Quick Navigation

Report Overview

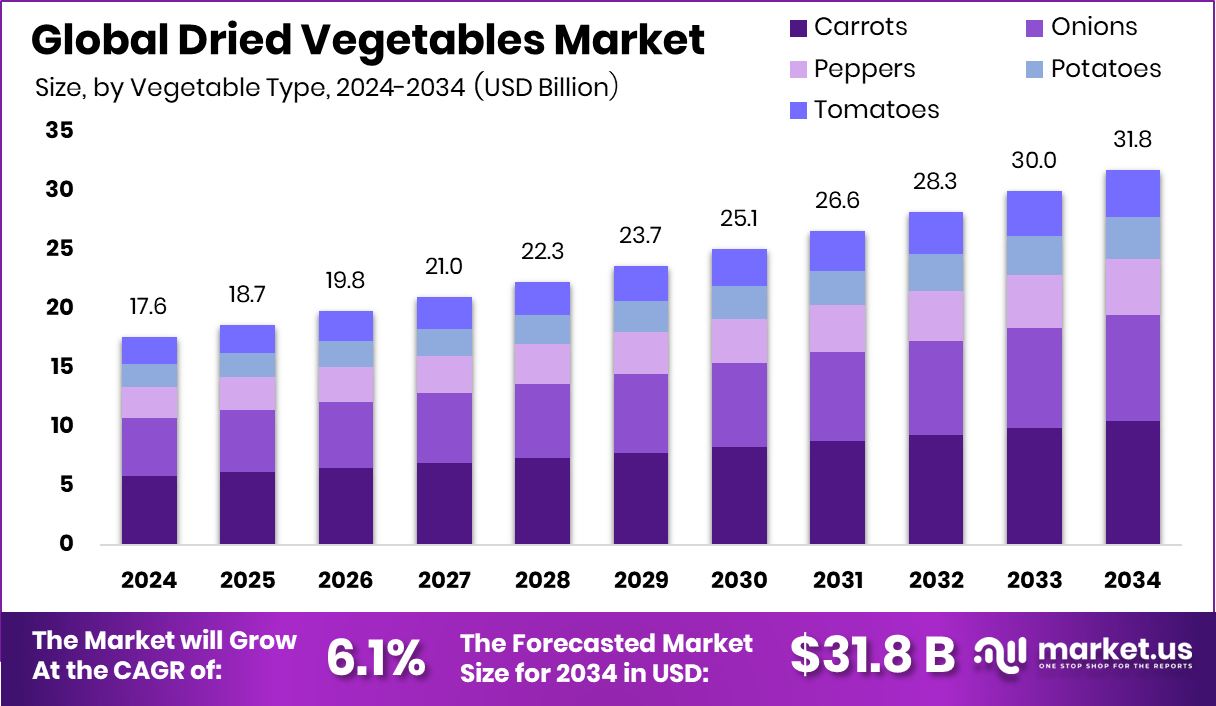

Global Dried Vegetables Market is expected to be worth around USD 31.8 billion by 2034, up from USD 17.6 billion in 2024, and grow at a CAGR of 6.1% from 2025 to 2034. North America’s strong processed food demand supports 47.9% dried vegetables market dominance.

Dried vegetables are fresh vegetables that have undergone a dehydration process to remove most of their water content while preserving their flavor, texture, and nutrients. This method increases shelf life and reduces storage and transportation costs. Common drying methods include air drying, freeze drying, and sun drying. Dried vegetables can be easily rehydrated in cooking and are widely used in soups, noodles, ready meals, and snack products.

The dried vegetables market consists of the production, distribution, and consumption of vegetables that have been preserved through dehydration techniques. This market serves multiple sectors, including food processing, HoReCa (Hotels, Restaurants, Catering), military rations, and emergency food supplies. Growth is driven by increased demand for shelf-stable and convenient food ingredients, especially in urban areas.

Urbanization and busy lifestyles are key growth drivers for the dried vegetables market. Consumers are seeking foods that are easy to store, prepare, and cook without compromising on nutrition. Dehydrated vegetables offer a solution by maintaining nutritional integrity and saving preparation time. Additionally, rising awareness around food waste reduction is prompting food manufacturers to adopt drying methods to preserve surplus harvests, further boosting market growth.

Demand for dried vegetables is rising in both developed and developing countries due to changing dietary preferences. In regions with limited refrigeration or seasonal access to fresh produce, dried vegetables serve as a practical alternative. The expanding ready-to-eat and instant meal segments are also significantly contributing to demand, particularly among younger consumers, office workers, and outdoor travelers who prioritize portability and ease of use.

Key Takeaways

- Global Dried Vegetables Market is expected to be worth around USD 31.8 billion by 2034, up from USD 17.6 billion in 2024, and grow at a CAGR of 6.1% from 2025 to 2034.

- In the Dried Vegetables Market, Carrots held a 32.9% share in the Vegetable Type segment.

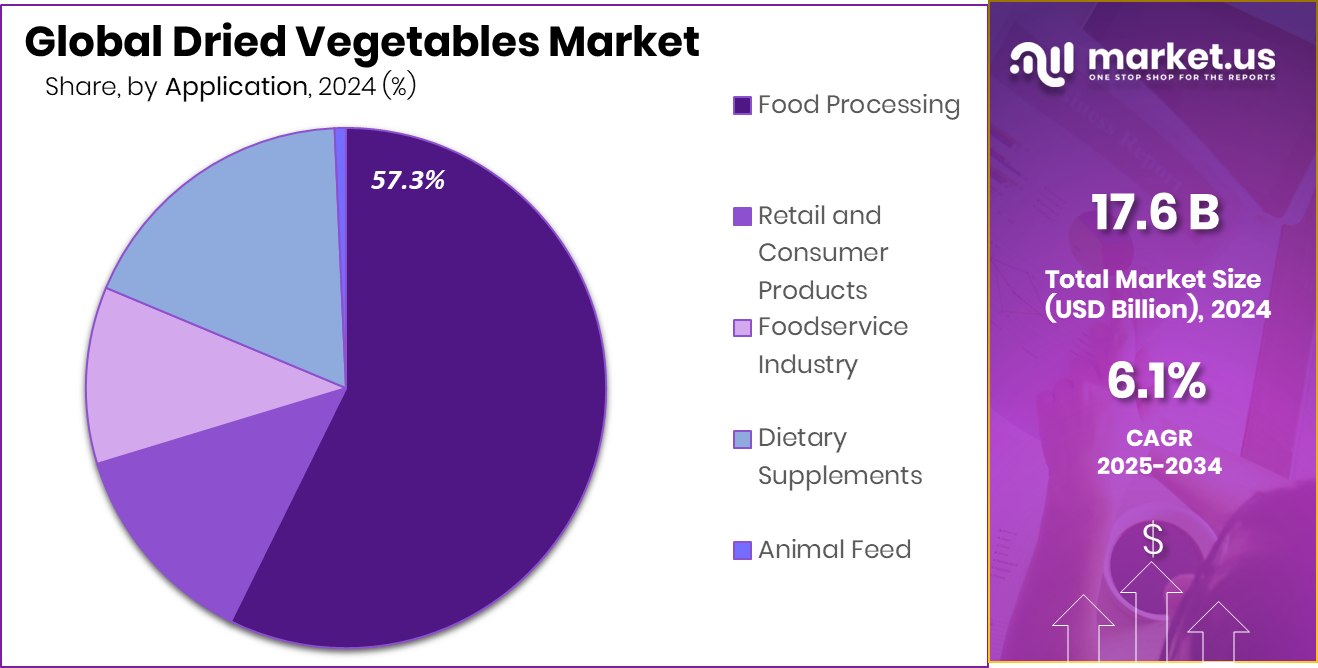

- Food processing dominated the dried vegetables market application segment with a 57.3% share in 2024.

- Supermarkets and Hypermarkets accounted for a 42.9% share in the Distribution Channel of the Dried Vegetables Market.

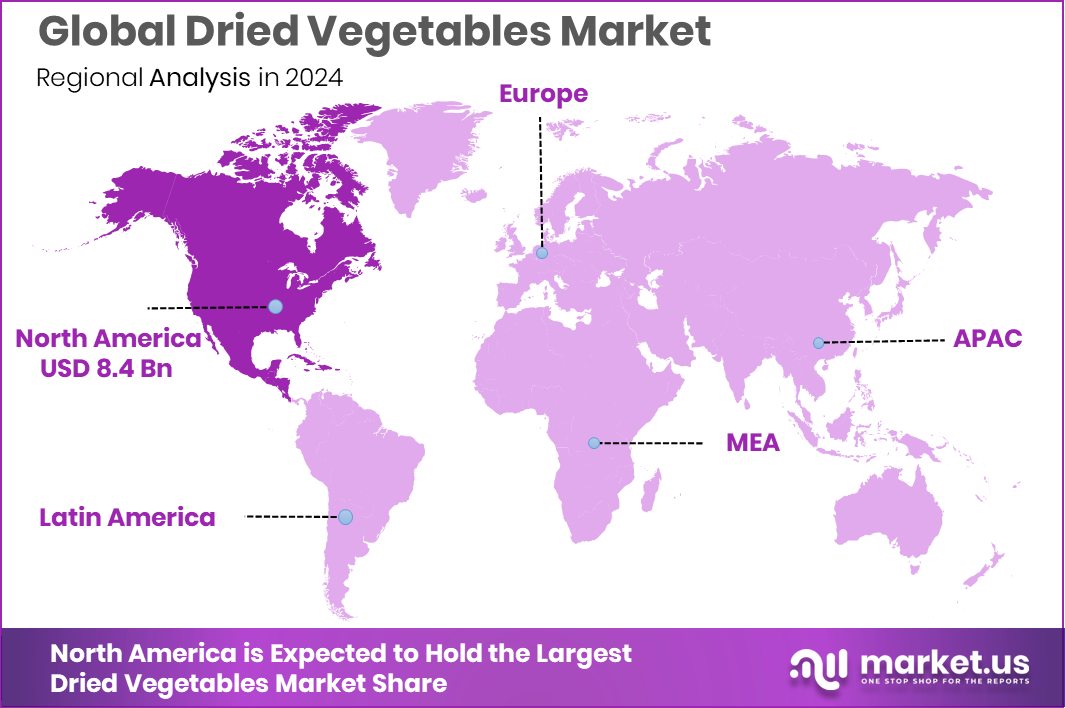

- The dried vegetables market in North America reached USD 8.4 Bn in 2024.

By Vegetable Type Analysis

In 2024, carrots led the dried vegetables market with a 32.9% share.

In 2024, Carrots held a dominant market position in the By Vegetable Type segment of the Dried Vegetables Market, with a 32.9% share. This dominance reflects the widespread usage of dried carrots across various food applications, including instant soups, ready-to-eat meals, and dehydrated food mixes.

Carrots are preferred in the dried form due to their rich color, sweetness, and high content of beta-carotene, which remains relatively stable during the drying process. Their versatility makes them a key ingredient for food manufacturers aiming to enhance flavor, texture, and nutritional value without using artificial additives.

The long shelf life and lightweight nature of dried carrots also support their demand in sectors such as military rations, outdoor meal kits, and emergency food supplies. Moreover, the cost-effectiveness of processing carrots, along with their year-round availability and minimal spoilage during dehydration, makes them a commercially viable choice for bulk production.

With growing consumer preference for natural ingredients and convenience-driven cooking solutions, dried carrots continue to maintain a strong foothold in the global market.

By Application Analysis

Food processing held a 57.3% share in the dried vegetables market in 2024.

In 2024, Food Processing held a dominant market position in the By Application segment of the Dried Vegetables Market, with a 57.3% share. This substantial share underscores the widespread incorporation of dried vegetables in packaged and processed food products such as instant noodles, ready meals, soups, sauces, and snack mixes.

Food manufacturers prefer dried vegetables due to their extended shelf life, consistent quality, and ability to retain flavor and nutrients post-rehydration. The convenience of using pre-dried ingredients helps reduce preparation time and operational costs in high-volume production environments. Additionally, dried vegetables eliminate the need for cold storage and simplify global distribution, supporting efficient supply chain management.

Their utility in creating clean-label and preservative-free products also aligns with consumer demand for healthier and natural food options. The food processing industry continues to scale up production of frozen and ambient packaged foods, further reinforcing demand for dehydrated ingredients like carrots, peas, and onions.

By Distribution Channel Analysis

Supermarkets and hypermarkets dominated distribution with a 42.9% share in 2024.

In 2024, Supermarkets and Hypermarkets held a dominant market position in the By Distribution Channel segment of the Dried Vegetables Market, with a 42.9% share. This leading position reflects the strong consumer preference for purchasing packaged dried vegetables through organized retail outlets offering variety, convenience, and immediate product availability.

Supermarkets and hypermarkets serve as primary points of sale for both branded and private-label dried vegetable products, allowing consumers to compare options based on packaging, quality, and pricing. These retail formats also provide visibility for new product launches, promotional campaigns, and in-store sampling, which influence consumer buying behavior.

The organized layout, wide shelf space, and availability of multiple SKUs in these stores enable easier access to dried carrots, peas, onions, and mixed vegetable packs in various forms such as flakes, powders, and granules. Bulk discounts, combo offers, and loyalty schemes further attract price-sensitive buyers, supporting high-volume sales.

As urbanization and modern retail infrastructure expand in emerging economies, supermarkets and hypermarkets continue to serve as the preferred distribution channel for convenience foods, including dried vegetables.

Key Market Segments

By Vegetable Type

- Carrots

- Onions

- Peppers

- Potatoes

- Tomatoes

By Application

- Food Processing

- Retail and Consumer Products

- Foodservice Industry

- Dietary Supplements

- Animal Feed

By Distribution Channel

- Supermarkets and Hypermarkets

- Online Retail

- Specialty Stores

- Foodservice Providers

- Others

Driving Factors

Rising Demand for Convenient and Shelf-Stable Foods

One of the main driving factors of the dried vegetables market is the growing consumer need for convenient and long-lasting food options. With more people living in cities and leading busy lifestyles, there’s less time for cooking fresh vegetables every day. Dried vegetables offer a solution—they are lightweight, easy to store, quick to prepare, and do not spoil easily.

Whether used in instant noodles, soups, ready meals, or backpacking kits, these vegetables help save time without losing flavor or nutrients. Their longer shelf life also reduces food waste at home. This demand for convenience, combined with rising interest in clean-label ingredients, is strongly supporting market growth across both developed and developing regions.

Restraining Factors

Loss of Fresh Taste and Texture Quality

One major factor that slows down the growth of the dried vegetables market is the noticeable change in taste and texture after drying. While drying helps keep vegetables usable for longer, the process can affect their original flavor, crispness, and appearance. Many consumers still prefer the natural taste and crunch of fresh vegetables, especially in home-cooked meals.

Dried vegetables may become too soft or bland once rehydrated, which can reduce their appeal in certain recipes. This hesitation is stronger in regions where fresh produce is easily available year-round. As a result, the preference for fresh vegetables over dried ones continues to be a major challenge, particularly in markets where freshness is closely linked to food quality.

Growth Opportunity

Growing Popularity of Plant-Based Diets Globally

The increasing global shift towards plant-based diets presents a significant growth opportunity for the dried vegetables market. As more consumers seek healthier and more sustainable food options, dried vegetables offer a convenient and nutritious alternative to fresh produce. They retain essential nutrients and have a longer shelf life, making them ideal for individuals aiming to incorporate more plant-based foods into their diets without the concern of rapid spoilage.

This trend is further supported by the rise in vegetarian and vegan lifestyles, as well as flexitarian diets, where people reduce meat consumption in favor of plant-based alternatives. The versatility of dried vegetables allows them to be used in a variety of dishes, from soups and stews to snacks and meal replacements, catering to the diverse needs of health-conscious consumers worldwide.

As awareness of the benefits of plant-based eating continues to grow, the demand for dried vegetables is expected to rise, offering manufacturers and retailers a promising avenue for expansion in the global food market.

Latest Trends

Innovations in Drying Techniques Enhance Quality

A significant trend in the dried vegetables market is the adoption of advanced drying technologies aimed at preserving the nutritional value, flavor, and texture of vegetables. Traditional drying methods often compromise the quality of the final product, leading to a loss of essential nutrients and altered taste.

However, modern techniques like freeze-drying and vacuum drying have revolutionized the industry by maintaining the integrity of vegetables during the dehydration process. These methods remove moisture efficiently while preserving the original characteristics of the vegetables, resulting in products that closely resemble their fresh counterparts.

The improved quality has increased consumer acceptance and demand for dried vegetables, especially among health-conscious individuals seeking convenient yet nutritious food options. Furthermore, these innovations have expanded the application of dried vegetables in various culinary uses, including ready-to-eat meals, soups, and snacks, thereby driving market growth and encouraging manufacturers to invest in cutting-edge drying technologies.

Regional Analysis

In 2024, North America held a 47.9% share of the dried vegetables market value.

In 2024, North America emerged as the leading region in the global dried vegetables market, capturing a dominant 47.9% share, equivalent to USD 8.4 billion in market value. The region’s strong position is primarily driven by high consumption of processed and convenience foods, along with widespread availability of packaged dried vegetable products across retail chains.

The growing preference for shelf-stable and ready-to-use ingredients among busy urban households and food manufacturers further supports this regional dominance. In Europe, market growth is sustained by increasing demand for clean-label and preservative-free food products, as consumers become more health-conscious and environmentally aware. Asia Pacific shows steady development, fueled by a rising middle-class population and expanding urban centers, which are boosting demand for dehydrated foods in both domestic and export markets.

Meanwhile, the Middle East & Africa and Latin America regions are witnessing gradual adoption, supported by advancements in food preservation technologies and expanding retail networks. However, North America remains the key revenue contributor in 2024, with its robust food processing industry and consistent consumer demand for long shelf-life, nutritious vegetables reinforcing its leadership in the global dried vegetables market landscape.

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

BCFoods continued to strengthen its global footprint by emphasizing food safety and quality. Their partnership with Agri-Neo introduced the Neo-Pure Pasteurized (NPP) technology in China, setting new standards for food safety in the dehydrated vegetable and spice market. This collaboration not only enhanced BCFoods’ product safety but also reinforced its commitment to delivering high-quality ingredients to its global clientele.

Eurocebollas, based in Spain, maintained its reputation for producing high-quality dehydrated onions. Their focus on sustainable farming practices and advanced dehydration techniques ensured a consistent supply of flavorful and long-lasting products. By catering to both domestic and international markets, Eurocebollas solidified its position as a reliable supplier in the European dried vegetables sector.

Garlico Industries, headquartered in Indore, India, showcased significant growth by expanding its range of dehydrated vegetable powders and flakes. Their emphasis on research and development led to the introduction of innovative products that met the evolving needs of the food processing industry. Garlico’s commitment to quality and customer satisfaction enabled it to strengthen its presence in both national and international markets.

Top Key Players in the Market

- BCFoods

- Eurocebollas

- Garlico Industries

- Jain Irrigation Systems

- Jaworski

- Kanghua

- Natural Dehydrated Vegetables

- Olam International

- Richfield

- Silva International

Recent Developments

- In May 2025, Olam Food Ingredients (OFI), a subsidiary of Olam Group, inaugurated a new instant coffee manufacturing facility in Linhares, Espírito Santo, Brazil. The facility focuses on producing premium instant coffee products using sustainable methods, including renewable energy sources. While this development is in the coffee sector, it showcases Olam’s commitment to sustainability, which may influence its operations in other areas, including dried vegetables.

- In January 2024, Silva International expanded its services to include product concept development. This initiative aims to assist clients in creating new food products by leveraging Silva’s expertise in dried ingredients.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2024) | USD 17.6 Billion |

| Forecast Revenue (2034) | USD 31.8 Billion |

| CAGR (2025-2034) | 6.1% |

| Base Year for Estimation | 2024 |

| Historic Period | 2020-2023 |

| Forecast Period | 2025-2034 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Vegetable Type (Carrots, Onions, Peppers, Potatoes, Tomatoes), By Application (Food Processing, Retail and Consumer Products, Foodservice Industry, Dietary Supplements, Animal Feed), By Distribution Channel (Supermarkets and Hypermarkets, Online Retail, Specialty Stores, Foodservice Providers, Others) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – GCC, South Africa, Rest of MEA |

| Competitive Landscape | BCFoods, Eurocebollas, Garlico Industries, Jain Irrigation Systems, Jaworski, Kanghua, Natural Dehydrated Vegetables, Olam International, Richfield, Silva International |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |