Quick Navigation

Report Overview

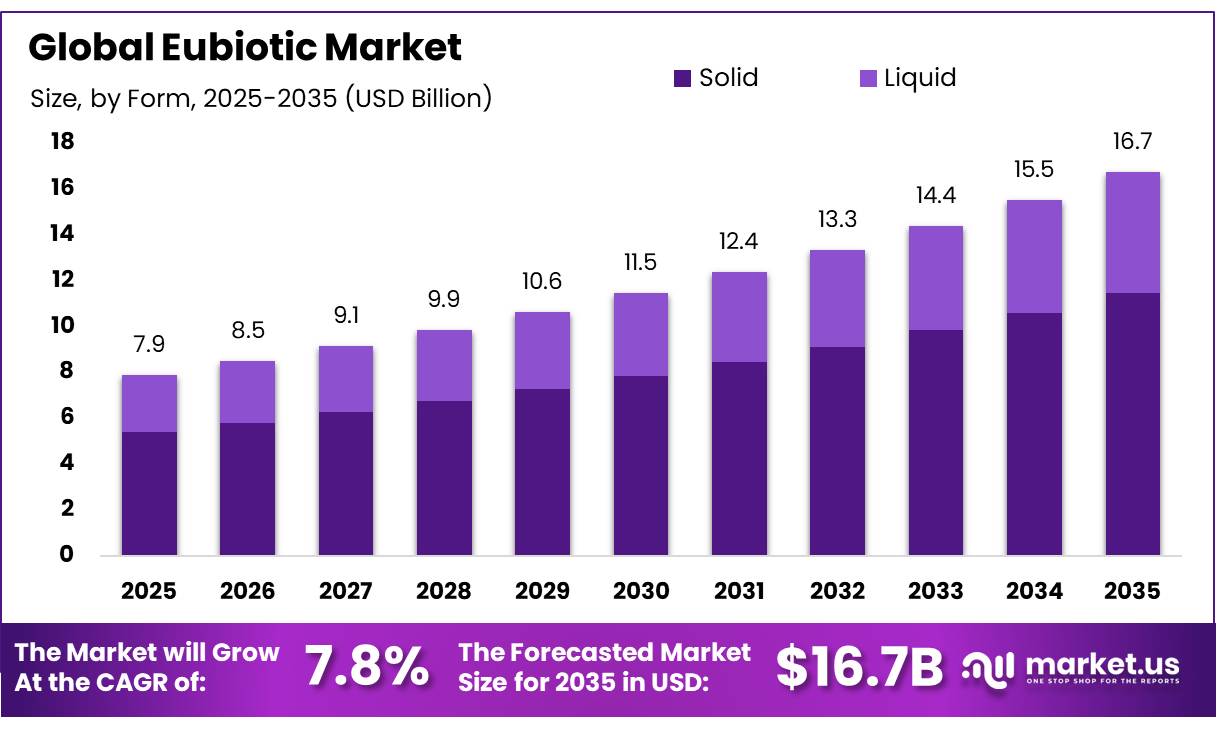

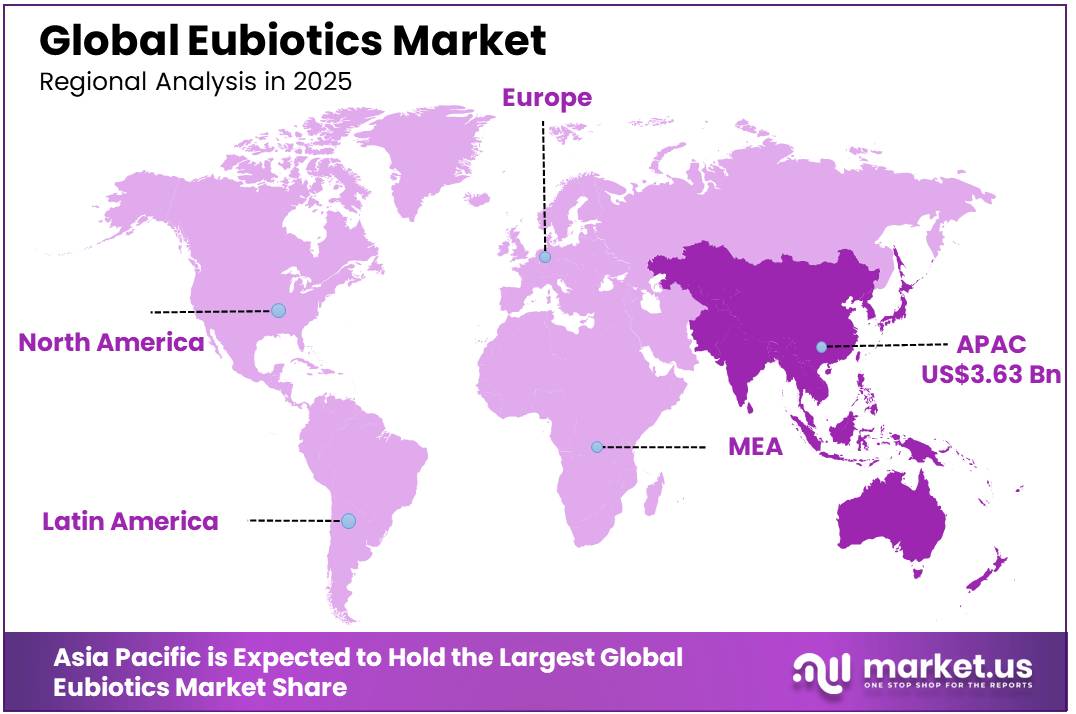

In 2025, the Global Eubiotics Market was valued at USD 7.9 billion, and between 2026 and 2035, this market is estimated to register a CAGR of 7.8%, reaching about USD 16.7 billion by 2035. Asia Pacific held a dominant market position, capturing more than a 46.1% share, holding USD 3.63 billion in revenue.

Eubiotics are feed and nutrition additives designed to support a balanced microbial environment in the gastrointestinal tract of livestock and aquaculture species. The category includes probiotics, prebiotics, organic acids, essential oils, enzymes, and other natural growth-promoting ingredients that enhance animal health, feed efficiency, and productivity. The industry has gained significant importance as livestock producers increasingly seek alternatives to antibiotic growth promoters while maintaining animal performance and food safety standards.

- Global livestock and animal protein production also supports demand for eubiotics. According to FAO’s Food Outlook, global meat production reached 373 million tonnes in 2024, up 1.4% from 2023, with growth led mainly by poultry and bovine meat. As poultry, swine, cattle, and aquaculture production expands, feed producers are using eubiotics to improve digestion, feed efficiency, gut balance, and animal performance.

Key Takeaways

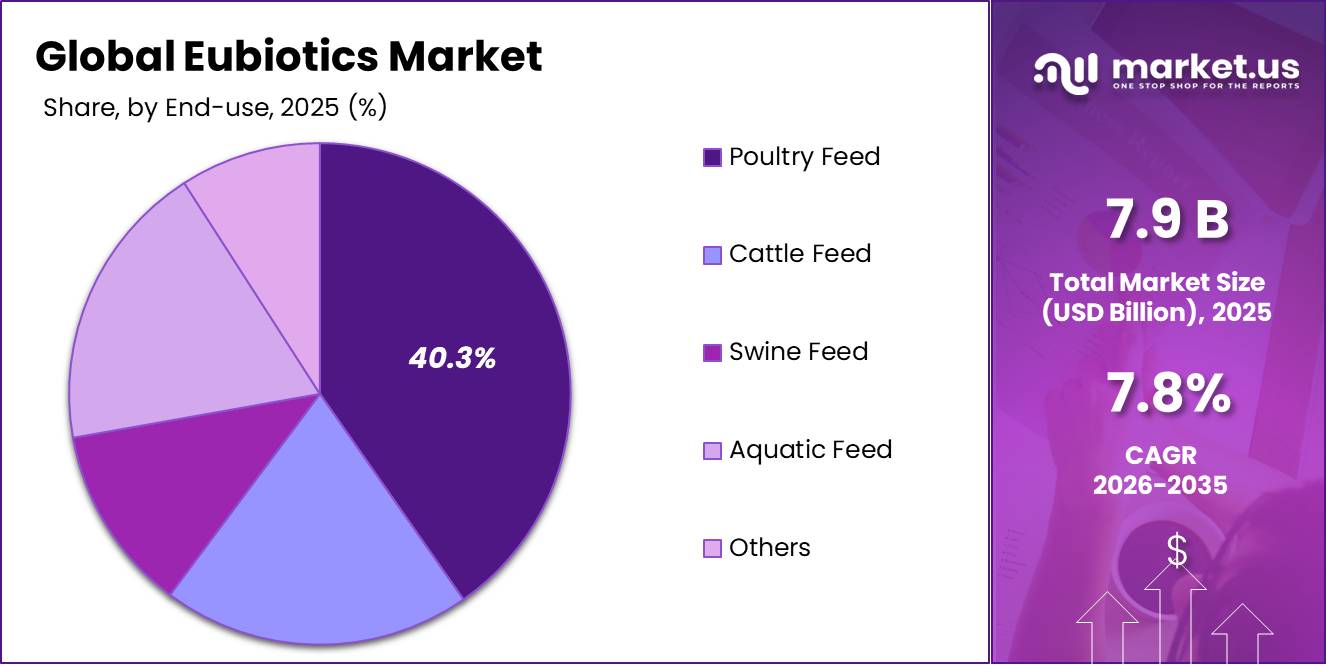

- The Global Eubiotics Market was valued at USD 7.9 billion in 2025.

- The market is projected to grow at a CAGR of 7.8% and is estimated to reach USD 16.7 billion by 2035.

- On the basis of products, Probiotics hold the largest market share by product at 40.5%.

- Solid formulations dominate the market with a 68.4% share, significantly outperforming liquids.

- On the basis of application, Gut Health is the leading application, accounting for 38.6% of the market.

- Poultry Feed represents the largest consumer segment, driving 40.3% of the market share.

- The Asia Pacific region is the global leader, commanding 46.1% of the total market.

The industry is shifting from simple feed additives to advanced precision farming methods that use technology. The use of AI, especially through tools like predictive microbiome analysis, automated feed design systems, and real-time gut monitoring, is speeding up the creation of highly targeted synbiotic mixes. This is greatly improving how efficiently animals convert feed into growth and making eubiotics a key part of modern animal farming practices.

Eubiotics Market Segmentation

Product Analysis

Probiotics represents dominant Segment in the Market.

Probiotics make up 40.5% of the revenue in the global eubiotics market. This strong position is because Bacillus spores can survive high temperatures used in making animal feed, allowing them to work effectively in the lower part of the digestive system. The market leadership is also supported by using mixtures of different probiotic strains like Lactobacilli, Bifidobacterium, and Streptococcus. These strains work together to ensure that the probiotics can still function well even if some strains don’t survive.

Combining probiotics, prebiotics, and plant-based ingredients into “smart” mixtures is the fastest-growing trend in animal feed. Rather than using a single component, companies are blending these ingredients together to improve animal gut health more effectively. Scientists now use AI and microbiome sequencing to tailor these blends for specific animals and farming situations. This technology has reduced the time it takes to develop these products from five years to under 24 months.

Form Analysis

Solid is a significant form in Eubiotics Market.

Solid formulations are dominant in the eubiotics market, holding 68.4% of the industry’s share. This segment leads the market due to its longer shelf life, which lasts between 18 to 36 months, much better than the 6 to 12 months of liquid options. Technologies such as advanced beadlets protect the active ingredients from heavy mechanical stress and high pelleting temperatures up to 90°C. This strong stability makes it easy to mix in industrial ribbon blenders, allows smooth pneumatic transport, and ensures dependable nutrient delivery. Because of these benefits, dry forms have become the standard in automated feed production for poultry, swine, and ruminant animals.

Liquid formulations are expected to grow the fastest, which is faster than the growth of solid formulations. This growth is mainly because more farms are using automated systems for adding these products to water in poultry operations and in aquaculture, where using liquid is essential due to the way water is used. The main reason for this growth is the use of smart farming equipment like automatic dosing devices, water lines that can measure and deliver the right amount, and tools that track how much is consumed. New technologies, such as spraying the product onto feed after it’s been formed into pellets, are also making it easier to use liquid products in more places.

End Use Analysis

Eubiotics Are Mostly Utilized in the Poultry Feed.

The biggest part of the eubiotics market comes from poultry feed, which takes in about 40.3% of the total revenue. This is because for a long time, people have been using eubiotics as a replacement for antibiotics in raising broiler chickens and egg-laying hens. On average, about 500 grams of eubiotics are added for every metric ton of feed to help improve how efficiently the chickens convert feed into meat or eggs. This segment is the main part of the market because farmers can see a quick return on their investment due to the short time it takes to raise broiler chickens, which is between 35 to 42 days.

The aquatic feed category will experience the fastest growth until 2035. As aquaculture grows to offer more than half of worldwide fish volume, producers are using specific eubiotics to improve nutritional digestion and disease resistance in salmon and shrimp. Antibiotic-free laws are driving the integration of multi-strain probiotics (such as Bacillus) to balance gut microbiota and prevent fatal disease outbreaks. Advances in aquatic encapsulation technology guarantee that these functional additions survive water-soluble administration, hence increasing survival rates.

Application Analysis

Eubiotics Are the Most Widely Used for Gut Health.

Gut health is the biggest use of eubiotics in the market, making up 38.6% of the industry. This area is leading because improving the health of the digestive system helps increase the height of the tiny finger-like structures in the intestines, which makes it easier for animals to absorb nutrients and prevents harmful bacteria from moving into the body. These changes help reduce sickness and the cost of treating animals, while also helping them gain weight steadily even in different farming environments. Also, because many countries have banned the use of antibiotics to help animals grow, maintaining a healthy gut naturally has become essential.

The immunity segment is growing the fastest in the eubiotics market. This quick growth is because of the connection between the gut and the immune system, as 70% of an animal’s immune cells are located in the gut. Now farmers are using yeast-based eubiotics to boost the natural immunity of livestock. This proactive method helps stop harmful bacteria like Salmonella, which is important for meeting high global food safety rules.

Key Market Segments

By Product

- Probiotics

- Lactobacilli

- Bifidobacterum

- Streptococcus

- Others

- Prebiotics

- Fructo-oligosaccharides (FOS)

- Inulin

- Galacto-Oligosaccharides (GOS)

- Mannan-Oligosaccharides (MOS)

- Others

- Organic Acids

- Phytogenic

- Others

By Form

- Liquid

- Solid

By Application

- Gut Health

- Immunity

- Yield

- Others

By End Use

- Cattle Feed

- Poultry Feed

- Swine Feed

- Aquatic Feed

- Others

Driver Analysis

AMR-control driven replacement of antibiotic growth promoters

FAO explicitly identifies feed ingredients and additives such as enzymes, competitive exclusion products, probiotics, prebiotics, acidifiers, plant extracts, essential oils, and yeast as options to substitute antibiotics as growth promoters, while also noting global livestock antimicrobial consumption at 63,151 tonnes in 2010, which shows the scale of the addressable replacement pool still embedded in animal production systems.

Adoption momentum is already visible at field level: in a 2025 FAO/Codex-linked report on Pakistan’s poultry sector, 60.8% of respondents considered probiotics the most effective antimicrobial alternative, 21.7% cited organic acids, and 60.8% reported using alternatives prophylactically rather than therapeutically, indicating that eubiotics are moving upstream into routine flock management rather than remaining a niche treatment adjunct.

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| AMR-control driven replacement of antibiotic growth promoters with probiotics, acids, enzymes, and phytogenics | +2.4% | EU core, North America core, China and South Asia adoption corridors, Latin America spill-over | Short term (≤ 2 years) |

| Feed-cost optimization and feed-conversion pressure in poultry and swine production | +1.9% | North America core, EU, Brazil-linked export chains, APAC intensive farming belts | Short term (≤ 2 years) |

| Faster microorganism validation and regulatory confidence for microbial feed additives | +1.4% | EU core, UK-aligned Europe, North America premium segments, APAC regulated import markets | Medium term (2-4 years) |

| Biosecurity, disease-prevention, and resilience investment after recurring animal-health shocks | +1.6% | North America dairy and poultry, EU livestock systems, East Asia intensive farms | Short term (≤ 2 years) |

| Shift toward preventive nutrition in organized poultry and aquaculture value chains | +1.3% | South Asia, Southeast Asia, China, Middle East poultry hubs | Medium term (2-4 years) |

| Organic and residue-sensitive animal production raising demand for non-antibiotic gut-health inputs | +0.9% | EU core, North America premium retail channels, Oceania, high-value export chains | Long term (≥ 4 years) |

Restraint Analysis

Feed-cost inflation crowding out additives

The first restraint is the compression of on-farm and integrator purchasing power caused by volatile feed economics, because eubiotics are usually sold as a value-enhancing inclusion but still compete for budget against energy, protein, medication, and working-capital needs; in 2026, feed buyers are navigating higher soybean and soymeal expectations in major agricultural outlooks, while India’s poultry chain has already seen soybean meal move from about USD 0.59/kg to USD 0.74/kg within roughly one month, a 25% jump that directly raises ration cost and weakens willingness to trial premium gut-health programs unless payback is visible within one production cycle.

Quantitatively, when total feed cost inflates by high-single-digit to low-double-digit percentages, an additive package representing only 0.5% to 2.0% of feed cost can still be cut or downgraded if expected feed conversion ratio improvement is uncertain, which translates into delayed reformulations, reduced inclusion rates, and stronger buyer insistence on price guarantees, thereby creating margin compression for additive suppliers and a modeled drag of about 1.4 percentage points on market CAGR in cost-sensitive poultry and swine systems.

Restraint Impact Analysis

| Restraint | (~) % Impact on CAGR | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Feed-cost inflation crowding out additives | -1.4% | APAC core, LatAm, North America poultry belts | Short term (≤ 2 years) |

| Regulatory approval and reauthorization drag | -1.1% | EU core, North America, selected APAC import markets | Medium term (2-4 years) |

| Disease shocks reducing herd and flock placements | -0.9% | EU, North America, East Asia poultry corridors | Short term (≤ 2 years) |

| Logistics and ingredient lead-time volatility | -0.8% | EU-APAC lanes, Middle East, India import channels | Medium term (2-4 years) |

| Price-performance pressure in low-margin farming | -1.0% | India, Southeast Asia, Africa, LatAm | Medium term (2-4 years) |

| Trade and tariff distortion on additive inputs | -0.6% | US-China lanes, EU imports, India specialty inputs | Medium term (2-4 years) |

Opportunity Analysis

Integrated antibiotic-reduction bundles

This is distinct from a normal driver because reduced antibiotic use already supports baseline demand, but the untapped upside comes from packaging eubiotics with biosecurity protocols, vaccination support, diagnostics, and performance guarantees into a measurable “antibiotic-reduction as a service” offer rather than selling isolated additives; FAO highlights that antimicrobial reduction depends on a broad system including hygiene, welfare, vaccination, and feed additives, which creates a monetizable gap for integrated programs rather than single-product transactions.

The value pool is large because only 42 countries were noted by FAO as having livestock antimicrobial-use data systems, while global livestock antimicrobial consumption was estimated at 63,151 tonnes in 2010 and future usage growth is expected to skew heavily toward animal production, particularly pigs and poultry, implying significant room for commercial solutions that reduce treatment dependence and improve measurable outcomes. Using literature indicating Bacillus-based probiotics can reduce post-weaning diarrhea in pigs by 30% and broiler mortality by 6% to 8%, suppliers that bundle eubiotics with flock or herd management protocols could plausibly capture 3% to 5% price premiums and 15% to 20% higher share of wallet per account, producing an incremental $250 million to $500 million global revenue opportunity and about +2.1 percentage points of CAGR upside in the EU, North America, and export-oriented Southeast Asian production systems over a 2- to 4-year execution horizon.

Opportunity Impact Analysis

| Opportunity | (~) % Potential CAGR | Geographic Relevance | Execution Window |

|---|---|---|---|

| Precision eubiotics platforms | +1.9% | North America core, EU, China, Brazil | Short term (≤ 2 years) |

| Aquaculture gut-health expansion | +1.6% | APAC, Latin America, Nordics | Medium term (2-4 years) |

| Pet microbiome premiumization | +1.4% | North America core, EU, Japan, South Korea | Short term (≤ 2 years) |

| Integrated antibiotic-reduction bundles | +2.1% | EU, North America, Southeast Asia | Medium term (2-4 years) |

| Portfolio roll-up and channel consolidation | +1.7% | Global, with EU and North America core | Short term (≤ 2 years) |

| Regulatory fast-follow specialty enzymes | +1.3% | EU, UK, Gulf, advanced APAC | Long term (≥ 4 years) |

Challenges Analysis

Strain Efficacy Variability

Eubiotics remain biologically attractive, but the market’s first major challenge is that performance is highly strain-, species-, ration-, and farm-condition-specific, which means the same probiotic, acidifier, or phytogenic program can deliver a 2 to 4 point feed-conversion improvement in one broiler system yet underperform by 0.5 to 1.5 points in another when temperature stress, pathogen load, water quality, or feed-mill pelleting intensity shift outside validated conditions; this variability is amplified because probiotics are now a large component of the category, with one source placing them at 40.4% of eubiotics revenue in 2025, while industrial feed systems still demand repeatable economics lot after lot.

In practical terms, even a 3% to 5% coefficient of variation in live performance can erase 15 to 35 basis points of producer margin in poultry and post-weaning swine programs, forcing suppliers to spend more on localized trials, multi-strain reformulation, encapsulation, shelf-life stabilization, and technical service teams rather than pure volume scaling. The result is an estimated -1.2% drag on market CAGR potential in 2026 because buyers delay full-portfolio conversion until suppliers can prove narrower efficacy bands across heat, pathogen, and feed-form scenarios, making the strategic response less about selling more product and more about building strain libraries, digital performance benchmarking, and species-specific evidence stacks that reduce biological outcome dispersion over the next 2 to 4 years.

Challenges Impact Analysis

| Challenge | (~) % CAGR Friction | Geographic Relevance | Mitigation Horizon |

|---|---|---|---|

| Strain Efficacy Variability | -1.2% | North America core, EU regulatory hubs, APAC intensive livestock belts | Medium term (2-4 years) |

| Dossier Compliance Burden | -0.9% | EU regulatory hubs, UK, export-aligned APAC markets | Medium term (2-4 years) |

| Fermentation Input Volatility | -1.0% | APAC production bases, Latin America importers, EU formulation centers | Short term (≤ 2 years) |

| Farm-Level Performance Dispersion | -1.1% | India, Southeast Asia, Latin America, Africa growth markets | Long term (≥ 4 years) |

| Regional Supply Concentration | -0.8% | APAC logistics corridors, Latin America, Middle East, Africa | Medium term (2-4 years) |

| Antibiotic-Free Transition Complexity | -1.4% | EU swine and poultry, India, China, Brazil, North America poultry | Long term (≥ 4 years) |

Geopolitical Impact Analysis

War economies are changing how the eubiotics supply chain works. The disruptions happening are actually helping to increase demand, acting as a catalyst for growth in this area.

The Russia-Ukraine war, now in its fourth year, has been the biggest geopolitical event affecting the eubiotics market in recent history. It has both increased costs and boosted demand. Russia and Ukraine together supply about 30% of the world’s wheat and 15% of corn, which are important ingredients for making organic acids. When the Black Sea trade routes were disrupted in 2022, the cost of these ingredients went up.

Also, Russia’s control over natural gas before the war made energy prices for fermentation and drying processes in Europe rise by 60 to 80%, which squeezed profits for companies like DSM-Firmenich, Novozymes, Chr. Hansen, and Lesaffre. When Western companies like Evonik left the market, it removed 30,000 tonnes of methionine supply each year. This unexpected situation pushed Russia to increase its own eubiotic production, with the government giving over 700 million euros a year to support local manufacturing.

In March 2025, a ban on prophylactic antibiotics created a new demand for alternatives in Russia. Attacks on ships in the Red Sea added 10 to 14 days to shipping times between Asia and Europe, making it harder to keep probiotics alive during transport. Because of this, the industry has started to use more stable spore-forming bacteria like Bacillus.

Regional Analysis

Asia Pacific Held the Largest Share of Eubiotics Market.

The Asia-Pacific region is the main leader in the global market, holding 46.1% of the share. This is because of India and China, which together have over 2.8 billion people. The growing population and increasing middle-class incomes are leading to a big rise in the demand for meat, dairy, and seafood. Because of this huge amount of consumption, along with new strict rules like China’s ban on using antibiotics to help animals grow, the poultry and fish farming supply chains in the region have quickly become more industrialized.

North America is an established, high-value section of the worldwide eubiotics industry. Stable population levels and stringent regulatory control, including FDA requirements, encourage the use of modern synbiotic and multifunctional feed solutions. Large-scale livestock integrators invest in high-quality formulations including multi-strain probiotics and phytogenic fractions to improve animal comfort, reduce antimicrobial resistance (AMR) risk, and achieve consistent feed efficiency and FCR metrics. Cost sensitivity is reduced due to enterprise-scale economics, enabling for the rapid adoption of cutting-edge eubiotic solutions.

Key Regions and Countries Covered

- North America

- The US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia & CIS

- Rest of Europe

- APAC

- China

- Japan

- South Korea

- India

- ASEAN

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

The eubiotics market displays a moderately consolidated, tier-structured oligopolistic behavior, where a small group of multinational chemical and life-sciences giants exert substantial control. The top five global suppliers, collectively command 43.8% of total industry revenue. This dominant tier maintains its market stronghold through intense capital concentration.

The core financial value is anchored by the top oligopoly, these smaller players survive by catering to localized livestock preferences and specific regional regulatory frameworks, particularly across emerging markets. However, as global supply chains tighten and large food retailers increasingly mandate standardized, antibiotic-free production, this fragmented tier faces intense pressure.

The Major Players In The Industry

- BASF SE

- Cargill, Incorporated

- ADM

- DSM

- Novus International, Inc.

- UAS Laboratories

- Lallemand, Inc.

- Calpis Co., Ltd.

- Advanced BioNutrition Corp

- BENEO

- BEHN MEYER

- Lesaffre Group

- Kemin Industries, Inc.

- DuPont de Nemours, Inc.

- Novozymes

- Other Key Players

Key Development

- In September 2025, ADM signed a definitive agreement with Alltech to create a North American animal feed joint venture, expected to launch in Q1 2026. ADM will contribute 11 U.S. feed mills, while Alltech will bring its Hubbard Feeds business, strengthening feed solutions and eubiotic-linked nutrition services.

- In June 2025, Lesaffre received a positive EFSA scientific opinion for Microsaf, its bacteria-based probiotic for chickens and other poultry for fattening. This supported future EU commercialization and strengthened Lesaffre’s probiotic eubiotics pipeline.

Report Scope

| Report Features | Description |

|---|---|

| Report Features | Description |

| Market Value (2025) | USD 7.9 Bn |

| Forecast Revenue (2035) | USD 16.7 Bn |

| CAGR (2026-2035) | 7.8% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Product (Probiotics, Prebiotics, Organic Acids, Phytogenic, Others), By Form (Liquid, Solid), By Application (Gut Health, Immunity, Yield, Others), By End Use (Cattle Feed, Poultry Feed, Swine Feed, Aquatic Feed, Others), By Region and Companies – Industry Segment Outlook, Market Assessment, Competition Scenario, Trends and Forecast 2025-2035 |

| Regional Analysis | North America – The US & Canada; Europe – Germany, France, The UK, Spain, Italy, Russia & CIS, Rest of Europe; APAC– China, Japan, South Korea, India, ASEAN & Rest of APAC; Latin America– Brazil, Mexico & Rest of Latin America; Middle East & Africa– GCC, South Africa, & Rest of MEA |

| Competitive Landscape | BASF SE, Cargill Incorporated, ADM, DSM, Novus International Inc., UAS Laboratories, Lallemand, Inc., Calpis Co. Ltd., Advanced BioNutrition Corp, BENEO, BEHN MEYER, Lesaffre Group, Kemin Industries, Inc., DuPont de Nemours, Inc., Novozymes, Other Key Players |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited Users and Printable PDF) |