Global Cereal Ingredients Market Size, Share, And Industry Analysis Report By Type (Wheat, Rice, Barley, Oats, Others), By Source (Organic, Conventional), By Form (Flakes, Puff, Others), By Application (Food and Beverages, Animal Feed, Others), By Region and Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Statistics, Trends and Forecast 2026-2035

- Published date: March 2026

- Report ID: 182091

- Number of Pages: 346

- Format:

-

keyboard_arrow_up

Quick Navigation

Report Overview

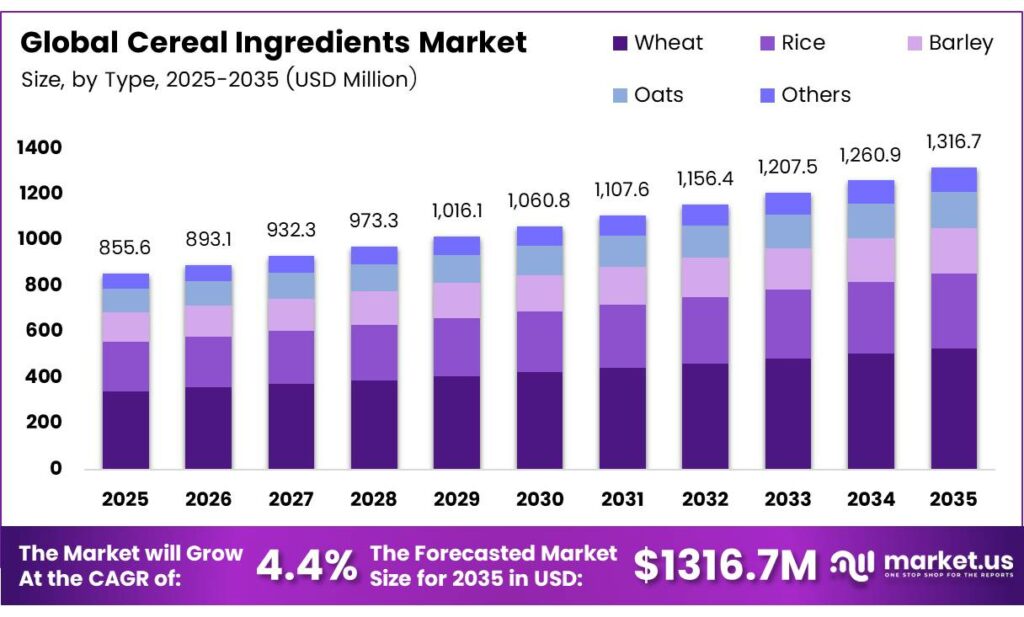

The Global Cereal Ingredients Market size is expected to be worth around USD 1,316.7 million by 2035 from USD 855.6 million in 2025, growing at a CAGR of 4.4% during the forecast period 2026 to 2035.

The cereal ingredients market covers raw and processed grain-derived inputs used across food production, animal feed, and industrial applications. Key cereal types include wheat, rice, barley, oats, and corn. These ingredients serve as foundational components in breakfast cereals, baked goods, beverages, and livestock feed formulations globally.

Market growth reflects rising global food demand driven by population expansion and rapid urbanization. Consumers increasingly seek convenient, nutrition-rich food options. Consequently, food manufacturers continue to expand production capacity and diversify their cereal ingredient portfolios to meet evolving dietary preferences across developed and emerging economies alike.

China’s cereal production reached 652.29 million tons in 2024, an increase of 10.86 million tons or 1.7% from 2023. This output expansion signals robust raw material availability supporting downstream cereal ingredient processors and manufacturers serving both domestic and export markets.

Organic cereal ingredients attract growing attention from health-conscious consumers and clean-label product manufacturers. Food companies reformulate products using whole-grain and minimally processed cereal inputs to align with public health guidelines. Moreover, rising demand for plant-based nutrition solutions continues to position cereal ingredients as versatile, scalable inputs across multiple food and beverage categories.

Key Takeaways

- The Global Cereal Ingredients Market is valued at USD 855.6 million in 2025 and is projected to reach USD 1,316.7 million by 2035 at a CAGR of 4.4% during the forecast period 2026 to 2035.

- Wheat holds the dominant share at 39.6% in 2025.

- Conventional leads the market with a 78.4% share in 2025.

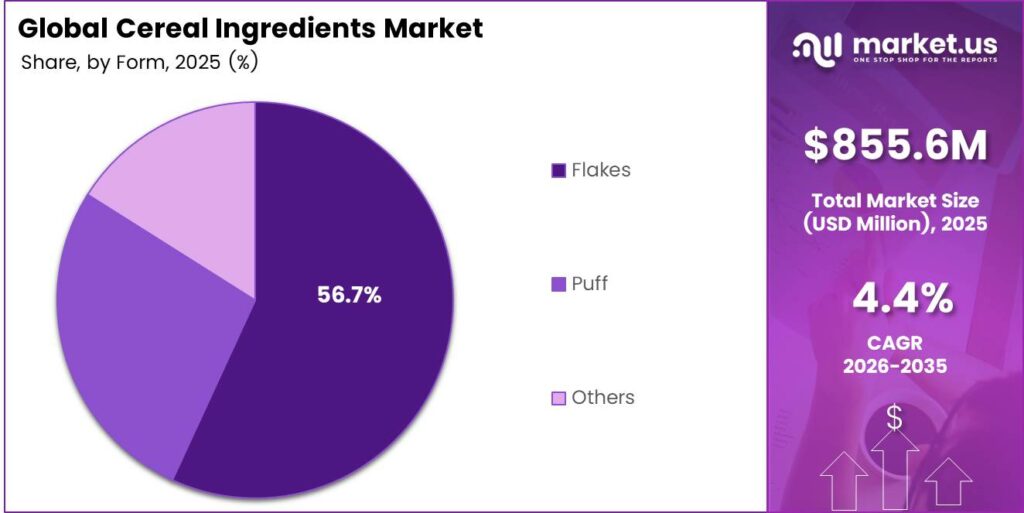

- Flakes dominate with a 56.7% share in 2025.

- Food and Beverages account for the largest share at 76.3% in 2025.

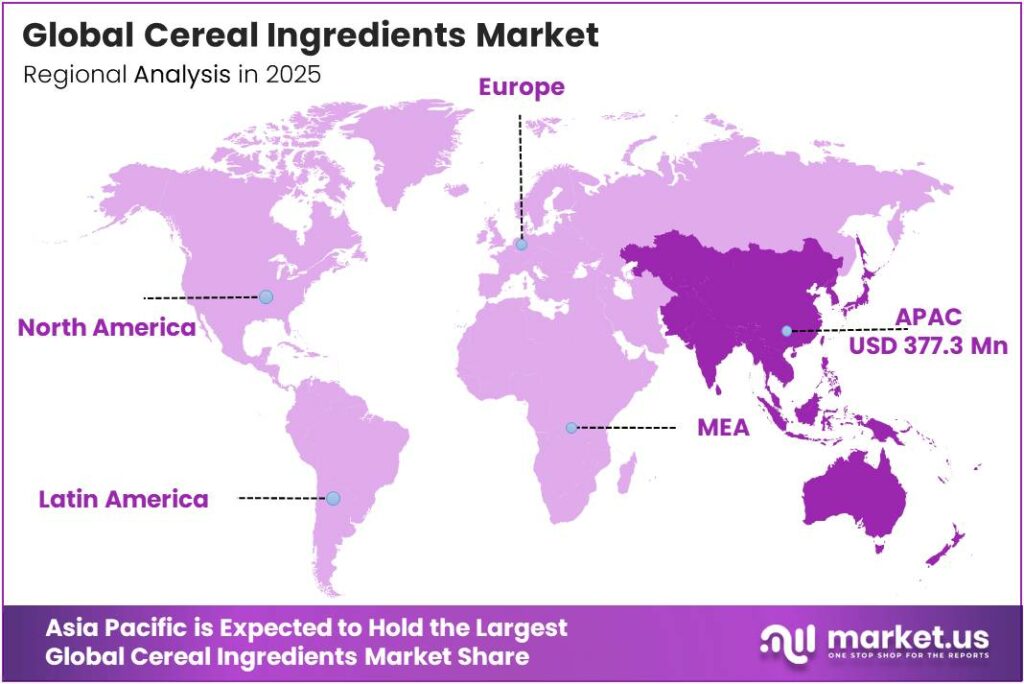

- Asia Pacific dominates the regional landscape with a 44.1% market share, valued at USD 377.3 million.

By Type Analysis

Wheat dominates with 39.6% due to its widespread use across baked goods and breakfast cereal formulations.

In 2025, Wheat held a dominant market position in the By Type segment of the Cereal Ingredients Market, with a 39.6% share. Wheat serves as the primary base for bread, pasta, biscuits, and breakfast cereals. Its high gluten content and versatile processing properties make it the preferred grain among food manufacturers globally. Moreover, growing demand for wheat-based convenience foods continues to reinforce this segment’s leadership position.

Rice holds a significant share within the cereal ingredients market, driven by its central role in Asian diets and infant nutrition products. Rice-based ingredients, including rice flour and rice flakes, find broad application in gluten-free food formulations. Additionally, rising consumer awareness about gluten intolerance accelerates rice ingredient adoption across developed and emerging markets alike.

Barley attracts increasing interest due to its nutritional benefits, particularly its high beta-glucan fiber content. Food and beverage manufacturers incorporate barley into health-focused products such as functional drinks, malt extracts, and whole-grain cereals. Furthermore, the animal feed sector drives substantial barley volume consumption, supporting its stable market presence alongside wheat and rice.

By Source Analysis

Conventional dominates with 78.4% due to established supply chains, lower costs, and widespread commercial availability.

In 2025, Conventional held a dominant market position in the By Source segment of the Cereal Ingredients Market, with a 78.4% share. Conventional cereal ingredients benefit from large-scale commercial farming, predictable supply volumes, and competitive pricing. Food manufacturers prefer conventional sources for high-volume production runs where cost efficiency remains a primary procurement criterion. Therefore, conventional ingredients continue to dominate global cereal ingredient supply chains.

Organic cereal ingredients represent the fastest-growing source segment, fueled by rising consumer demand for clean-label and sustainably produced food products. Premiumization trends drive food brands to incorporate organic wheat, oat, and rice ingredients into their formulations. However, limited certified organic farmland and higher production costs currently constrain supply growth and keep organic ingredient volumes below conventional market levels.

By Form Analysis

Flakes dominate with 56.7% due to their widespread use in ready-to-eat breakfast cereal products.

In 2025, Flakes held a dominant market position in the By Form segment of the Cereal Ingredients Market, with a 56.7% share. Cereal flakes derived from wheat, oats, rice, and corn serve as the core ingredient in the global breakfast cereal industry. Their ready-to-eat convenience, long shelf life, and nutritional fortification potential make them a preferred form for both retail and food service applications.

Puff cereal ingredients find strong application in snack foods, coated confections, and children’s breakfast products. Puffed grains offer a light texture and high absorption capacity for flavoring coatings and inclusions. Additionally, the growing snacking trend among urban consumers supports incremental demand growth for puffed cereal formats across the Asia Pacific and North American markets.

By Application Analysis

Food and Beverages dominate with 76.3% due to extensive cereal ingredient use across breakfast cereals, baked goods, and beverages.

In 2025, Food and Beverages held a dominant market position in the By Application segment of the Cereal Ingredients Market, with a 76.3% share. This segment encompasses breakfast cereals, baked goods, malt-based beverages, snacks, and dairy-alternative products. Rising urbanization and demand for convenient, nutrition-rich food products continuously expand cereal ingredient consumption across food and beverage manufacturing globally.

Breakfast Cereals represent the single largest sub-category within food and beverages, driven by consumer demand for quick, nutritious morning meal solutions. Manufacturers consistently reformulate products with whole grains, added vitamins, and reduced sugar profiles to address evolving health preferences. Consequently, breakfast cereal production volumes continue to consume significant shares of global wheat, oat, rice, and corn ingredient supply.

Animal Feed represents the second largest application segment, consuming significant volumes of corn, barley, and wheat by-products. Rapid livestock and poultry sector expansion across Asia and Latin America drives sustained demand for cereal-based feed formulations. Additionally, rising protein consumption globally accelerates animal husbandry activities, creating consistent volume uptake for cereal ingredients directed toward feed applications.

Key Market Segments

By Type

- Wheat

- Rice

- Barley

- Oats

- Others

By Source

- Organic

- Conventional

By Form

- Flakes

- Puff

- Others

By Application

- Food and Beverages

- Breakfast Cereals

- Baked Goods

- Others

- Animal Feed

- Others

Emerging Trends

Whole-Grain Formulations Gain Ground as Health Guidelines Reshape Ingredient Preferences

Food manufacturers actively reformulate products to align with public health guidelines emphasizing whole-grain cereal ingredients. Consumer awareness around fiber intake, heart health, and metabolic wellness drives demand for minimally processed grain inputs. The North American breakfast cereals market was worth USD 17.15 billion in 2026, reflecting how health-driven reformulation trends translate into large commercial opportunities for cereal ingredient suppliers.

Precision Agriculture and Real-Time Data Transform Cereal Grain Supply Chains

Precision agriculture adoption enhances yield consistency and quality standards for major cereal grains, including wheat, rice, and corn. Farmers use real-time weather monitoring and price signals to optimize planting decisions and reduce production variability. Additionally, geopolitical influences continue shifting global trade patterns, altering supplier market shares and creating new sourcing dynamics for cereal ingredient buyers across North America, Europe, and the Asia Pacific.

Drivers

Livestock Sector Growth and Urbanization Drive Strong Demand for Cereal Ingredients

Surging livestock and poultry sector expansion fuels massive demand for corn and wheat in animal feed applications globally. Simultaneously, population growth combined with accelerating urbanization drives higher consumption of wheat-based staples and baked goods. United States cereal production totaled 454.99 million tonnes in 2024, demonstrating the agricultural capacity supporting cereal ingredient supply chains serving both food and feed markets.

Favorable Weather Conditions and Trade Agreements Strengthen Ingredient Supply

Favorable reservoir recovery and above-average precipitation events boost corn and rice production recoveries across key agricultural regions. Consequently, cereal ingredient processors benefit from improved raw material availability and more stable input pricing. Moreover, preferential trade agreements and competitive grain pricing enable higher import volumes across strategic markets, reducing supply disruptions and supporting consistent ingredient procurement for food and feed manufacturers.

Restraints

Water Scarcity and Limited Arable Land Cap Output in Key Cereal Producing Regions

Chronic water scarcity and limited arable land permanently restrict wheat and barley production in arid agricultural zones across the Middle East, North Africa, and Central Asia. These structural supply limitations constrain ingredient availability and push procurement costs higher for food manufacturers. India’s cereal production reached 391.12 million tonnes in 2024, yet production stress from water access challenges continues to threaten yield stability in drought-prone growing areas.

Climate Disruptions and Infrastructure Gaps Create Persistent Supply Vulnerabilities

Recurrent typhoons, droughts, and post-harvest facility shortages trigger sharp declines in rice and corn yields across Southeast Asia and sub-Saharan Africa. Inadequate storage infrastructure amplifies post-harvest losses, reducing effective ingredient supply reaching processing facilities. Therefore, food manufacturers sourcing from climate-vulnerable regions face elevated supply chain risks, increased ingredient costs, and greater procurement unpredictability during adverse seasonal weather periods.

Growth Factors

Export Expansion and Milling Capacity Investments Unlock New Revenue Streams

Rising global demand for imported cereal grains opens export expansion pathways for major producing countries, including the United States, Canada, Australia, and Brazil. Simultaneously, investments in new milling capacity create scope for higher-value processed flours and flakes production. Cargill is actively building a canola processing facility in Regina, Saskatchewan, with the capacity to process 1 million metric tons annually, exemplifying how industry leaders expand infrastructure to capture cereal ingredient growth opportunities.

Strategic Reserve Policies and Supplier Diversification Strengthen Market Resilience

Strategic reserve management policies adopted by governments ensure a stable cereal ingredient supply during periods of price volatility and geopolitical disruption. Food manufacturers benefit from diversified global supplier bases that reduce dependency risks and unlock new sourcing efficiencies. Additionally, expanded trade relationships across Asia, Africa, and Latin America open new procurement channels, enabling cereal ingredient buyers to maintain supply continuity and negotiate more competitive input pricing effectively.

Regional Analysis

Asia Pacific Dominates the Cereal Ingredients Market with a Market Share of 44.1%, Valued at USD 377.3 Million

Asia Pacific leads the global cereal ingredients market, accounting for a 44.1% share valued at USD 377.3 million in 2025. The region benefits from massive agricultural output across China, India, and Southeast Asia, combined with a large and rapidly growing processed food manufacturing base. Rising disposable incomes, expanding urban populations, and strong government investment in food security infrastructure further reinforce the Asia Pacific’s dominant regional position in cereal ingredient consumption.

North America maintains a strong cereal ingredients market presence supported by advanced agricultural technology, large-scale grain processing infrastructure, and robust breakfast cereal manufacturing activity. The United States and Canada collectively represent major cereal grain producers and ingredient exporters. Moreover, growing consumer preference for whole-grain, fortified, and organic cereal products drives continued innovation and premium ingredient demand across North American food manufacturing channels.

Europe sustains steady cereal ingredient demand driven by its well-established bakery, malt beverages, and breakfast cereal industries. Germany, France, and the United Kingdom serve as key consumption and processing hubs for wheat, oat, and barley ingredients. Additionally, stringent EU food safety and sustainability regulations encourage manufacturers to adopt certified, traceable, and sustainably sourced cereal inputs across their product formulations.

Latin America emerges as a growing cereal ingredient producer and exporter, with Brazil leading regional grain output capacity. Expanding livestock and poultry industries drive strong domestic demand for corn and soy-adjacent cereal feed ingredients. Furthermore, favorable agricultural land availability and government programs supporting crop yield improvement position Latin America as a strategic cereal ingredient supply source for both regional and international buyers.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

Bahlsen is a well-established European food manufacturer with deep expertise in biscuit and bakery product production using high-quality cereal ingredients. The company focuses on sourcing premium wheat and grain inputs to maintain consistent product quality across its snack and confectionery portfolio. Bahlsen’s commitment to sustainable sourcing and product innovation positions it as a strong participant in the specialty cereal ingredient value chain.

Kraft Foods operates a broad food manufacturing portfolio that relies extensively on cereal-based ingredients across its biscuit, cracker, and convenience food product categories. The company leverages strong supplier relationships and global procurement networks to ensure consistent access to wheat, corn, and oat ingredients. Kraft Foods applies cereal ingredients across a diverse range of branded products targeting both retail consumers and food service operators.

Biscoff specializes in caramelized biscuit products that depend on high-quality wheat flour and specialty cereal ingredient inputs for consistent taste and texture delivery. The brand has built significant consumer recognition globally through airline partnerships and retail distribution expansion. Biscoff’s ingredient sourcing strategy emphasizes quality, consistency, and flavor precision, reflecting a focused approach to cereal ingredient utilization in premium biscuit manufacturing.

Stroopwafels represent a distinctive Dutch confectionery category that relies on wheat-based waffle layers produced from carefully sourced cereal flour ingredients. The product category has expanded into international retail markets through growing consumer interest in European specialty snacks. Stroopwafel manufacturers prioritize cereal ingredient quality and consistency to maintain the authentic texture and taste that defines this recognized snack format globally.

Top Key Players in the Market

- Bahlsen

- Kraft Foods

- Biscoff

- Stroopwafels

- Mackays

- Duchess

- Millefoglie

Recent Developments

- In 2025, Bahlsen will focus on the sustainable sourcing of key cereal ingredients like wheat flour, which aligns directly with the cereal ingredients sector. Bahlsen sources 100% of its wheat flour via controlled contract farming, with a strong emphasis on regional sourcing to support sustainability from the field onward.

- In 2025, Kraft Foods / Kraft Heinz wheat flour, grains, or biscuit/cookie lines were detailed in company reports. Kraft Heinz’s 2024 ESG Report emphasizes responsible sourcing and sustainable agriculture broadly, including Supplier Guiding Principles, a Global Deforestation- and Conversion-Free Policy, and supplier engagement via webinars and audits.

Report Scope

Report Features Description Market Value (2025) USD 855.6 Million Forecast Revenue (2035) USD 1,316.7 Million CAGR (2026-2035) 4.4% Base Year for Estimation 2025 Historic Period 2020-2024 Forecast Period 2026-2035 Report Coverage Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments Segments Covered By Type (Wheat, Rice, Barley, Oats, Others), By Source (Organic, Conventional), By Form (Flakes, Puff, Others), By Application (Food and Beverages, Animal Feed, Others) Regional Analysis North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East & Africa (GCC, South Africa, and Rest of MEA) Competitive Landscape Bahlsen, Kraft Foods, Biscoff, Stroopwafels, Mackays, Duchess, Millefoglie Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited Users and Printable PDF)  Cereal Ingredients MarketPublished date: March 2026add_shopping_cartBuy Now get_appDownload Sample

Cereal Ingredients MarketPublished date: March 2026add_shopping_cartBuy Now get_appDownload Sample -

-

- Bahlsen

- Kraft Foods

- Biscoff

- Stroopwafels

- Mackays

- Duchess

- Millefoglie

Our Clients

- 182091

- March 2026