Quick Navigation

- Report Overview

- Key Statistics

- Key Takeaways

- U.S. Advanced Aerial Mobility Market Size

- Mode of Operations Segment Analysis

- Application Segment Analysis

- Key Market Segments

- Driving Factors

- Restraining Factors

- Growth Opportunities

- Challenging Factors

- Growth Factors

- Latest Trends

- Key Regions and Countries

- Key Players Analysis

- Recent Developments

- Report Scope

Report Overview

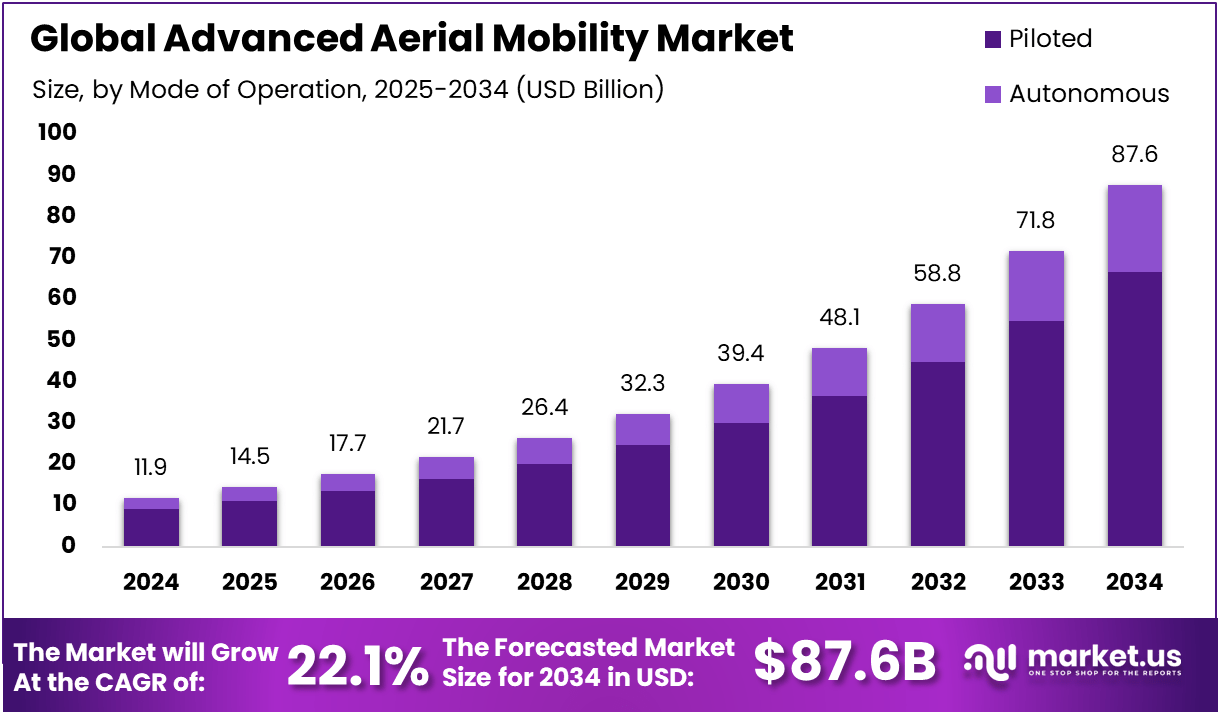

The Global Advanced Aerial Mobility Market size is expected to be worth around USD 87.6 billion by 2034, from USD 11.9 billion in 2024, growing at a CAGR of 22.1% during the forecast period from 2024 to 2033.

Advanced aerial mobility refers to the deployment of urban air mobility vehicles for transporting passengers or cargo, majorly through electric or hybrid vertical take-off and landing (VTOL) aircraft. This includes autonomous or remotely piloted aircraft and aims to improve suburban, urban, and rural transportation.

The market for advanced aerial mobility is growing rapidly due to increasing global traffic congestion, the requirement for a faster mode of transportation, and technological advancements in aerial vehicles. There is also an ongoing investment from market leaders in developing suitable vehicles to enable quick point-to-point air transportation.

Additionally, the growing adoption of eVTOL which serves as an air taxi, advancements in propulsion systems, and development in infrastructures, is reshaping the market by providing huge opportunities for the market.

Key Statistics

Aircraft Production & Deployment

- eVTOL Aircraft in Development: Over 300 different eVTOL (electric Vertical Take-Off and Landing) aircraft designs are currently in development worldwide.

- Projected eVTOL Units by 2030: Estimates vary, but some project over 1,60,000 eVTOL units operating globally by 2030.

- Initial Production Rates: Early production runs for some eVTOL manufacturers are targeting 500-600 aircraft per year, scaling up as demand increases.

Infrastructure & Vertiports

- Estimated Vertiport Cost: Construction costs for a single vertiport can range from $2 million to $10 million, depending on size, location, and features.

- Vertiport Capacity: A typical vertiport might handle 20-30 eVTOL flights per hour during peak times.

- Investment in Vertiport Infrastructure: Billions of dollars are expected to be invested in vertiport infrastructure over the next decade.

Regulations & Safety

- FAA Certification Time: The FAA (Federal Aviation Administration) certification process for new eVTOL aircraft can take 3-5 years (or longer).

- Pilot Training Hours: Specific pilot training requirements for eVTOL aircraft are still being finalized, but are expected to be in the range of 40-60 hours of flight training, plus simulator time.

- Safety Target: The AAM industry is aiming for a safety record that is at least as good as, or better than, that of commercial airlines (which currently have a very low accident rate, measured in accidents per million flight hours).

Key Takeaways

- In 2024, the Piloted segment held a dominant market position, capturing more than a 76.1% share of the Global Advanced Aerial Mobility Market.

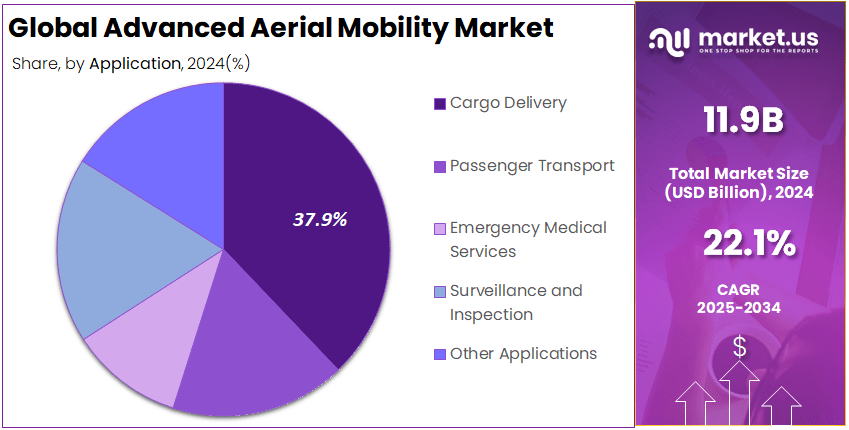

- In 2024, the Cargo Delivery segment held a dominant market position, capturing more than a 37.9% share of the Global Advanced Aerial Mobility Market.

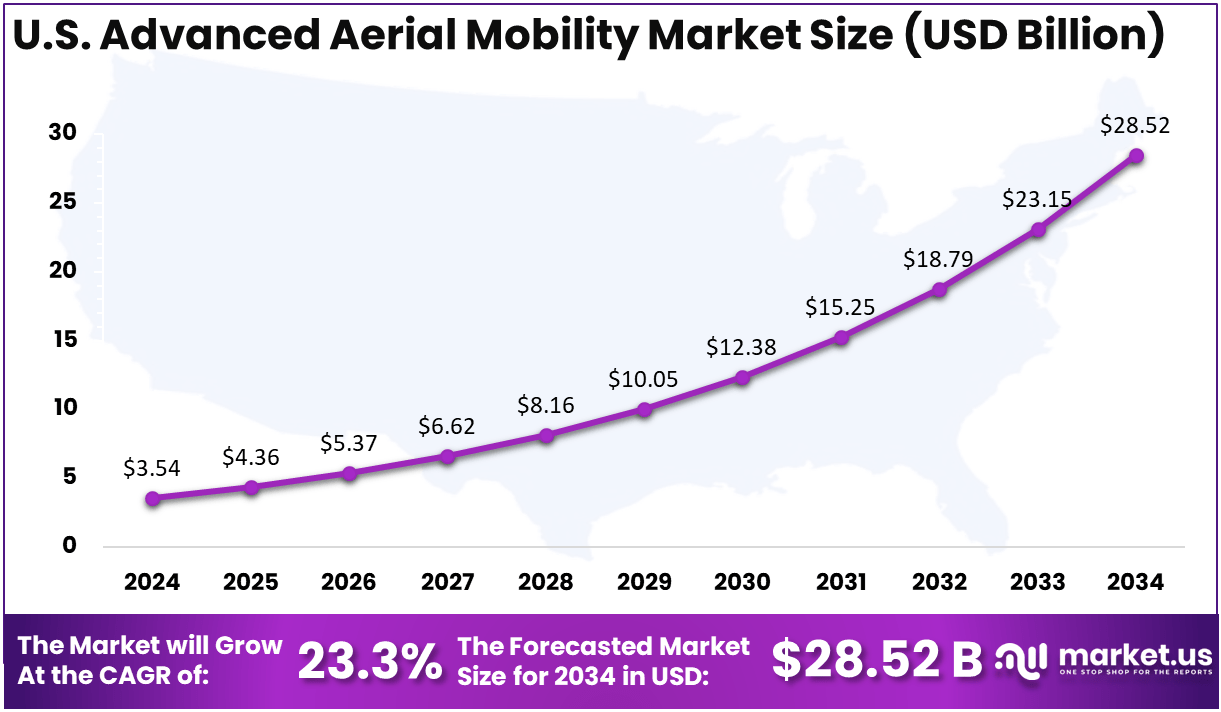

- The US Advanced Aerial Mobility Market was valued at USD 3.54 billion in 2024, with a robust CAGR of 2%.

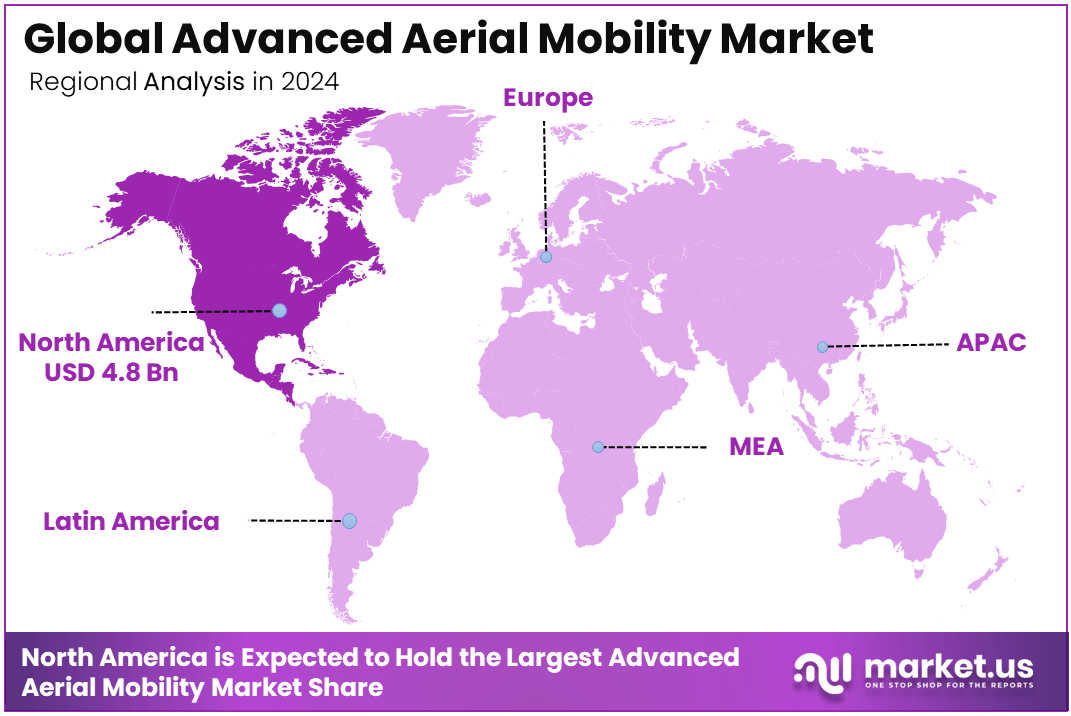

- In 2023, North America held a dominant market position in the global Advanced Aerial Mobility Market, capturing more than a 40.3% share.

- According to gov.uk, Private investment, which includes venture capital, private equity, debt, and post-IPO financing, into advanced aerial mobility-related companies, totaled £8.1 billion, with the UK accounting for approximately 5% of private investment.

- According to volpe.dot.gov, The current order backlog for new advanced aerial mobility aircraft, including electric vertical take-off and landing vehicles, surveillance, and delivery drones includes more than 21,300 aircraft worth an estimated $118 billion. The number of packages delivered by drone increased by more than 80 percent, and 1 million drone deliveries were made in 2023.

U.S. Advanced Aerial Mobility Market Size

The US Advanced Aerial Mobility Market was valued at USD 3.54 billion in 2024, with a robust CAGR of 23.2%. This is majorly due to the growing investments of the U.S. government in supporting advanced aerial mobility through funding, regulatory frameworks, and pilot projects. For instance, the Federal Aviation Administration (FAA) has invested in the certification of electric vertical-take-off-and-landing (eVTOL) aircraft and the creation of drone corridors.

Additionally, the U.S. region is also known for its higher focus on innovations and early adoption of technologies. These actors have contributed to the increasing demand for the market in the U.S. region particularly.

In 2023, North America held a dominant market position in the global Advanced Aerial Mobility Market, capturing more than a 40.3% share. North America has a presence of major key players such as Joby Aviation, Wisk Aero, and others. These companies are at the forefront of developing eVTOL aircraft and related technologies.

Additionally, Advanced aerial mobility technologies are seen as having dual-use applications benefiting both commercial transportation and national defense. This dual-use potential drives future investment and development in the market from the North American region.

Mode of Operations Segment Analysis

In 2024, the Piloted segment held a dominant market position, capturing more than a 76.1% share of the Global Advanced Aerial Mobility Market. Piloted operations are perceived as safer and more reliable, especially in the early stage of advanced aerial mobility technology development. Having a human pilot on board could aid in managing unexpected situations and ensure passenger confidence.

Moreover, regulatory bodies like the Federal Aviation Administration (FAA) have established frameworks that are more accommodating to piloted operations. This makes it easier for companies to get the necessary approvals and certifications for their aircraft.

Application Segment Analysis

In 2024, the Cargo Delivery segment held a dominant market position, capturing more than a 37.9% share of the Global Advanced Aerial Mobility Market. Cargo delivery through aerial mobility offers faster transportation as compared to traditional ground-based methods, especially for urgent or time-sensitive deliveries. Moreover, using aerial routes aids bypass road traffic and congestion, leading to quicker and more reliable delivery times.

Additionally, using aerial mobility for cargo delivery can reduce the carbon footprint by optimizing delivery routes and reducing the reliance on traditional delivery vehicles. There is also a growing demand for rapid delivery services, driven by e-commerce and the need for efficient supply chain solutions, driving the demand for cargo delivery segment in the market.

Key Market Segments

By Mode of Operation

- Piloted

- Autonomous

By Application

- Cargo Delivery

- Passenger Transport

- Emergency Medical Services

- Surveillance and Inspection

- Other Applications

Driving Factors

Increasing Urban congestion

The increasing urban congestion has led to an increasing demand for advanced aerial mobility market. Technologies such as eVTOLs, could bypass ground traffic, offering faster and more direct routes for transportation. This is highly valuable in congested urban areas where travel times can be unpredictable and lengthy.

Furthermore, by taking a portion of the traffic off the roads and into the air, advanced aerial mobility could help reduce overall congestion in cities, leading to smoother traffic flow and less time spent in gridlock. These factors contribute to the overall market growth across the globe.

Restraining Factors

Safety concerns

The potential for accidents, both during take-off, flight, and landing is a major concern for the market. Ensuring the safety and reliability of advanced aerial mobility technologies is paramount to gaining public trust and regulatory approval.

Furthermore, public acceptance of advanced aerial mobility is closely tied to perceived safety. Any incidents or accidents involving Advanced aerial mobility vehicles can significantly impact public trust and acceptance.

Growth Opportunities

Partnerships and collaborations

Partnerships and collaborations allow for the companies to share resources, such as technology, expertise, and funding. This can accelerate the development of advanced aerial mobility technologies and reduce costs.

Collaborations can provide access to new markets and customer bases. For instance, Tata Elxsi has partnered with the CSIR-National Aerospace Laboratories (CSIR-NAL) to develop advanced air mobility technologies. This collaboration focuses on unmanned aerial vehicles (UAVs), urban air mobility (UAM), and electric vertical take-off and landing (eVTOL) aircraft.

Challenging Factors

Lack of Infrastructure

Advanced aerial mobility relies on specialized landing and take-off zones called vertiports. Developing these facilities needs significant investment and urban planning, which can be time-consuming and complex.

Furthermore, many advanced aerial mobility vehicles, especially eVTOLs, require electric charging infrastructure. Developing a network of charging stations that can support the unique requirements of advanced aerial mobility vehicles is essential for widespread adoption.

Growth Factors

Increasing urbanization and traffic congestion drive the need for efficient and fast transportation solutions. Advanced aerial mobility can offer an alternative to ground-based transportation, alleviating congestion and improving urban mobility.

Advanced aerial mobility offers a greener alternative to traditional transportation methods, reducing carbon emissions and noise pollution. This aligns with global efforts to combat climate change and promote sustainable transportation.

Latest Trends

Companies are developing quieter, more efficient electric propulsion systems to extend flight times and reduce noise pollution. This is crucial for regulatory approval and public acceptance. Furthermore, the development of autonomous technologies for advanced aerial mobility vehicles is progressing, aiming to enhance safety and operational efficiency.

Additionally, the development of autonomous technologies for advanced aerial mobility vehicles is progressing, aiming to enhance safety and operational efficiency. It is also expanding into new regions and applications, such as emergency services, logistics, and agriculture.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia

- Netherlands

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Singapore

- Thailand

- Vietnam

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Key Players Analysis

One of the leading players in the market is Volocopter GmbH, a German company that specializes in the development of electric vertical take-off and landing (eVTOL) aircraft. Their flagship product, the Volocopter 2X, is a two-passenger eVTOL that is designed for urban air mobility.

Another prominent player in the market is Wisk Aero LLC, an American company that focuses on developing autonomous eVTOL aircraft. Their most advanced offering is a four-passenger eVTOL air taxi that is designed to be fully autonomous.

Top Key Players in the Market

- Airbus

- Joby Aviation

- Lilium

- EHang

- Volocopter GmbH

- Wisk Aero LLC

- Supernal, LLC

- BETA Technologies

- PIPISTREL

- Eve Air Mobility

- Vertical Aerospace

- Other Key Players

Recent Developments

- In June 2024, Airbus and Avincis, a well-established European helicopter operator, signed a Memorandum of Understanding (MoU) to partner on the development of Advanced Air Mobility (AAM). The companies will collaborate to explore opportunities for operating electric vertical take-off and landing (eVTOL) aircraft throughout Europe.

- In May 2024, Kadet Defence Systems launched India’s first Loitering Aerial Munitions (LAM) under a unique Development cum Production Partner (DCPP) model with the Defence Research and Development Organisation (DRDO). These LAM systems encompass cutting-edge technologies, including Canister Aerial Loitering Munition (CALM), Combat UAVs with stand-off capabilities, and Tactical VTOL UAVs. Kadet has secured a contract to deliver over 50 LAM systems by year-end, meeting the operational requirements of the Indian armed forces.

- In April 2024, IndiGo Airlines’ parent InterGlobe Enterprises reportedly launched electric air taxi services in India by 2026. The airlines’ parent is in the final stages of signing a joint venture (JV) with US-based Archer Aviation to deploy 200 electric vertical takeoffs and landing (eVTOL) aircraft that can carry up to four passengers “just like helicopters”.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2024) | USD 11.9 billion |

| Forecast Revenue (2034) | USD 87.6 billion |

| CAGR (2025-2034) | 22.1% |

| Largest Market | North America |

| Base Year for Estimation | 2024 |

| Historic Period | 2020-2023 |

| Forecast Period | 2025-2034 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Mode of Operation (Piloted, Autonomous), by Application (Passenger Transport, Cargo Delivery, Emergency Medical Services, Surveillance and Inspection, Other Applications), Region |

| Regional Analysis | North America (US, Canada), Europe (Germany, UK, Spain, Austria, Rest of Europe), Asia-Pacific (China, Japan, South Korea, India, Australia, Thailand, Rest of Asia-Pacific), Latin America (Brazil), Middle East & Africa(South Africa, Saudi Arabia, United Arab Emirates) |

| Competitive Landscape | Airbus, Joby Aviation, Lilium, EHang, Volocopter GmbH, Wisk Aero LLC, Supernal, LLC, BETA Technologies, PIPISTREL, Eve Air Mobility, Vertical Aerospace, Other Key Players |

| Customization Scope | We will provide customization for segments and at the region/country level. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |