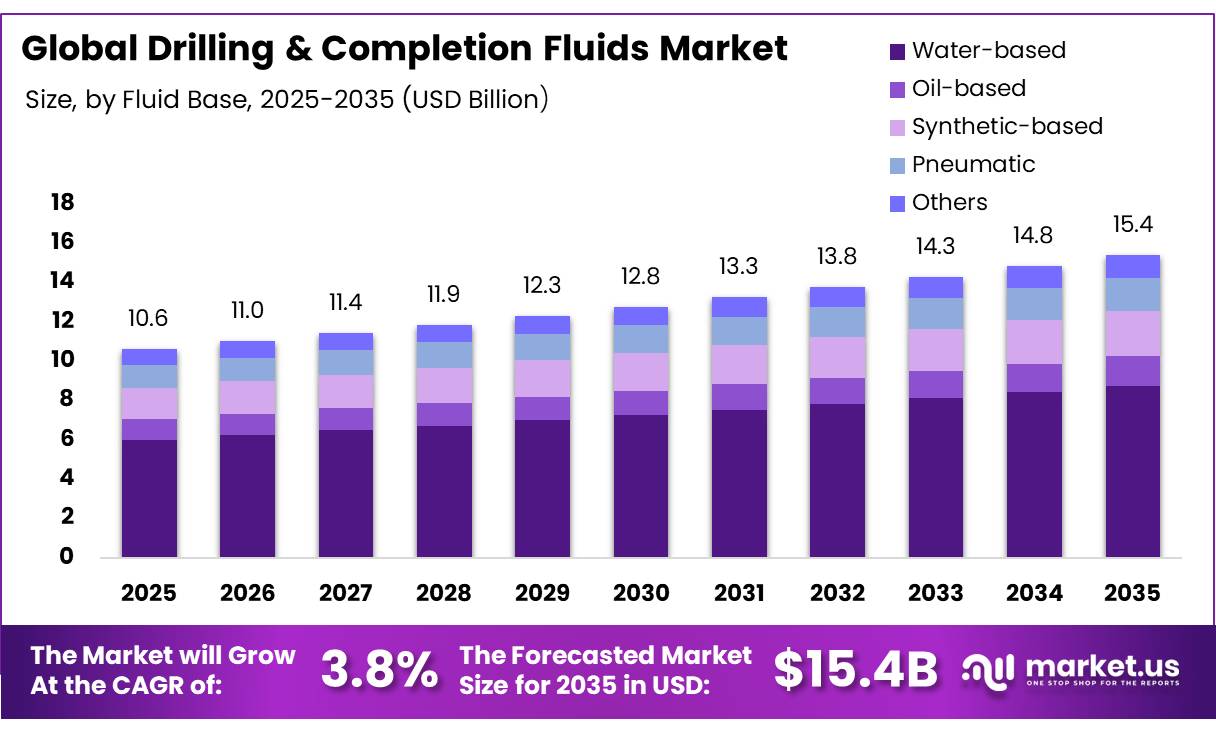

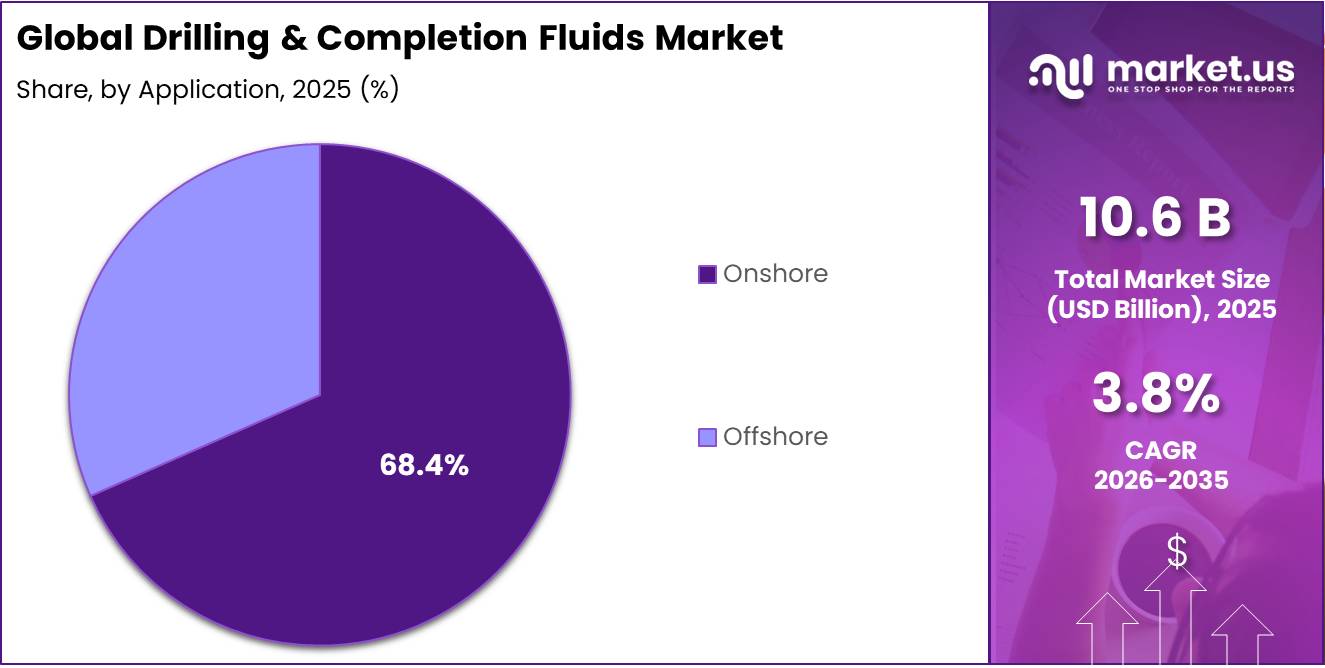

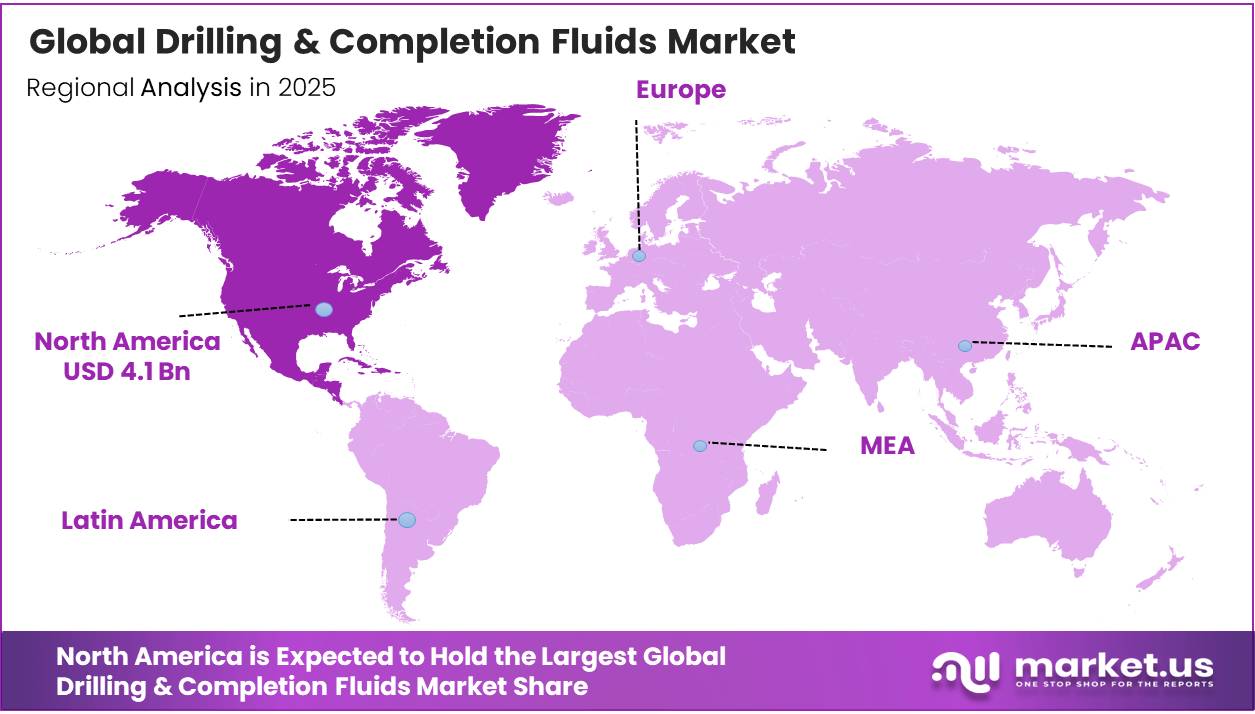

The Global Drilling And Completion Fluids Market size is expected to be worth around USD 15.4 Billion by 2035, from USD 10.6 Billion in 2025, growing at a CAGR of 3.8% during the forecast period from 2026 to 2035. In 2025, North America held a dominant market position, capturing more than a 38.9% share, holding USD 12.5 Billion revenue.

The global drilling & completion fluids market is positioned within a structurally active upstream oil and gas ecosystem, where fluid systems support drilling, well construction, and reservoir preparation across onshore and offshore developments. Demand is closely linked to drilling intensity, particularly in regions where unconventional resources dominate output.

The fluid consumption is strongly influenced by the prevalence of horizontal drilling and multi-stage hydraulic fracturing. In the United States, horizontal wells account for over 90% of oil and gas production in key shale basins, reflecting their critical role in modern extraction methods that require engineered drilling and completion fluids for pressure control and formation stability. The increasing shift toward pad drilling and multi-well completions has further intensified per-well fluid usage and reduced cycle times, reinforcing steady consumption patterns across shale plays.

