Quick Navigation

Report Overview

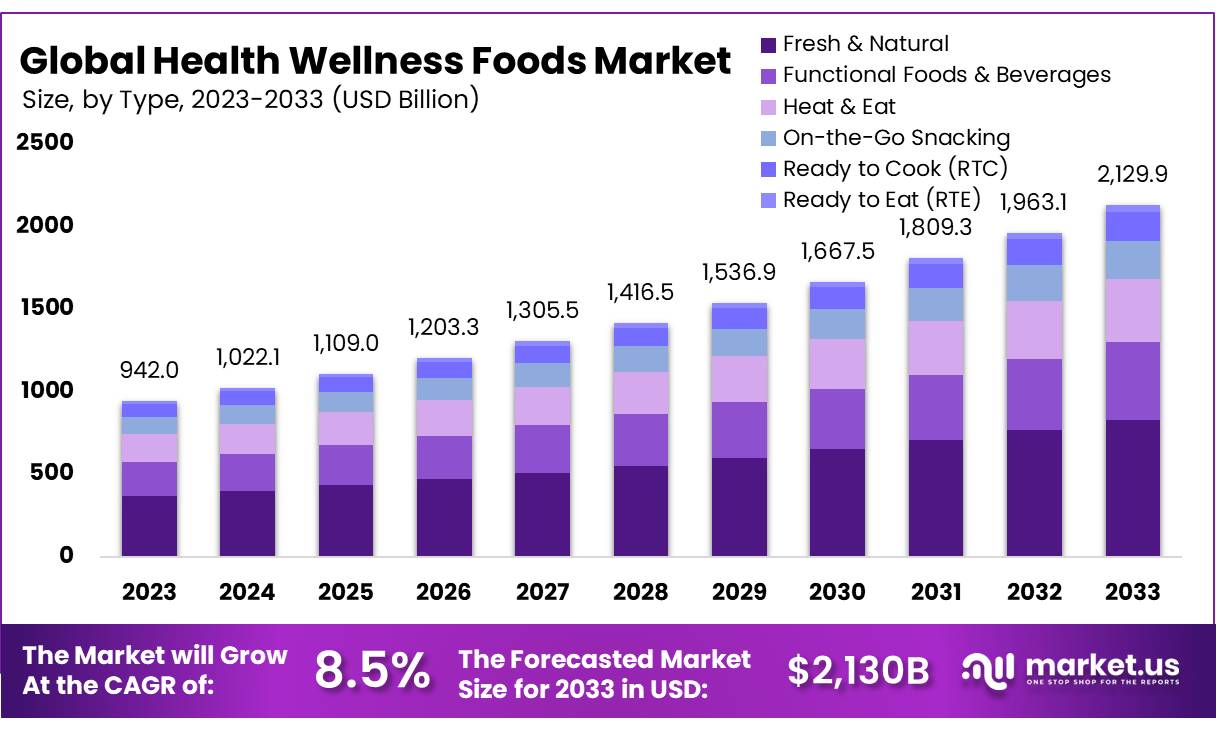

The Global Health Wellness Foods Market size is expected to be worth around USD 2129.9 Bn by 2033, from USD 942.04 Bn in 2023, growing at a CAGR of 8.5% during the forecast period from 2024 to 2033.

The Global Health and Wellness Foods Market is witnessing substantial growth, fueled by heightened consumer awareness of the integral relationship between nutrition and overall health. This market encompasses a wide array of products, including functional foods, organic items, fortified snacks, plant-based alternatives, and dietary supplements, tailored to address various consumer health concerns such as cardiovascular health, digestive support, immunity enhancement, and weight management. As modern lifestyles shift towards preventive healthcare, this sector has emerged as a key area for innovation and strategic investments.

The prevalence of chronic diseases such as diabetes, obesity, and cardiovascular ailments has intensified demand for healthier dietary options. In 2023, nearly 39% of global consumers actively avoided high-sugar products, while 28% prioritized items labeled as organic. The organic food segment, valued at approximately $227 billion in 2023, continues to grow as consumers favor non-GMO and chemical-free food options, reflecting a clear alignment with clean-label trends.

Key growth drivers include demographic, economic, and cultural transformations. Urbanization, coupled with rising disposable incomes in emerging markets, has fueled the demand for premium, health-centric foods. Regions like Asia-Pacific, with its expanding middle-class population, are emerging as lucrative markets for health and wellness products. Additionally, the global pandemic significantly heightened consumer focus on immune health, spurring a surge in demand for products enriched with vitamins C and D, zinc, and probiotics. Notably, sales of probiotic-enriched foods experienced a 12% year-on-year increase in 2022, underlining the growing preference for gut-health solutions.

Furthermore, the rise of personalized nutrition, enabled by advancements in biotechnology and AI-driven health analytics, is catering to individualized dietary requirements, further broadening market opportunities.

The market’s growth trajectory is poised to remain strong, driven by increasing access to under-served regions and innovations in sustainable food production. Consumers are gravitating towards brands that emphasize transparent sourcing and eco-friendly practices, compelling companies to adopt green technologies and sustainable manufacturing processes. The expansion of direct-to-consumer (DTC) models and e-commerce channels is also accelerating market penetration, especially in areas with growing digital adoption. As these dynamics continue to evolve, the health and wellness foods market is set for sustained growth over the coming decade.

Key Takeaways

- Health Wellness Foods Market size is expected to be worth around USD 2129.9 Bn by 2033, from USD 942.04 Bn in 2023, growing at a CAGR of 8.5%.

- Functional Foods & Beverages segment held a dominant position in the Health Wellness Foods Market, capturing more than a 38.4% share.

- Non-Genetically Modified Organism (Non-GMO) Food captured a dominant market position within the Health Wellness Foods Market, securing over a 74.3% share.

- Low Fat segment held a dominant market position in the Health Wellness Foods Market, capturing more than a 54.2% share.

- Conventional foods held a dominant position in the Health Wellness Foods Market, capturing more than a 65.2% share.

- Gluten-Free category held a dominant market position in the Health Wellness Foods Market, capturing more than a 28.4% share.

- Weight Management segment held a dominant position in the Health Wellness Foods Market, capturing more than a 34.3% share.

By Type

In 2023, the Functional Foods & Beverages segment held a dominant position in the Health Wellness Foods Market, capturing more than a 38.4% share. This segment includes products that are fortified with additional vitamins, minerals, and other beneficial substances to offer health benefits beyond basic nutrition. Products like probiotic drinks, fortified breakfast cereals, and energy bars are typical in this category, catering to consumers seeking dietary support for health and wellness goals.

Other significant segments include Fresh & Natural, which emphasizes whole, unprocessed foods that align with a clean eating trend, and On-the-Go Snacking, which offers convenient, health-oriented snacks tailored for busy lifestyles. The Heat & Eat, Ready to Cook (RTC), and Ready to Eat (RTE) categories also continue to grow, driven by consumer demand for convenience combined with health consciousness. These products range from pre-packaged meals that require minimal preparation to snacks and dishes that are ready to consume immediately, supporting the needs of time-strapped consumers looking for quick and healthy eating options.

By Nature

In 2023, Non-Genetically Modified Organism (Non-GMO) Food captured a dominant market position within the Health Wellness Foods Market, securing over a 74.3% share. This considerable market share reflects a growing consumer preference for foods perceived as natural and safer, aligning with broader health and environmental concerns. Non-GMO foods are favored for their lack of genetic modifications, which appeals to consumers seeking pure and organic dietary choices.

Genetically Modified Organism (GMO) Food constitutes the remainder of the market, catering to sectors where enhanced crop durability and yield are crucial. Despite technological advantages, GMO foods face consumer skepticism regarding their health and environmental impacts, limiting their prevalence in the health wellness sector. As we move into 2024, the trend towards non-GMO foods is likely to strengthen, driven by continuing consumer demand for transparency and natural ingredients in their food choices.

By Fat Content

In 2023, the Low Fat segment held a dominant market position in the Health Wellness Foods Market, capturing more than a 54.2% share. This preference is driven by the widespread consumer perception that low-fat foods are healthier and assist in managing weight and reducing the risk of chronic diseases. Low-fat products range from dairy items, like milk and yogurt, to snacks and prepared meals, catering to a broad audience seeking healthier dietary options.

The No Fat and Reduced-Fat segments also play significant roles in the market, each catering to specific consumer needs and preferences. No Fat foods are often chosen by those on strict dietary regimes or with specific medical conditions requiring fat intake management, while Reduced-Fat foods offer a balance, reducing fat content without compromising taste or texture too significantly. As health consciousness continues to rise, these segments are expected to grow, reflecting ongoing consumer interest in dietary health and wellness.

