Quick Navigation

Report Overview

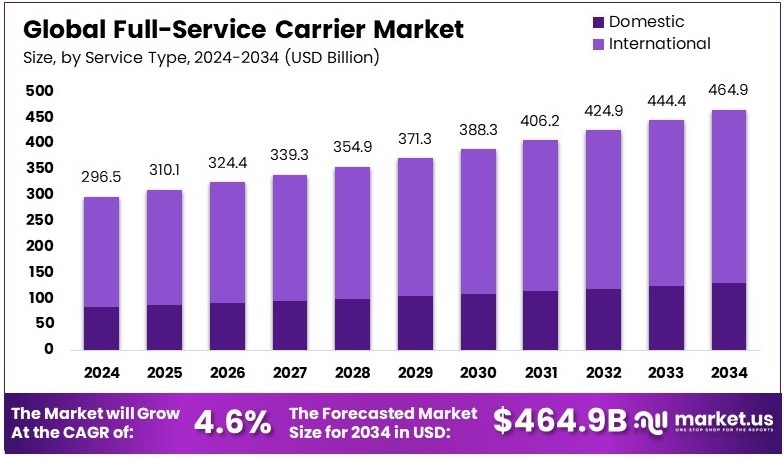

The Global Full-Service Carrier Market size is expected to be worth around USD 464.9 Billion by 2034, from USD 296.5 Billion in 2024, growing at a CAGR of 4.6% during the forecast period from 2025 to 2034.

Full-Service Carrier is a transportation provider managing complete shipping processes. It offers a wide range of services including freight, warehousing, and delivery. The firm handles all aspects of logistics. Clients benefit from integrated solutions that cover transportation needs. The service is reliable, comprehensive, and designed to support complex supply chains.

Full-Service Carrier Market consists of companies offering comprehensive logistics and transportation solutions. Firms in this market manage shipping, warehousing, and freight services. They provide integrated supply chain management to various industries. Companies focus on dependable service and complete logistical support. The market caters to businesses requiring efficient transportation solutions globally.

The Full-Service Carrier market is thriving as airlines recover post-pandemic, with American Airlines reporting $54.2 billion and Delta Air Lines $61.6 billion in annual revenues for 2024. Furthermore, IndiGo plans to increase its international destinations to 40 by March 2025, up from 26, strengthening its global presence and enhancing connectivity.

Additionally, the global air travel demand soared to new heights in 2024, with total passenger traffic increasing by 10.4% over 2023, and capacity growth at 8.7%. This led to a record-high load factor of 83.5%, signaling robust market health and high efficiency in seat utilization. The International Air Transport Association (IATA) noted this trend reflects a recovery surpassing pre-pandemic levels by 3.8%.

On a broader scale, challenges like aircraft shortages and economic uncertainties persist, yet the industry remains resilient. For instance, despite these hurdles, rising airfares contributed significantly to profitability, with U.S. airfares in December 2024 seeing their fastest rise in 21 months.

European ticket prices also saw a 6% increase year-on-year, showcasing the sector’s ability to adapt and capitalize on market conditions. Government regulations continue to influence industry standards and practices, ensuring safety and sustainability in operations.

Key Takeaways

- The Full-Service Carrier Market was valued at USD 296.5 billion in 2024 and is projected to reach USD 464.9 billion by 2034, with a CAGR of 4.6%.

- In 2024, International dominates the service type segment with 73.2%, driven by global connectivity and expanding cross-border travel demand.

- In 2024, Economy leads the flight class segment with 80.3%, reflecting its widespread popularity among cost-conscious travelers worldwide.

- In 2024, Wide-body dominates the aircraft type segment with 67.5%, owing to its efficiency in long-haul international flights.

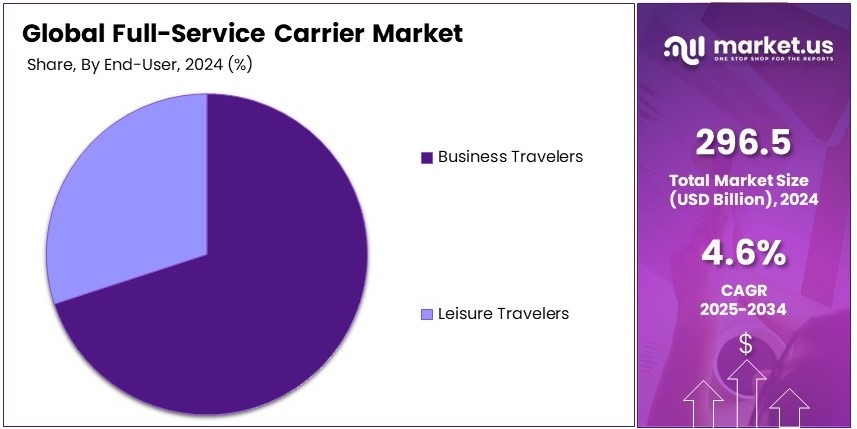

- In 2024, Business Travelers drive the end-user segment, emphasizing the growing demand for premium travel experiences across multiple continents.

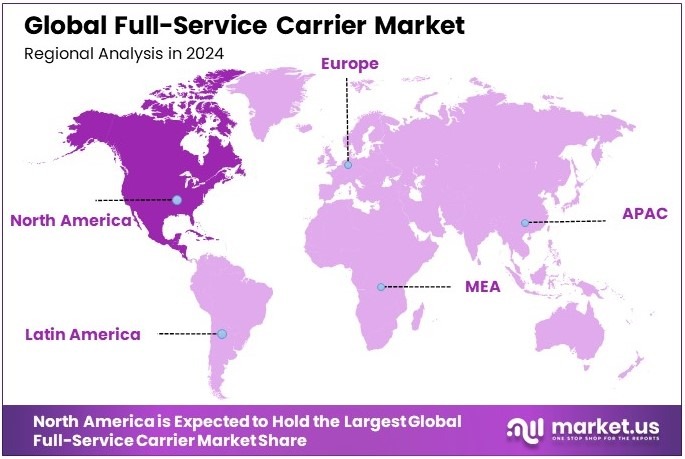

- In 2024, North America leads the regional segment, leveraging robust air travel infrastructure and high passenger demand effectively.

Service Type Analysis

International sub-segment dominates with 73.2% due to increased global connectivity and economic integration.

The International service type is the dominant force in the Full-Service Carrier Market, largely because of the expanded global interactions in business and tourism. Airlines operating internationally benefit from the broader reach and higher revenue opportunities provided by long-haul flights, which typically command premium pricing and higher yields.

This sub-segment’s growth is fueled by global economic integration, making international travel more necessary and frequent for both business and leisure travelers.

Domestic services, while essential, focus on shorter routes within the same country. These flights are crucial for connecting smaller cities to major hubs, facilitating local commerce and advanced air mobility. They contribute to the market by serving as feeders to international flights, integrating regional traffic into global travel networks.

Flight Class Analysis

Economy class dominates with 80.3% due to its affordability and broad appeal to the general population.

Economy class is the backbone of the Full-Service Carrier Market, primarily due to its accessibility and affordability, which appeal to the widest audience.

The majority of travelers opt for economy class, driven by the competitive pricing and improved service offerings that full-service carriers provide over budget airlines. This class’s dominance is also supported by enhanced seating comfort and in-flight services that have become more sophisticated over time.

Business class offers a more refined experience with additional amenities and services targeted at business travelers or those seeking more comfort. It provides significant revenue per passenger for airlines due to higher ticket prices.

First class, although the least dominant, caters to the luxury segment of the market, offering premium services and exclusive experiences. It remains important for brand prestige and differentiation in the competitive airline market.

Aircraft Type Analysis

Wide-body aircraft dominate with 67.5% due to their capacity to handle long-haul international flights efficiently.

Wide-body aircraft are crucial in the Full-Service Carrier Market, especially for international routes where their high capacity and long-range capabilities are necessary. These aircraft types are preferred by airlines for their efficiency in carrying more passengers per flight, which reduces the cost per seat-mile, making them economically viable for long-distance routes.

Narrow-body aircraft, while less dominant in this segment, are indispensable for domestic and short-haul international flights. Their versatility and lower operational costs make them suitable for routes with less demand or shorter distances.

End-User Analysis

Business travelers dominate the end-user segment due to their frequent and regular travel patterns.

Business travelers are the primary market for full-service carriers, as they often travel frequently and value the additional services such as lounge access, extra baggage allowances, and flexible ticketing that full-service carriers offer. This group’s consistent travel frequency ensures steady demand and revenue for airlines.

Leisure travelers, although a larger group in volume, tend to be more price-sensitive and fluctuate seasonally. They contribute to filling capacity but are less consistent as a customer base compared to business travelers.

Key Market Segments

By Service Type

- Domestic

- International

By Flight Class

- Economy

- Business

- First Class

By Aircraft Type

- Narrow-body Aircraft

- Wide-body Aircraft

By End-User

- Leisure Travelers

- Business Travelers

Driving Factors

Air Travel Expansion Drives Market Growth

Global air travel demand continues to surge as more people seek convenient ways to connect across continents. The expanding middle‐class population drives this trend, with increased disposable income leading to more frequent travel. Airlines improve network connectivity by offering multiple flight routes and enhancing passenger experiences.

New services such as in‐flight entertainment, gourmet meals, and comfortable seating boost customer satisfaction. Strategic alliances and code‐sharing agreements help carriers reach broader markets, enabling seamless travel across regions and continents, and creating a robust global network.

In addition, carriers adopt fuel‐efficient aircraft and sustainable aviation initiatives to reduce costs and environmental impact. Newer aircraft models lower fuel consumption and emit fewer greenhouse gases. This technological advancement supports both profitability and regulatory compliance.

Airlines invest in modern fleets and innovative practices to meet growing environmental standards while improving operational efficiency. As a result, passengers enjoy more reliable schedules and better service quality.

Restraining Factors

High Operational Costs Restraints Market Growth

Rising fuel prices and high operational costs pose significant challenges for full-service carriers. Airlines struggle to maintain profitability as fuel expenses soar and maintenance costs increase.

Strict government regulations and rigorous aviation safety standards add further pressure. These requirements force carriers to invest in advanced technology and training.

In addition, competition from low-cost carriers offering budget-friendly travel options intensifies market pressure. Such competitors attract price-sensitive travelers, reducing market share for full-service airlines.

Moreover, global travel demand fluctuates due to economic shifts and geopolitical tensions. Uncertain economic conditions lead to fewer bookings and lower revenues during downturns. Safety concerns and regulatory fines further strain budgets and operational capabilities.

Growth Opportunities

Emerging Market Expansion Provides Opportunities

Airlines find new growth opportunities by expanding into emerging markets with rising air travel demand. Regions in Asia, Africa, and Latin America show strong potential for increased passenger traffic.

Carriers invest in premium cabin upgrades and personalized services to attract high-end travelers. Enhanced comfort, exclusive lounges, and tailored in-flight experiences drive customer loyalty and satisfaction.

In addition, airlines adopt AI and big data tools for predictive maintenance and flight optimization. These advanced systems monitor aircraft performance and reduce delays, resulting in improved efficiency and lower costs.

Loyal customers benefit from well-designed loyalty programs and ancillary revenue streams. Such programs offer rewards, discounts, and added services that encourage repeat travel. Furthermore, airlines use data analytics to understand passenger preferences and refine service offerings.

Emerging Trends

Digital and Sustainable Innovations Are Latest Trending Factor

Airlines are embracing digital and sustainable trends to enhance the travel experience. There is a rising focus on sustainable aviation fuel and carbon neutrality goals.

Carriers invest in cleaner fuel alternatives to reduce emissions and meet environmental targets. AI-powered chatbots and self-service kiosks now provide efficient customer support at airports. These tools streamline check-in processes and improve passenger communication.

In addition, biometric and contactless check-in solutions gain popularity for their speed and security. Such innovations shorten wait times and create smoother travel experiences.

Moreover, airlines are expanding in-flight connectivity and Wi-Fi services to keep passengers connected during flights. Enhanced connectivity offers entertainment and productivity options for travelers.

Digital tools improve operational efficiency and service quality. As a result, passengers enjoy a more personalized and responsive journey. These trending factors reflect the industry’s commitment to modern technology and environmental responsibility.

Regional Analysis

North America Dominates with Major Market Share

North America leads the Full-Service Carrier Market with a major share. This prominence is driven by the region’s strong airline network, high travel demand, and world-class airport infrastructure.

The region benefits from a high frequency of domestic and international flights and a preference for premium travel services among passengers. Additionally, partnerships between airlines for code-sharing and loyalty programs enhance passenger experiences and operational efficiency.

The future influence of North America in the global Full-Service Carrier Market is likely to remain strong. Advances in airline services and growing tourism will continue to fuel market growth, potentially increasing North America’s market share further.

Regional Mentions:

- Europe: Europe holds a key position in the Full-Service Carrier Market, supported by its rich aviation history and strategic airline alliances. The region focuses on high service quality and connectivity, making it a preferred choice for international travelers.

- Asia Pacific: Asia Pacific is rapidly growing in the Full-Service Carrier Market, led by rising middle-class income and increasing air travel in countries like China and India. This growth is supported by expanding airport infrastructure and the introduction of new routes.

- Middle East & Africa: The Middle East and Africa are advancing in the Full-Service Carrier Market due to investments in fleet expansion and luxury services. The regions are becoming important hubs for international travel between the East and the West.

- Latin America: Latin America is developing its presence in the Full-Service Carrier Market, driven by economic improvements and a growing demand for international travel. Improvements in airline offerings and regional connectivity are key to this growth.

Key Regions and Countries Covered in the Report

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Competitive Landscape

In the competitive Full-Service Carrier market, four companies distinguish themselves as industry leaders: American Airlines Group, Delta Air Lines, Inc., United Airlines Holdings, Inc., and Lufthansa Group. These carriers are essential in shaping global air travel dynamics through their extensive networks, service offerings, and market strategies.

American Airlines Group, with its vast domestic and international network, excels in providing extensive flight options and premium services that cater to both business and leisure travelers. Their focus on customer service and operational efficiency helps maintain their market dominance.

Delta Air Lines is known for its reliability, customer service, and technological innovations in the aviation industry. Delta’s investments in biometrics and real-time baggage tracking systems enhance passenger convenience and safety, setting high industry standards.

United Airlines Holdings operates a large domestic and international network, facilitating major global connections. Their commitment to sustainability and the modernization of their fleet with fuel-efficient aircraft positions them as a forward-thinking leader in the sector.

Lufthansa Group, renowned for its operational excellence and premium services, holds a strong position in Europe and beyond. The group’s focus on innovation and passenger comfort in full-service offerings ensures high customer loyalty and international acclaim.

These top full-service carriers not only drive significant traffic in the global airline market but also lead in setting trends for service excellence and technological advancements. Their strategic expansions and upgrades in service quality and efficiency are pivotal as the airline industry continues to evolve, particularly in addressing the challenges of sustainable aviation and digital transformation.

Major Companies in the Market

- American Airlines Group

- Delta Air Lines, Inc.

- United Airlines Holdings, Inc.

- Lufthansa Group

- Air France-KLM

- British Airways (International Airlines Group)

- Emirates

- Qatar Airways

- Singapore Airlines

- Cathay Pacific Airways

- Qantas Airways Limited

- Turkish Airlines

- Japan Airlines Co., Ltd.

Recent Developments

- Ryder and Cardinal Logistics: On February 2024, Ryder System, Inc. bolstered its dedicated transportation solutions by acquiring Cardinal Logistics, a North Carolina-based company. This acquisition aims to enhance Ryder’s supply chain solutions and expand its customer base in the dedicated transportation sector.

- Roadrunner Transportation Systems: On November 2024, Roadrunner Transportation Systems announced a significant shift in ownership, with an investment group led by CEO Chris Jamroz acquiring over 80% of the company. This infusion of capital, amounting to “tens of millions” of dollars, is intended to facilitate mergers and acquisitions, focusing on less-than-truckload (LTL) operations to enhance market presence.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2024) | USD 296.5 Billion |

| Forecast Revenue (2034) | USD 464.9 Billion |

| CAGR (2025-2034) | 4.6% |

| Base Year for Estimation | 2024 |

| Historic Period | 2020-2023 |

| Forecast Period | 2025-2034 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Service Type (Domestic, International), By Flight Class (Economy, Business, First Class), By Aircraft Type (Narrow-body Aircraft, Wide-body Aircraft), By End-User (Leisure Travelers, Business Travelers) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA |

| Competitive Landscape | American Airlines Group, Delta Air Lines, Inc., United Airlines Holdings, Inc., Lufthansa Group, Air France-KLM, British Airways (International Airlines Group), Emirates, Qatar Airways, Singapore Airlines, Cathay Pacific Airways, Qantas Airways Limited, Turkish Airlines, Japan Airlines Co., Ltd. |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |