Global Biorational Pesticides Market Size, Share Analysis Report By Type (Biorational Insecticides, Biorational Fungicides, Biorational Nematicides, Others), By Formulation (Liquid, Dry), By Source (Botanical, Microbials, Non-Organic, Others), By Mode of Application (Foliar Spray, Soil Treatment, Trunk Injection, Others) , By Region and Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Trends and Forecast 2026-2035

- Published date: Mar 2026

- Report ID: 180860

- Number of Pages: 346

- Format:

-

keyboard_arrow_up

Quick Navigation

Report Overview

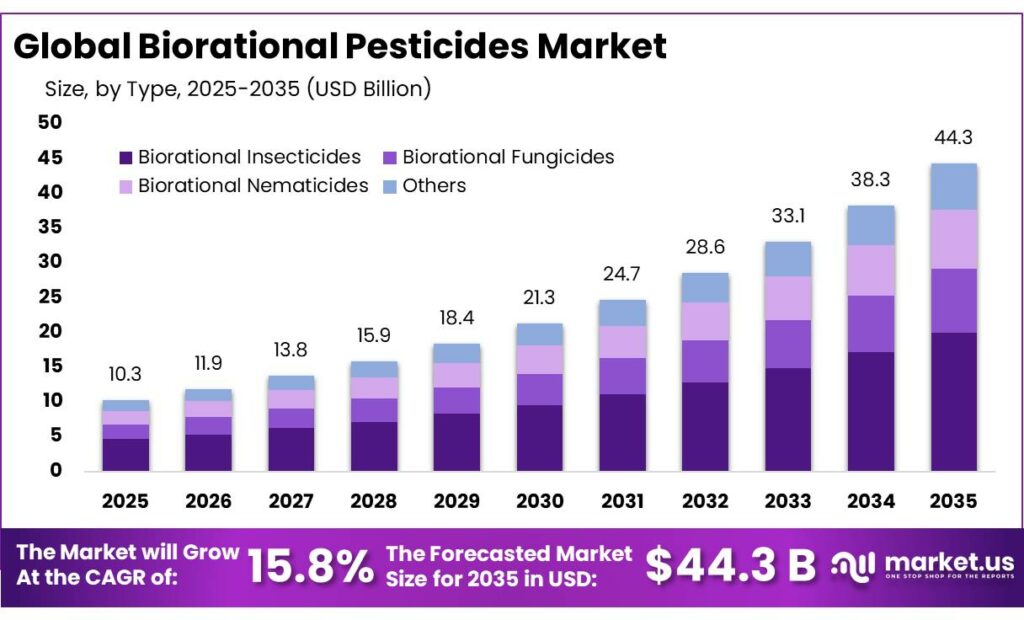

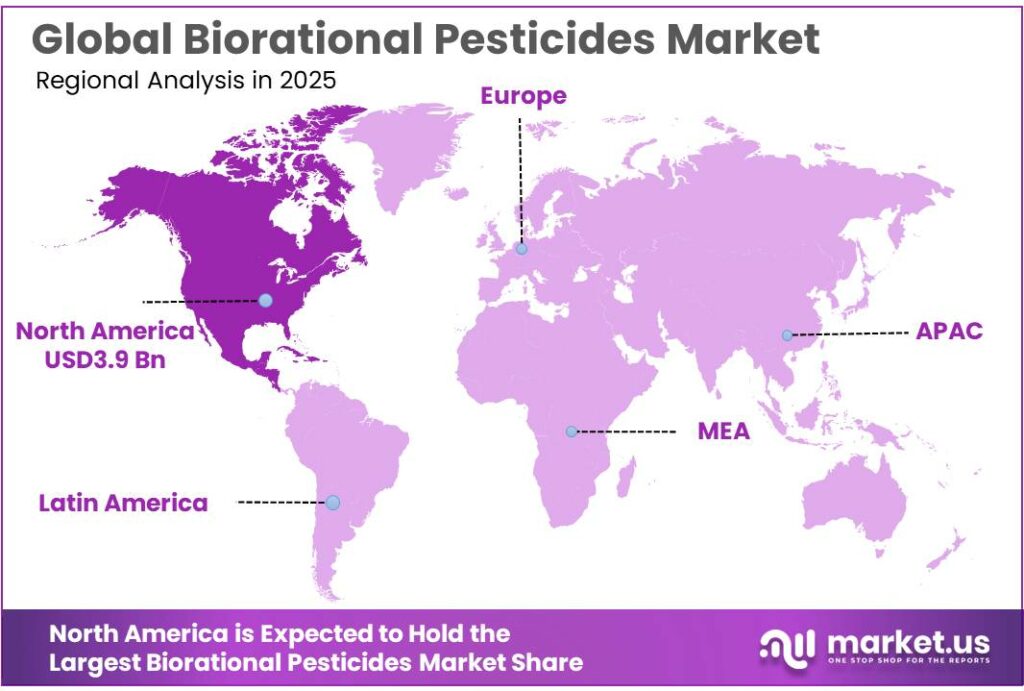

The Global Biorational Pesticides Market size is expected to be worth around USD 44.3 Billion by 2035, from USD 10.3 Billion in 2025, growing at a CAGR of 15.8% during the forecast period from 2026 to 2035. In 2025, North America held a dominant market position, capturing more than a 38.4% share, holding USD 3.9 Billion revenue.

Biorational pesticides represent a strategically important segment of crop protection because they are designed to act with higher target specificity, lower non-target impact, and stronger compatibility with integrated pest management systems than many conventional synthetic chemistries.

The Food and Agriculture Organization reported that total agricultural pesticide use worldwide reached 3.70 million tonnes of active ingredients in 2022, up 4% year on year, 13% over a decade, and roughly double the 1990 level. FAO indicates that feeding the global population by 2050 will require about 70% more food production than 2005/07 levels, which increases the need for crop protection tools that can preserve yields while supporting sustainability, residue compliance, and resistance management.

- According to the 2026 edition of The World of Organic Agriculture, organic farming is now practiced in more than 180 countries, with nearly 99 million hectares under organic management and at least 4.8 million farmers involved globally; the same source states that global organic food and drink sales reached almost €145 billion in 2025. This matters directly for biorational pesticides because these products are often better aligned with residue restrictions, pollinator protection requirements, and retailer-led sustainability standards.

On the regulatory side, industrial adoption is also benefiting from relatively supportive review pathways in some jurisdictions: the U.S. EPA states that new biopesticide active ingredients are typically registered in less than 11 months, materially faster than conventional pesticide review timelines.

- In Europe, the European Commission has set a target of 50% reduction in the use and risk of chemical pesticides by 2030, which structurally improves the outlook for biorational alternatives and integrated programs. In the United States, USDA’s Organic Transition Initiative is a $300 million effort to help producers transition into organic systems, expanding the addressable market for biological and biorational crop-protection inputs.

The strongest opportunities are expected in residue-sensitive export crops, greenhouse cultivation, precision application, tank-mix compatibility with conventional products, and resistance-management programs where biological rotation is increasingly valuable. Overall, the industry outlook remains favorable because biorational pesticides are becoming less of a substitute category and more of a core enabler of resilient, regulation-ready food production systems.

- The EU also reported organic retail sales rising by more than 128% over 10 years, from about EUR 18 billion in 2009 to EUR 41 billion in 2019, while organic farmland expanded from 8.3 million hectares in 2010 to 13.8 million hectares in 2019, equivalent to 8.5% of utilised agricultural area. In the United States, USDA’s Organic Transition Initiative represents a USD 300 million investment to support producers shifting toward organic systems.

Key Takeaways

- Biorational Pesticides Market size is expected to be worth around USD 44.3 Billion by 2035, from USD 10.3 Million in 2025, growing at a CAGR of 9.7%.

- Biorational Insecticides held a dominant market position, capturing more than a 45.8% share.

- Liquid held a dominant market position, capturing more than a 69.1% share.

- Microbials held a dominant market position, capturing more than a 39.6% share in the biorational pesticides market.

- Foliar Spray held a dominant market position, capturing more than a 51.7% share.

- North America held the dominant position in the biorational pesticides market, accounting for nearly 38.4% of the global share with an estimated value of around USD 3.9 billion.

By Type Analysis

Biorational Insecticides dominates with 45.8% due to growing demand for eco-friendly pest control in agriculture

In 2024, Biorational Insecticides held a dominant market position, capturing more than a 45.8% share of the global biorational pesticides market. This strong position was mainly supported by the increasing demand for targeted pest control solutions that are safer for crops, beneficial insects, and the environment. Farmers across major agricultural regions continued to adopt biorational insecticides as part of integrated pest management practices, particularly in fruits, vegetables, and high-value horticultural crops where residue control is critical. These products are designed to control insects such as aphids, whiteflies, caterpillars, and beetles while minimizing harm to pollinators and natural predators.

By Formulation Analysis

Liquid formulations dominate with 69.1% due to easier application and better field coverage

In 2024, Liquid held a dominant market position, capturing more than a 69.1% share in the biorational pesticides market by formulation. This leading position was mainly supported by the convenience and effectiveness of liquid-based crop protection products in agricultural operations. Farmers generally prefer liquid formulations because they are easy to dilute, mix, and apply through conventional spraying equipment. These products allow uniform distribution on crop surfaces, which improves pest control efficiency and ensures better coverage across large farming areas. As a result, liquid biorational pesticides became the preferred option for many growers, especially in fruit, vegetable, and plantation crop farming.

By Source Analysis

Microbials dominate with 39.6% as farmers shift toward biologically derived pest control

In 2024, Microbials held a dominant market position, capturing more than a 39.6% share in the biorational pesticides market by source. This strong presence was mainly driven by the growing use of naturally occurring microorganisms such as bacteria, fungi, viruses, and protozoa that help control crop pests and diseases. Farmers increasingly adopted microbial solutions because they offer targeted pest control while causing minimal harm to beneficial insects and surrounding ecosystems. These products are widely used in vegetable farming, fruit cultivation, and greenhouse agriculture where sustainable pest management practices are becoming more important.

By Mode of Application Analysis

Foliar Spray dominates with 51.7% as farmers prefer direct crop protection methods

In 2024, Foliar Spray held a dominant market position, capturing more than a 51.7% share in the biorational pesticides market by mode of application. This method remained widely used because it allows pesticides to be applied directly to plant leaves where pests and diseases are most active. Farmers prefer foliar spraying since it provides quick action and visible results, especially in crops that are vulnerable to insect attacks and fungal infections. The approach also helps ensure that the active ingredients reach the targeted pest population effectively, improving crop protection outcomes.

Key Market Segments

By Type

- Biorational Insecticides

- Biorational Fungicides

- Biorational Nematicides

- Others

By Formulation

- Liquid

- Dry

By Source

- Botanical

- Microbials

- Non-Organic

- Others

By Mode of Application

- Foliar Spray

- Soil Treatment

- Trunk Injection

- Others

Emerging Trends

Increasing Adoption of Integrated Pest Management (IPM) Supporting Biorational Pesticides

One of the most important recent trends shaping the biorational pesticides industry is the growing adoption of Integrated Pest Management (IPM) in modern agriculture. IPM is an approach that combines biological, cultural, and chemical pest control methods to reduce environmental damage while maintaining crop productivity. Because biorational pesticides are generally derived from natural sources and have lower toxicity compared with conventional chemicals, they fit well within IPM programs and are increasingly used by farmers around the world.

Agriculture today faces increasing challenges from pest outbreaks, climate change, and the need to produce more food for a growing population. At the same time, excessive use of chemical pesticides has raised concerns about environmental safety and human health. According to the Food and Agriculture Organization (FAO), global pesticide use increased by about 70% between 2000 and 2022, reflecting the growing dependence on chemical crop protection in many agricultural systems.

The rising use of chemical pesticides has encouraged governments and international organizations to promote more sustainable pest control strategies. Integrated Pest Management is one of the most widely supported approaches because it reduces pesticide dependency while still protecting crop yields. The FAO explains that IPM focuses on using ecological processes such as natural predators and biological pest control to manage crop pests while reducing pesticide residues in food and the environment.

Drivers

Rising Crop Losses and the Need for Safer Pest Control Solutions

One of the strongest driving factors behind the growth of biorational pesticides is the rising threat of crop losses caused by pests and plant diseases. Around the world, farmers face increasing pressure to protect crops while also maintaining environmental safety and food quality. According to the Food and Agriculture Organization (FAO), up to 40% of global crop production is lost every year due to plant pests and diseases. These losses are not only a challenge for farmers but also create a serious problem for global food security and agricultural sustainability.

- The economic impact of these losses is also significant. FAO estimates that plant diseases alone cause more than USD 220 billion in global economic losses each year, while invasive insects account for at least USD 70 billion in additional losses annually. Such figures highlight the scale of the problem and explain why governments, research institutions, and farmers are increasingly looking for safer and more effective pest management methods.

Government initiatives have also played a role in promoting sustainable pest management practices. For example, the FAO and international partners have launched several programs focused on improving plant health and encouraging responsible pesticide use. Global awareness campaigns such as the International Year of Plant Health highlighted the importance of protecting crops from pests and diseases while promoting safer pest control technologies. These initiatives encourage farmers and agricultural institutions to adopt biological and environmentally friendly pest management tools, including biorational pesticides.

At the same time, the growth of organic farming has further strengthened the demand for biorational pest control products. Organic agriculture is expanding rapidly around the world. According to FAO statistics, organic farming is now practiced in almost 190 countries, covering nearly 99 million hectares of agricultural land and involving more than 4.3 million farmers globally. Because organic farming restricts the use of synthetic pesticides, growers in this sector rely heavily on biological pest control solutions such as microbial and botanical pesticides.

Restraints

Limited Awareness and Adoption Among Farmers in Developing Regions

One of the major restraining factors for the growth of biorational pesticides is the limited awareness and adoption among farmers, especially in developing agricultural regions. Even though biological and environmentally friendly crop protection products are gaining attention globally, many farmers still rely heavily on conventional chemical pesticides because they are more familiar, easily available, and often perceived as more effective in controlling pests quickly.

- According to the Food and Agriculture Organization (FAO), global pesticide use in agriculture reached about 3.73 million tonnes of active ingredients in 2023, showing how strongly farmers still depend on chemical pest control solutions. The same report indicates that pesticide application intensity averaged 2.40 kilograms per hectare of cropland worldwide, reflecting the widespread use of synthetic crop protection products in farming systems.

Another issue is the lack of technical knowledge and training among farmers. In several developing countries, agricultural extension systems still focus more on traditional chemical crop protection practices. A research analysis on pesticide safety practices found that the average level of proper pesticide safety use among farmers in developing regions was around 43.1%, highlighting the gaps in awareness, training, and proper pesticide management.

Government programs and international organizations are trying to address this challenge through training and awareness campaigns. The FAO and other agricultural bodies promote Integrated Pest Management (IPM) programs that encourage farmers to reduce dependence on chemical pesticides and adopt biological control methods where possible. These programs include field demonstrations, farmer education workshops, and extension services designed to improve farmers’ understanding of safer pest management practices.

Opportunity

Rapid Expansion of Organic Farming Creating New Opportunities for Biorational Pesticides

One of the biggest growth opportunities for the biorational pesticides industry comes from the rapid expansion of organic and sustainable farming worldwide. As consumers become more concerned about food safety, environmental protection, and chemical residues in food, demand for organically produced crops is rising steadily. Organic farming systems rely heavily on biological pest control tools because synthetic chemical pesticides are restricted in certified organic production.

- According to the Food and Agriculture Organization (FAO) and global organic agriculture reports, organic farming is now practiced in almost 190 countries worldwide. The total area under organic agriculture has reached nearly 99 million hectares, with more than 4.3 million farmers involved in organic production globally. These numbers show how quickly organic farming has expanded over the past decade, creating a growing demand for environmentally friendly pest management solutions.

The organic food market itself is also growing rapidly. Global sales of organic food and beverages reached about EUR 136 billion in 2023, reflecting strong consumer demand for healthier and sustainably produced food products. Another reason this trend creates growth opportunities is the scale of global agriculture itself. FAO estimates that there are more than 608 million farms worldwide, and over 90% of them are family farms that manage about 70–80% of global farmland and produce nearly 80% of the world’s food.

For example, international organizations such as FAO continue to promote plant health programs that encourage environmentally friendly pest management solutions. FAO estimates that 20–40% of global crop production is lost every year due to pests and plant diseases, which highlights the importance of developing safer and more effective crop protection technologies.

Regional Insights

North America dominates the Biorational Pesticides Market with 38.4% share, reaching about USD 3.9 Billion

North America held the dominant position in the biorational pesticides market, accounting for nearly 38.4% of the global share with an estimated value of around USD 3.9 billion. The region’s strong leadership is mainly supported by advanced agricultural practices, strict environmental regulations, and increasing demand for sustainable farming solutions. The United States and Canada are the major contributors within this regional market, where farmers are gradually shifting toward biological crop protection products to reduce reliance on conventional chemical pesticides.

Government agencies such as the U.S. Environmental Protection Agency (EPA) have established regulatory frameworks that encourage the development and registration of biological pesticides, helping companies introduce safer and environmentally friendly pest control products. As of recent records, hundreds of biopesticide active ingredients have been registered by the EPA, showing strong regulatory support for biological pest management solutions.

Agricultural sustainability initiatives and the growth of organic farming have also strengthened the demand for biorational pesticides in North America. According to the United States Department of Agriculture (USDA), certified and exempt organic product sales in the United States reached USD 9.6 billion in 2022, representing a 32% increase compared with 2017, with approximately 39,506 organic producers operating across the country.

Key Regions and Countries Insights

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

BASF SE is one of the largest chemical and agricultural solution providers in the world. In 2024, BASF reported total global sales of about €65.3 billion, highlighting its strong global market presence. The company’s Agricultural Solutions division generated approximately €9.8 billion in revenue in 2024, representing a significant share of BASF’s overall business portfolio. BASF also invests heavily in innovation, dedicating around 11% of its revenue to research and development, which supports the development of biological crop protection technologies, including biorational pesticides and sustainable farming solutions.

FMC Corporation is a global agricultural sciences company known for developing crop protection technologies, including biological and biorational solutions. In 2024, FMC reported total revenue of about USD 4.25 billion, reflecting its strong presence in global crop protection markets. The company operates in over 100 countries and employs around 5,700 people worldwide. FMC also recorded USD 737 million in operating cash flow in 2024, demonstrating its financial stability and continued investment in research for new pest management technologies and sustainable agricultural products.

Sumitomo Chemical Co. Ltd is a major global chemical and agricultural solutions provider headquartered in Japan. The company operates in multiple sectors including agrochemicals, pharmaceuticals, and advanced materials. In FY2024, the company reported sales revenue of around ¥540.2 billion in one of its major business segments, supported by strong demand for chemical and agricultural products. Sumitomo Chemical also employs over 32,500 people globally and continues to expand its crop protection portfolio through biological and biorational technologies aimed at improving sustainable agriculture and environmental safety.

Top Key Players Outlook

- BASF SE

- FMC Corporation

- Sumitomo Chemical Co. Ltd

- Valent BioSciences LLC

- Biobest Group

- Bayer AG

- Syngenta AG

- Pro Farm Group Inc

- Gowan Company

- BIONEMA

Recent Industry Developments

In 2024, BASF reported total global sales of about €65.3 billion, reflecting its strong position in the global chemical and agricultural market. Within this, the Agricultural Solutions segment generated around €9.8 billion in sales in 2024, which includes crop protection products, seeds, and biological solutions used in sustainable farming.

In 2024, FMC Corporation reported total revenue of about USD 4.25 billion, reflecting its strong position in the global crop protection industry. The company has also built a growing biological product pipeline, and its biologicals business generated around USD 240 million in revenue in 2024, showing 33% annual growth, which was one of the fastest growth rates in the biological crop protection segment.

Report Scope

Report Features Description Market Value (2025) USD 10.3 Bn Forecast Revenue (2035) USD 44.3 Bn CAGR (2026-2035) 15.8% Base Year for Estimation 2025 Historic Period 2020-2024 Forecast Period 2026-2035 Report Coverage Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments Segments Covered By Type (Biorational Insecticides, Biorational Fungicides, Biorational Nematicides, Others), By Formulation (Liquid, Dry), By Source (Botanical, Microbials, Non-Organic, Others), By Mode of Application (Foliar Spray, Soil Treatment, Trunk Injection, Others) Regional Analysis North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – GCC, South Africa, Rest of MEA Competitive Landscape BASF SE, FMC Corporation, Sumitomo Chemical Co. Ltd, Valent BioSciences LLC, Biobest Group, Bayer AG, Syngenta AG, Pro Farm Group Inc, Gowan Company, BIONEMA Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF)  Biorational Pesticides MarketPublished date: Mar 2026add_shopping_cartBuy Now get_appDownload Sample

Biorational Pesticides MarketPublished date: Mar 2026add_shopping_cartBuy Now get_appDownload Sample -

-

- BASF SE

- FMC Corporation

- Sumitomo Chemical Co. Ltd

- Valent BioSciences LLC

- Biobest Group

- Bayer AG

- Syngenta AG

- Pro Farm Group Inc

- Gowan Company

- BIONEMA

Our Clients

- 180860

- Mar 2026