Global Activated Carbon Market Size, Share, And Industry Analysis Report By Raw Material (Coal-Based, Coconut Shell Based, Wood Based), By Form (Powdered Activated Carbon, Granular Activated Carbon, Extruded Pelletised Activated Carbon), By Application (Drinking Water Treatment, Decolorisation Treatment, Sugar Production, Concentration Treatment, Solvent Recovery), By End-User (Water Treatment, Industrial Processing, Healthcare, Food and Beverage, Automotive), By Region and Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Statistics, Trends and Forecast 2025-2034

- Published date: February 2026

- Report ID: 178713

- Number of Pages: 327

- Format:

-

keyboard_arrow_up

Quick Navigation

Report Overview

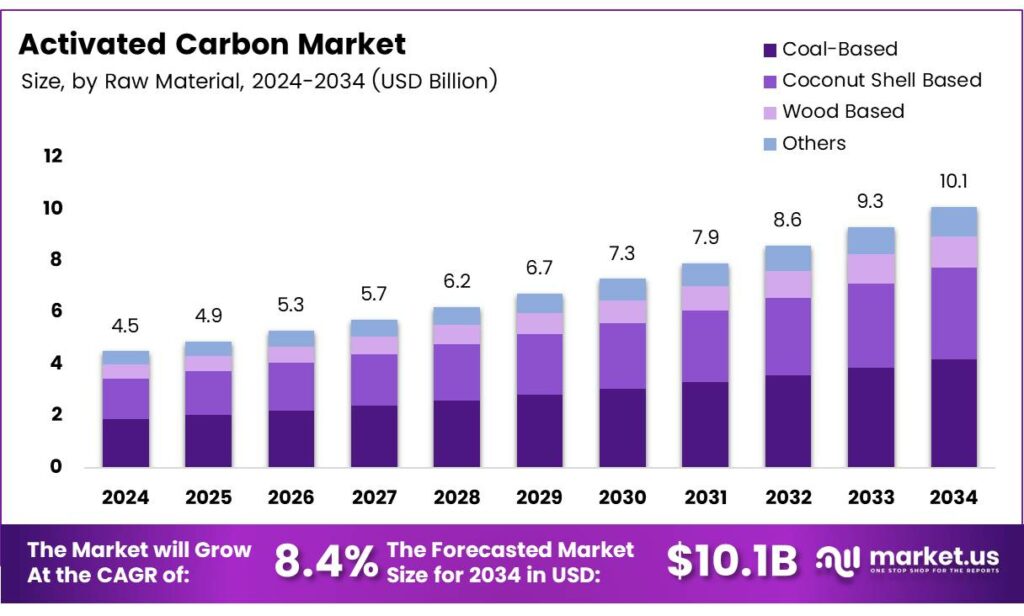

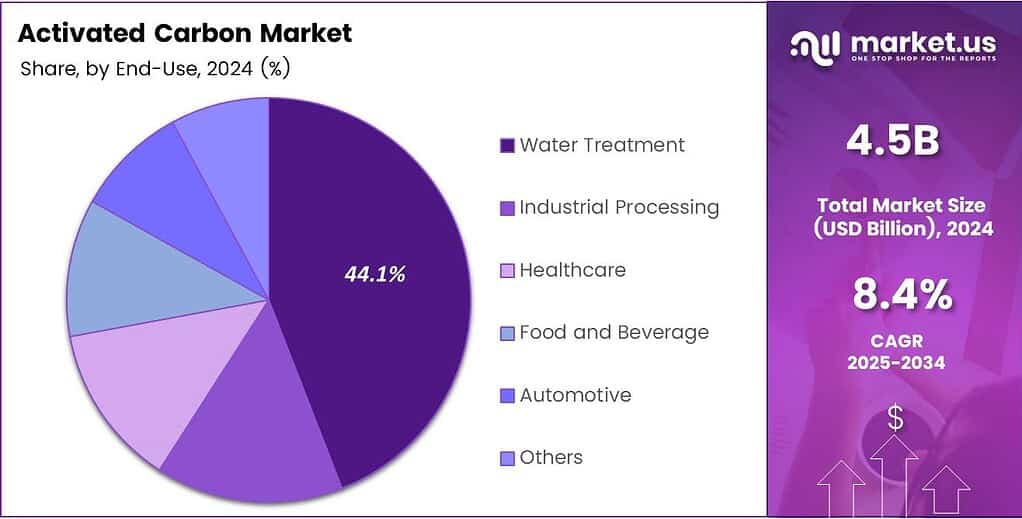

The Global Activated Carbon Market size is expected to be worth around USD 10.1 billion by 2034 from USD 4.5 billion in 2024, growing at a CAGR of 8.4% during the forecast period 2025 to 2034.

Activated carbon is a highly porous material that removes contaminants, toxins, and impurities from liquids and gases. Industries use it widely across water treatment, food processing, healthcare, and automotive sectors. Its exceptional adsorption capacity makes it one of the most versatile purification materials available in global markets today.

Water treatment plants drive the largest share of activated carbon demand globally. Municipalities and industrial facilities rely on these carbon-based filtration materials to meet increasingly strict environmental standards. Consequently, expanding urban populations and growing industrial wastewater volumes continue to push demand for advanced water purification solutions upward year after year.

- Global trade data highlights the scale of this industry. Global imports of activated carbon reached $2.08 billion, based on trade statistics from over 131 reporting countries, reflecting consistent international demand despite a year-on-year decline from $2.53 billion.

- Key supplier nations demonstrate strong export capacity. India exported activated carbon worth $242.2 million, covering 141.9 million kilograms, confirming its position as one of the top global suppliers. Furthermore, Sri Lanka exported $133.6 million worth of activated carbon, underlining South Asia’s critical role in global supply chains for coconut-shell-based carbon products.

The food and beverage industry also contributes meaningfully to market expansion. Manufacturers use carbon-based purification solutions for decolorization, deodorization, and sugar refining processes. Additionally, pharmaceutical companies increasingly adopt activated carbon for medicinal purification and dialysis applications, further broadening the addressable market for producers worldwide.

Key Takeaways

- The Global Activated Carbon Market is valued at USD 4.5 billion in 2024 and is projected to reach USD 10.1 billion by 2034, at a CAGR of 8.4% during the forecast period 2025 to 2034.

- Coal-Based activated carbon dominates with a 48.5% market share in 2025.

- Powdered Activated Carbon (PAC) leads with a 49.7% share in 2025.

- Drinking Water Treatment holds the largest share at 51.4% in 2025.

- Water Treatment accounts for 44.1% of the market share in 2025.

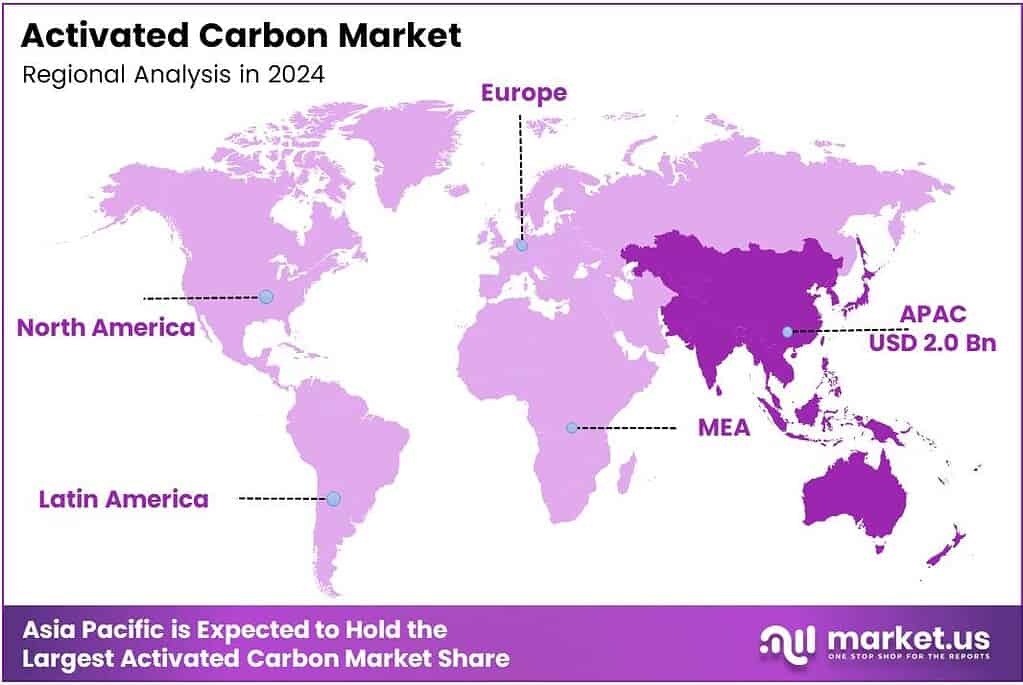

- Asia Pacific dominates the regional landscape with a 44.9% market share, valued at USD 2.0 billion.

By Raw Material Analysis

Coal-Based activated carbon dominates with 48.5% due to its abundant availability and cost-effectiveness in large-scale industrial applications.

In 2025, Coal-Based activated carbon held a dominant market position in the By Raw Material segment of the Activated Carbon Market, with a 48.5% share. Coal feedstocks offer high carbon content and consistent adsorption performance. Moreover, coal-based variants suit large-scale industrial and water treatment applications where volume and cost efficiency are primary procurement criteria.

Coconut Shell-Based activated carbon commands strong demand due to its superior micropore structure and hardness. Additionally, environmental sustainability preferences drive buyers toward this renewable raw material. Coconut shell carbon performs exceptionally well in drinking water treatment and PFAS adsorption, making it a preferred choice in high-purity filtration applications across developed markets.

Wood-based activated carbon offers a larger pore size distribution suitable for decolorization and liquid-phase applications. Food and beverage manufacturers frequently select this variant for sugar refining and pharmaceutical purification processes. However, wood-based carbon holds a smaller market share compared to coal and coconut shell alternatives due to lower adsorption density.

Others in the raw material segment include peat and petroleum coke-based carbons. These materials serve niche industrial applications where specific pore characteristics are required. Consequently, their market contribution remains limited, though specialty chemical producers continue exploring alternative feedstocks to reduce dependency on conventional raw materials.

By Form Analysis

Powdered Activated Carbon (PAC) dominates with 49.7% due to its versatility and ease of use in liquid-phase treatment processes.

In 2025, Powdered Activated Carbon (PAC) held a dominant market position in the By Form segment of the Activated Carbon Market, with a 49.7% share. PAC integrates easily into existing water treatment infrastructure without requiring major equipment changes. Moreover, its fine particle size maximizes surface contact with contaminants, delivering fast and effective adsorption in municipal and industrial treatment systems.

Granular Activated Carbon (GAC) serves as the preferred form for continuous flow filtration systems, including fixed-bed and moving-bed reactors. Water utilities and industrial operators widely adopt GAC because it supports on-site reactivation and reuse, reducing long-term operational costs. Additionally, GAC performs reliably in PFAS removal applications, driving its growing adoption in regulated markets.

Extruded Pelletised Activated Carbon (EAC) finds primary application in gas-phase treatments, including air purification, automotive canisters, and industrial gas cleaning. Its cylindrical pellet structure delivers low pressure drop and high mechanical strength. Therefore, automotive manufacturers and industrial gas processors favor EAC for emission control and cabin air filtration systems requiring durable, long-lasting carbon media.

By Application Analysis

Drinking Water Treatment dominates with 51.4% as municipalities worldwide prioritize clean water access and regulatory compliance.

In 2025, Drinking Water Treatment held a dominant market position in the By Application segment of the Activated Carbon Market, with a 51.4% share. Water utilities globally use activated carbon to remove organic compounds, chlorine, and emerging contaminants from drinking water supplies. Consequently, stricter PFAS regulations across North America and Europe continue to fuel procurement volumes in this application segment.

Decolorisation Treatment applications cover a wide range of industrial processes where color removal from liquids is essential. Food manufacturers, textile producers, and chemical processors use activated carbon extensively for this purpose. Moreover, demand in this segment grows steadily as quality standards for consumer products tighten across global markets.

Sugar Production relies on activated carbon to remove colorants and impurities from raw sugar liquor during refining. Sugar mills in major producing countries such as Brazil, India, and Thailand maintain consistent demand for powdered and granular carbon types. Additionally, rising global sugar consumption supports sustained procurement activity within this application category.

Concentration Treatment and Solvent Recovery applications use activated carbon to capture and recover valuable solvents in chemical and pharmaceutical manufacturing. These processes reduce waste and lower production costs. Furthermore, PFAS Adsorption Treatment is rapidly emerging as a high-growth application as governments mandate remediation of per- and polyfluoroalkyl substance contamination in soil and groundwater globally.

By End-User Analysis

Water Treatment dominates with 44.1% as utilities and municipalities represent the single largest end-user base for activated carbon globally.

In 2025, Water Treatment held a dominant market position in the By End-User segment of the Activated Carbon Market, with a 44.1% share. Municipal water authorities and industrial wastewater treatment facilities consume the largest volumes of activated carbon annually. Moreover, regulatory pressure from bodies such as the U.S. EPA and the EU Water Framework Directive continues to expand carbon-based filtration requirements across public and private water systems.

Industrial Processing end-users span chemicals, mining, and petroleum refining sectors that rely on activated carbon for process purification and emissions control. These industries consume significant volumes of granular and extruded carbon forms. Additionally, stricter air quality regulations drive the adoption of activated carbon in industrial gas cleaning and stack emissions treatment systems worldwide.

Healthcare end-users include pharmaceutical manufacturers and dialysis equipment producers that use high-purity activated carbon for medicinal applications. Demand growth in this segment aligns with global healthcare expansion and rising investments in renal care infrastructure. Furthermore, the Food and Beverage and Automotive sectors contribute to growing volumes as producers upgrade purification standards and emission control technologies, respectively.

Key Market Segments

By Raw Material

- Coal-Based

- Coconut Shell-Based

- Wood Based

- Others

By Form

- Powdered Activated Carbon (PAC)

- Granular Activated Carbon (GAC)

- Extruded Pelletised Activated Carbon (EAC)

By Application

- Drinking Water Treatment

- Decolorisation Treatment

- Sugar Production

- Concentration Treatment

- Solvent Recovery

- PFAS Adsorption Treatment

- Others

By End-User

- Water Treatment

- Industrial Processing

- Healthcare

- Food and Beverage

- Automotive

- Others

Emerging Trends

Regenerable Systems and Specialty Carbon Technologies Transform the Activated Carbon Industry

Water utilities and industrial operators are increasingly transitioning to regenerable granular activated carbon systems featuring on-site reactivation facilities. These setups reduce replacement costs and lower carbon footprints significantly. Moreover, in 2025, Calgon Carbon agreed to acquire the reactivated carbon business of Sprint Environmental Services, LLC, reinforcing industry movement toward circular carbon management and sustainable water treatment operations.

Coconut-shell-derived activated carbon gains strong traction for high-performance PFAS contaminant removal in hotspot remediation zones. Regulatory agencies across the U.S. and Europe designate PFAS as priority contaminants, accelerating procurement of specialized coconut-shell carbons. Additionally, impregnated and nano-activated carbons are emerging for targeted industrial pollutant capture where conventional grades cannot achieve required performance thresholds.

Circular economy practices now shape product development strategies across the activated carbon industry. Manufacturers invest in low-carbon footprint production methods and waste-to-resource feedstock programs. Furthermore, producers explore energy storage and battery applications for specialty activated carbons, opening entirely new end-use segments beyond traditional environmental and purification markets that have historically defined this industry.

Drivers

Stringent Environmental Regulations and Rising Clean Water Demand Fuel Activated Carbon Market Growth

Governments worldwide enforce stricter regulations mandating mercury removal, PFAS remediation, and volatile organic compound reduction in water and air treatment systems. Regulatory agencies such as the U.S. EPA continuously tighten permissible contaminant limits. Consequently, municipalities and industrial operators expand their activated carbon procurement budgets to achieve and maintain compliance with these evolving environmental standards.

- Rapid urbanization and industrialization across Asia, Africa, and Latin America intensify demand for clean water and effective wastewater treatment solutions. Growing city populations strain existing treatment infrastructure, prompting investments in new carbon-based filtration capacity. Ingevity Corporation’s Performance Materials segment, which includes automotive activated carbon products, recorded net sales of $609.6 million in 2024, reflecting robust commercial demand in this application area.

The automotive industry drives consistent demand for activated carbon through cabin air filtration and fuel vapor emission control applications. Vehicle manufacturers integrate carbon-based canisters to meet increasingly stringent evaporative emission standards. Additionally, growing food and beverage sector requirements for decolorization, deodorization, and purification of consumables sustain stable long-term procurement volumes across multiple global markets.

Restraints

Raw Material Scarcity and High Production Costs Limit Activated Carbon Market Accessibility

Acute scarcity of key feedstocks such as coconut shells and high-quality coal creates persistent supply pressure across the activated carbon industry. Seasonal harvesting cycles, weather events, and competing agricultural demands frequently disrupt coconut shell availability. Moreover, price volatility in these raw materials forces manufacturers to revise product pricing, which challenges cost-sensitive buyers in price-competitive procurement environments.

Elevated production costs associated with high-temperature activation processes and energy-intensive manufacturing significantly impact profit margins. Smaller producers and buyers in developing regions face particular difficulty absorbing these costs. Additionally, global supply chain disruptions expose activated carbon manufacturers to logistics delays and input shortages that reduce production reliability and limit market accessibility for emerging-market customers.

Developing regions often lack the infrastructure required to support advanced activated carbon manufacturing and distribution networks. High capital expenditure requirements for activation furnaces and quality control systems create barriers for new market entrants. Therefore, market consolidation among established global players intensifies, while smaller regional producers struggle to compete effectively on both quality and volume delivery commitments.

Growth Factors

Reactivation Technologies and New Application Sectors Accelerate Activated Carbon Market Expansion

Reactivated carbon technologies enable producers and end-users to recover and reuse spent activated carbon at significantly lower costs than virgin material procurement. This approach supports sustainability goals while reducing total operating expenditure for water utilities and industrial processors. In 2025, Kemira Oyj completed the acquisition of Norit’s UK reactivation operations, signaling strong industry investment in circular carbon recovery infrastructure.

- The European Union imported activated carbon worth $443.3 million, making it the world’s largest regional importer by value. This scale of demand reflects both existing infrastructure needs and ongoing regulatory-driven procurement. Additionally, energy storage and battery application development for specialty carbons opens new revenue streams beyond conventional environmental purification markets for forward-looking activated carbon producers.

Pharmaceutical and healthcare sectors represent high-value growth opportunities for specialty activated carbon producers. Dialysis purification, medicinal poison treatment, and drug manufacturing processes require ultra-pure carbon grades that command premium pricing. Furthermore, biogas upgrading and renewable energy scrubbing applications create rising demand for activated carbon in gas purification systems, supporting global clean energy transitions.

Regional Analysis

Asia Pacific Dominates the Activated Carbon Market with a Market Share of 44.9%, Valued at USD 2.0 Billion

Asia Pacific leads the global activated carbon market, holding a 44.9% share valued at USD 2.0 billion. China, India, Japan, and South Korea drive the region’s dominance through large-scale water treatment investments and robust industrial manufacturing activity. Moreover, the region hosts major coconut-shell activated carbon producers in Sri Lanka, the Philippines, and Indonesia, making it both a leading producer and consumer globally.

North America represents one of the most regulated and high-value markets for activated carbon worldwide. The United States enforces rigorous PFAS and mercury removal standards that sustain strong domestic demand. Reflecting its dual role as both a major importer and a significant global exporter of high-value carbon materials.

Europe maintains strict environmental and drinking water quality directives that underpin consistent activated carbon demand across the region. Germany, France, and the UK function as primary consumption centers within the European market. Furthermore, the EU’s focus on PFAS remediation and circular economy principles accelerates investment in reactivation facilities and advanced carbon-based purification technologies throughout the continent.

The Middle East and Africa region presents growing opportunities for activated carbon suppliers as water scarcity concerns intensify across arid zones. Gulf Cooperation Council nations invest in desalination and industrial water treatment infrastructure that utilizes activated carbon. However, market penetration remains limited by high import costs and underdeveloped local manufacturing capacity compared to more mature regional markets.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

Kuraray Co., Ltd. operates as a leading global activated carbon producer through its Functional Materials segment, which includes the Calgon Carbon business. Kuraray’s broad product portfolio and strong presence in water treatment and industrial purification markets position it as a top-tier supplier globally.

Norit holds a well-established position in the global activated carbon industry, particularly across European water treatment and food-grade purification markets. The company operates reactivation facilities that support circular carbon recovery for both potable water and industrial applications. Its reactivation business in the UK, recently acquired by Kemira Oyj in 2025, highlights Norit’s strategic infrastructure assets across European purification supply chains.

Albemarle Corporation maintains a diversified portfolio of specialty chemicals, including activated carbon and related purification materials. The company serves energy storage, refining, and environmental markets with high-performance carbon solutions. Albemarle’s global manufacturing footprint and technical expertise in advanced materials position it competitively across multiple activated carbon application segments, including industrial processing and environmental remediation.

Tronox Holdings Plc participates in the activated carbon and specialty minerals market through its advanced materials operations. The company focuses on delivering high-purity industrial solutions across multiple sectors, including environmental and chemical processing markets. Tronox’s integration of mineral processing expertise with specialty chemical production supports its ability to serve diverse activated carbon end-user industries across global markets.

Top Key Players in the Market

- Kuraray Co., Ltd.

- Norit

- Albemarle Corporation

- Tronox Holdings Plc

- Osaka Gas Chemicals Co., Ltd.

- Kureha Corporation

- Ingevity Corporation

- Evoqua Water Technologies LLC

- Haycarb PLC

- Iluka Resources Limited

Recent Developments

- In 2025, Calgon Carbon agreed to acquire the industrial reactivated carbon business of Sprint Environmental Services, LLC, including a reactivation plant near Houston, Texas (Gulf of Mexico region), 21 employees, and related assets. The move addresses growing demand for reactivated carbon in industrial applications and supports expansion for drinking water treatment amid tightening U.S. PFAS regulations.

- In 2025, Kemira Oyj completed the acquisition of Norit’s UK reactivation operations. This includes a reactivation facility in Purton, UK, that regenerates spent granular or pelletized activated carbon for reuse in potable water/food applications (Green reactivation) and non-food (Amber).

Report Scope

Report Features Description Market Value (2024) USD 4.5 Billion Forecast Revenue (2034) USD 10.1 Billion CAGR (2025-2034) 8.4% Base Year for Estimation 2024 Historic Period 2020-2023 Forecast Period 2025-2034 Report Coverage Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments Segments Covered By Raw Material (Coal-Based, Coconut Shell Based, Wood Based, Others), By Form (Powdered Activated Carbon (PAC), Granular Activated Carbon (GAC), Extruded Pelletised Activated Carbon (EAC)), By Application (Drinking Water Treatment, Decolorisation Treatment, Sugar Production, Concentration Treatment, Solvent Recovery, PFAS Adsorption Treatment, Others), By End-User (Water Treatment, Industrial Processing, Healthcare, Food and Beverage, Automotive, Others) Regional Analysis North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East & Africa (GCC, South Africa, and Rest of MEA) Competitive Landscape Kuraray Co., Ltd., Norit, Albemarle Corporation, Tronox Holdings Plc, Osaka Gas Chemicals Co., Ltd., Kureha Corporation, Ingevity Corporation, Evoqua Water Technologies LLC, Haycarb PLC, Iluka Resources Limited Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited Users and Printable PDF)  Activated Carbon MarketPublished date: February 2026add_shopping_cartBuy Now get_appDownload Sample

Activated Carbon MarketPublished date: February 2026add_shopping_cartBuy Now get_appDownload Sample -

-

- Kuraray Co., Ltd.

- Norit

- Albemarle Corporation

- Tronox Holdings Plc

- Osaka Gas Chemicals Co., Ltd.

- Kureha Corporation

- Ingevity Corporation

- Evoqua Water Technologies LLC

- Haycarb PLC

- Iluka Resources Limited

Our Clients

- 178713

- February 2026