The onshore activity remains dominant globally, accounting for roughly two-thirds of drilling operations, supported by lower costs and widespread unconventional development. Water-based fluids maintain the largest share by formulation type, commonly exceeding 50% of total usage, due to regulatory acceptance and cost efficiency in conventional and shallow drilling environments.

- In the US, horizontal wells increased from 10% in 2014 to 22% in 2024. Since 2018, over two-thirds of production has come from wells producing 100-3,200 BOE/d, while about 78-80% of wells consistently produce 15 BOE/d or less, reflecting a highly distributed production structure across more than 22 output categories.

Regionally, North America leads consumption, driven by prolific shale basins such as the Permian, Bakken, and Eagle Ford, alongside offshore Gulf of Mexico developments requiring high-performance synthetic systems for HPHT conditions. Meanwhile, offshore deepwater projects increasingly rely on advanced fluid chemistries to manage extreme pressure-temperature environments, reinforcing the market’s shift toward higher-specification formulations.

- According to the U.S. Bureau of Ocean Energy Management (BOEM), deepwater fields, defined as water depths greater than 1,000 feet, account for approximately 94% of Gulf of Mexico crude oil production and nearly 80% of natural gas output, underscoring the structural importance of deepwater operations in U.S. offshore supply chains.

Key Takeaways

- The global drilling & completion fluids market was valued at US$10.6 billion in 2025.

- The global drilling & completion fluids market is projected to grow at a CAGR of 3.8% and is estimated to reach US$15.4 billion by 2035.

- On the basis of fluid base, water-based drilling & completion fluids dominated the market, constituting 56.7% of the total market share.

- Based on the drilling stage, drilling fluids dominated the drilling & completion fluids market, with a substantial market share of around 68.3%.

- Based on the well type, conventional wells led the market, comprising 65.9% of the total market.

- Among the applications of drilling & completion fluids, onshore applications held a major share in the market, 68.4% of the market share.

- In 2025, North America was the most dominant region in the drilling & completion fluids market, accounting for 38.9% of the total global consumption.

Fluid Base Analysis

Rice Cakes are a Prominent Segment in the Drilling & Completion Fluids Market.

Water-based fluids hold the leading share of the global drilling & completion fluids market, accounting for 56.70% of total demand. Their dominance is largely driven by cost efficiency, ease of handling, and broad applicability across conventional drilling operations. These systems are widely used in onshore projects and less complex well conditions, where high-performance alternatives are not essential.

A significant advantage of water-based fluids lies in their relatively lower environmental impact. With tightening regulations around fluid disposal and toxicity, operators are increasingly favoring solutions that align with environmental compliance requirements. This has further strengthened their adoption across both mature and emerging markets.

Ongoing improvements in additive technologies have further enhanced their performance, enabling better wellbore stability and lubrication. Combined with lower operational costs, these factors continue to support the strong position of water-based fluids in the market.

Drilling Stage Analysis

Drilling Fluids Dominated the Drilling & Completion Fluids Market.

Drilling fluids represent the dominant segment in the global drilling & completion fluids market, accounting for 68.30% of total demand. Their leading position is attributed to their critical role throughout the well construction process, where they are essential for maintaining wellbore stability, controlling formation pressure, and transporting drill cuttings to the surface. These functions make drilling fluids indispensable across all well types, from conventional to unconventional, and across both onshore and offshore operations.

The high consumption volume of drilling fluids compared to completion and work-over fluids further reinforces their market dominance. Each drilling operation requires continuous circulation and replenishment of fluids, leading to sustained demand over the drilling lifecycle. Additionally, increasing well complexity, including deeper wells and challenging geological formations, has driven the need for advanced drilling fluid systems with enhanced performance characteristics. This ongoing evolution in drilling practices continues to support the strong share of the drilling fluids segment in the market.

Well Type Analysis

Drilling & Completion Fluids Products Are Mostly Utilized in the Conventional Wells.

Conventional wells account for the largest share of the global drilling & completion fluids market, representing 65.90% of total demand. Their dominance is primarily driven by the extensive number of mature oil and gas fields that continue to be actively developed and maintained across key producing regions. These wells typically involve less complex geological formations, allowing for the widespread use of cost-effective fluid systems, particularly water-based fluids.

The relatively lower operational and technical challenges associated with conventional wells contribute to their continued preference among operators, especially in regions with established infrastructure and stable production profiles. Additionally, ongoing investments in brownfield developments and enhanced oil recovery (EOR) projects further sustain demand for drilling and completion fluids in this segment.

Despite the growing focus on unconventional resources, conventional wells remain a stable and consistent contributor to market demand due to their lower risk profile, predictable output, and economic viability in a wide range of oil price scenarios.

Application Analysis

Onshore Applications Held a Major Share of the Drilling & Completion Fluids Market.

The onshore segment accounts for the largest share of the global drilling & completion fluids market, representing 68.40% of total demand. This dominance is primarily supported by the higher volume of drilling activities conducted on land-based oil and gas fields, which continue to serve as the backbone of global hydrocarbon production. Onshore operations generally involve lower capital expenditure and shorter project cycles compared to offshore developments, making them more economically viable for a wide range of operators.

The extensive presence of mature oilfields, particularly in regions with established petroleum infrastructure, further sustains the demand for drilling and completion fluids in onshore applications. These projects often require continuous drilling, work-over, and well maintenance activities, ensuring steady consumption of fluid systems throughout the well lifecycle.

Additionally, the expansion of unconventional resource development, such as shale and tight oil formations, is heavily concentrated in onshore basins. This has further reinforced the segment’s dominance, as these operations require significant volumes of specialized drilling fluids to support complex drilling techniques.

Key Market Segments

By Fluid Base

- Water-based

- Oil-based

- Synthetic-based

- Pneumatic

- Others

By Drilling Stage

- Drilling Fluids

- Completion and Work-over Fluids

By Well Type

- Conventional

- Unconventional

By Application

- Onshore

- Offshore

Drivers

Rising Complexity in Unconventional Wells Driving Adoption of Specialized Drilling & Completion Fluids.

Rising unconventional resource development and increasing drilling complexity are structurally elevating demand intensity for drilling & completion fluid systems due to higher well counts, extended lateral drilling, and more demanding reservoir conditions.

- According to the U.S. Energy Information Administration (EIA), horizontal wells accounted for about 94% of oil production and 92% of natural gas production in the Lower 48 states by December 2024, reflecting their dominance in shale and tight formations where advanced fluid systems are essential for hydraulic fracturing and wellbore stability.

The production behavior in these wells shows rapid decline profiles, requiring continuous drilling activity. The EIA data indicates that output from older wells fell by 4.3 million barrels per day between December 2023 and 2024, necessitating more than 15,000 new wells in 2024 to offset declines. This cycle directly increases consumption of drilling fluids, as each new well requires substantial volumes during drilling and completion stages.

Horizontal drilling in shale formations enables significantly greater reservoir contact, and by 2018, horizontal wells accounted for nearly all production in key shale plays such as the Marcellus, reaching about 99% of output in that basin. This shift has been accompanied by longer lateral sections, multi-stage hydraulic fracturing, and high-density well pad development, all of which require fluid systems with enhanced rheological control, shale inhibition, and thermal stability.

Restraints

Stringent Environmental Regulations Limiting the Adoption of Conventional Drilling & Completion Fluids.

Stringent environmental regulations governing drilling and completion activities are increasingly influencing operational flexibility and fluid selection strategies across upstream projects. Regulatory frameworks such as the U.S. EPA’s Oil and Gas Extraction Effluent Guidelines (40 CFR Part 435) impose discharge restrictions on drilling fluids, drill cuttings, and completion-related waste streams, with offshore discharges of non-aqueous drilling fluids and associated cuttings prohibited in multiple operating zones, while water-based systems are also subject to strict zero-discharge requirements in specific offshore categories under defined conditions.

Drilling and completion fluids are explicitly classified as regulated wastewater constituents under these guidelines, requiring operators to manage fluid recovery, treatment, and disposal within permitted limits across onshore and offshore facilities. The requirement for National Pollutant Discharge Elimination System (NPDES) permitting further adds compliance complexity, as operators must continuously demonstrate adherence to pollutant thresholds and waste handling protocols, particularly for oil and grease content and residual chemical additives.

- According to the US EIA, the number of producing wells peaked at 1,031,161 in 2014, declining to 930,445 in 2023 and further to 918,481 in 2024.

In unconventional extraction, wastewater streams often contain high total dissolved solids (TDS), organic compounds, metals, and naturally occurring radioactive materials (TENORM), necessitating advanced treatment or reinjection practices rather than direct discharge. This increases reliance on closed-loop mud systems and cuttings reinjection, raising operational complexity and reducing flexibility in fluid management.

The regulatory push toward reduced offshore discharge has further accelerated substitution toward lower-toxicity water-based and synthetic-based formulations, but these alternatives require higher chemical engineering input and cost-intensive compliance validation. Consequently, operators face increased operational burden in maintaining performance standards while meeting tightening environmental thresholds, particularly in deepwater and environmentally sensitive regions where enforcement intensity is highest.

Opportunities

Expanding Offshore and Deepwater Activities Unlocking New Avenues for Drilling & Completion Fluids.

The expansion of offshore and deepwater oil and gas activities is creating sustained demand growth opportunities for drilling & completion fluid systems, driven by the technical intensity and scale of subsea developments.

- In the Gulf of Mexico alone, over 2,300 active oil and gas leases span approximately 12.5 million acres of federal offshore acreage, with most concentrated in the Central Planning Area, supporting continuous exploration and development activity.

The region remains the primary offshore hydrocarbon hub for the United States, with deepwater production contributing the majority of offshore output for more than a decade, reflecting sustained utilization of high-specification drilling and completion fluids designed for HPHT and ultra-deepwater conditions. The deepwater wells often require mobile offshore drilling units such as drillships and semisubmersibles capable of operating in water depths exceeding 7,500 feet, where fluid systems must maintain stability under extreme pressure differentials and low-temperature seabed conditions.