By Category

In 2023, Conventional foods held a dominant position in the Health Wellness Foods Market, capturing more than a 65.2% share. This segment includes mainstream food products that are not specifically labeled as organic. Despite growing interest in organic products, conventional foods remain popular due to their affordability and wide availability. These products meet the basic regulatory standards for health and safety without the additional organic certifications, making them accessible to a broader range of consumers.

The Organic category, though smaller, is gaining traction, driven by consumer perceptions of higher quality and environmental benefits. Organic foods are produced under stringent conditions with no synthetic pesticides or fertilizers, appealing to health-conscious consumers looking for natural and environmentally friendly eating options. As awareness and availability of organic products increase, this segment is expected to grow, reflecting a shift in consumer preferences towards more sustainable and health-conscious diets.

By Free From Category

In 2023, the Gluten-Free category held a dominant market position in the Health Wellness Foods Market, capturing more than a 28.4% share. This segment caters to consumers with celiac disease, gluten intolerance, or those who choose to avoid gluten for lifestyle reasons. Gluten-free products range from breads and pastas to snacks and ready meals, reflecting a growing consumer demand for foods that support digestive health and wellness.

The Free From category include Artificial Color-Free, Artificial Flavor-Free, Lactose-Free, Nut-Free, Soy-Free, and Sugar-Free products. Each of these segments addresses specific dietary needs and preferences, with consumers increasingly seeking out foods that eliminate common allergens or unwanted additives. This trend is driven by a growing awareness of food sensitivities and a general shift towards cleaner eating.

By Application

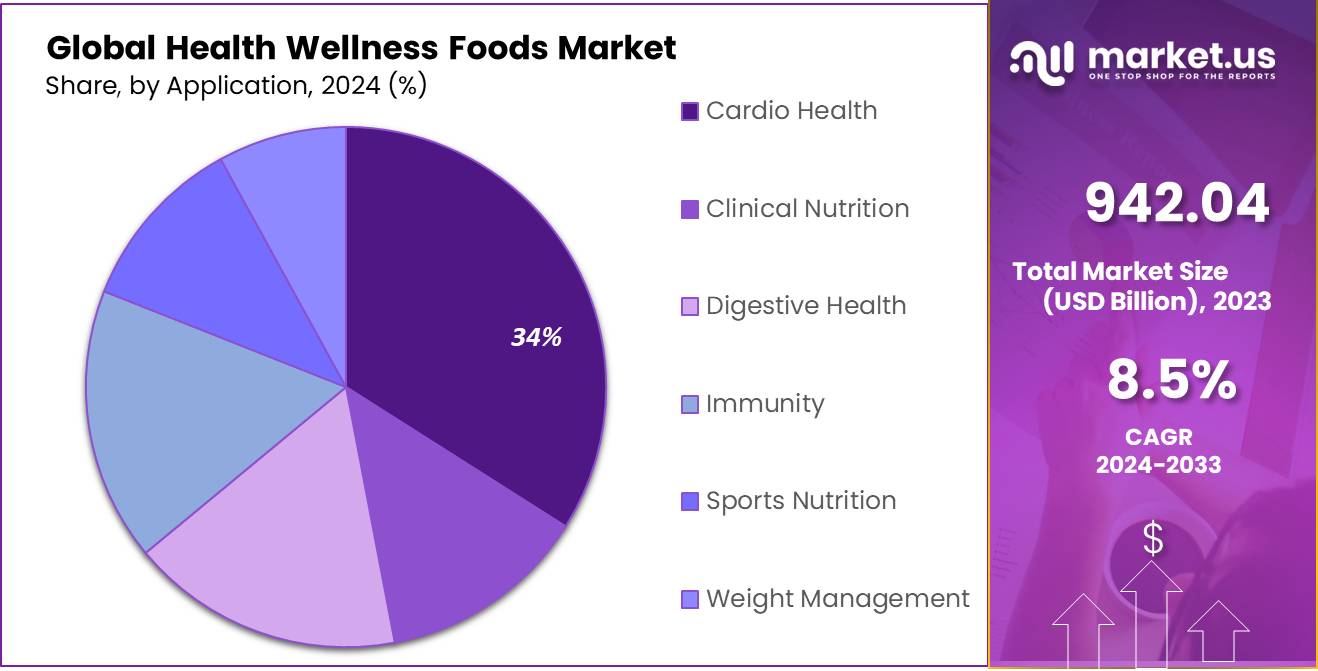

In 2023, the Weight Management segment held a dominant position in the Health Wellness Foods Market, capturing more than a 34.3% share. This sector caters to consumers aiming to lose, manage, or maintain their weight through dietary choices. Products in this segment typically include meal replacements, low-calorie snacks, and fortified nutritional products designed to enhance satiety and reduce caloric intake.

Cardio Health, which focuses on foods beneficial for heart health, and Digestive Health, offering products like probiotics and fiber-rich foods that promote gut well-being. The Immunity segment has also seen growth, with an increased demand for foods enhanced with vitamins and minerals to support immune system function. Sports Nutrition and Clinical Nutrition continue to evolve, driven by specific needs for athletic performance and medical dietary requirements, respectively. Each of these segments addresses distinct health concerns, reflecting the diverse needs and preferences of health-conscious consumers.

By Distribution Channel

In 2023, Supermarkets & Hypermarkets held a dominant market position in the Health Wellness Foods Market, capturing more than a 44.4% share. This channel remains the most accessible and preferred option for consumers purchasing health and wellness foods, offering a wide variety of products under one roof.

Online Mode is rapidly growing, reflecting the increasing consumer preference for convenience and the rise of e-commerce platforms that offer competitive pricing and home delivery. Pharmacies & Drugstores also play a critical role, especially for clinically oriented nutrition products, while Convenience Stores cater to on-the-go consumers looking for quick and healthy snacking options. Each distribution channel supports the unique shopping preferences and lifestyles of health-conscious consumers, contributing to the diverse landscape of the market.

Key Market Segments

By Type

- Fresh & Natural

- Functional Foods & Beverages

- Heat & Eat

- On-the-Go Snacking

- Ready to Cook (RTC)

- Ready to Eat (RTE)

By Nature

- Genetically Modified Organism Food

- Non-Genetically Modified Organism Food

By Fat Content

- Low Fat

- No Fat

- Reduced-Fat

By Category

- Conventional

- Organic

By Free From Category

- Artificial Color-Free

- Artificial Flavor-Free

- Gluten-Free

- Lactose-Free

- Nut-Free

- Soy-Free

- Sugar-free

By Application

- Cardio Health

- Clinical Nutrition

- Digestive Health

- Immunity

- Sports Nutrition

- Weight Management

By Distribution Channel

- Convenience Stores

- Pharmacies & Drugstores

- Supermarkets & Hypermarket

- Online Mode

- Others

Drivers

Increasing Awareness and Demand for Functional Foods

One of the primary driving factors for the Health Wellness Foods market is the increasing consumer awareness of and demand for functional foods. These foods are enhanced with nutrients or beneficial ingredients that offer specific health benefits beyond basic nutrition. According to industry reports, the functional foods segment has seen significant growth, driven by rising health consciousness among consumers worldwide.

Governments and health organizations are also promoting the benefits of healthier eating habits, supporting the growth of this market. For instance, initiatives like the USDA’s MyPlate, which emphasizes fruit, vegetable, and whole grain consumption, underline the importance of nutritious diets. This governmental support is crucial as it helps raise awareness about the link between diet and health, encouraging consumers to make more informed food choices.

Moreover, with the ongoing global health challenges, there has been a sharp increase in consumer interest in foods that support immune health, weight management, and chronic disease management. This shift is reflected in the growing popularity of products enriched with vitamins, minerals, antioxidants, and fibers, which are perceived to offer protective benefits against health issues.

The demand for these functional and health-enhancing foods is expected to continue rising, driven by health trends and supported by innovation in food technologies that make these products more effective and appealing to health-conscious consumers.

Restraints

High Cost and Accessibility Issues

A significant restraining factor in the Health Wellness Foods market is the high cost of these products compared to conventional food items. Health and wellness foods often involve more expensive ingredients, advanced production technologies, and rigorous certification processes, all of which contribute to higher retail prices. This price disparity can make health-oriented foods less accessible to lower-income consumers, limiting the market’s growth potential.

Additionally, there is often a lack of availability in certain regions, particularly in rural or underserved urban areas, where supermarkets and health food stores are less prevalent. This accessibility issue is compounded in countries with less developed retail infrastructures, where distribution channels for specialized health and wellness products are not as well established.

Governmental and non-governmental organizations are aware of these barriers and have been working to promote better access to healthy food options through various initiatives. For example, some regions offer subsidies for local organic farmers or incentives to retailers to stock healthier food options in economically disadvantaged areas.

Opportunity

Expansion into Plant-Based and Alternative Protein Products

A major growth opportunity within the Health Wellness Foods market lies in the expanding sector of plant-based and alternative protein products. Consumer demand for plant-based foods is soaring, driven by factors like health concerns, environmental awareness, and ethical considerations regarding animal welfare. According to industry analysts, the global plant-based food market is expected to grow exponentially, with projections suggesting a multi-billion dollar increase by the end of the decade.

This trend is supported by significant innovations in food technology that have improved the taste and texture of plant-based products, making them more appealing to a broader audience, including those who do not follow a strictly vegetarian or vegan diet. Moreover, governmental health organizations worldwide are encouraging dietary shifts towards more plant-based foods due to their benefits for health and the environment.

The rise in flexitarian diets, where consumers predominantly eat vegetarian food but occasionally consume meat, also opens new avenues for growth. Manufacturers are increasingly developing and marketing a wider range of plant-based options to cater to this diverse consumer base, from plant-based dairy alternatives to meat substitutes and beyond.

This segment’s growth is facilitated by increasing investments from both new startups and established food companies aiming to capitalize on the plant-based trend. These developments promise significant expansion opportunities for the Health Wellness Foods market, positioning plant-based and alternative protein products as key drivers of future growth.

Trends

Integration of Superfoods into Daily Diets

A significant trend in the Health Wellness Foods market is the growing incorporation of superfoods into everyday diets. Superfoods, rich in vitamins, minerals, antioxidants, and other essential nutrients, are gaining traction due to their health benefits, which include enhancing immunity, reducing inflammation, and potentially lowering the risk of chronic diseases. Consumers are increasingly aware of the nutritional value of foods like berries, nuts, seeds, and ancient grains, and are incorporating them not just in meals but also in snacks and beverages.

This trend is supported by both health experts and dietary guidelines that recommend diverse and nutrient-rich food intake for overall health improvement. Food manufacturers are responding by expanding their product lines to include ingredients known for their health benefits, such as matcha, spirulina, and turmeric, which are being used in everything from functional drinks to breakfast foods and snacks.

Regional Analysis

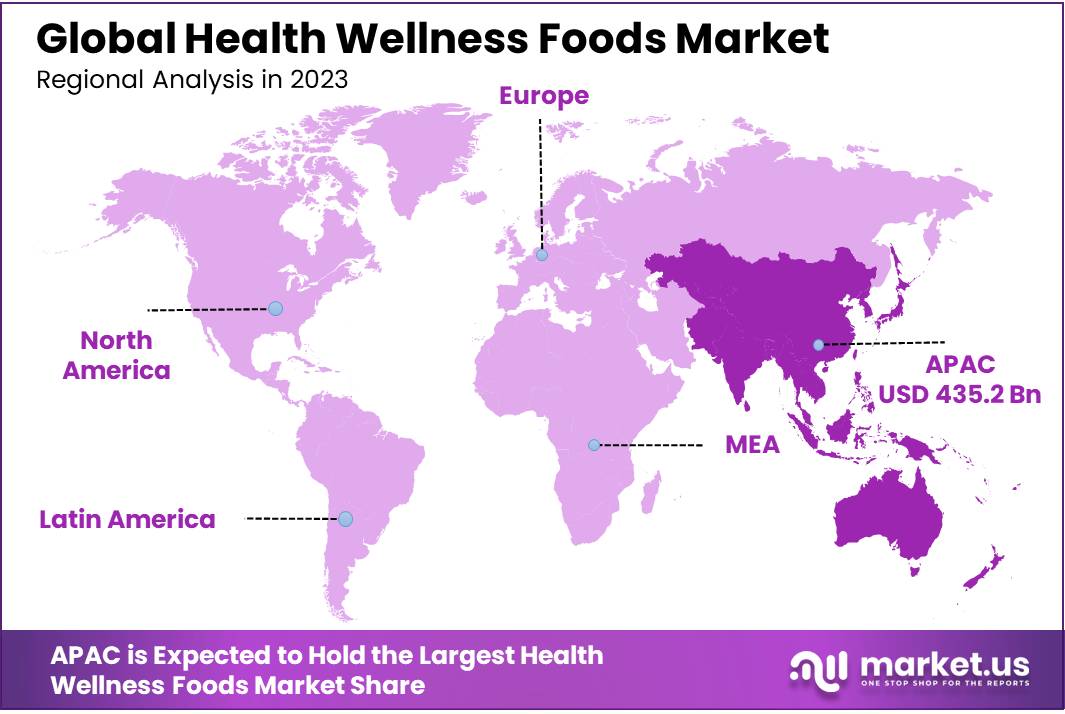

In 2023, the Asia Pacific (APAC) region dominated the Health Wellness Foods market, holding a substantial 46.9% share and generating revenues of USD 435.2 billion. This dominance is driven by a growing middle-class population with increased disposable income and rising health consciousness, particularly in countries like China, India, and Japan. Consumers in these areas are increasingly demanding healthier food options, which has spurred local and international companies to expand their health-focused product offerings in the region.

North America and Europe also hold significant shares in the market, supported by well-established health and wellness trends and high consumer awareness about the benefits of healthy eating. In these regions, organic and non-GMO products are particularly popular, reflecting a broader consumer preference for natural and environmentally sustainable food options.

Latin America and the Middle East & Africa, while smaller in market share, are experiencing rapid growth in demand for health wellness foods. This growth is fueled by urbanization, rising health awareness, and increasing economic stability, which are encouraging the adoption of healthier lifestyles. As these regions continue to develop, the potential for market expansion remains significant, driven by changing consumer preferences and increasing health-related education.

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Key Players Analysis

The Health Wellness Foods market is shaped by key players who are driving innovation and addressing the increasing global demand for healthier food options. Nestlé SA leads the industry with its diversified portfolio of health-focused products, ranging from infant nutrition to functional foods.

The company’s emphasis on research and development enables it to create products tailored to evolving consumer needs, such as plant-based alternatives and nutrient-enhanced offerings. Similarly, Fonterra Co-operative Group Limited plays a significant role, leveraging its expertise in dairy nutrition to produce health-centric ingredients and solutions for both consumers and industrial clients.

Top Key Players

- Nestlé S.A.

- Danone S.A.

- PepsiCo Inc.

- General Mills Inc.

- Kraft Heinz Company

- Mondelez International Inc.

- GlaxoSmithKline PLC

- Abbott Laboratories

- Herbalife Nutrition Ltd.

- Archer Daniels Midland Company

- Chobani Global Holdings LLC

- Clif Bar & Company

- Dairy Farmers of America Inc.

- Glanbia PLC

- Yakult Honsha Co., Ltd.

Recent Developments

Asha Ram & Sons Pvt. Ltd. is recognized as a Great Place to Work in India, reflecting its commitment to employee satisfaction and a positive work environment.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2023) | USD 942.0 Bn |

| Forecast Revenue (2033) | USD 2129.9 Bn |

| CAGR (2024-2033) | 8.5% |

| Base Year for Estimation | 2023 |

| Historic Period | 2020-2022 |

| Forecast Period | 2024-2033 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Type (Fresh and Natural, Functional Foods and Beverages, Heat and Eat, On-the-Go Snacking, Ready to Cook (RTC), Ready to Eat (RTE)), By Nature (Genetically Modified Organism Food, Non-Genetically Modified Organism Food), By Fat Content (Low Fat, No Fat, Reduced-Fat), By Category (Conventional, Organic), By Free From Category (Artificial Color-Free, Artificial Flavor-Free, Gluten-Free, Lactose-Free, Nut-Free, Soy-Free, Sugar-free), By Application (Cardio Health, Clinical Nutrition, Digestive Health, Immunity, Sports Nutrition, Weight Management), By Distribution Channel (Convenience Stores, Pharmacies and Drugstores, Supermarkets and Hypermarket, Online Mode, Others) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA |

| Competitive Landscape | Nestlé S.A., Danone S.A., PepsiCo Inc., General Mills Inc., Kraft Heinz Company, Mondelez International Inc., GlaxoSmithKline PLC, Abbott Laboratories, Herbalife Nutrition Ltd., Archer Daniels Midland Company, Chobani Global Holdings LLC, Clif Bar & Company, Dairy Farmers of America Inc., Glanbia PLC, Yakult Honsha Co., Ltd. |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |