Quick Navigation

Report Overview

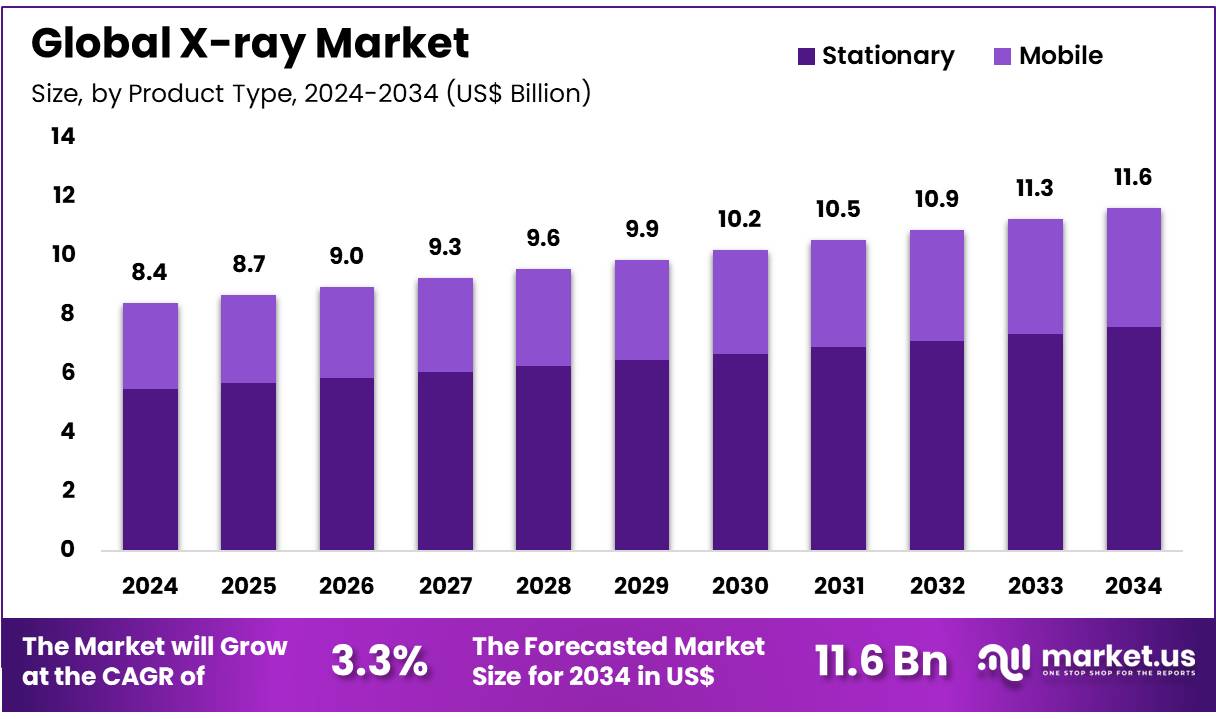

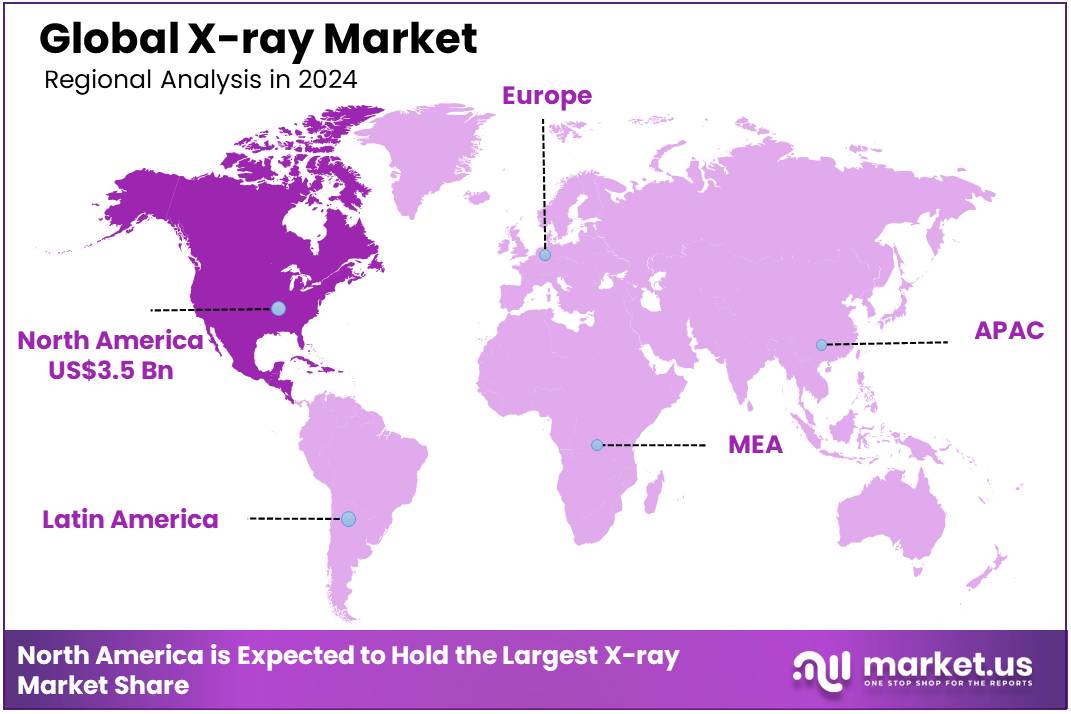

Global X-ray Market size is expected to be worth around US$ 11.6 Billion by 2034 from US$ 8.4 Billion in 2024, growing at a CAGR of 3.3% during the forecast period 2025 to 2034. In 2023, North America led the market, achieving over 41.2% share with a revenue of US$ 3.5 Billion.

Increasing demand for accurate diagnostics and advancements in imaging technology are major drivers of the X-ray market. As healthcare providers seek faster, more precise diagnostic tools, X-ray systems, especially those with integrated AI capabilities, have become indispensable for detecting a variety of conditions, from bone fractures to cancers.

The rise of mobile X-ray systems and portable units has further expanded their use in emergency care and remote settings, offering convenience and accessibility. Additionally, the growing prevalence of chronic diseases and aging populations fuels the need for routine diagnostic imaging.

In November 2021, GE Healthcare obtained FDA approval for its AI-powered algorithm designed to evaluate the placement of Endotracheal Tubes (ETTs). This technology, integrated into mobile X-ray systems, automates measurements, prioritizes cases, and enhances overall image quality control. This trend of incorporating AI into X-ray technology presents significant opportunities for improving diagnostic accuracy and workflow efficiency across healthcare settings.

Key Takeaways

- In 2024, the market for X-ray generated a revenue of US$ 8.4 Billion, with a CAGR of 3.3%, and is expected to reach US$ 11.6 Billion by the year 2033.

- The product type segment is divided into stationary and mobile, with stationary taking the lead in 2023 with a market share of 65.5%.

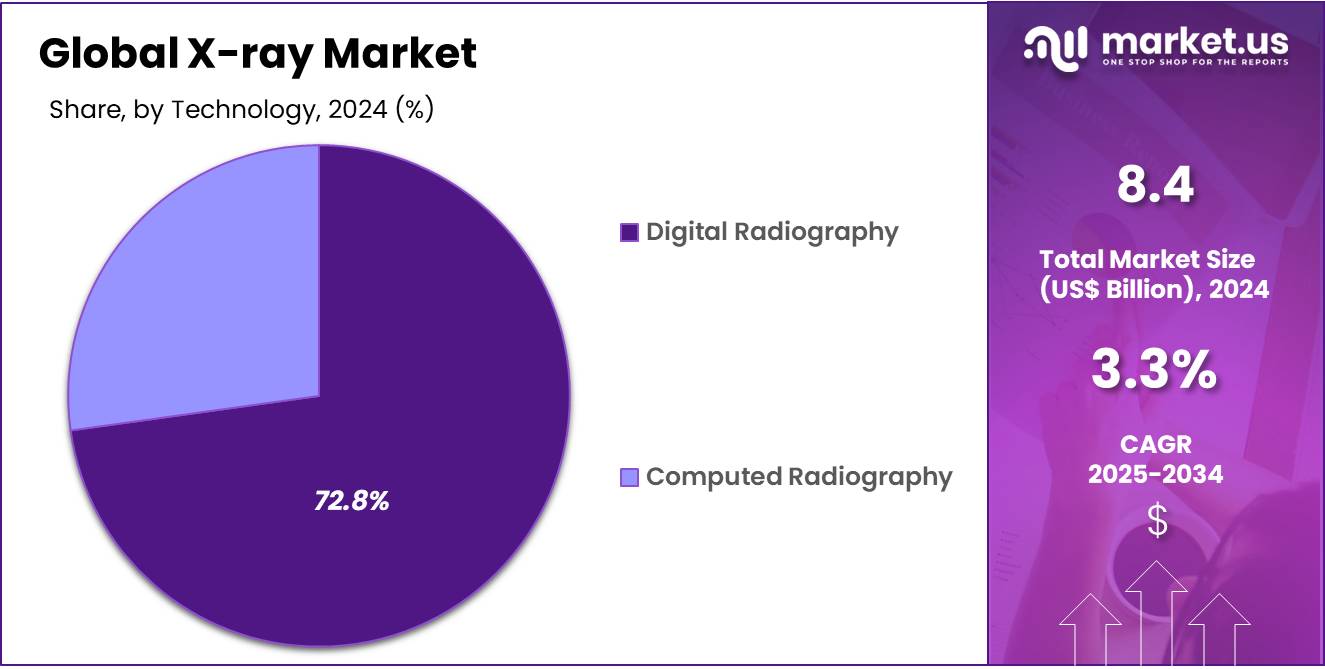

- Considering technology, the market is divided into digital radiography and computed radiography. Among these, digital radiography held a significant share of 72.8%.

- Furthermore, concerning the application segment, the market is segregated into radiography, fluoroscopy, and mammography. The radiography sector stands out as the dominant player, holding the largest revenue share of 58.4% in the X-ray market.

- The end-user segment is segregated into hospitals, diagnostic imaging centres, and others, with the hospitalssegment leading the market, holding a revenue share of 76.3%.

- North America led the market by securing a market share of 41.2% in 2024.

Product Type Analysis

The stationary segment led in 2023, claiming a market share of 65.5% as hospitals, diagnostic centers, and healthcare facilities continue to rely on traditional, high-quality imaging systems for comprehensive diagnostic purposes. Stationary X-ray machines, known for their reliability, high-resolution imaging, and durability, are anticipated to remain popular for routine diagnostic applications, particularly in larger healthcare facilities.

The increasing demand for accurate and detailed imaging, especially in orthopedics, cardiology, and oncology, is likely to drive the growth of stationary systems. Additionally, technological advancements such as digital detectors and enhanced image processing are projected to increase the efficiency and capabilities of stationary X-ray machines, further boosting their adoption in clinical settings.

Technology Analysis

The digital radiography held a significant share of 72.8% due to the increasing demand for faster, more efficient, and higher-quality diagnostic imaging. Digital radiography (DR) systems offer numerous advantages over traditional X-ray technology, including quicker image capture, the ability to enhance and manipulate images, and the reduction of radiation exposure. As healthcare providers seek to improve diagnostic accuracy while reducing patient wait times, DR technology is likely to become the preferred choice.

Furthermore, the integration of DR systems with hospital information systems (HIS) and electronic medical records (EMR) for better workflow management is anticipated to drive the growth of this segment. The growing adoption of DR in both developed and emerging markets is projected to continue expanding the digital radiography segment.

Application Analysis

The radiography segment had a tremendous growth rate, with a revenue share of 58.4% as radiography remains a fundamental diagnostic tool across various medical fields. Radiography is essential for the diagnosis and monitoring of conditions such as fractures, infections, lung diseases, and cardiac conditions. The increasing prevalence of these conditions, coupled with technological advancements in radiography systems, is likely to drive the demand for X-ray systems.

Additionally, the shift towards more advanced imaging techniques, such as digital radiography, which offers improved image quality and faster results, is anticipated to contribute to the growth of the radiography segment. As healthcare providers focus on delivering quicker and more accurate diagnostic results, radiography will continue to be a cornerstone in diagnostic imaging.

End-user Analysis

The hospitalssegment grew at a substantial rate, generating a revenue portion of 76.3% as hospitals remain the primary location for complex diagnostic imaging procedures. Hospitals are projected to continue being the largest users of X-ray technology due to their capacity to handle a wide range of medical conditions and provide comprehensive care. The increasing demand for diagnostic imaging, driven by the rising incidence of chronic diseases and the aging population, is likely to fuel the adoption of X-ray systems in hospitals.

Furthermore, hospitals’ continued investment in advanced imaging technologies, such as digital radiography and mobile X-ray systems, is expected to improve patient care and workflow efficiency. As hospitals seek to enhance diagnostic capabilities and streamline operations, the demand for X-ray systems in these settings is projected to grow.

Key Market Segments

Product Type

- Stationary

- Mobile

Technology

- Digital Radiography

- Computed Radiography

Application

- Radiography

- Fluoroscopy

- Mammography

End-user

- Hospitals

- Diagnostic Imaging Centres

- Others

Drivers

Increasing Demand for Diagnostic Imaging is Driving the Market

The rising prevalence of chronic diseases and an aging population have significantly increased the demand for diagnostic imaging services, thereby driving the X-ray market. In 2023, the global medical X-ray market was valued at approximately US$14.24 billion. This growth is largely attributed to the increasing need for early diagnosis of various medical conditions, including cardiovascular diseases, respiratory disorders, and orthopedic issues.

