Global Filling Machine Market Size, Share, And Industry Analysis Report By Product (Rotary, Aseptic, Net Weight, Volumetric), By Mode of Operation (Automatic, Semi-automatic), By Container Type (Bottles, Cans, Pouches and Sachets, Tubes and Cartridges), By Filling Technology (Piston, Gravity, Time-Pressure, Vacuum, Auger), By Application (Beverages, Food, Chemicals, Personal Care, Pharmaceuticals), By Region and Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Statistics, Trends and Forecast 2026-2035

- Published date: March 2026

- Report ID: 181826

- Number of Pages: 290

- Format:

-

keyboard_arrow_up

Quick Navigation

- Report Overview

- Key Takeaways

- By Product Analysis

- By Mode of Operation Analysis

- By Container Type Analysis

- By Filling Technology Analysis

- By Application Analysis

- Key Market Segments

- Emerging Trends

- Drivers

- Restraints

- Growth Factors

- Regional Analysis

- Key Regions and Countries

- Key Players Analysis

- Recent Developments

- Report Scope

Report Overview

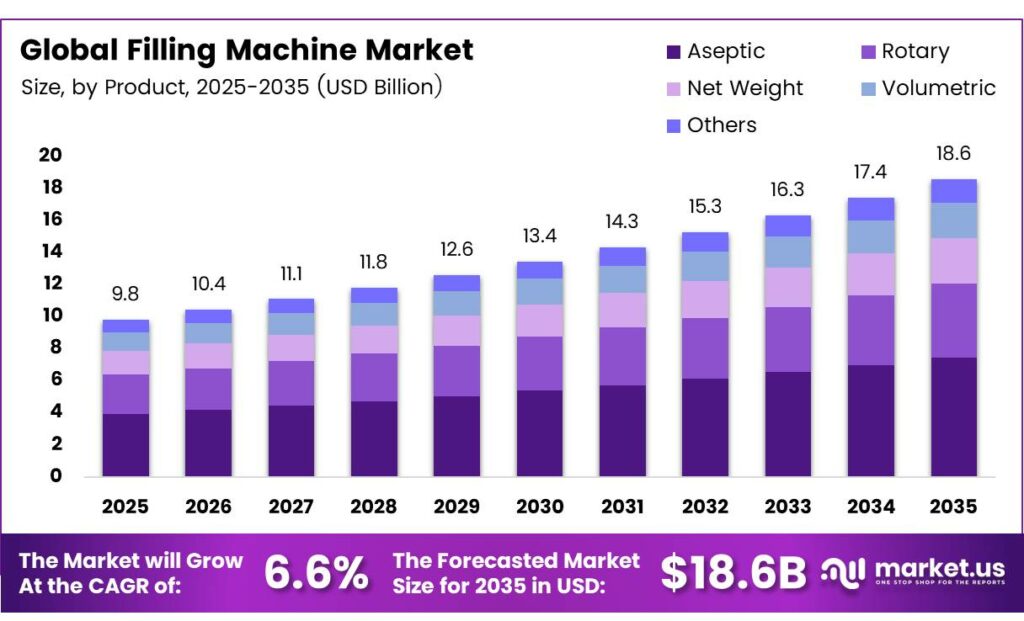

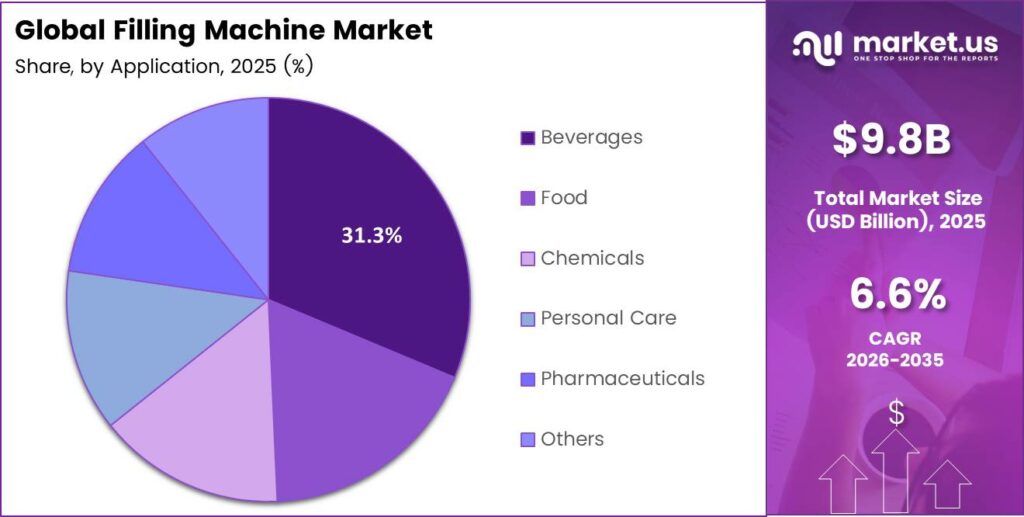

The Global Filling Machine Market size is expected to be worth around USD 18.6 billion by 2035 from USD 9.8 billion in 2025, growing at a CAGR of 6.6% during the forecast period 2026 to 2035.

The filling machine market covers industrial equipment that measures and transfers liquid, semi-liquid, and dry products into containers such as bottles, cans, pouches, vials, and tubes. Moreover, these machines serve a wide range of industries, including food and beverage, pharmaceuticals, personal care, and chemicals. Manufacturers rely on filling equipment to achieve precision, speed, and compliance with hygiene standards.

Filling machines operate across multiple technologies, including piston, gravity, volumetric, time-pressure, and auger systems. Each technology addresses specific product viscosities and container formats. Consequently, manufacturers select equipment based on production volume, product type, and regulatory requirements specific to their industry segment.

Tetra Pak reported net sales of €12,820 million in 2024, while operating with 24,546 employees as of December 2024, demonstrating the immense scale of global liquid-food filling and packaging demand. This scale underscores how large-format filling platforms anchor supply chains across dairy, juice, and beverage sectors worldwide.

Krones AG generated €5.3 billion of revenue in 2024 with €537 million of EBITDA and employed 20,379 people. This performance confirms that filling and packaging technology for beverages and liquid food commands enormous market value. Furthermore, Tetra Pak sold 179 billion packs globally in 2023, reflecting the sheer volume of filling operations executed annually across the world.

Global demand for packaged goods continues to rise sharply across both developed and emerging economies. Urbanization, rising incomes, and consumer preference for ready-to-use products drive consistent investment in filling and packaging infrastructure. Additionally, the pharmaceutical and personal care sectors push demand toward sterile, aseptic, and high-precision filling platforms.

Key Takeaways

- The Global Filling Machine Market is valued at USD 9.8 billion in 2025 and is projected to reach USD 18.6 billion by 2035 at a CAGR of 6.6% during the forecast period 2026 to 2035.

- Rotary filling machines dominate with a 31.6% market share in 2025.

- Automatic filling machines hold the largest share at 71.2% in 2025.

- Bottles lead with a 34.7% share among all container categories.

- Piston technology commands a 27.5% share of the market.

- The Beverages segment holds the top position with a 31.3% share.

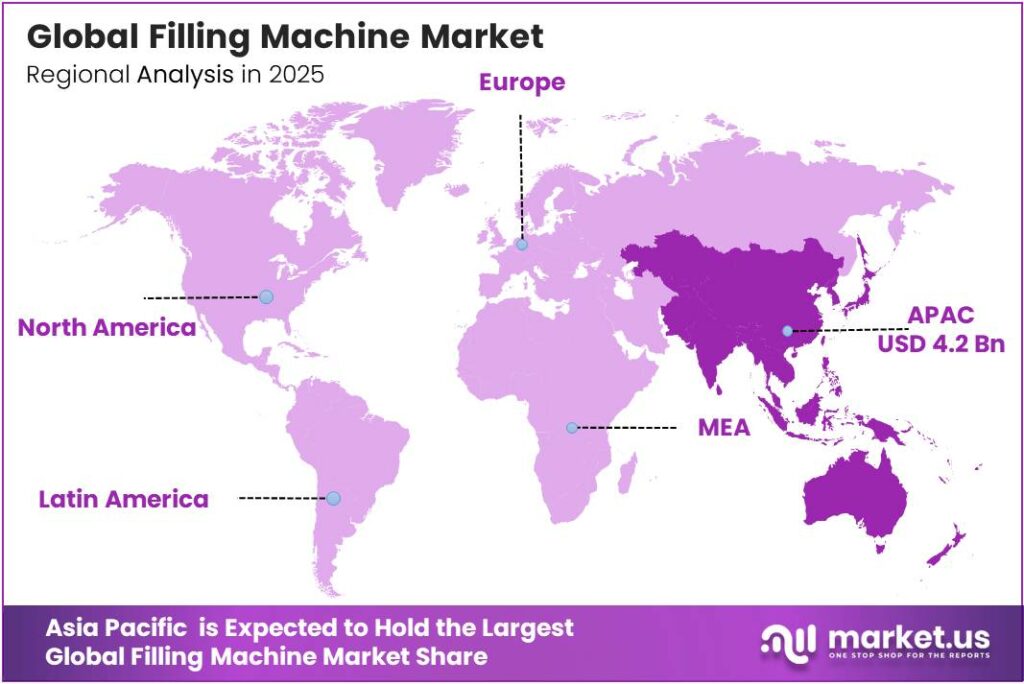

- Asia Pacific dominates the regional landscape with a 43.1% share, valued at approximately USD 4.2 billion.

By Product Analysis

Rotary filling machines dominate with 31.6% due to high-speed multi-station design suited for large-scale production.

In 2025, Rotary filling machines held a dominant market position in the By Product segment of the Filling Machine Market, with a 31.6% share. These machines handle multiple containers simultaneously, enabling high throughput in beverage, dairy, and liquid food operations. Moreover, rotary platforms support quick changeover across container formats, making them the preferred choice for large-scale manufacturers.

Aseptic filling machines serve a critical role in pharmaceutical, dairy, and ready-to-drink beverage applications where sterility is non-negotiable. These systems use sterilized environments and sealed chambers to prevent microbial contamination. Consequently, aseptic equipment commands premium pricing and strong demand from biopharmaceutical manufacturers and high-value food producers globally.

By Mode of Operation Analysis

Automatic filling machines dominate with 71.2% due to superior throughput, precision, and reduced labor dependency in high-volume production environments.

In 2025, Automatic filling machines held a dominant market position in the By Mode of Operation segment of the Filling Machine Market, with a 71.2% share. Manufacturers prefer automatic systems because they deliver consistent fill accuracy, operate at high speeds, and minimize human error. Moreover, automation reduces long-term labor costs while improving overall production efficiency.

Semi-automatic filling machines combine manual intervention with mechanical assistance, making them suitable for small and mid-sized production facilities. These systems require an operator to position containers or initiate fill cycles. However, their lower capital cost and flexible setup make them accessible to contract manufacturers, startups, and producers operating across multiple low-volume product lines.

By Container Type Analysis

Bottles dominate with 34.7% due to widespread use across beverage, personal care, and pharmaceutical applications globally.

In 2025, Bottles held a dominant market position in the By Container Type segment of the Filling Machine Market, with a 34.7% share. Bottles serve as the most universally adopted container format across water, juices, sauces, and personal care products. Additionally, high consumer preference for resealable and portable bottle packaging sustains strong equipment demand.

Cans filling systems serve the rapidly growing carbonated beverage, beer, and energy drink segments. Can-filling lines operate at extremely high speeds and require specialized seaming and pressure-filling technology. Consequently, beverage manufacturers investing in canned product lines drive consistent capital investment in high-speed can-filling infrastructure worldwide.

By Filling Technology Analysis

Piston filling technology dominates with 27.5% due to its accuracy and versatility across viscous and semi-viscous product categories.

In 2025, Piston filling technology held a dominant market position in the By Filling Technology segment of the Filling Machine Market, with a 27.5% share. Piston systems draw product into a cylinder and discharge a precise volume, making them ideal for sauces, creams, and gels. Furthermore, piston technology supports a wide viscosity range, giving manufacturers broad product flexibility.

Gravity filling systems use product weight to control flow into containers, working best with thin, free-flowing liquids such as water, alcohol, and juices. These machines are simple, cost-effective, and low-maintenance. Time-Pressure systems dispense product using timed valve openings under constant pressure, offering fast and consistent performance for mid-viscosity liquids.

By Application Analysis

Beverages dominate with 31.3% due to massive global consumption volumes and ongoing capacity expansions by beverage manufacturers worldwide.

In 2025, Beverages held a dominant market position in the By Application segment of the Filling Machine Market, with a 31.3% share. Global beverage consumption across water, carbonated drinks, juices, and energy drinks sustains massive demand for high-speed filling lines. Moreover, premiumization trends in alcoholic and functional beverages push manufacturers toward advanced aseptic and rotary systems.

Food applications cover sauces, dairy, condiments, edible oils, and ready meals requiring precise and hygienic filling equipment. Strict food safety regulations require manufacturers to invest in certified filling platforms. Chemicals fill serves industrial cleaning, agricultural, and specialty chemical producers needing corrosion-resistant, high-throughput volumetric or gravity systems.

Key Market Segments

By Product

- Rotary

- Aseptic

- Net Weight

- Volumetric

- Others

By Mode of Operation

- Automatic

- Semi-automatic

By Container Type

- Bottles

- Cans

- Pouches and Sachets

- Tubes and Cartridges

- Vials/Syringes

- Others

By Filling Technology

- Piston

- Gravity

- Time-Pressure

- Mass/Flow Meter

- Vacuum

- Auger (Powder)

By Application

- Beverages

- Food

- Chemicals

- Personal Care

- Pharmaceuticals

- Others

Emerging Trends

Robotic and Fully Automated Filling Lines Replace Labor-Intensive Operations

Manufacturers increasingly deploy robotic and fully automated filling lines to reduce dependence on manual labor in high-volume facilities. These systems improve throughput consistency and minimize downtime from human error. Germany exported $3.26 billion of container-filling machinery in 2024, making it the world’s top exporter and demonstrating the scale of demand for advanced automated solutions. Additionally, Tetra Pak operated 51 production plants in 2023, while Sidel maintained 14 plants, reflecting the broad global manufacturing infrastructure supporting these trends.

Multi-Format and Real-Time Monitoring Systems Reshape Production Flexibility

Quick-changeover and multi-format filling systems gain rapid adoption as manufacturers handle increasingly diverse product portfolios and SKU ranges. These platforms allow rapid switching between container types and fill volumes without lengthy downtime. GEA Group’s Liquid and Powder Technologies division generated €1,674 million of revenue in 2024 with a 10.6% EBITDA margin, illustrating the financial scale of liquid-handling demand.

Drivers

Rising Demand for Hygienic Packaged Goods Across Food, Beverage, and Personal Care Sectors

Consumer demand for hygienically packaged food, beverage, and personal care products continues to grow strongly across global markets. Urbanization and changing lifestyles accelerate purchases of ready-to-use and single-serve packaged goods. Furthermore, the expansion of biopharmaceutical production creates an urgent need for advanced sterile and aseptic filling equipment, directly expanding the addressable market for high-precision filling platforms.

Automation Adoption and Regulatory Compliance Accelerate Equipment Investment

Manufacturers worldwide implement advanced automation technologies to boost throughput and reduce operational waste across filling lines. These investments deliver measurable gains in production efficiency and quality consistency. Syntegon raised order intake to €1.8 billion in 2024, signaling strong pipeline demand driven by compliance and automation-linked equipment procurement.

Restraints

High Capital Costs Limit Market Access for Small-Scale Manufacturers

Filling machines, particularly automated and aseptic systems, require substantial upfront capital investment that small and medium-scale manufacturers often struggle to finance. Ongoing maintenance, calibration, and spare parts costs add to total ownership expenses. Consequently, smaller producers in developing markets frequently delay equipment upgrades or continue using outdated filling systems that limit their production capacity and product quality potential.

Integration Complexity and Specialized Expertise Create Operational Barriers

Integrating new filling equipment into existing production lines presents significant technical challenges for many manufacturers. Modern filling systems require specialized engineering expertise for installation, calibration, and ongoing troubleshooting. Moreover, the shortage of trained technical staff in emerging markets amplifies integration risk, increasing project timelines and costs. Therefore, these barriers slow adoption rates, particularly among cost-sensitive producers operating in price-competitive industries.

Growth Factors

Pharmaceutical Fill-Finish Demand and Sustainable Packaging Drive New Investment Cycles

Booming contract fill-finish services in pharmaceuticals create strong demand for scalable and modular filling systems that meet GMP and aseptic standards. Biologic drugs, vaccines, and injectable therapies require specialized high-precision equipment. OPTIMA Packaging Group’s revenue reached €800 million in 2024, up 20% year over year, demonstrating the momentum of this investment cycle.

Asia-Pacific Industrialization and Smart Manufacturing Unlock Long-Term Market Potential

Rapid industrialization and urbanization across Asia-Pacific markets generate new manufacturing capacities in food, beverage, and consumer goods. These regions represent the fastest-growing demand pool for both entry-level and advanced filling systems. Moreover, the emergence of smart manufacturing integrating IoT-enabled filling machines enhances process optimization, real-time quality control, and predictive maintenance capabilities.

Regional Analysis

Asia Pacific Dominates the Filling Machine Market with a Market Share of 43.1%, Valued at USD 4.2 Billion

Asia Pacific leads the global filling machine market with a dominant 43.1% share, valued at approximately USD 4.2 billion in 2025. The region’s massive food processing, beverage, and pharmaceutical manufacturing base drives consistent equipment demand. Moreover, rapid urbanization across China, India, and Southeast Asia fuels new production facility investments.

North America maintains a strong and mature filling machine market supported by large-scale food, beverage, and pharmaceutical industries. Manufacturers in the region prioritize automation, precision, and compliance with FDA and other regulatory standards. Additionally, rising demand for flexible and aseptic packaging solutions encourages investment in advanced high-speed filling systems across the United States and Canada.

Europe holds a significant position in the global filling machine market, anchored by world-class machinery manufacturing in Germany and Italy. The region’s advanced industrial base supports strong domestic demand and large export volumes. Furthermore, stringent EU food safety and pharmaceutical regulations drive continuous equipment upgrades among regional manufacturers, sustaining steady replacement and modernization demand.

The Middle East and Africa region presents a growing demand for filling equipment driven by expanding beverage, food processing, and consumer goods industries. Infrastructure development programs and foreign investment in manufacturing support capacity additions. Moreover, beverage and packaged food growth across Gulf Cooperation Council countries and sub-Saharan Africa creates new opportunities for both rotary and volumetric filling platforms.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

Barry-Wehmiller Companies, Inc. operates as a diversified global supplier of manufacturing technology and services, with a strong presence in filling and packaging equipment through its subsidiary brands. The company focuses on delivering engineered solutions for the beverage, food, and consumer goods industries. Moreover, its customer-centric approach and broad service network support long-term client relationships across multiple regions and production scales.

Ronchi Mario S.P.A. specializes in the design and manufacture of liquid filling and capping machines for personal care, cosmetics, pharmaceutical, and food industries. The company’s Italian engineering heritage supports precision-focused product development across diverse container formats. Furthermore, Ronchi Mario’s modular machine architecture enables customers to configure lines suited to both small-batch and high-volume production environments efficiently.

KHS Group delivers comprehensive filling and packaging solutions for the beverage, food, and non-food industries with a strong emphasis on sustainability and energy efficiency. The company offers rotary fillers, aseptic lines, and complete turnkey production systems. Additionally, KHS Group continuously invests in digital and smart manufacturing capabilities, enabling clients to integrate connected filling platforms into modern, data-driven production environments.

Accutek Packaging Equipment Companies, Inc. manufactures a broad portfolio of filling, capping, labeling, and conveying equipment serving pharmaceutical, cosmetic, food, and chemical industries. The company provides both standard and custom-engineered solutions for customers ranging from startup operations to established large-scale manufacturers. Consequently, Accutek’s flexible product range and accessible pricing position it as a strong option across diverse market segments.

Top Key Players in the Market

- Barry-Wehmiller Companies, Inc.

- Ronchi Mario S.P.A.

- KHS Group

- Accutek Packaging Equipment Companies, Inc.

- Gea Group AG

- Tetra Laval International S.A.

- Krones AG

- JBT Corporation

- Coesia S.P.A.

Recent Developments

- In 2025, BW Packaging integrated its BW Filling & Closing, BW Flexible Systems, and BW Integrated Systems divisions into a single unified organization under the BW Packaging brand. The move unifies over 2,000 team members and product lines (including filling and closing equipment from brands such as Angelus, Hayssen, Pneumatic Scale, and Hema) to deliver fully integrated packaging solutions and lifetime aftermarket support.

- In 2025, KHS USA announced a two-phase expansion of its Brookfield, Wisconsin headquarters, adding approximately 24,000 sq ft of new office space and a 65,000 sq ft manufacturing facility with up to 45 additional workstations to support increased production of filling and packaging equipment.

Report Scope

Report Features Description Market Value (2025) USD 9.8 Billion Forecast Revenue (2035) USD 18.6 Billion CAGR (2026-2035) 6.6% Base Year for Estimation 2025 Historic Period 2020-2024 Forecast Period 2026-2035 Report Coverage Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments Segments Covered By Product (Rotary, Aseptic, Net Weight, Volumetric, Others), By Mode of Operation (Automatic, Semi-automatic), By Container Type (Bottles, Cans, Pouches and Sachets, Tubes and Cartridges, Vials/Syringes, Others), By Filling Technology (Piston, Gravity, Time-Pressure, Mass/Flow Meter, Vacuum, Auger (Powder)), By Application (Beverages, Food, Chemicals, Personal Care, Pharmaceuticals, Others) Regional Analysis North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East & Africa (GCC, South Africa, and Rest of MEA) Competitive Landscape Barry-Wehmiller Companies Inc., Ronchi Mario S.P.A., KHS Group, Accutek Packaging Equipment Companies Inc., Gea Group AG, Tetra Laval International S.A., Krones AG, JBT Corporation, Coesia S.P.A. Customization Scope Customization for segments and region/country levels will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited Users and Printable PDF)

-

-

- Barry-Wehmiller Companies, Inc.

- Ronchi Mario S.P.A.

- KHS Group

- Accutek Packaging Equipment Companies, Inc.

- Gea Group AG

- Tetra Laval International S.A.

- Krones AG

- JBT Corporation

- Coesia S.P.A.

Our Clients

- 181826

- March 2026