Recent offshore project developments, including large-scale floating production systems and multi-well deepwater hubs, indicate continued investment in complex offshore architectures. These developments inherently require advanced synthetic-based and engineered water-based fluid systems, reinforcing long-cycle demand visibility for high-performance drilling and completion fluid technologies in offshore environments.

Trends

Shift Toward Environmentally Sustainable Drilling & Completion Fluid Systems.

The shift toward environmentally sustainable drilling & completion fluid systems is increasingly shaped by toxicity thresholds, and waste handling practices across onshore and offshore operations.

In the United States, the EPA’s Oil and Gas Extraction Effluent Guidelines (40 CFR Part 435) regulate wastewater discharges from drilling, well completion, and production activities under the National Pollutant Discharge Elimination System (NPDES), including restrictions on synthetic-based and oil-based fluid discharges in specific offshore contexts.

Similarly, offshore rules applied beyond three miles from shore have historically limited pollutant releases, contributing to controlled adoption of alternative fluid systems in sensitive marine zones. Furthermore, there is an ongoing substitution of conventional oil-based systems with modified synthetic and enhanced water-based formulations designed to meet biodegradability and inhibition requirements in complex wells.

Moreover, offshore developments, particularly in deepwater basins, are driving higher adoption of advanced water-based and low-toxicity synthetic systems due to stricter marine ecosystem protections. At the same time, additive innovation, including nano-enhanced lubricants and low-toxicity inhibitors, is improving water-based fluid performance, narrowing the gap with oil-based alternatives and reinforcing their suitability in extended-reach and unconventional drilling applications.

Geopolitical Impact Analysis

Geopolitical Volatility Reshaping Upstream Activity Patterns and Supply Dynamics in the Drilling & Completion Fluids Market.

Geopolitical tensions have increasingly acted as a structural volatility trigger for the drilling & completion fluids market by influencing upstream investment cycles, supply chain continuity, and operational intensity across key producing regions. Episodes of conflict in the Middle East have demonstrated measurable impacts on crude benchmarks, with Brent crude briefly exceeding the US$100 per barrel level during periods of heightened disruption risk and shipping constraints through strategic chokepoints such as the Strait of Hormuz, which carries roughly one-fifth of global seaborne oil flows. Such price spikes typically prompt short-term adjustments in exploration and production activity, directly affecting demand for drilling fluids used in well construction and completion operations.

Sanctions on major producing nations, particularly Russia, have reconfigured global supply chains for oilfield services and critical inputs such as specialty chemicals and additives used in synthetic and oil-based fluid systems. Russia drilled 7,610 production wells in 2024, while U.S. activity remained significantly higher at approximately 15,000 wells, reflecting uneven drilling continuity across sanctioned and non-sanctioned regions.

Trade redirections, including Russia’s reported shift of over 80% of crude exports toward Asian markets, have further altered logistics flows, increasing transportation distances and influencing offshore and deepwater drilling demand in alternative supply regions.

Similarly, geopolitical disruptions have contributed to cost inflation in upstream services, with offshore vessel day rates and subsea equipment costs rising amid constrained availability and higher risk premiums. These conditions have reinforced preference for high-performance drilling and completion fluids capable of supporting complex HPHT and deepwater wells, while encouraging inventory pre-positioning and localized blending strategies to mitigate supply chain exposure.

Regional Analysis

North America Accounting for the Highest Share in the Global Drilling & Completion Fluids Market.

North America holds the largest share of the global drilling & completion fluids market, accounting for 38.90% of total demand. This dominance is primarily supported by the region’s strong upstream oil and gas activity, particularly in the United States, where large-scale shale development and tight oil extraction continue to drive extensive drilling operations. The widespread adoption of horizontal drilling and hydraulic fracturing techniques has significantly increased the consumption of advanced drilling and completion fluid systems across key basins.

- According to U.S. Energy Information Administration (EIA) data, the United States produced approximately 13.3-13.4 million barrels per day of crude oil in 2023-2024, while natural gas production rose from 128.0 billion cubic feet per day in December 2023 to 128.8 billion cubic feet per day in December 2024, reflecting sustained high drilling activity across major producing basins such as the Permian, Bakken, and Eagle Ford formations.

The region benefits from highly developed oilfield services infrastructure and the presence of major industry participants, enabling efficient deployment of technologically advanced fluid solutions. Similarly, continuous investment in unconventional resource development, especially in shale plays, further reinforces demand stability. These combined factors ensure North America’s leading position in the global market landscape.

Key Regions and Countries

- North America

- The US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia & CIS

- Rest of Europe

- APAC

- China

- Japan

- South Korea

- India

- ASEAN

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

Manufacturers of drilling & completion fluids focus on strengthening technical differentiation through continuous formulation innovation tailored to complex well conditions such as high-pressure, high-temperature environments and unconventional reservoirs. A strong emphasis is placed on developing environmentally compliant fluid systems with lower toxicity, improved biodegradability, and reduced waste generation to align with tightening regulatory expectations across key operating regions.

Companies further invest in advanced additive chemistries that enhance wellbore stability, lubricity, and drilling efficiency, helping operators reduce non-productive time. Strategic collaboration with exploration and production companies enables customized fluid solutions based on basin-specific geology and operational requirements. Additionally, manufacturers are strengthening global supply chains and establishing regional blending and service facilities to ensure faster delivery, cost efficiency, and improved responsiveness to localized demand conditions.

The Major Players in The Industry

- Baker Hughes Company

- Schlumberger Limited

- Halliburton Company

- Weatherford International plc

- Newpark Resources Inc.

- TETRA Technologies Inc.

- National Oilwell Varco Inc.

- CES Energy Solutions Corp.

- Chevron Phillips Chemical Co. LLC

- M-I SWACO

- Scomi Energy Services Bhd

- AES Drilling Fluids LLC

- Anchor Drilling Fluids USA

- Flotek Industries Inc.

- Gumpro Drilling Fluids Pvt. Ltd.

- Oilfield Chemical Co. Baker Petrolite

- Petrochem Performance Chemicals Ltd.

- Q’Max Solutions Inc.

- IMDEX Limited

- Valence Drilling Fluids LLC

- Other Key Players

Key Development

- In November 2024, Baker Hughes opened a new liquid mud plant to support expansion in the Namibian region, featuring capacity for drilling and completion fluids, cementing, and multi-modal facilities.

- In September 2025, IMS and Newpark Fluids Systems are pleased to announce a strategic collaboration agreement to deliver cutting-edge, real-time drilling fluids measurement and analysis solutions to customers worldwide.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | US$10.6 Bn |

| Forecast Revenue (2035) | US$15.4 Bn |

| CAGR (2026-2035) | 3.8% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Fluid Base (Water-based, Oil-based, Synthetic-based, Pneumatic, and Others), By Drilling Stage (Drilling Fluids and Completion and Work-over Fluids), By Well Type (Conventional and Unconventional), By Application (Onshore and Offshore) |

| Regional Analysis | North America – The US & Canada; Europe – Germany, France, The UK, Spain, Italy, Russia & CIS, Rest of Europe; APAC– China, Japan, South Korea, India, ASEAN & Rest of APAC; Latin America– Brazil, Mexico & Rest of Latin America; Middle East & Africa– GCC, South Africa, & Rest of MEA |

| Competitive Landscape | Baker Hughes Company, Schlumberger Limited, Halliburton Company, Weatherford International plc, Newpark Resources Inc., TETRA Technologies Inc., National Oilwell Varco Inc., CES Energy Solutions Corp., Chevron Phillips Chemical Co. LLC, M-I SWACO, Scomi Energy Services Bhd, AES Drilling Fluids LLC, Anchor Drilling Fluids USA, Flotek Industries Inc., Gumpro Drilling Fluids Pvt. Ltd., Oilfield Chemical Co.. Baker Petrolite, Petrochem Performance Chemicals Ltd., Q’Max Solutions Inc., IMDEX Limited, Valence Drilling Fluids LLC, and Other Players. |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited Users and Printable PDF) |