The adoption of X-ray imaging as a non-invasive and cost-effective diagnostic tool has further fueled its demand across hospitals and diagnostic centers. The versatility and effectiveness of X-ray imaging in detecting a wide range of medical conditions continue to bolster its use.

Additionally, the integration of advanced imaging technologies in healthcare facilities has enhanced the accuracy and speed of diagnosis, supporting market expansion. As the demand for diagnostic services increases globally, the market for X-ray devices is expected to continue to grow.

Restraints

High Equipment Costs are Restraining the Market

Despite technological advancements, the high initial investment and maintenance costs of X-ray equipment pose significant challenges to market growth. The substantial expenses associated with purchasing and maintaining advanced X-ray systems can be prohibitive, especially for healthcare facilities in developing regions. This financial barrier limits the adoption of state-of-the-art imaging technologies, hindering the expansion of diagnostic services.

The cost burden also affects smaller clinics and rural healthcare providers who may struggle to afford the necessary equipment, leading to disparities in access to quality care. Moreover, the need for specialized training to operate sophisticated X-ray machines adds to the overall expenditure, further restraining market growth.

Addressing these challenges requires strategic investments and policies aimed at making X-ray technologies more accessible and affordable to a broader range of healthcare providers. Without effective cost-management solutions, the market’s potential will remain limited in certain regions.

Opportunities

Technological Advancements in Digital X-ray Systems are Creating Growth Opportunities

Advancements in digital X-ray technology present significant growth opportunities in the market. Digital systems offer numerous advantages over traditional analog methods, including reduced radiation exposure, faster image processing, and enhanced image quality. Digital radiography has improved accessibility and efficiency, driving its adoption across hospitals, clinics, and diagnostic centers.

These technologies not only enhance patient outcomes by providing clearer images but also help healthcare providers make quicker decisions, particularly in emergency settings. Furthermore, the integration of advanced medical imaging technologies into digital X-ray systems improves patient care by offering more accurate diagnoses.

The rise of wireless digital systems is also improving workflow efficiency in healthcare environments. As digital X-ray technology continues to evolve, the market is poised for expansion, with increasing demand for these advanced solutions that offer a range of benefits, including ease of use, better patient comfort, and improved image quality.

Impact of Macroeconomic / Geopolitical Factors

Macroeconomic and geopolitical factors significantly influence the X-ray market. Economic downturns can lead to reduced healthcare budgets, limiting investments in advanced imaging technologies. In contrast, periods of economic growth often result in increased healthcare spending, which boosts the adoption of state-of-the-art X-ray systems.

Geopolitical stability encourages international collaboration and the distribution of medical technologies, ensuring consistent availability of necessary devices worldwide. However, geopolitical tensions can disrupt global supply chains, leading to shortages or delays in obtaining critical components for X-ray machines, which may hinder diagnostic services. Additionally, changes in healthcare regulations or tariffs in different regions can affect the availability and cost of imaging devices.

Cultural attitudes towards preventive healthcare can also influence market demand, as regions emphasizing routine screening will likely see higher demand for X-ray services. Despite these challenges, the ongoing trend toward digitalization in medical imaging and the growing demand for portable X-ray solutions provide promising growth opportunities, enhancing access to diagnostic imaging across diverse patient populations.

Latest Trends

Shift Towards Portable and Point-of-Care X-ray Solutions is a Recent Trend

A notable recent trend in the X-ray market is the increasing demand for portable and point-of-care imaging solutions. Portable X-ray devices offer flexibility and convenience, allowing for imaging in various settings, including emergency rooms, intensive care units, and remote locations. The portability of these devices enables healthcare providers to conduct immediate diagnostic imaging on-site, reducing the time needed for patient transfer and diagnosis.

The increased adoption of portable X-ray systems is driven by the need for rapid and accessible diagnostic imaging, particularly in critical care scenarios. In 2023, portable X-ray devices represented a substantial segment of the medical imaging market.

The trend towards portability is expected to continue growing, as these devices allow healthcare providers to offer timely imaging results, thereby improving clinical decision-making and patient outcomes. As healthcare facilities increasingly look for solutions that can accommodate high mobility and efficiency, portable X-ray systems are becoming a key component of modern medical practices.

Regional Analysis

North America is leading the X-ray Market

North America dominated the market with the highest revenue share of 41.2% owing to several key factors. A significant contributor was the increasing prevalence of chronic diseases, leading to a higher demand for diagnostic imaging services. Technological advancements in X-ray systems, such as the development of digital radiography, enhanced image quality and efficiency, attracting more healthcare facilities to adopt these systems.

For instance, the digital radiography segment dominated the market with a revenue of US$6.2 billion in 2023, and continued to grow in 2024. Additionally, the rising geriatric population in North America necessitated more frequent medical imaging, further boosting the market. Government initiatives aimed at improving healthcare infrastructure and funding for advanced medical equipment also played a role in market expansion.

Major players like Siemens Healthineers and GE Healthcare contributed to market growth by introducing innovative X-ray solutions, enhancing diagnostic capabilities, and meeting the evolving needs of healthcare providers. These factors collectively resulted in a robust growth trajectory for the X-ray market in North America throughout 2024.

The Asia Pacific region is expected to experience the highest CAGR during the forecast period

Asia Pacific is expected to grow with the fastest CAGR owing to the increasing demand for diagnostic imaging services, driven by a rising geriatric population and a higher prevalence of chronic diseases. Technological advancements in X-ray equipment, such as the development of portable and digital systems, are expected to enhance accessibility and efficiency, particularly in rural and underserved areas.

For example, the Asia Pacific portable X-ray devices market size is estimated at US$1.54 billion in 2024, projected to reach US$2.57 billion by 2029. Government initiatives aimed at improving healthcare infrastructure and increasing healthcare spending are likely to facilitate the adoption of advanced X-ray technologies.

Major companies like Canon Inc., Fujifilm Holdings Corporation, and Siemens AG are actively participating in the market, introducing innovative products tailored to the needs of the Asia-Pacific region. These factors are expected to contribute to the significant growth of the X-ray market in the Asia-Pacific region during the forecast period.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia

- Netherland

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- New Zealand

- Singapore

- Thailand

- Vietnam

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Key Players Analysis

Key players in the X-ray market focus on technological innovation, product diversification, and strategic partnerships to drive growth. They invest in the development of advanced imaging systems, such as digital radiography and portable X-ray machines, to improve diagnostic accuracy and accessibility.

Companies also collaborate with healthcare institutions and research organizations to expand their market presence and enhance product offerings. They target emerging markets with growing healthcare infrastructures and rising demand for medical imaging. Additionally, regulatory approvals and investments in artificial intelligence integration are helping to streamline processes and enhance patient outcomes.

Siemens Healthineers, headquartered in Erlangen, Germany, is a global leader in medical technology and imaging solutions. The company offers a wide range of advanced diagnostic equipment, including state-of-the-art X-ray systems. Siemens Healthineers continues to innovate by integrating artificial intelligence into its imaging solutions, improving diagnostic accuracy and efficiency.

The company has a strong global presence, with a focus on expanding into emerging markets and providing tailored solutions for healthcare providers. Through strategic acquisitions and partnerships, Siemens Healthineers maintains its position as a key player in the diagnostic imaging sector.

Top Key Players

- Siemens Healthineers AG

- Shimadzu Corporation

- New Medical Imaging

- Konica Minolta

- GE Healthcare

- Carestream

- Canon Medical Systems

- AGFA

Recent Developments

- In April 2024, Shimadzu expanded its operations on the West Coast of the US by acquiring California X-ray Imaging Services, Inc. This acquisition aims to enhance the company’s direct sales capabilities for medical systems in this strategic region.

- In March 2022, Konica Minolta launched the AeroDR TX m01, a portable X-ray system equipped with wireless dynamic digital radiography features. This innovation was rolled out in Japan to provide greater mobility and efficiency in medical imaging.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2024) | US$ 8.4 billion |

| Forecast Revenue (2034) | US$ 11.6 billion |

| CAGR (2025-2034) | 3.3% |

| Base Year for Estimation | 2024 |

| Historic Period | 2020-2023 |

| Forecast Period | 2025-2034 |

| Report Coverage | Revenue Forecast, Market Dynamics, COVID-19 Impact, Competitive Landscape, Recent Developments |

| Segments Covered | By Product Type (Stationary and Mobile), By Technology (Digital Radiography and Computed Radiography), By Application (Radiography, Fluoroscopy, and Mammography), By End-user (Hospitals, Diagnostic Imaging Centres, and Others) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, New Zealand, Singapore, Thailand, Vietnam, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA |

| Competitive Landscape | Siemens Healthineers AG, Shimadzu Corporation, New Medical Imaging, Konica Minolta, GE Healthcare, Carestream, Canon Medical Systems, and AGFA. |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |