Global Angiography Devices Market By Product Type (Angiography Systems, Vascular Closure Devices, Guidewires, Contrast Media, Catheters, Balloons and Angiography Accessories), By Application (Diagnostic and Therapeutic), By Technology (X-Ray Angiography, MR Angiography and CT Angiography), Region and Companies – Industry Segment Outlook, Market Assessment, Competition Scenario, Trends and Forecast 2026-2035

- Published date: Feb 2026

- Report ID: 178195

- Number of Pages: 390

- Format:

-

keyboard_arrow_up

Quick Navigation

Report Overview

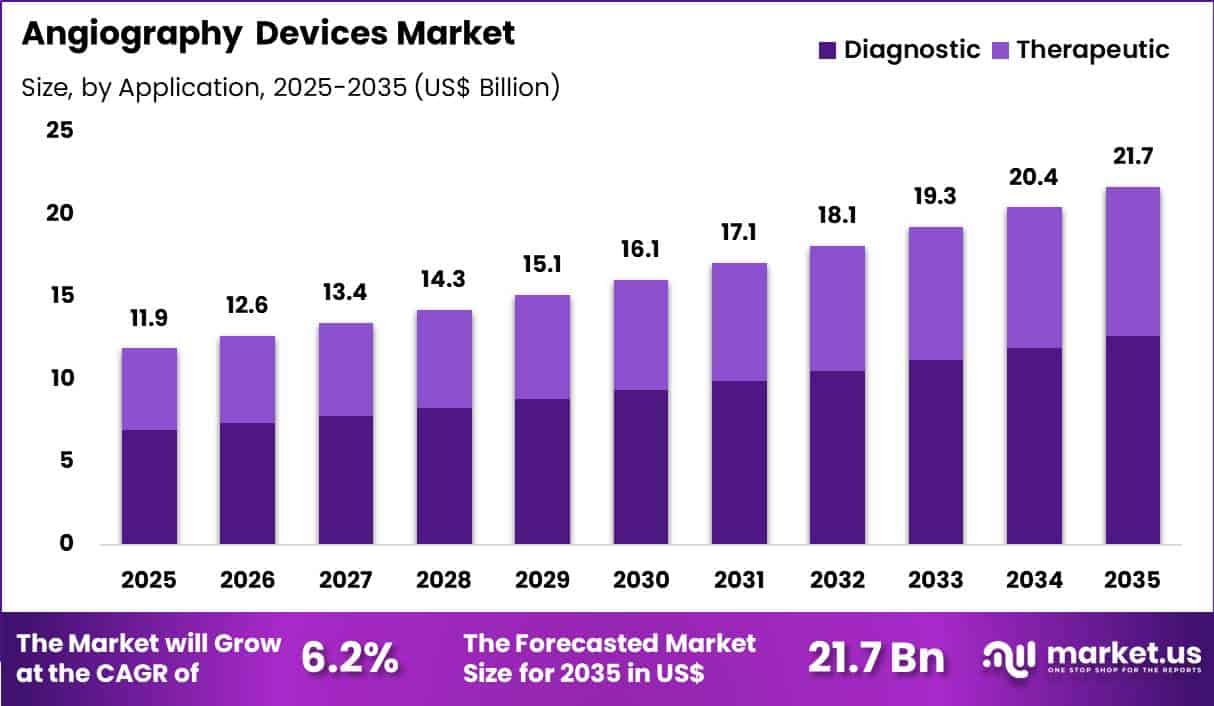

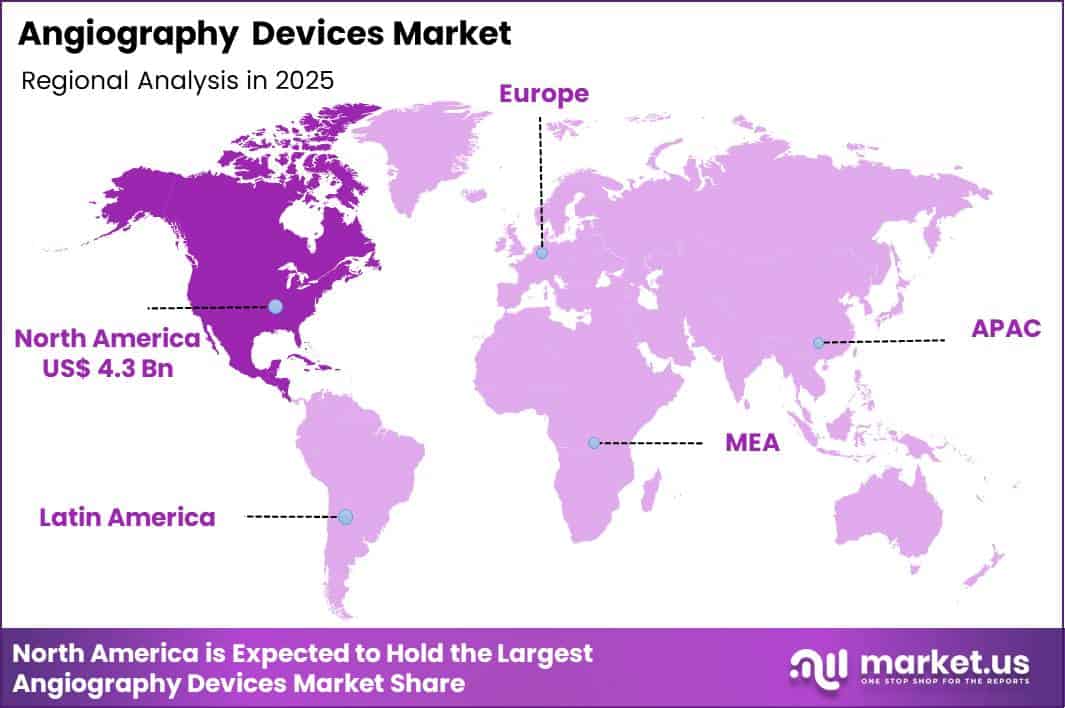

The Global Angiography Devices Market size is expected to be worth around US$ 21.7 Billion by 2035 from US$ 11.9 Billion in 2025, growing at a CAGR of 6.2% during the forecast period 2026-2035. In 2025, North America led the market, achieving over 36.3% share with a revenue of US$ 4.3 Billion.

Rising demand for precise vascular diagnostics and minimally invasive interventions propels the angiography devices market as interventional radiologists and cardiologists require advanced imaging systems to visualize blood vessels with exceptional clarity.

Cardiologists increasingly utilize digital subtraction angiography to detect coronary artery stenoses during percutaneous coronary interventions, guiding stent placement and balloon angioplasty in acute myocardial infarction cases.

These devices support peripheral angiography in lower extremity arterial disease, identifying occlusions and enabling endovascular revascularization for patients with critical limb ischemia. Radiologists apply cerebral angiography to evaluate intracranial aneurysms and arteriovenous malformations, facilitating precise coil embolization and flow diversion procedures.

Angiography equipment also enables pulmonary artery assessments in chronic thromboembolic pulmonary hypertension, supporting catheter-directed thrombolysis and balloon pulmonary angioplasty. Vascular surgeons employ intraoperative angiography to confirm patency of bypass grafts and endografts during aortic aneurysm repairs, reducing the need for revision surgeries.

Manufacturers pursue opportunities to integrate artificial intelligence algorithms that enhance image quality and automate vessel segmentation, expanding applications in complex hybrid procedures combining open and endovascular techniques. Developers advance flat-panel detector systems with lower radiation doses, broadening utility in pediatric interventions where minimizing exposure remains critical.

These innovations facilitate real-time 3D rotational angiography that improves navigation in tortuous vessels during neurointerventional treatments. Opportunities emerge in portable C-arm systems for hybrid operating rooms, supporting on-table decision-making in trauma and emergency vascular cases.

Companies invest in contrast-sparing technologies and high-frame-rate imaging, addressing patient safety in high-risk populations. Recent trends emphasize seamless integration with robotic platforms and cloud-based analytics, positioning angiography devices as foundational tools in value-based interventional care focused on accuracy, efficiency, and reduced complications.

Key Takeaways

- In 2025, the market generated a revenue of US$ 11.9 Billion, with a CAGR of 6.2%, and is expected to reach US$ 21.7 Billion by the year 2035.

- The product type segment is divided into angiography systems, vascular closure devices, guidewires, contrast media, catheters, balloons and angiography accessories, with angiography systems taking the lead with a market share of 33.7%.

- Considering application, the market is divided into diagnostic and therapeutic. Among these, diagnostic held a significant share of 58.2%.

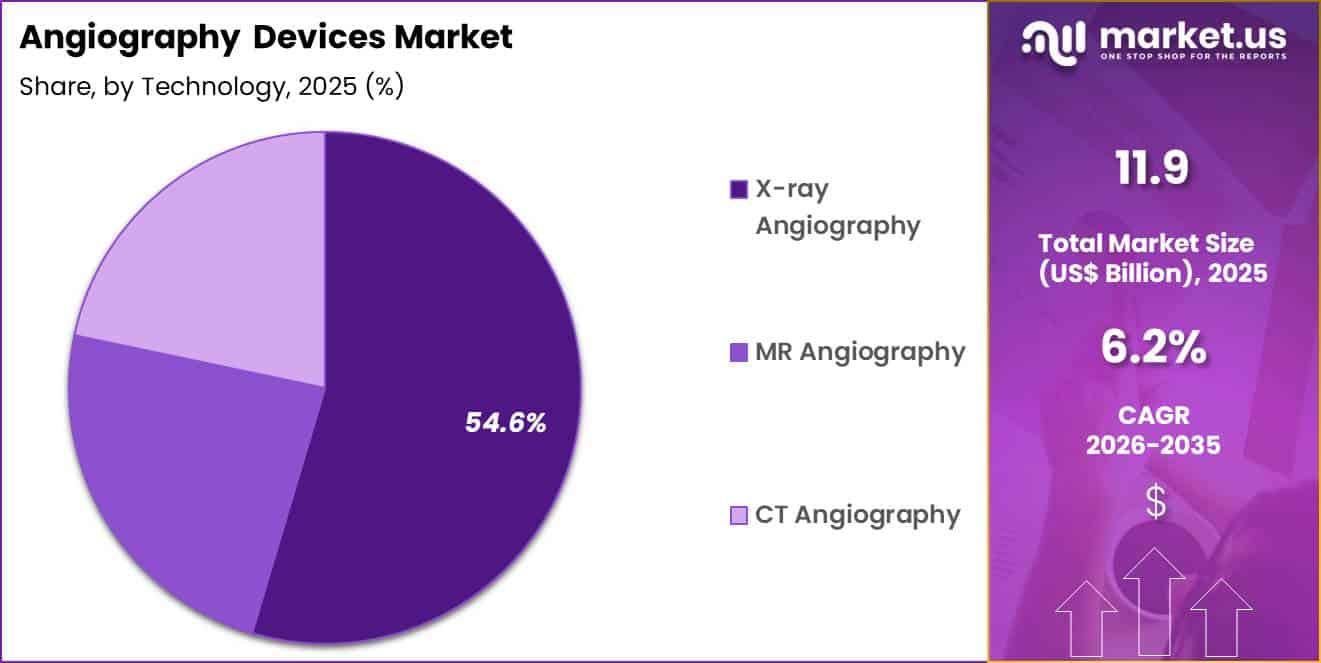

- Furthermore, concerning the technology segment, the market is segregated into x-ray angiography, MR angiography and CT angiography. The x-ray angiography sector stands out as the dominant player, holding the largest revenue share of 54.6% in the market.

- North America led the market by securing a market share of 36.3%.

Product Type Analysis

Angiography systems contributed 33.7% of growth within product type and led the angiography devices market due to their central role in vascular imaging and interventional guidance. Hospitals invest in advanced angiography suites to support high volumes of cardiovascular and peripheral vascular procedures. These systems provide real-time visualization that enhances procedural accuracy and clinical confidence. Increasing prevalence of coronary artery disease and stroke risk factors drives demand for imaging infrastructure.

Growth strengthens as healthcare providers upgrade to digital flat-panel detectors and hybrid imaging platforms. Integration with navigation and 3D reconstruction tools improves diagnostic clarity. Expanding catheterization labs in emerging regions further elevate system installations.

Hospitals prioritize high-throughput imaging to manage rising patient loads efficiently. The segment is expected to remain dominant as vascular disease burden continues to require comprehensive imaging capabilities.

Application Analysis

Diagnostic applications generated 58.2% of growth within application and emerged as the leading segment due to the increasing need for early and precise vascular assessment. Clinicians rely on angiography to detect stenosis, aneurysms, and occlusions before planning interventions. Preventive cardiology and neurology programs emphasize early imaging to reduce complications. Rising screening initiatives for high-risk populations strengthen diagnostic procedure volumes.

Growth accelerates as awareness of cardiovascular disease increases across aging populations. Diagnostic workflows form the foundation for therapeutic planning, which reinforces imaging demand. Improvements in image resolution and contrast enhance diagnostic confidence.

Referral patterns from primary care to specialized imaging centers further expand volumes. The segment is anticipated to maintain leadership as early vascular detection remains critical to patient management strategies.

Technology Analysis

X-ray angiography accounted for 54.6% of growth within technology and dominated the angiography devices market due to its established clinical utility and real-time imaging capability. Interventional cardiologists and radiologists depend on X-ray-based systems for both diagnostic and guided therapeutic procedures. High spatial resolution and dynamic imaging support accurate vessel visualization. Broad reimbursement familiarity further reinforces adoption across healthcare systems.

Growth continues as technology advances reduce radiation exposure and improve image processing speed. Hybrid operating rooms increasingly incorporate X-ray angiography platforms for complex procedures. Training familiarity and long-standing clinical guidelines sustain preference.

Expansion of minimally invasive vascular interventions further strengthens utilization. The segment is projected to remain dominant as X-ray angiography continues to serve as the backbone of interventional vascular imaging.

Key Market Segments

By Product Type

- Angiography Systems

- Vascular Closure Devices

- Guidewires

- Contrast Media

- Catheters

- Balloons

- Angiography Accessories

By Application

- Diagnostic

- Therapeutic

By Technology

- X-Ray Angiography

- MR Angiography

- CT Angiography

Drivers

Increasing prevalence of cardiovascular diseases is driving the market

The global escalation in cardiovascular diseases has markedly elevated the demand for angiography devices, which are crucial for diagnosing and treating conditions like coronary artery disease through detailed vascular imaging. Advanced diagnostic practices and lifestyle factors have led to more frequent identifications of heart-related issues, expanding the application of angiography in interventional cardiology.

Healthcare providers are increasingly deploying these devices to support minimally invasive procedures that improve patient outcomes in CVD management. The link between hypertension and heart attacks further intensifies the need for precise angiographic visualization in clinical settings.

Government health entities are prioritizing CVD prevention, fostering the integration of angiography technologies in public hospitals. The association between stroke risks and vascular blockages underscores the market’s growth for diagnostic catheters and contrast media. National health initiatives emphasize early detection to reduce mortality rates from cardiovascular events.

Key manufacturers are enhancing device features to address this rising clinical imperative. According to the World Health Organization, an estimated 19.8 million people died from cardiovascular diseases in 2022, representing approximately 32% of all global deaths. This driver sustains investments in interventional radiology infrastructure across regions.

Restraints

High cost of angiography devices is restraining the market

The premium pricing of angiography systems, including hybrid suites and digital flat-panel detectors, restricts their accessibility in facilities with limited capital budgets. Manufacturing complexities for high-resolution imaging components contribute to elevated production expenses for these advanced devices. Smaller hospitals often face challenges in justifying investments amid competing equipment priorities.

Regulatory compliance for radiation safety adds layers of cost to procurement and maintenance. In public sectors, fiscal priorities favor basic diagnostic tools over sophisticated angiography setups. Providers sometimes delay upgrades, opting for refurbished units to manage operational finances.

This restraint affects scalability in resource-constrained environments globally. Collaborative leasing models seek to negotiate better terms, though effectiveness varies. Despite procedural advantages, economic considerations impede equitable distribution of technology. Addressing these through value-based pricing remains essential for overcoming market limitations.

Opportunities

Growth in imaging segment revenues is creating growth opportunities

The upward trend in revenues from medical imaging segments presents avenues for angiography devices to integrate into expanding diagnostic portfolios. Increased investments in radiology infrastructure support the deployment of angiography systems in high-volume centers. Strategic partnerships with hospitals facilitate customized solutions for vascular imaging needs.

The large installed base in developed economies amplifies potential for system upgrades. Policy reforms in diagnostic reimbursement bolster investments in interventional suites. Primary corporations are initiating regional hubs to optimize supply chains and reduce logistics costs. This opportunity aligns with efforts to bridge gaps in cardiovascular care through technology.

Focused expansions can capture significant shares in dynamic healthcare landscapes. GE HealthCare reported imaging revenues of $8,855 million in 2023, increasing to $9,245 million in 2024. Siemens Healthineers reported imaging segment adjusted revenues of €11.9 billion in fiscal year 2023, increasing to €12.3 billion in fiscal year 2024.

Impact of Macroeconomic / Geopolitical Factors

Macroeconomic conditions influence the angiography devices market through hospital capital planning, cardiovascular procedure volumes, and reimbursement visibility. Inflation and elevated interest rates increase financing costs for cath lab upgrades, which slows investment in imaging systems and supporting hardware.

Geopolitical tensions disrupt supplies of detectors, semiconductors, contrast injectors, and precision components, raising lead time risk and procurement complexity. Current US tariffs on imported imaging equipment and electronic subassemblies increase acquisition and service costs, which compresses vendor margins and lengthens approval cycles for buyers.

These constraints weigh more heavily on mid sized hospitals and emerging programs. On the positive side, trade pressure encourages regional assembly, supplier diversification, and lifecycle service optimization. Growing incidence of coronary artery disease and demand for minimally invasive interventions sustain strong clinical utilization. With disciplined sourcing, workflow efficiency, and technology driven differentiation, the market remains positioned for stable and confident growth.

Latest Trends

Launch of combined CT-angiography systems is a recent trend in the market

In 2025, the introduction of integrated CT-angiography platforms has enhanced interventional capabilities by allowing seamless switching between modalities in one suite. These systems feature advanced detectors for improved image quality and reduced radiation exposure during procedures. Manufacturers are emphasizing flexibility to support a range of clinical applications from diagnosis to treatment.

Clinical trials in 2025 demonstrated faster workflows with these hybrid configurations. Canon Medical gained FDA clearance for its Alphenix 4D CT system in 2025, combining the Alphenix Sky+ angiography with the Aquilion One/Insight Edition CT. This innovation addresses needs for efficient patient throughput in busy radiology departments.

The trend focuses on interoperability with existing hospital systems for data sharing. Regulatory endorsements in 2025 for combined features have hastened product rollout. Industry collaborations refine software for real-time 3D reconstruction. These developments aim to optimize outcomes in complex vascular interventions.

Regional Analysis

North America is leading the Angiography Devices Market

North America accounted for a 36.3% share of the Angiography Devices market in 2024, supported by high volumes of cardiovascular and neurovascular procedures across advanced hospital networks. Interventional cardiologists expanded use of image guided diagnostics and minimally invasive treatments for coronary artery disease and peripheral vascular disorders.

Aging demographics and lifestyle related risk factors continued to drive procedure growth in both inpatient and outpatient catheterization labs. Hospitals upgraded to flat panel detector systems and hybrid operating rooms to improve imaging precision and workflow efficiency. Reimbursement stability for cardiac interventions strengthened capital investment decisions.

Expansion of ambulatory cardiovascular centers also increased equipment utilization rates. A strong supporting indicator comes from the Centers for Disease Control and Prevention, which reported in 2023 that heart disease remains the leading cause of death in the US, accounting for over 695,000 deaths annually, reinforcing sustained demand for advanced vascular imaging solutions.

The Asia Pacific region is expected to experience the highest CAGR during the forecast period

The Angiography Devices market in Asia Pacific is expected to grow steadily during the forecast period as governments expand cardiac care infrastructure and improve access to interventional treatment. Rising incidence of hypertension, diabetes, and obesity increases the burden of coronary and cerebrovascular diseases.

Public and private hospitals invest in modern catheterization laboratories to address growing patient volumes. Medical tourism in countries such as India and Thailand further strengthens procedural demand. Training programs enhance specialist expertise in minimally invasive vascular interventions. Urbanization and lifestyle changes continue to elevate cardiovascular risk across emerging economies.

A verifiable indicator appears in 2023 data from the World Health Organization, which confirmed that cardiovascular diseases account for nearly one third of total deaths globally, highlighting the strong regional need for diagnostic and interventional vascular imaging technologies.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia

- Netherland

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- New Zealand

- Singapore

- Thailand

- Vietnam

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Key Players Analysis

Key competitors in the angiography devices market grow by advancing imaging clarity, reducing procedure time, and integrating 3D and AI-assisted analytics that help clinicians make faster, more precise decisions during cardiovascular interventions.

They also strengthen customer value by bundling systems with comprehensive service agreements, clinician training programs, and workflow software that enhance operational efficiency for hospitals and cardiac centers. Firms expand commercial reach through strategic alliances with large healthcare networks, diagnostic labs, and group purchasing organizations that secure long-term contracts and preferred supplier status.

Geographic expansion into North America, Europe, and high-growth Asia Pacific supports balanced revenue contributions as demand rises for minimally invasive diagnostics and interventional procedures. Philips Healthcare exemplifies a diversified medical technology leader with a robust portfolio of imaging platforms, deep clinical partnerships, and a coordinated global sales and support infrastructure that aligns innovation with physician needs.

The company advances its market position through disciplined R&D investment, targeted acquisitions that broaden its cardiovascular offerings, and a customer-centric strategy that translates technological progress into tangible clinical and economic value.

Top Key Players

- Siemens Healthineers

- GE HealthCare

- Philips Healthcare

- Canon Medical Systems

- Shimadzu Corporation

- Boston Scientific

- Abbott

- Medtronic

- B. Braun

- Terumo Corporation

Recent Developments

- In October 2024, Shimadzu Corporation introduced SMART Voice, a voice-controlled functionality integrated into its Trinias angiography systems. The feature is designed to streamline catheterization workflows by allowing hands-free system operation, helping clinicians maintain procedural focus while reducing manual interaction. The company plans to showcase the technology at industry events in Kobe, Washington, D.C., and at the RSNA exhibition in Chicago.

- In June 2024, NIDEK CO., LTD. launched the RS-1 Glauvas Optical Coherence Tomography system. Capable of scanning speeds up to 250 kHz, the platform delivers rapid, high-resolution imaging to support glaucoma and retinal vascular disease assessment. The system enhances B-scan clarity and incorporates AngioScan OCT-Angiography technology to improve visualization of chorioretinal microvascular structures, supporting more confident clinical evaluation.

Report Scope

Report Features Description Market Value (2025) US$ 11.9 Billion Forecast Revenue (2035) US$ 21.7 Billion CAGR (2026-2035) 6.2% Base Year for Estimation 2025 Historic Period 2020-2024 Forecast Period 2026-2035 Report Coverage Revenue Forecast, Market Dynamics, COVID-19 Impact, Competitive Landscape, Recent Developments Segments Covered By Product Type (Angiography Systems, Vascular Closure Devices, Guidewires, Contrast Media, Catheters, Balloons and Angiography Accessories), By Application (Diagnostic and Therapeutic), By Technology (X-Ray Angiography, MR Angiography and CT Angiography) Regional Analysis North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, New Zealand, Singapore, Thailand, Vietnam, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA Competitive Landscape Siemens Healthineers, GE HealthCare, Philips Healthcare, Canon Medical Systems, Shimadzu Corporation, Boston Scientific, Abbott, Medtronic, B. Braun, Terumo Corporation Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF)

-

-

- Siemens Healthineers

- GE HealthCare

- Philips Healthcare

- Canon Medical Systems

- Shimadzu Corporation

- Boston Scientific

- Abbott

- Medtronic

- B. Braun

- Terumo Corporation

Our Clients

- 178195

- Feb 2026